Kreate ilmoitti tänään 2020-01-25 pyrkivänsä pörssiin.

Aloitetaan ketju firman ruotimiseksi!

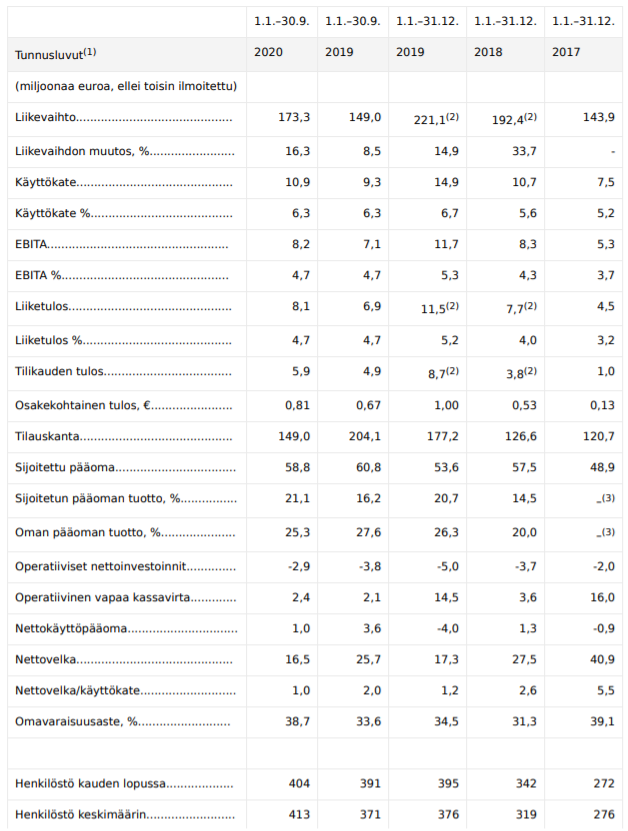

Kreate Group on Suomen johtavia infrarakentajia. Yhtiö tarjoaa ratkaisuja siltoihin, teihin ja ratoihin, ympäristö- ja pohjarakentamiseen, kiertotalouteen sekä geoteknisiin tarpeisiin. Vaativien kohteiden erikoisosaaja panostaa kokonaisvaltaiseen laatuun ja kustannustehokkuuteen. Konsernin liikevaihto vuonna 2019 oli noin 220 miljoonaa euroa ja yhtiö työllistää yli 400 henkilöä.

Pikaisesti vilkaistuna liikevaihto ollut kasvava. Niin käyttökate%, EBITA% kuin liiketulos% suht johdonmukainen, ts ei poukkoile ja raksafirmalle ok tasoa. Sijoitettu pääoma ja Oma pääoma tuottaneet mukavasti 15%…20% / 20%…25%. Velkaisuus hallinnassa.

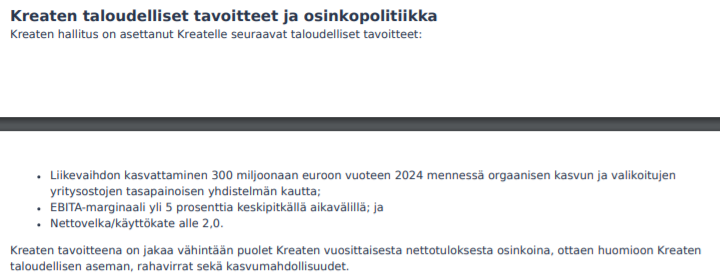

Tavoitteena 2024 liikevaihto 300 MEUR eli kasvu jatkuisi, EBITA hieman ylös nykytasosta, >5%

Itse annista tässä niin vähän tietoa, että houkuttelevuudesta merkitsijälle ei voi oikein sanoa mitään.

Vanhoja osakkeida myytydään, kerätään rahaa 10 MEUR, ankkurisijoittajat sitoutuneet merkitsemiseen jos lopullinen markkina-arvo jää max 73 MEUR.

Suunnitellun Listautumisannin odotetaan koostuvan osakemyynnistä, jossa eräät Kreaten osakkeenomistajat myyvät osakkeitaan, sekä noin 10 miljoonan euron osakeannista (Listautumisantiin liittyvien palkkioiden ja kulujen jälkeen). Osakeannilla kerättävät varat on tarkoitus käyttää Kreaten pääomarakenteen vahvistamiseen, mikä luo Kreatelle paremmat edellytykset toteuttaa sen kasvustrategiaa. Suomalainen perheyhtiö Harjavalta Oy ja Tirinom Oy (Timo ja Ritva Pekkarisen sijoitusyhtiö) ovat sitoutuneet tulemaan suunnitellun Listautumisannin ankkurisijoittajiksi (“Ankkurisijoittajat”). Ankkurisijoittajat ovat kukin erikseen sitoutuneet merkitsemään osakkeita lopulliseen merkintähintaan mahdollisessa Listautumisannissa tietyin edellytyksin ja ehdolla, että Kreaten koko osakekannan arvostus on lopullisella merkintähinnalla (annista saatavien varojen jälkeen) enintään 73 miljoonaa euroa. Ankkurisijoittajat ovat sitoutuneet ostamaan Kreaten osakkeita määrät, jotka johtavat seuraaviin suhteellisiin osuuksiin Kreaten kaikista liikkeeseen lasketuista osakkeista mahdollisen Listautumisannin toteuttamisen jälkeen: Harjavalta Oy 15,5 prosenttia ja Tirinom Oy 10,5 prosenttia.

Numeroiden valossa homma näyttää omaan silmään ihan hyvältä, vahva oman pääoman tuotto ja tasaista kasvua viime vuosina orgaanisesti. Vielä jää nähtäväksi osaavatko toteuttaa hyviä yritysostoja ja tietysti listautumishinta jos listautuvat on tärkeä.

Muuten kaupungistuminen tukee tarvetta infrarakentamiselle ja korjausliiketoiminta tuo hyvää jatkumoa ja näkyvyyttä liiketoimintaan. Palvelutarjoama on kaikenkaikkiaan hyvin laaja. Ympäristöasioita ja kiertotaloutta nostetaan myös hyvin esille joka istuu tähän päivään ja voi olla että yhtiö saa sillä myös tehtyä kulusäästöjä jonkun verran.

Yhtiön keskittyessä erityisesti erikoisosaamista vaativiin infrahankkeisiin voisin kuvitella tämän tuovan tietynlaista vallihautaa kilpailijoita kohtaan, sillä se kellä se osaaminen on ja track record on vahva voittaa projekteja pidemmän päälle.

Ehkä riskeinä voisi nähdä erilaiset onnettomuudet hankkeissa tai yllättävät kulut ja viivästykset. Kaikenkaikkiaan tässä kohtaa mielestäni kokonaisuus näyttää hyvältä ja nyt vielä kiinnostaa se mahdollinen listautumishinta. Jäädään odottelemaan

Aika raflaava otsikko!

Kreate mainitsikin päivän uutisessaan, että 61% laskutuksesta on julkiselta puolelta, ja saattaapi yksityisen sektorin laskutuksesta osa olla julkisen sektorin urakoita

Kun katsoo Kreaten projektiesimerkkejä niin käyhän tuo hyvin selväksi…

Kreaten asiakaskunta koostuu suurimmaksi osaksi julkisen sektorin asiakkaista. 1.1.2019–30.9.2020 välillä 31 prosenttia Kreaten myynnistä tuli valtio-omisteisilta tahoilta, 30 prosenttia kunnallisen puolen asiakkailta ja loput 39 prosenttia yksityisen sektorin asiakkailta.

Firman kotisivuilta löytyy viime vuodelta vain tosi käppyinen half-year rapsa, josta historiaan vertaamalla ja perkaamalla sain seuraavan suuntaista fundapyöritystä. Tarkempaa analyysiä ja lukuja vielä tarvitaan, kun sitä tulee.

Vuosi 2020, mikäli oletetaan identtinen H2 vs H1:

Liikevaihto 216M€ / kasvu% -2.9%

EBIT 8.8M€ / EBIT% +4.1%

Nettotulos 4.7M€

Koronavuosi näkyisi siis hienoisena liikevaihdon ja kannattavuuden laskuna.

Opan Q1-Q3 postaamaan liikevaihtoon tämä tosin -11M€ perässä, joten ehkä tämä on bear-skenario

Oman ennusteensa mukaan tavoittelevat 300M€ liikevaihtoa ja >=5.0% EBITA 2024 mennessä. Oikaisin ja laskin 5.0% EBITillä:

LV 2021: 244.0M€ 2022: 272.0M€ 2023: 300.0M€ (+13.0%/+11.5%/+10.3%)

Liikevaihdon kasvu on linjassa historiamediaanin kanssa ja oletuksena hienoinen tuottavuuden parantuminen.

Tuottavuuden ja velkaisuuden ollessa ok tässä on ihan mielenkiintoisen potentiaalinen keissi nimenomaan kasvun myötä. EPS:n kasvu >30%, EPS CAGRit myös hyviä lukemia, hyvä liikevaihdon kasvu menneessä sekä ennusteessa ja erinomainen nettotuloksen historiallinen kasvu koronakuopan huomioiden.

Seuraillut tuota kreaten toimintaa niin vaikuttanut tosi hyvältä. Projekteissa alitettu budjetteja ja aikatauluja joten kyllä mukaan lähdetään jos hinta kohdillaan.

Ettei tarvitse noita H1/H2-vertailuja noin tehdä, niin ihan ilmoittavat jo tuossa tiedotteessa, että liikevaihto 2020 tulisi alustavien tietojen mukaan olemaan 235m€, EBITA n. 10,5m€ (4,5%). Itse myös ymmärsin, että vuonna 2024 liikevaihto olisi juuri tuon 300m€ eikä 2023. Joka tapauksessa, jos se on 300m€ 2024, se vastaisi n. 6,3% keskimääräistä vuosikasvua. Vastaisi aika hyvin myös juuri 2019->2020 kasvua 221m->235m (6,33%).

Olen myös kuullut alalla olevilta, että olisi hyvä firma ja myös numeroista päätellen potentiaalia on. Annetut tavoitteet (300m€ ja >5% EBITA) ovat myös mielestäni hyviä, enkä näkisi että olisi mitenkään liikaa optimismia tässä. Toivottavasti hinnoittelu ei pilaa tätä.

Noniin kiitoksia, toki tämä meni minulta ohitse.

Jos 2000 liikevaihto on tuossa jamassa ja 300M€ on annettu vasta vuoden 2024 liikevaihtotavoitteeksi niin tuntuisi, että tavoitteissa olisi jopa nostamisen varaa.

Joo ei todellakaan tule. Taas yksi niistä anneista, jossa 10000 euron sijoituksella saat tonnilla osakkeita. Selvää on, että tulee moninkertainen ylimerkintä.

Yleisöpuolelle tulossa siis vain noin 10% koko annin koosta. Kuulostaa todella härskiltä. Eli murusia jää, jos ei merkkaa instikkapuolella. Btw ne jotka tätä merkkaa instikkapuolella, kyllä litsoo somessa ja blogeissa pikavoittojenmetsästäjät merkkaamaan. Listautumiset on nykyään kasinoa ja se jatkuu, niin kauan ennen kuin ensimmäisella kerralla porukalla jää ne 10x yli oikeesti tahdotun määrän laput käteen. Hurjalta tuntuu kun kuulee juttuja että porukka vetää isolla lainavivulla about tutkimatta näihin sisään.

Yleisöannin pieni koko on minusta ymmärrettävää, sillä koko transaktio on aika pieni.

Instituutioannin 3,8 miljoonasta osakkeesta ymmärtääkseni 2,3 miljoonaa on kaupattu etukäteen ankkurisijoittajille Harjavalta Oy:lle ja Tirinom Oy:lle. Muille instituutioille jää siis jaettavaksi vain 1,5 miljoonaa osaketta. Tähän verrattuna yleisöannin (vähintään) 0,4 miljoonaa osaketta tuntuu minusta ihan kohtuulliselta allokaatiolta. Tietysti kun niukkuutta jaetaan, syntyy helposti pettymyksiä.

Toistaiseksi tämä IPO näyttää minusta kiinnostavalta ja valuaatio kohtuulliselta. Täytyy tutustua tarkemmin, kun maanantaina tulee lisää materiaalia jakoon.