A brief introduction to Intervacc, a company whose stock is associated with significant expectations during H1 2021.

Company: Intervacc AB (IVACC), Stockholm Stock Exchange. Company Website. Founded in 2001, CEO Andersson since 2018. The company has been developing a new type of vaccine for horses for several years.

Product: Strangvac vaccine for equine strangles, which is a dangerous, highly contagious animal disease. The disease causes severe inflammation in the animal’s respiratory tract. It has been difficult to develop a sufficiently effective and reliable vaccine against it. Vaccines have been on the market before, but they have had unpleasant side effects. Article about the vaccine here

Potential: Strangvac has performed well in tests and the drug is in the final approval phase. The product has few competitors because other drugs have problems. Since Strangvac is based on a new innovation, the technology can also be utilized in the production of other vaccines.

Short-term expectations: EMA approval of the vaccine during H1 2021 and the vaccine would be on sale during H2 2021.

Company results and cash: The company is in a cost management phase and is loss-making, but its cash position is strong and no new share issues are expected. The year 2022 is expected to be profitable.

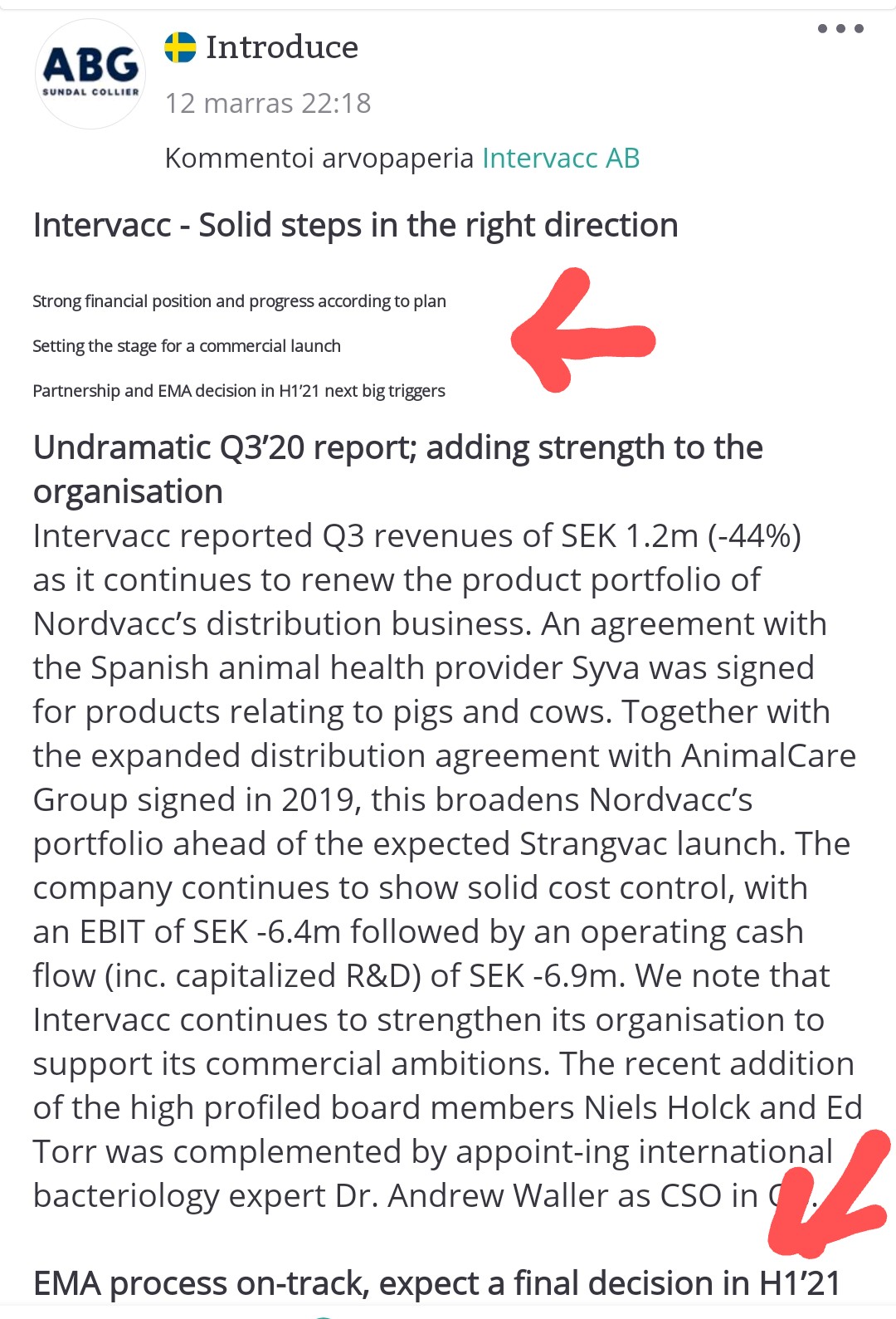

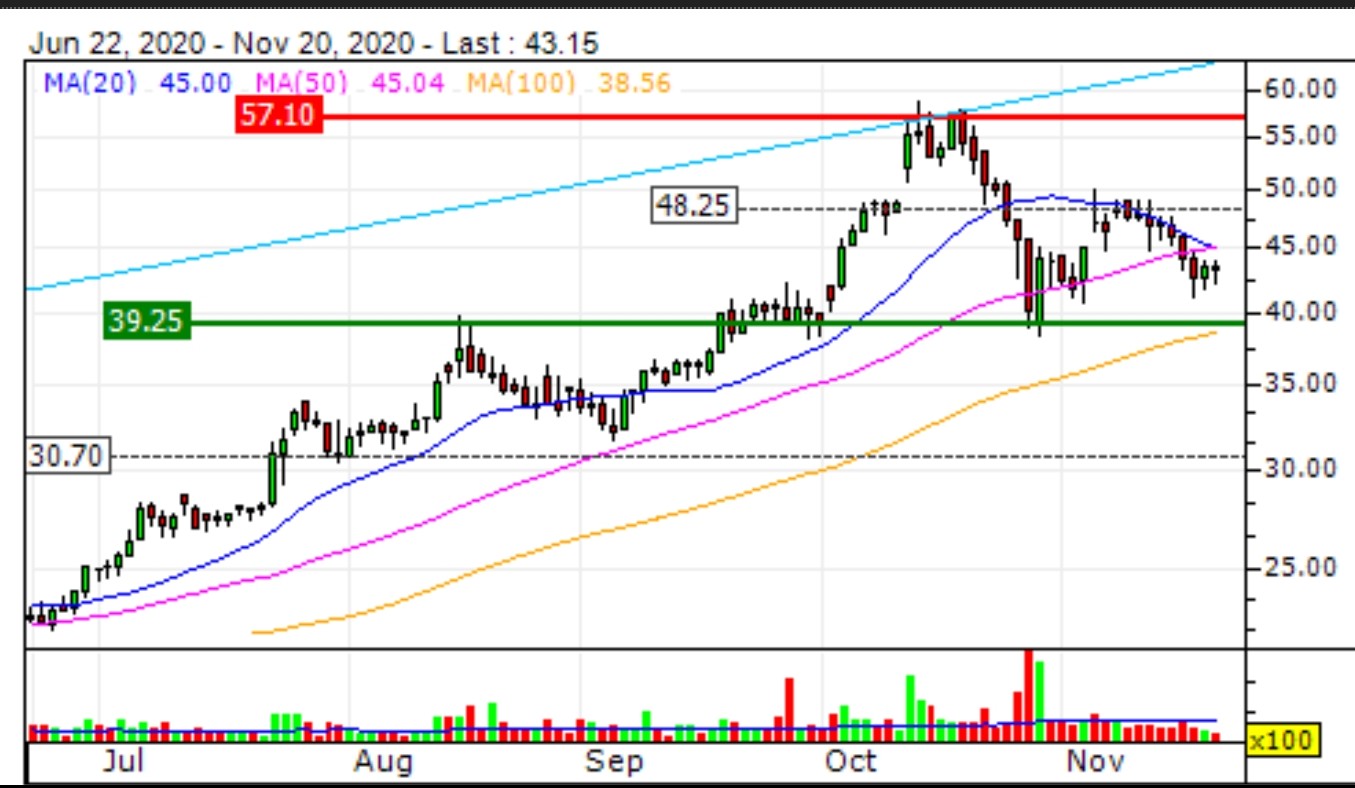

Stock valuation: ATH 57 SEK after Danske Bank set its target price at 80 SEK (13.10.2020). The stock has now had a quieter period and is currently at 43 SEK (20.11.2020).

The valuation is based, among other things, on the assessment that Intervacc will be able to announce the outcome of the regulatory review of the Strangvac vaccine in Europe towards mid-2021, with the launch of Strangvac shortly thereafter.

According to Danske Bank, the commercial opportunities, both in the short term and in the medium to long term, should be significant as there are many incentives to vaccinate horses against the equine disease strangles.

Danske Bank also points out that Intervacc has several long-term opportunities to become a significant company in animal health.

I jumped on this train a little over a year ago, an interesting start to the year is coming.

The probability of approval for the Strangvac® vaccine is considered 90% certain, and the target market size is €1.2-1.8 billion.

Here is a link to an article about the vaccine (though not very recent):

In addition, there is a vaccine for pigs in the pipeline, among others, whose potential is considered much greater.

Here is a copied summary from the Kauppalehti discussion forum:

Intervacc - Breathe easy: Strangvac is on the way

Strangvac offers strong, long-lasting efficacy with an excellent safety profile and easy administration (intramuscular injection).

Strangvac: a clear improvement compared to alternative treatments

Antibiotics are ineffective against strangles

Strangvac net price 15 euros per dose.

Equine strangles is the most commonly diagnosed infectious disease in equids.

60 million horses worldwide

Strong platform

Strong team (R&D team expertise)

Right niche

Lower regulatory burden (veterinary vaccine market versus human therapeutic medicines)

The average cost of bringing an animal vaccine product to the veterinary market is a fraction of the cost of human medicines.

@AnthiS, that target market information is very interesting. The company is currently trading at a valuation of over 200 million euros. If the target market is 1.2 - 1.8 billion euros, that sounds good.

It would be interesting to know how that target market was calculated. Is the size of the target market based on vaccinating all horses to develop immunity, or is the vaccine the type that is used as a medicine only when symptoms appear?

Another relevant point is that similar vaccines can indeed be developed for pigs, for example. So the company also has significant growth prospects already listed, which is why the case has significant long-term growth potential. If Strangvac gets approval, I would assume that the starting point for other medicines based on the same innovation is good.

Interesting opening and the prospects are appealing, but with the information I managed to dig up, the current valuation seems unnecessarily expensive.

Thanks to @AnthiS for the links, those ABGSC reports (introduce.se) in particular were interesting reading. In my opinion, the comprehensive report from April 2019 outlined the market potential well. Have there been any updates to the estimates since then, or where did that 1.2 - 1.8 billion euro potential come from? Or has someone else estimated differently?

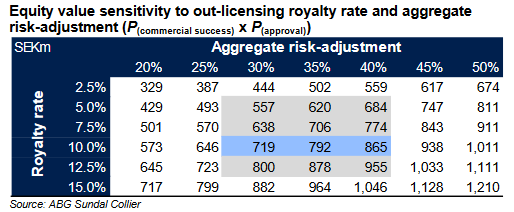

What I managed to glean from the comprehensive report was that the total lifetime value of the Strangvac vaccine was estimated in the base scenario to be 720-865 MSEK. When compared to the current valuation of 2,176.96 MSEK, it looks expensive.

Valuation sensitivity analysis from the comprehensive report:

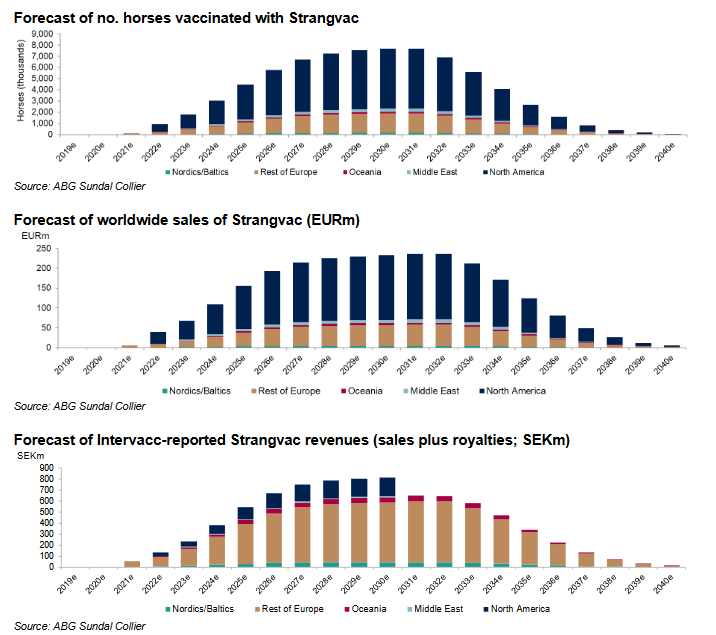

When I summed the bars in the last graph, i.e., Intervacc’s forecasted direct sales + royalties, it seemed to be in the order of 8 - 8.5 billion SEK, or roughly 0.8 - 0.85 billion euros. And these are, of course, future revenues, which still need to be calculated into profit and discounted to present value, from which they have calculated the previously mentioned 720-865 MSEK value for this product.

So, pretty high expectations have been priced in for the other pipeline candidates, if there haven’t been any updates to the earnings potential in that comprehensive report.

Thanks, excellent additional information on profitability! Reviewing these in more detail has been on my to-do list and was my goal when I opened the chain.

Initial thoughts on valuation. Edit: clarified calculation. In ABG’s analysis, Peak Ebita 42.6%, taxes 20%. R&D is accounted for before Ebita.

2022 revenue 150 MSEK / 15 M€. Assumption: zero profit.

2023 revenue 250 MSEK / 25 M€. Profit after tax = Revenue growth after 2022 * 0.4 → Profit 4 M€. P/E ratio 50x. Ebita% would then be 20%.

2024 revenue 400 MSEK / 40 M€. Profit formation like 2023, profit 10 M€. P/E ratio 20x. Ebita% would then be 30%.

2025 revenue 550 MSEK / 55 M€. Profit formation like 2023, profit 20 M€. P/E ratio 10x. Ebita% would then be 43%.

This profit formation is a rough estimate, but it is within the framework of ABG’s Ebita analysis.

Four to five years out, the valuation would be quite reasonable for a pharmaceutical company, in my opinion, provided that sales permits are obtained in the spring and product demand is predictable. I would assume that the company would be valued at a P/E ratio of 25x - 70x in 2025 if this forecast has materialized, depending, among other things, on whether there are new products in the pipeline and what the outlook is going forward.

these, of course, are future revenues, which still need to be calculated into profit and discounted to present value, from which they have calculated the previously mentioned 720-865 MSEK value for this product.

@Hapakka, your reference to the table of royalties of 720-856 MSEK only includes, as I understand it, royalty payments from biosimilars. This is not about the entire revenue potential of the drug, but only about royalties. If the EBITA% were 30-40%, then the rough order of magnitude of the vaccine’s product life cycle revenue before taxes would be 3 billion SEK.

720-856 MSEK is the extensive report’s view of the fair value of the entire company. It is based on a 30-40% probability of getting marketing authorization and commercial success. If one believes that the probabilities are higher, then one can estimate the value based on the previous table.

With 100% probability, this would result in the current market value of 2,176.96 MSEK, if the size of the royalties remains on the better side.

I understood that the upper one is an estimate of the total drug sales and the lower one is an estimate of the revenue generated by sales for Intervacc, i.e., own sales (Nordics/Baltics) + royalties from partner sales (rest of the world). Edit: so apparently, we understood it in the same way.

A vaccine for pigs would be very significant. The stock might have already discounted some of the value of this possibility. With a quick search, I couldn’t find information on how far along the tests for this product are.

African Swine Fever has spread from Africa to parts of Europe and Asia. China has seen the worst of it

"It has now infected more than 60 per cent of Chinese pigs and globally, we think it has infected or will infect more than a third of all pigs on this planet. So it’s a huge problem for the industry,” he said

Looking at Europe’s share of Intervacc’s forecasted revenue, EMA approval will be a significant factor. Once it’s in the bag, the company will move into a new phase where funding will be sufficient for years to come, and the company will be able to develop its products while achieving good or at least reasonable profits. Another similar product by 2025, e.g., the already mentioned pig vaccine, would take the company to a new level. The track record of the horse vaccine will be a market indicator for evaluating the potential of new launches.

In summary: EMA approval and positive news about other pipeline products during H1 2021 will give the stock two significant drivers, and Danske’s target price is justified.

Of course, there is a risk in the stock at the current valuation if there were any setbacks, but in my opinion, the “niche” of veterinary medicines is easier to grasp and predict for a pharmaceutical company, also regarding drug approvals. As Intervacc invests and specializes in this area, it seems like a good strategy. So, it’s the Musti ja Mirri (a pet supply chain) of the pharmaceutical industry.

Intervacc’s website mentions that a pig vaccine is being developed against diseases (e.g., sepsis, blood poisoning) caused by the Streptococcus suisbacterium. African swine fever, on the other hand, is a disease spread by a virus. Could there have been a misunderstanding regarding this pig vaccine?

Yep, a misunderstanding. A company called VIDO - Intervac is developing a vaccine for swine fever. So it’s a different company.

The company’s website shows the status of their projects. The cattle and pig projects seem to be in the early stages, with the pig medicine slightly further along. Based on the timelines, new medicines are several years away. On the bright side, there are two medicines in the pipeline.

According to the company’s website news from 2015, Strangvac has been a product “close to a solution” since 2015. So the vaccine has been under development for a long time. However, I would assume that since the new medicines apparently utilize Strangvac’s innovation, development could be faster. Without better information, launch expectations should be set for 2025. Any clarifications on these timelines would be interesting and a positive opportunity.

A very moderate position has been opened, which leaves room for further investment if the price drops, but we are in if it starts to rise.

It was very atypical for me to get involved in such an uncertain opportunity and with so little background work.

The investment decision was made because a friend, who owns a horse and spends every day at the stable, saw very positive aspects in this.

The horse’s head disease is apparently a seasonal flu-like illness that spreads in the stable where it settles. It usually comes with imported horses. Apparently, it is also a serious disease that fells horses. He believed that every horse owner would acquire this if an effective vaccine became available. As an outsider, I have noticed how much money is spent on horse care and maintenance, and the horse itself is a very large investment. A vaccine that secures one’s investment is a small price compared to the total costs involved with a horse. NOTE: These are my friend’s and my own personal thoughts.

The positive drivers are definitely that the vaccine is apparently effective and on its way to the markets. On the downside, there’s a risk if there are complications in the approval process.

Great to have a dedicated thread for Intervacc! As I understand it, the horse vaccine needs to be administered once a year to maintain its protective effect. This didn’t seem to come across in the messages. Annual vaccination would mean stable production potential. So, if the net price of the vaccine is 15 EUR and 10% coverage of the horse population (i.e., 6 million horses) is achieved, it would be 90 million EUR annually, or probably 850 million SEK. Based on those forecast images, it seems that 6 million vaccines is the upper limit, meaning that a more comprehensive vaccination rate for the global horse population is not anticipated? Perhaps someone wiser could elaborate, correct, or comment on this aspect.

One thing I’ve been thinking about is the lifecycle of the horse vaccine. Is it really true that the product will expire and disappear in 20 years? Or can we assume that Intervacc will develop the product and a more effective version will replace it, providing longer-term income for the company?

I guess the logic was that patents protect the drug until around 2030-2031. After that, generic drug competition will start, which will eat into both sales and margins. It’s unlikely to be that straightforward in reality, and I recall that years ago, Orion’s Parkinson’s drugs performed significantly better and longer than expected after their patents expired. It’s still hard to rely on sales remaining good when one doesn’t know the dynamics of the market and supply chains at all.

This is indeed an interesting perspective: if the forecast assumes (only) a 10% penetration into the horse population, for example, a 15% penetration could be seen as a quite significant positive opportunity. Of course, this would require an analysis of what the 10% assumption is based on, to better understand what the realistic range is here.

Right! I pulled that 10% assumption out of thin air in a previous message, based on charts some clever people have made. Whether they had a 10% assumption for vaccination coverage is unknown. The global horse population probably divides into subgroups. In some, there’s a strong economic interest (racehorses, riding schools, etc.), while in others, it’s a hobby. I’d assume this in Western countries, but what about the situation with horses in Asia, Russia…?