In growth companies, analysts’ forecasts tend to be quite spread out, because a large part of the company’s value is determined by distant cash flows. For example, in Inderes’ analysis of Saab, the terminal component of discounted cash flows (2035 and beyond) is 81%.

I wouldn’t underestimate the work of analysts. Both their due diligence and expertise are likely better than 99% of investors. However, they don’t have a crystal ball either. I would personally prefer if the analysis included bull, base, and bear target prices, which would communicate the uncertainties related to the investment case better than a single target price.

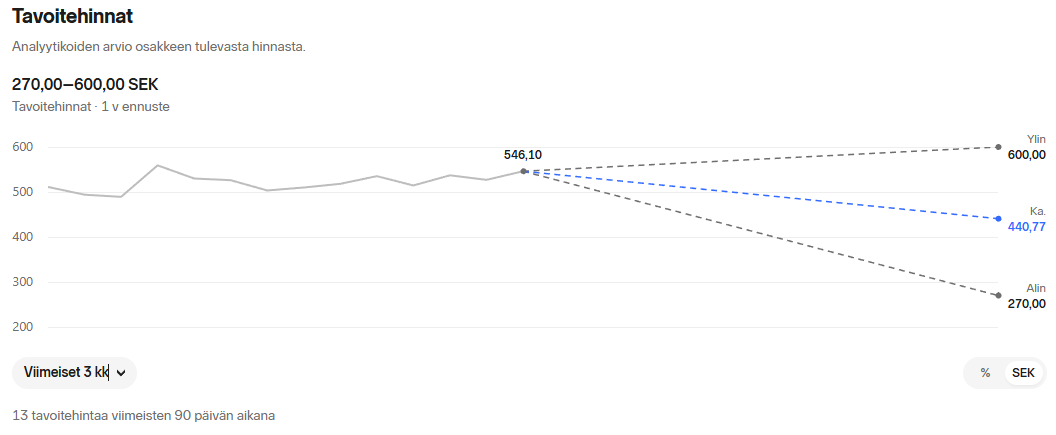

Regarding Saab, the analysts’ consensus looks like this, so Inderes isn’t even the most bearish of the group.

Finally, a word of caution. In my opinion, the European defense industry is the clearest bubbling sector in the market. For example, there were no Europe Defence UCITS ETFs before this year, and now there are 9. I don’t know where we are in the bubble, but eventually, Saab’s stock price curve will likely start to resemble this very familiar curve to you. I recommend gradually lightening your position so that you can lock in profits from your successful stock pick this time.