Even though his statements have been bearish, he has had all sorts of holdings. I would have gladly been along for that ride.

17 Likes

Well, it’s a bit touch and go. They seem to be operating with quite a lot of leverage and risk, and the comparison point is probably price return S&P ![]()

5 Likes

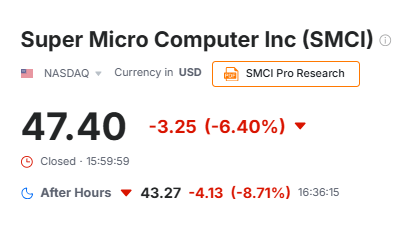

This current AI company (a former barbecue charcoal company) can still rise into the green even on a stock market downturn day like this ![]()

26 Likes

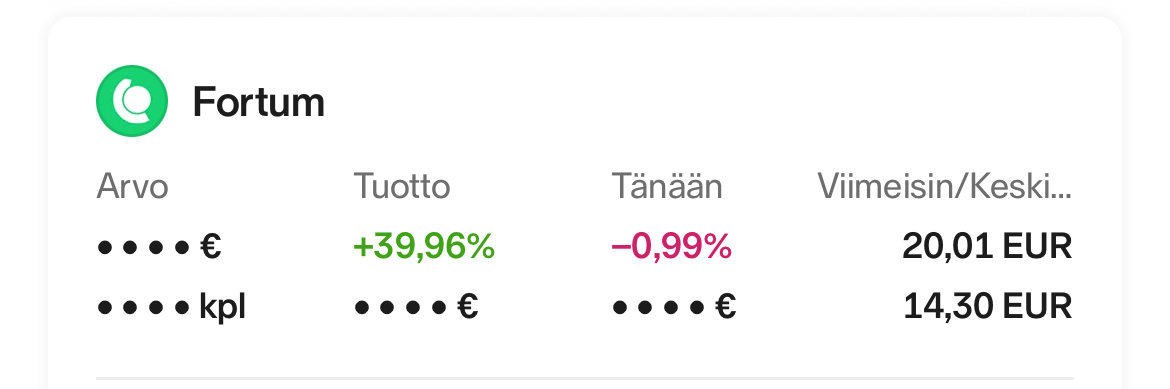

Things have been fast-paced and volatile with EQR, and so far the share price development has been ‘erratic’. The price of tungsten has continued its climb, and so

3 Likes

Chipotle, specializing in Mexican-style fast food, has seen its stock price drop to less than half of its peaks last December. Last week’s Q3 earnings report also led to a -20% stock price reaction due to an earnings miss and weak guidance. On the other hand, the company has a multi-year track record of profitable growth, and there should be plenty of room to grow by opening new restaurants. A trailing P/E of 28 still prices in growth, of course, but it is at least a more moderate multiple than before. ![]()

10 Likes

Yep, and these were the market reactions today…

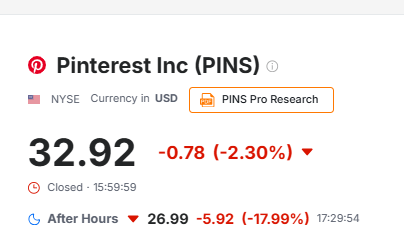

and even though some did quite well, it still went into the red. Well, these two brothers didn’t do so well. ![]()

2 Likes

Well, the main reason for the decline became clear, thanks to the American Recruit. ![]()

7 Likes

Sampo’s results are coming soon, and it would be great if they still had the Nordea stake in their ownership… NOW would finally be the time to sell Nordea, not in 2021…

5 Likes

Very strange stock reactions for NOVO and NORDEA. NOVO’s soft result is rewarded with a significant rise, and Nordea’s extremely ambitious targets and promising capital markets day output were rewarded with a -3% drop. Well, I bought 100 shares of Nordea for my son’s portfolio.

11 Likes

I haven’t followed Nordea, but Novo has been sliding for several weeks already towards its earnings report, so the market didn’t have high expectations for Novo either. Could we soon state that Novo has bottomed out, given that today’s data shows a slight green? I had a limit order at 299 DKK, but I haven’t gotten it yet. There’s still time today ![]()

13 Likes

Novo’s reaction is not particularly special. Market expectations were exceeded. The decline in the upper end of the guidance has indeed been taken into account for several weeks. I myself was also pleased that the lower end held. It would have been

18 Likes

Omeros (the drug developer) has had an eventful year. In October, it tripled due to a partnership, but that has now already halved, and the year’s overall performance is currently in the red.

Just a reminder to those eagerly awaiting deals: they might come, but the stock price might fall before that, so it won’t always be so exciting.

It will be interesting to see if Omeros still becomes a stock rocket; I’m not buying it just yet, at least.

4 Likes

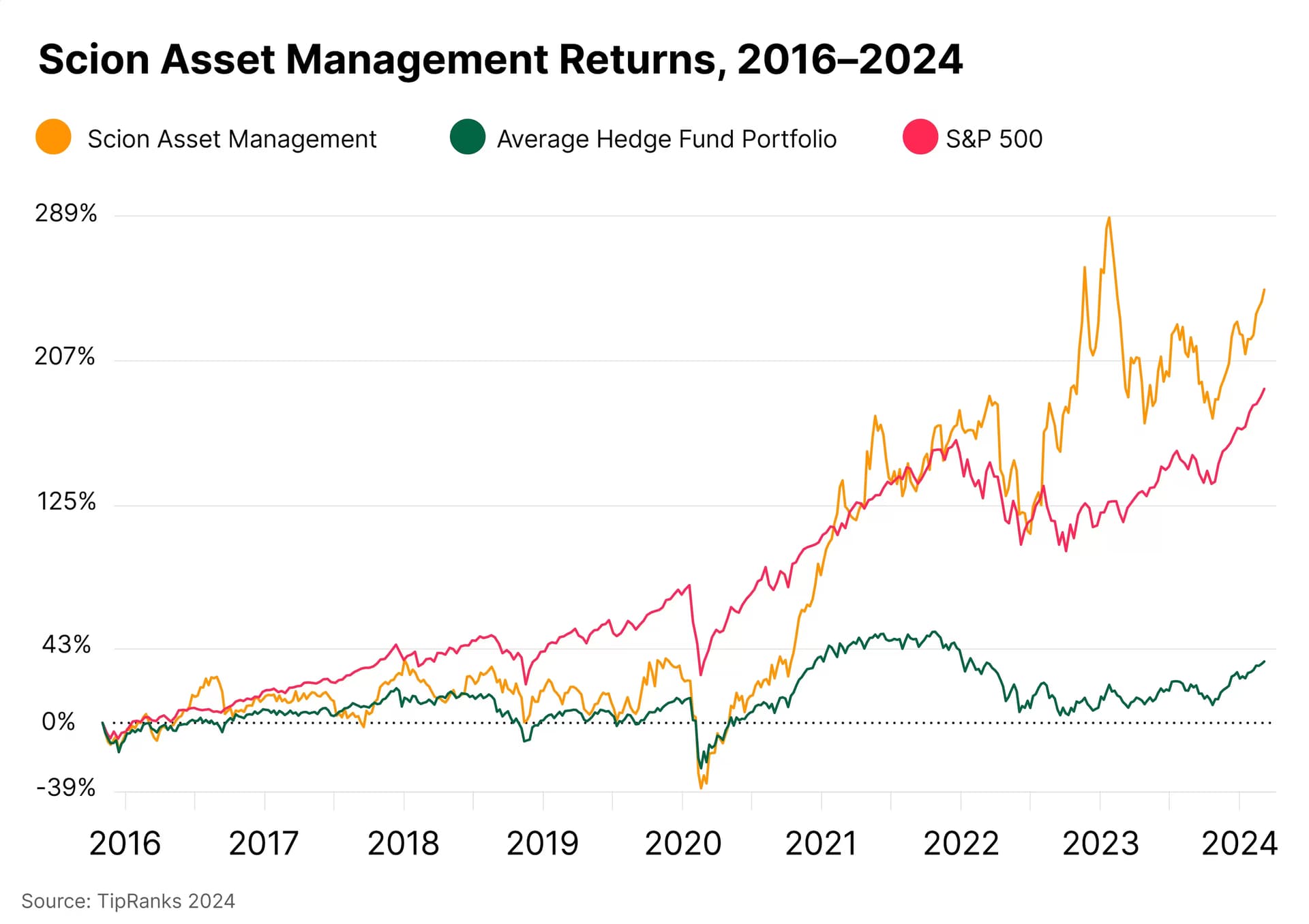

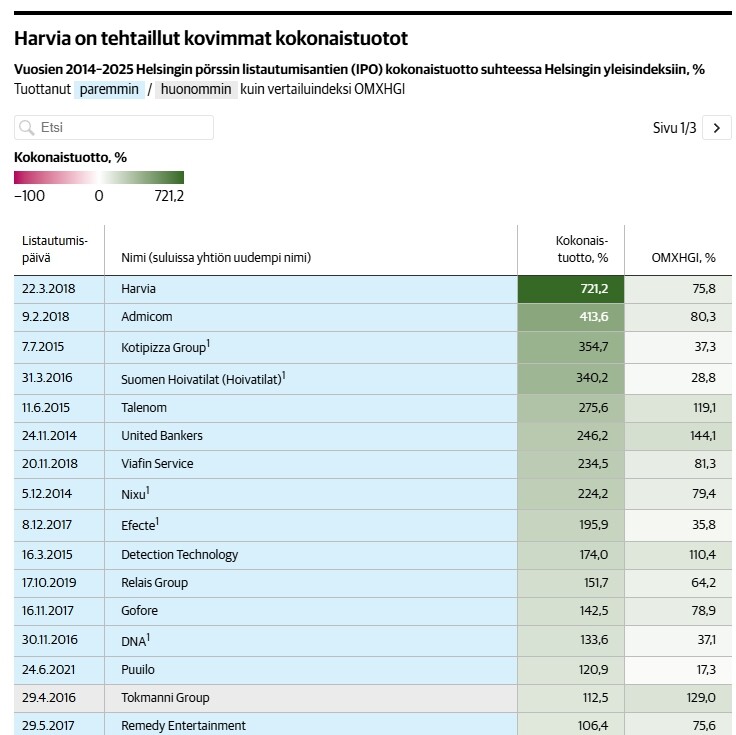

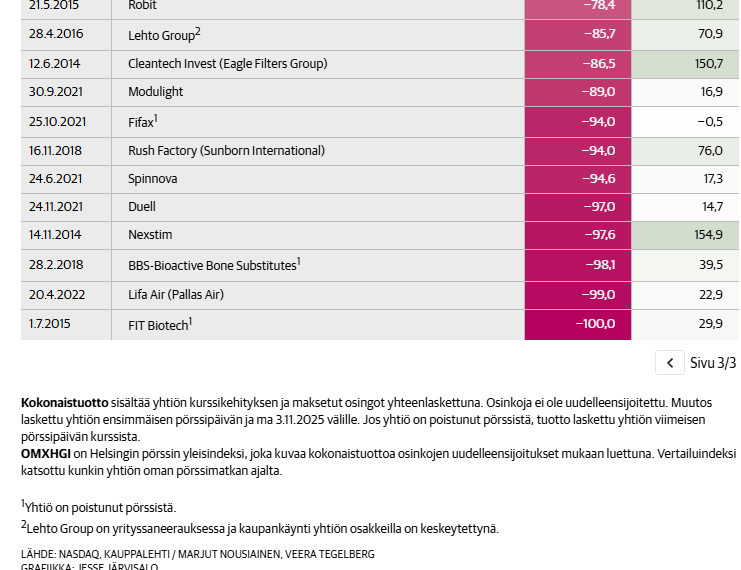

Kauppalehti now has a big and very interesting article which reviews the returns of all companies listed on the Helsinki Stock Exchange in 2014-2025. An interesting and extensive listing; numerically, the majority of stock market listings have been disappointments. Attached are screenshots of the best and worst returns:

“Puttonen gives three rules of thumb: It’s worth participating in offerings. However, one should not expect big quick profits from all of them. If you want to cash in on returns, it’s advisable to exit after the first day.

Over a long, three-year period, it is typical for listed companies to underperform compared to the index, professors say. There isn’t one single reason for this. The phenomenon is likely related to companies being able to time their listings to a moment when their value is high and everything looks good.

“Life on the stock exchange is not so blissful then, and growth prospects do not materialize as expected,” Puttonen says.”

“Of the IPOs between 2014–2025, every third has outperformed the benchmark index, including dividends, during its stock market journey, KL’s calculations reveal. Overall, more than four out of ten had generated total returns, including dividends.”

6 Likes

That article doesn’t really say much about whether it has been worthwhile to participate in IPOs, because returns have not been calculated since the IPO. For example, Kempower’s IPO price was €5.74, the current price is €15, meaning it has yielded 160%. In the table, the return is 96%.

2 Likes

Yeah, true. Of course, if one had participated with larger sums in every offering, the outcome would likely have been even worse, because from the “good” offerings, one received quite few shares, whereas from the “bad” ones, one received many shares. For example, from the Kempower offering specifically, one did not receive a large number of shares:

(Kempower: From the public offering, a total of approximately 1.4 million new shares will be issued. Since approximately 34,000 new owners emerged from the public offering, this means an average of 41 shares per individual small investor. This, in turn, means an investment of less than 237 euros in the company at a subscription price of 5.74 euros.)

2 Likes

I can’t cite studies right now, but I recall reading that first-day returns are statistically often positive, but as xlat said, over a slightly longer period, IPOs generally underperform the market.

Spin-offs, on the other hand, have generally overperformed.

1 Like

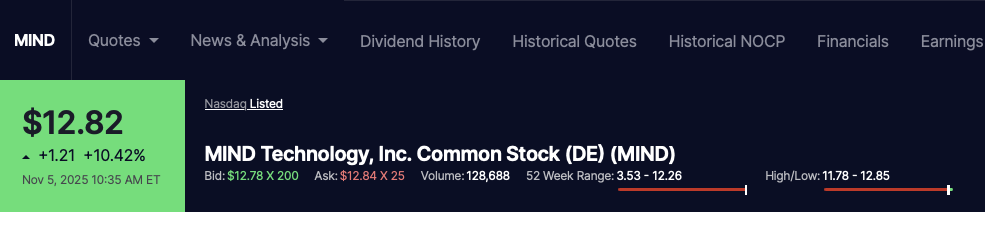

MIND’s rise is a bit frightening. It’s at a 3-year high, and there have been several such highs in the past couple of weeks. I lightened my position again to keep it manageable. 400 shares left from AOT and the company’s AOT. I can’t think of any other driver than the hype around rare metal exploration and its potential large-scale shift to the oceans. Still 3660 shares left in the portfolios. Shorts were taken heavily at a price of 9.50, no idea if they are still there, but if they are, it might already be a bit nerve-wracking.

Thanks largely to MIND, the tax authority will be able to extract 15k from me to patch up the Finnish economy.

10 Likes