Here are Aapeli’s comments from the analyst and investor call preceding the quiet period.

Kalmar held an analyst and investor call yesterday preceding the Q3 quiet period. Based on the company’s comments, there had been no significant change in the market situation compared to the outlook provided with the Q2 results. Kalmar will publish its Q3 results on October 31.

Patrick Terminals Places Significant Order for Automated Straddle Carriers with Kalmar

Kalmar has received a significant order for 14 hybrid Kalmar AutoStrad™ straddle carriers from Patrick Terminals. The equipment will be deployed at the Sydney AutoStrad terminal. The order was booked in Kalmar’s Q3 2025 orders, and delivery is scheduled to be completed during Q3 2026.

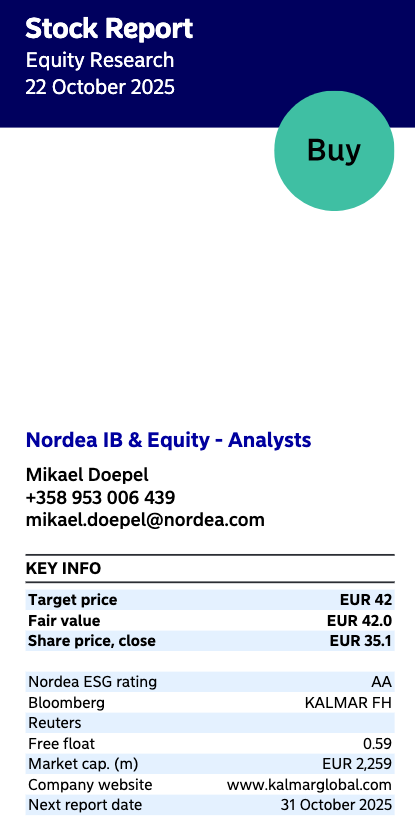

OP raises its recommendation from REDUCE to BUY and the target price from €38 to €40.

According to OP, the stock is undervalued and the order slump is priced into the stock. The analysis is available in the online bank for OP’s customers.

As a shareholder, these OP recommendation upgrades cause more fear than hope regarding the direction of the share price development. Fortunately, they cannot directly affect companies’ earning capabilities.

Fortunately, the OP-Suomi fund only owns 163,000 shares, 0.11% of the share capital, and was still on the buying side in September, increasing its shareholding. Well, it will be interesting to see what happens now that they changed the recommendation to Buy.

Analyst’s preview comments regarding Kalmar’s Q3 results. At the same time, the recommendation rises to ADD (previous: REDUCE), the target price remains unchanged at EUR 39.00.

Kalmar’s Interim Report January–September 2025: Improved Profitability in the Quarter

Record-high comparable operating profit margin of 13.8 percent, supported by Services and improved efficiency

Global market uncertainty continued, with the constantly changing customs and trade policy situation dampening decision-making

Strong performance in Services with both increased received orders and profitability

Received orders for Equipment decreased by 20 percent from the comparison period, but showed stable growth in January-September

2025 guidance unchanged.

July–September 2025 in brief:

Received orders decreased by 10 percent and amounted to EUR 375 (416) million

Order book at the end of the period was EUR 961 million (31.12.2024: EUR 955 million)

Sales increased by 3 percent and amounted to EUR 436 (425) million

Sales of Eco-solutions1 product group accounted for 46 (40) percent of the Group’s sales, increased by 17 percent and amounted to EUR 201 (172) million

Operating profit was EUR 61 (54) million, or 13.9 (12.7) percent of sales. Operating profit includes EUR 1 (-4) million in items affecting comparability

Comparable operating profit was EUR 60 (57) million, or 13.8 (13.5) percent of sales, an increase of 4 percent

Cash flow from operations before financing items and taxes was EUR 26 (72) million

Profit for the period was EUR 45 (36) million

Undiluted earnings per share were EUR 0.70 (0.56)

Interest-bearing net debt / EBITDA2 was 0.3x (0.4x).

We reiterate our Add recommendation for Kalmar and our target price of 39 euros. The company’s Q3 result slightly exceeded our forecasts, with record-level margins supporting the development, while orders fell short of expectations, driven by the more cyclical equipment side. Services development, on the other hand, was broadly stronger than our expectations. The company’s market comments remained unchanged, and the demand situation has remained stable or good outside of the Americas. Reflecting the overall picture, forecast changes remained minor, and we see the stock’s valuation as attractive when compared to favorable long-term earnings growth prospects.

OP raises target price to 42.00 (40.00) and reiterates BUY

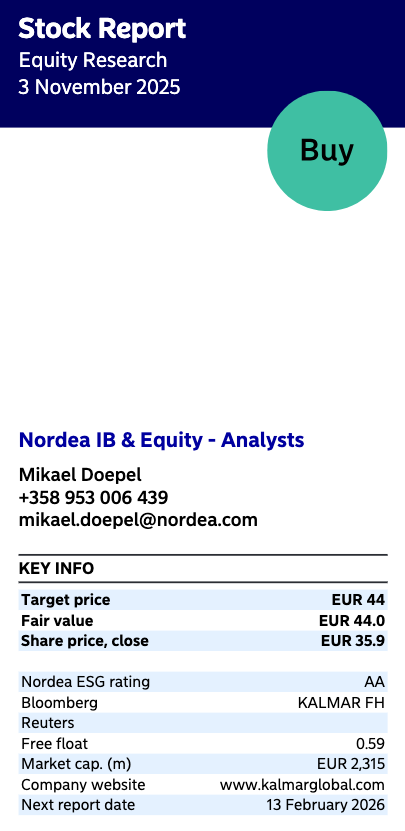

Nordea published its updated Kalmar analysis after the Q3 results. The target price rises to 44.00 euros (previous: 42.00 €), the recommendation remains at BUY.

Kalmar and Forth Ports Continue Their Cooperation with a Large Follow-up Order for Hybrid Straddle Carriers

Kalmar has received a follow-up order for three Kalmar hybrid straddle carriers from Forth Ports Group. The equipment will be deployed at Forth Ports Grangemouth. The large order was booked in Kalmar’s Q4 2025 orders, and the delivery of the equipment is scheduled to be completed during Q2 2026.

Forth Ports Grangemouth is Scotland’s largest port, handling nine million tonnes of cargo annually through dedicated container, liquid, and general cargo terminals.

KALMAR CORPORATION, PRESS RELEASE, December 3, 2025 at 11:00 AM

Kalmar and Patrick Terminals Sign New 10-Year Strategic Supply Agreement

Kalmar has signed a new 10-year strategic supply agreement with Patrick Terminals. The supply agreement strengthens a partnership spanning over two decades, which has been significant for Australia

The idea might be a bit ahead of its time, or perhaps just at the right time, but has anyone happened to come across whether Kalmar has been involved in space-related logistics in one way or another? One would imagine that launch sites (spaceports?) need a massive amount of equipment to move parts and other cargo, etc., so it would be great to hear if Kalmar (and other engineering companies) are involved in these slightly more far-fetched areas.

It’s getting a bit sci-fi, but space-related technology is developing at a staggering pace, and once the associated transportation technology becomes scalable, the need for other logistics related to the industry will likely explode.