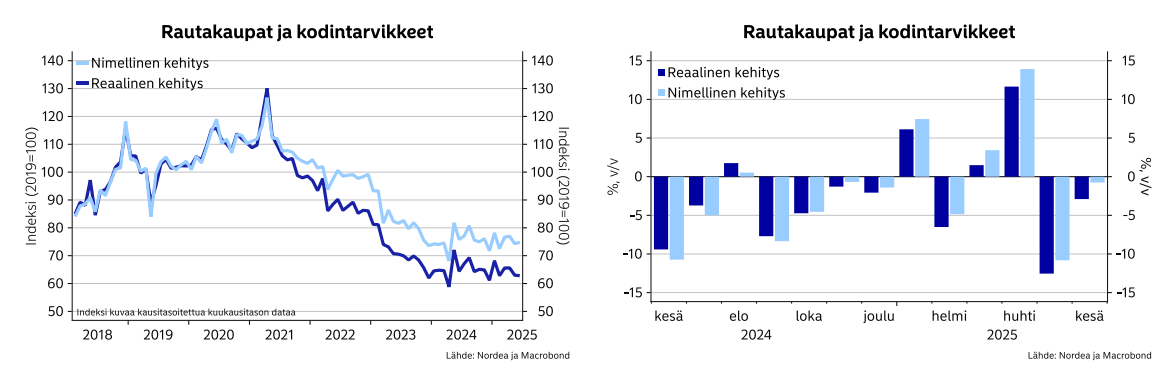

Huh. Quite staggering figures are emerging from the construction sector. Yesterday, Kesko reported disappointment regarding its hardware and technical trade.

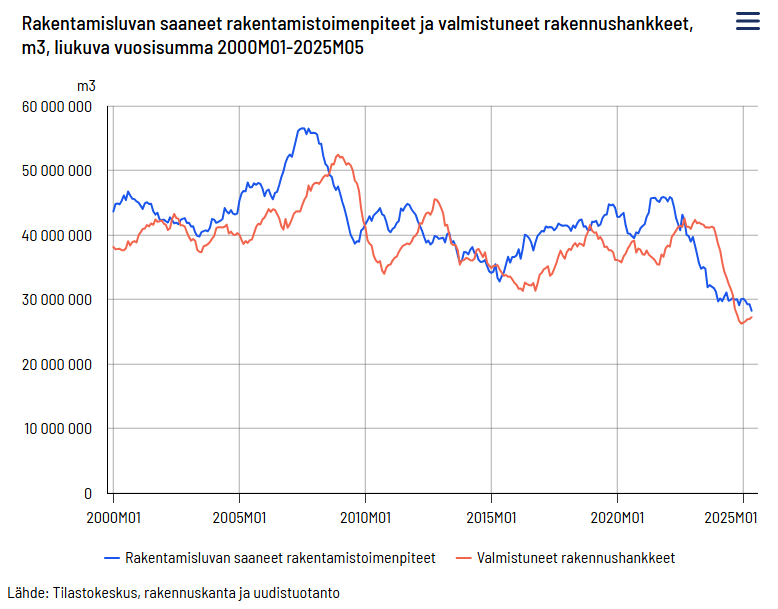

Last year, the consensus was that construction would pick up well in '25, but now it’s starting to look like construction won’t properly get going even in '26. Even the historically dismal building permit figures from last year are taking a hit, with a -9% in May!

Volume of granted building permits decreased by 9% from a year ago in May 2025 | Statistics Finland

KH Koneet’s performance has indeed been remarkable given these conditions. Hopefully, in a few weeks, we’ll hear that the miracle-making has continued. Or have I somehow misunderstood KH Koneet’s product range structure? Isn’t a significant part of the range still related to construction, and the property maintenance/material handling/agriculture range still smaller?

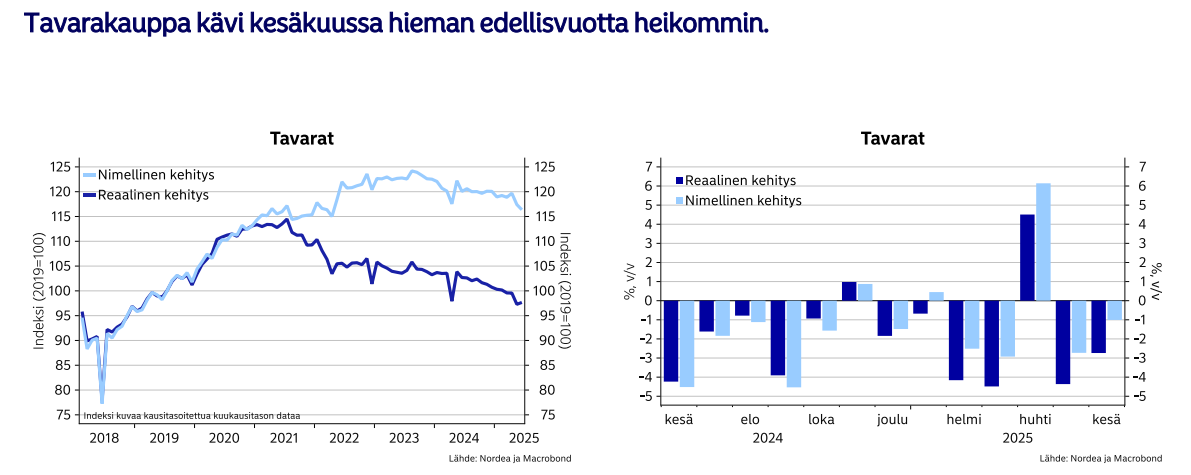

Regarding Indoor, Nordea’s card payment data indicates a strong April but a quiet May-June in the home goods trade. The correlation of this statistic to Indoor’s sales was not strong, but it generally confirms that Finnish consumers are still not shopping as they used to.

I increasingly wonder about this: How is the Finnish consumer so stubbornly constrained? For about three years now, CEOs have consistently reported in their interim reports how interest rates and inflation have eroded consumer confidence. BUT consumer confidence is not recovering, EVEN THOUGH inflation is close to zero AND interest rates are below the long-term average!?! It seems there are quite significant buyer’s markets in consumer-side M&A right now.

Indoor’s sale has been ongoing for almost half a year now, and Nikulainen mentioned already in winter that there had been interest. Hopefully, we will hear positive news on the matter in connection with H1.

In June, news about competitors was linked here too, when Sukari stated, “Masku had its worst result in history last year. We restructured, tried to save, and stay afloat by all means,” and predicted that half of Finland’s furniture retail brick-and-mortar stores would disappear.

Terrible results at Masku – A harsh statement from Topi Sukari. Masku is apparently now putting a lot of effort into e-commerce. “When I turn 80, I will be number one in Finland with AI and e-commerce,” Sukari declares.

A few weeks ago, we heard about the progress of Isku’s restructuring program, and it seems that protection from creditors is coming.

Isku Interior’s restructuring program progresses – This is how the company renews itself | Kauppalehti

It has often been discussed on this forum that Jysk and Ikea are tough competitors for Sotka and Asko. But I see Masku and Isku (for Asko) as perhaps even worse/direct competitors. I mean, wouldn’t it be much easier to grab market share from Masku and Isku than from the big giants? Would Masku or Isku exiting the market be a positive surprise and excellent news for Indoor? Especially before Indoor’s sale, such news would have a big and positive impact. Masku’s financial data from '23 is public, but what is Masku’s current resilience? And would there be more public information about Isku’s debt restructuring somewhere?