Japani kiistää jyrkästi Kiinan väitteet siitä, että sen linja Taiwanin kriisiin olisi muuttunut, lisäksi Japani perään kuuluttaa lisää keskustelua, jotta kahden Aasian suurimman talouden välit eivät kiristyisi enempää.

Kiinan varoitukset ja muut toimet sekä kommentit ovat jo heijastuneet matkailuun ja tuontirajoituksiin, mikä lisää painetta muutenkin herkkään tilanteeseen.

Taloudessa panokset ovat kovat; Kiina on yhä Japanin tärkein kauppakumppani ja samalla myös avainraaka-aineiden toimittaja. Siksi Japani yrittää vähentää riippuvuuttaan, mutta jännitteiden kasvu voisi silti heilauttaa koko Aasian talousnäkymiä.

Juttu pitäisi olla kai muurin takana, jos on lukenut ilmaiseksi tietyn määrän uutisia.

Japanin ensi vuoden palkkaneuvottelut alla olevan jutun mukaan vaikuttavat menevän liittojen näkökulmasta suostuisasti; ammattiliitot vaativat taas reiluja korotuksia ja tiukka työvoimatilanne painaa yrityksiä myöntymään.

Jutussa todetaan myös, että jatkuvat palkkojen korotukset vahvistavat odotuksia siitä, että Japanin keskuspankki nostaa korkoja pian. Silti Yhdysvaltain tullit ja heikko talousnäkymä luovat kuitenkin samalla varjoja yritysten päätöksille.

Labour unions demand bumper pay hikes despite US tariffs

Tight labour market pressures firms to maintain big pay hikes

BOJ awaits early signs of wage talks for rate hike decision

Japanin suurimman ammattiliiton Rengon johtaja Tomoko Yoshino painostaa hallitusta hillitsemään hintojen nousua, jotta palkankorotukset eivät valuisi ihan hukkaan. Hänen mukaansa inflaation pitäisi saada rauhoitettua selvästi, jotta työntekijöille saataisiin lisää tarvittavaa ostovoimaa.

Jutun mukaan Yoshino ajaa edelleen reiluja palkankorotuksia erityisesti pienille yrityksille. Hän muistuttaa, että myös tullit ja heikko jenin kurssi lisäävät epävarmuutta, siks hän korostaakin tarvetta saada palkat ja hinnat vakaalle uralle.

“In her negotiations this year Yoshino will have to navigate the implications of trade policy developments and their impacts on larger manufacturers. After many rounds of trade talks, Washington agreed in July to fix tariffs on imports from Japan at 15%. While the rate is lower than the 25% originally threatened, it remains well above levels before Donald Trump began his second term as president.”

Japanin keskuspankki vihjaa mahdollisesta koronnostosta jo tämän vuoden joulukuussa, kun jenin heikkous lisää inflaatiopaineita ja poliittinen vastustus alkaa hellittämään. Yhä useammat ovat muuttuneet haukkamaisemmiksi, lisäksi markkinoita “valmistellaan” yllätyksen välttämiseksi. Koronnoston ajoitus riippuu paljolti myös Yhdysvaltain keskuspankin linjasta.

Samaan aikaan BOJ on pohtinut, että voiko heikko jeni pitää inflaation korkealla aiempaa pidempään. Palkankorotusten näkymät ja vähentyneet pelot Yhdysvaltain taloudesta tukevat sen normalisointia, vaikka päätökseen vaikuttavat yhä tietysti poliittiset ja kansainväliset paineet.

Japani aikoo rahoittaa Takaichin talouspaketin yli 11,5 biljoonan jenin lisävelalla, eli selvästi suuremmalla summalla kuin Ishiban hallituksen ohjelma tarvitsi.

Vahva verokertymä pienentää velan tarvetta, muttei kuitenkaan poista sitä.

Bank of America arvioi, että Japanin talous jatkaa maltillista kasvua ensi vuonnakin, kun kotimainen kysyntä ja yritysten investoinnit paikkaavat heikkoa vientiä.

BofA nosti kasvuennusteitaan ja uskookin inflaation rauhoittuvan sekä palkkojen tukevan kulutusta että työvoimapulan vauhdittavan investointeja.

Suurin epävarmuus liittyy Takaichin hallituksen finanssilinjaan.

Alla olevassa FT:n jutussa kerrotaan, että Japani on pitkään pyörittänyt valtavaa velkataakkaa, mutta alhaiset korot ovat luoneet vaarallisen harhan ettei velka olisi mikään ongelma. BoJ on pitänyt korot keinotekoisen matalina, mutta koron nousukausi koronan jälkeen romahdutti jenin ja teki selväksi ettei korkokattoja voi enää puolustaa ilman valuuttakriisin riskiä.

Nyt jutun mukaan korot on pakko päästää nousemaan, mutta ne ovat keinotekoisen alhaalla. Japanilla ei käytännössä ole enää kunnolla finanssipuskuria.

Jutussa tuodaa ilmi, että jos uusi pääministeri Takaichi haluaa oikeasti erottua niin hänen pitäisi uskaltaa kiristää taloutta esim. veronkorotuksia, menojen leikkauksia tai sitten vaikka laittaa valtion omaisuutta myyntiin. Markkinat palkitsisivat kuulemma jo pienestäkin suunnanmuutoksesta.

Japanin valtiovarainministeri varoitti, että jenin nopeat ja epävakaat liikkeet eivät perustu varsinaisesti talouden perusteisiin. Hän korosti myös, että tarvittaessa valuuttainterventiot ovat mahdollisia. Jutussa todetaan, että markkinat odottavat nyt keskuspankin viestiä mahdollisista koronnostoista jenin tukemiseksi.

Markets last week had been looking out for intervention by Tokyo to shore up the declining yen, but the currency stabilised. On Monday, all eyes will be on a speech by Bank of Japan Governor Kazuo Ueda to see whether he signals a likely rate increase at the BOJ’s December meeting, which would help lift the currency.

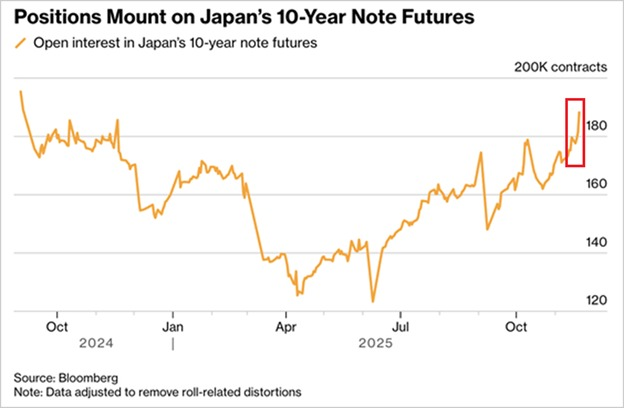

Japanin valtionlainamarkkina alkaa yskähdellä pahasti. Kymmenvuotisten futuurien määrä on noussut korkealle, hinnat ovat painuneet 2008 tasoille ja korot nousseet tuntuvasti.

Sijoittajat näyttävät kasvattavan shorttejaan kovaa vauhtia, mikä lisää markkinan hermoilua entisestään.

Tämä tulee olemaan tiukka paikka pääministerille joka ratsastaa nimenomaan “vanhoilla hyvillä arvoilla.” Mikä tahansa liike mikä uhkaa 40+ väestönosaa on erittäin vaikea tehdä. Toisaalta jos nuoria kuritetaan menevät kaikki syntyvyyden tukitoimet vessasta alas. Mutta jos näistä kahdesta pitää valita, nuoret saavat luultavasti maksella hinnan, joka on omiaan vähentämään koheesiota jonka raiteilla Japani kulkee.

Japanin palvelusektori jatkoi vahvaa kasvua marraskuussa, kun maan PMI nousi 53,2:een ja työllisyys kasvoi nopeimmin kymmeneen kuukauteen.

Kustannusten nousu johti hintoja ylös, lisäksi palvelut kompensoivat teollisuuden heikkoutta ja composite-PMI (palvelu+teollisuus) kohosi 52,0:aan. Jutussa sanotaan, että uusi elvytyspaketti voi edesauttaa kysyntää.

Alla olevassa jutussa kerrotaan, miten Japanin keskuspankki on haastavassa tilanteessa; koronnostot kiristäisivät taloutta ja voisivat nostaa pitkien valtionlainojen tuottoja entisestään, mutta sitten taas korkojen pitäminen matalana voi kiihdyttää jo korkeaa inflaatiota.

Japanin velka paisuu, lisäksi tilanteella on vaikutuksia myös kansainvälisiin markkinoihin jne.

Key Points

On Thursday, yield on the benchmark 10-year JGBs hit a high of 1.917%, surging to their strongest level since 2007.

If the BOJ sticks with its policy of raising rates, it risks sending yields higher.

If it cuts or keeps rates steady to support growth, inflation could accelerate further.

Japanin ministeri Minoru Kiuchi toivoo keskuspankilta suunnalta tiivistä yhteydenpitoa hallituksen, mutta ei vastustanut mahdollista joulukuun koronnostoa. Markkinat tulkitsivat ministerin lausunnot merkiksi siitä, ettei hallitus estäisi koron nostoa 0,5:stä 0,75 prosenttiin.

Japanin aluepankkien realisoitumattomat tappiot kotimaisista joukkovelkakirjoista nousivat syyskuun loppuun mennessä ennätykselliseen yli 21,3 miljardiin dollariin, eli yli kolminkertaisiksi keväästä.

Tappioita kertyy jo viidettä vuotta, kun Japanin valtionlainojen arvonlasku on historiallisen jyrkkää.

Japanin pääministeri Sanae Takaichi ajaa jättimäistä elvytyspakettia velkarahalla juuri nyt, kun korkotasot ja jenin heikkous hermostuttavat sijoittajia.

Valtion velka on jo erityisesti opposition mielestä valmiiksi valtava ja markkinoilla pohditaankin, kuka ostaa kaikki uudet joukkovelkakirjat. Moni pelkääkin, että jos kasvu jää haaveeksi niin käteen jää vain kasa entistä kalliimpaa velkaa Japanille itselleen.

Extra bond sales will also test an already fragile market, where demand - especially for long-dated paper - has traditionally been uneven from foreign investors and has been drying up for years from domestic banks and insurers.

After accounting for redemptions and decreased purchases by the Bank of Japan, net supply in the market will jump by nearly 11 trillion yen in 2026 from 58 trillion in 2025, according to Bank of America estimates.

“The problem is … who’s going to buy these bonds?” said Sally Greig, head of global bonds at Scottish long-only manager Baillie Gifford. “We’ve still got more supply to absorb and Japan’s not the only one spending money.”

Japanin jeni on hetkeksi “rauhoittunut”, kun BOJ:n pääjohtaja Kazuo Ueda vihjasi uusista koronnostoista ja markkinat hinnoittelevatkin joulukuulle jo noin 80 prosentin todennäköisyyden koronnostoista.

Analyytikot silti odottavat jenin heikkouden jatkuvan ensi vuodelle, samalla kun uusi pääministeri Sanae Takaichin 137 miljardin dollarin elvytyspaketti lisäävät entisestään inflaatio- ja velkahuolta.

Japanin talous supistui kolmannella neljänneksellä odotettua enemmän, sillä BKT laski 0,6 prosenttia ja vuosivauhti oli -2,3 prosenttia.

Vienti ja kotimainen kysyntä heikkenivät, lisäksi investoinnit kääntyivät laskuun ja heikko kehitys voi viivästyttää Japanin keskuspankin mahdollisia koronnostoja sekä lisätä alla olevan jutun mukaan myös paineita finanssipolitiikkaan.

Japanissa on juuri mitattu 7,2 magnitudin maanjäristys. NHK-yleisradioyhtiön mukaan ainakin rannikolle on annettu tsunamivaroitus Tyynellämerellä tapahtuneen maanjäristyksen takia.

The earthquake registered an intensity of 6+ on Japan’s seismic scale of 1-7 in Aomori Prefecture, according to the JMA. Japan’s scale measures the intensity of shaking at specific locations, with 6+ representing severe tremors that make it difficult for people to remain standing.

Morgan Stanleyn mielestä Japanin elektroniikkayhtiöt hyötyvät teollisuuden elpymisestä, tekoälyn kasvusta ja sähköistymisestä.

Pankki nostaa esille TDK:n, Muratan, Niterran, Meiko Electronicsin ja Hirose Electricin, joille kaikilla odotetaan vahvaa tuloskasvua akkujen, komponenttien, piirilevyjen ja liittimien kysynnän vetämänä. Yhtiöt on käyty hyvin tiiviisti alla olevassa jutussa läpi, sen verran vain, että ideoiksi, mitä voi ehkä lähteä itsenäisesti tutkimaan.

Japanin tuottajahinnat nousivat marraskuussa odotetusti 2,7 prosenttia vuodentakaisesta ja 0,3 prosenttia kuukaudessa.

Reuters Tankan -indeksi, eli joka on ilmeisesti suurten teollisuusyritysten luottamusindeksi, putosi +17:stä +10:een, ja siinä sitten taas suunta onkin alaspäin. Taustalla painavat kasvuhuolet ja se, että keskuspankki vihjailee vähitellen kiristyvästä korkolinjasta.