Arttu Heikura haastatteli Keskon pääjohtajaa Jorma Rauhalaa Q4:n kunniaksi

Aiheet:

00:00 Aloitus

00:12 Yhteenveto Q4-tuloksesta

02:38 Markkinaosuuden kasvu

04:24 Hintakilpailu

06:18 Median tekemät ostoskorivertailut

08:51 RT-kaupan tilanne

10:54 Maakohtaiset erot

12:18 Onnisen kilpailutilanne

14:03 Autokaupan kehitys ja kilpailu

16:46 Romutuspalkkiokampanjan vaikutus uusien autojen markkina

18:19 Konsernin rakenne

20:21 Urheilukaupan rooli Keskossa

21:16 Investoinnit, velkatilanne ja voitonjako

23:44 Ohjeistuksen taustaoletukset

Aika mukavasti tämä juna etenee. Ainakin itselleni suurin huoli on ollut päivittäistavarapuolella, jonka tilanne nyt tuntuu olevan stabiloitumassa. En nopeasti bongannut ainakaan mitään huolestuttavaa, mihin voisi takertua, mutta kansainvälistymiseen liittyvät menneet epäonnistumiset kummittelevat aina taustalla. Toivottavasti niistä saatu oppi kantaa vielä pitkälle.

Täälläpä on ollut tuloksen jälkeen hiljaista. Tässä vielä meidän ajatukset Q4:sta ja vuoden 2026 ohjeistuksesta. Näkymät vaikuttavat suht positiivisilta etenkin kun katsoo vuoteen 2027. Tästä syystä jatkettiin positiivisella näkemyksellä vaikka kuluvan vuoden arvostuskertoimet ovatkin melko kireät.

Poimintoja:

PT-kaupan myymäläverkoston uudistamisen nettovaikutuksen pitäisi olla neutraali 2026 ja positiivinen 2027. 2025 verkostosta tuli vielä negatiivista vaikutusta markkinaosuuksiin. Eli hintainvestointiohjelma tuotti merkittävää tulosta etenkin citymarketeissa.

Hintainvestointiohjelma jatkuu ja kauppiaat ovat tähän Keskon tapaan sitoutuneita.

RT-kaupan markkinassa ei selviä paranemisen merkkejä vielä, mutta toimialan sisäinen hintakilpailu vaikuttaa taantuneen. Tässä kilpailijat ilmeisesti tajuneet, että toiminnalla pitäisi tehdä pitkällä jänteellä myös tulosta, mikä on tuonut painetta hinnankorotuksille. Keskohan tekee Teknisessä tukkukaupassa valtaosan markkinan tuloksesta Suomessa.

Autokaupassa markkina jatkunee heikkona, mutta romutuspalkkio saattaa tuoda jotain tukea uusien autojen markkinan kehitykselle. K-auton kasvu perustuu siis yhtiön omaan vahvaan suoritukseen.

OP puolestaan laski tavoitehinnan 21 euroon aiemmasta 21,5 eurosta ja siirtyi lisää-suosituksesta vähennä-puolelle.

Ohjeistus on vain marginaalisesti viime vuoden alun ohjeistusta parempi. Rauhalan aikana on ollut vähän taipumusta liiallisen optimismiin, joten ei osake ainakaan halvalta näytä. Laatuyhtiötä kaupan kireästi hinnoiteltuna.

Hyvä katsaus. Itse näen Keskon kansainvälistymistarinana. Toki on mielenkiintoista ja tärkeää, että markkinaosuustaisto kotimaassa sujuu hyvin. Mutta jos kansainvälistyminen onnistuu, on tässä aineksia vaikka mihin. Mielestäni Kesko on aika hyvässä vaiheessa, kun ensin on hieman hakattu päätää seinään Ruotsissa K-rauta konseptin kanssa, niin jatkossa löytynee tarvittavaa nöyryyttä ja halua oppia ja hyödyntää epäonnistumisita tulleita kokemuksia. Johdosta on nyt paljon kiinni.

Autokaupan toimialajohtaja Johanna Ali kävi Kauppalehden Talousaamussa juttelemassa viime vuoden tuloksista, tämän vuoden näkymistä ja autoalan tilanteesta.

Keskon myynti nousi tammikuussa 4 %. Orgaaninen liikevaihto kasvoi prosentilla. Kasvu syntyi kaikkien toimialojen vetämänä. Tammikuun kehitys ylitti konsernitason ennusteemme hienoisesti. Tilanne ei toistaiseksi aiheuta välitöntä muutostarvetta ennusteisiimme, sillä kvartaalia on jäljellä vielä kaksi kuukautta.

Keskosta kiinnostuneiden onnenpäivä: tuore vuosiraportti on julkaistu läpipengottavaksi!

Tietoa löytyy paitsi viime vuoden tapahtumista ja luvuista myös mm. strategiasta,

K-kauppiasmallista, toimintaympäristöstä ja riskeistä, kiinteistöistä sekä vastuullisuusteoista.

Muistutuksena osakkeenomistajille, että torstaina 26.3. järjestettävään yhtiökokoukseen ehtii vielä ilmoittautua mukaan tai tilata verkkolinkin 19.3. klo 16 saakka. Paikkana K-Kampus Helsingin Kalasatamassa. Lisätiedot ja ohjeet: Yhtiökokous 2026

Keskon myynti nousi helmikuussa 5 %. Orgaaninen liikevaihto lisääntyi kolmella prosenttilla. Kasvu syntyi kaikkien toimialojen vetämänä. Tammi-helmikuun kehitys on ollut myönteistä ennusteisiimme nähden, mutta maaliskuu, jonka aikana geopoliittiset jännitteet ovat nousseet merkittävästi, on vielä raportoimatta. Tästä syystä tarkastelemme ennusteitamme vasta maaliskuun myyntilukujen raportoinnin jälkeen.

Päivittäistavarakaupan viime vuoden markkinaosuuksia on julkaistu:

Tuossa vertailua vuoden takaa:

Pienemmistä toimijoista Lidlin osuus nousi 0,1 % ja Tokmannin laski 0,1 %. S-ryhmän osuus nousi 0,2 % ja K-ryhmän taas laski samaiset 0,2 %. Mutta kuten tiedetään K:n markkinaosuus kääntyi kasvuun viimeisellä kvartaalilla.

Alla on Artun kommentit Keskon maaliskuun menosta.

Keskon myynti nousi maaliskuussa 12 % jokaisen toimialan vetämänä. Vertailukelpoisen myynnin kasvu oli 10 %. Konsernin Q1:n myynnin kehitys on ollut myönteistä suhteessa ennusteisiimme, mutta vuoden pienimmällä kvartaalilla ennusteylityksen vaikutus koko vuoden ennusteisiimme on marginaalinen. Päivitämme ennusteemme ajantasaisiksi lähipäivinä.

Arttu nyt kiltisti nostaa kolmeenkymppin eikä ole penseä virkansa vuoksi. Koska tietää että että trendi jatkuu samalaisena kunnes yllättäen katkeaa. Nyt mahtavat numerot.

Byggmax (fokus B2C-rakentamisessa) valitteli kylmästä alkuvuoden säästä, jonka takia heillä Q1:n myynti 5 %:n laskussa. Kesko mainitsi Q4-tuloksen yhteydessä mulle samasta kylmästä säästä, mutta ei se RT-kaupan luvuissa oikein tahtonut näkyä

Alta löytyy Artun etkoilut, kun Kesko kertoo Q1-tuloksestaan keskiviikkona 29.4.

Keskon myynti kehittyi Q1:llä varsin hyvin, minkä turvin arvioimme konsernin tuloksen nousseen vertailukaudesta. Odotamme yhtiön myös toistavan tuloskasvua viitoittavan ohjeistuksensa. Numeroiden ohella seuraamme tulospäivänä erityisellä mielenkiinnolla Keskon näkymiä. Päivitimme kommentin yhteydessä ennusteemme myyntilukujen mukaisiksi ja lisäsimme kasvuodotuksiin ripauksen varovaisuutta, mutta Keskon mittakaavassa muutokset vuositasolla olivat marginaalisia.

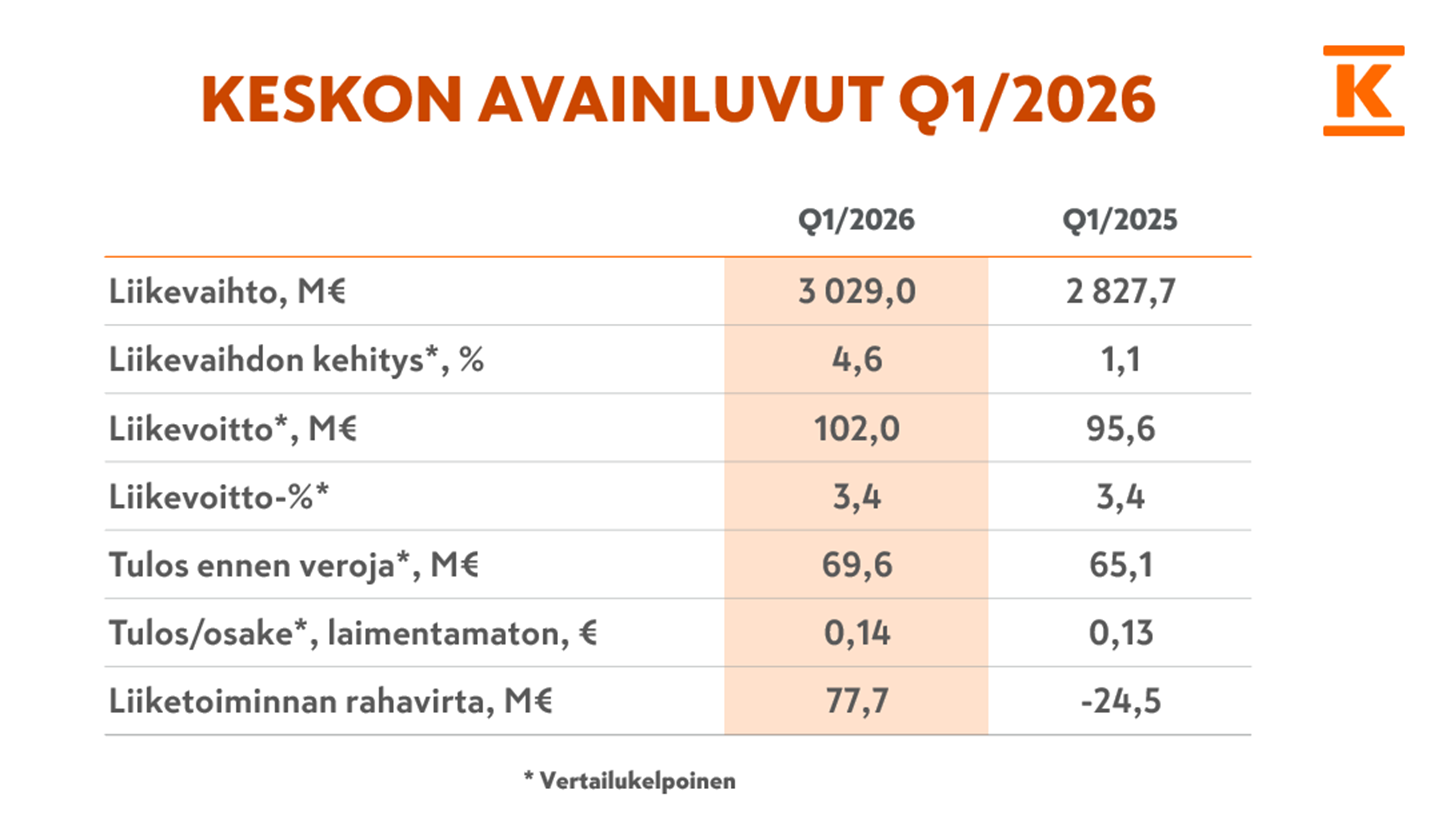

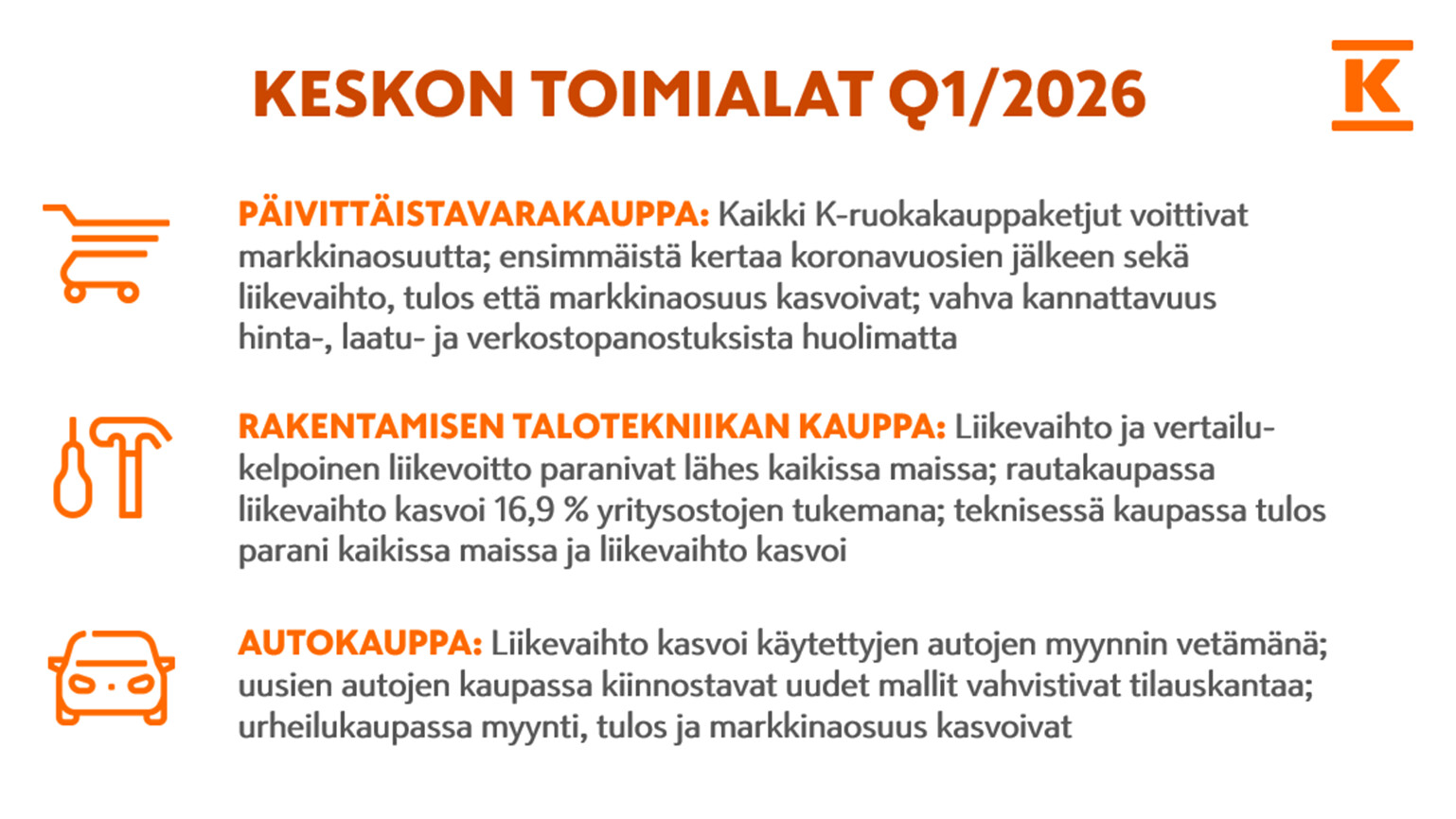

Q1-tulos on julkaistu: Liikevaihto kasvoi kaikilla toimialoilla ja Keskon vertailukelpoinen tulos parani. Kaikilla toimialoilla nähtiin myönteistä kehitystä verrattain haastavana jatkuneesta markkinasta huolimatta.

Tulosohjeistus pysyy ennallaan: Keskon toimintaympäristön, liikevaihdon ja tuloksen arvioidaan paranevan vuonna 2026 kaikilla toimialoilla ja kaikissa toimintamaissa. Vuoden 2026 vertailukelpoisen liikevoiton arvioidaan olevan tasolla 650–750 MEUR.