The company has had a vaccine for piglets as a development project, and now promising results have been obtained in the development work. The company’s share price has been going down like a sled (along with the general sentiment?). The main product is a horse vaccine, and now there are promising results for supplementing the product range.

5 Likes

Regarding the equine vaccine, the company has now announced an information campaign following the product’s sales. And the slumped share price has now picked up a bit; we’ll see in the future. As far as I know, the vaccine is only sold in Sweden (?). And it certainly needs to be marketed when such a vaccine is available, as some horse enthusiasts are probably quite unaware of it.

[Nordnet’s reporting cannot be linked rationally, so the text is below]

Intervacc: Together Against Strangles

29.4.2022 13.29 •

On March 23rd, Strangvac was released for sale in Sweden, and the following week the first pharmacies began placing orders and receiving the vaccine. Since Strangvac was approved in Europe in August 2021, we have worked intensively to inform leading equine veterinarians, and we have had very productive meetings with over 100 so-called Key Opinion Leaders across Europe. With Strangvac becoming available for sale, the next phase began: meeting and educating veterinarians around Sweden to inform them about Strangvac. The interest has been very high, and our team has already met many veterinarians and held training sessions. Strangvac is launched in Sweden, and we will now gradually launch it in the rest of the Nordics and Europe.

In parallel with educating veterinarians, we have launched the “Together against strangles” initiative, aiming to raise awareness among horse owners about the disease strangles and the importance of implementing infection control measures. We are fully dedicated to the mission of reducing the spread and effects of strangles. During April, we collaborated with Svensk Galopp, and we have several other events booked for the future. Among other things, we will represent Intervacc with a booth at the Falsterbo Horse Show and the World Cup in Herning this summer. With information and knowledge, we can protect our horses together!

We continue to have many strangles outbreaks in Sweden. During the five-year period 2016-2020, an average of 76 stables with confirmed strangles outbreaks were reported annually in Sweden. Only the first diagnosed horse in a stable is reported as an outbreak. An outbreak can, therefore, include several sick horses. We are regularly contacted by desperate horse owners who have suffered strangles outbreaks. Every outbreak is a tragedy that, in addition to great suffering for affected horses, also means worry and financial burden for the horse owner. In April, the first horses in Sweden were vaccinated with the newly launched vaccine against strangles. We have a new tool in the important fight against strangles.

Next week, the “Stop Strangles” campaign will begin, an information campaign about strangles and infection control for horses run by SVA and supported by several of the major equine organizations in Sweden. We at Intervacc also support this initiative while working on our long-term campaign to spread knowledge about strangles and infection control. Together, we can #stopstrangles.

1 Like

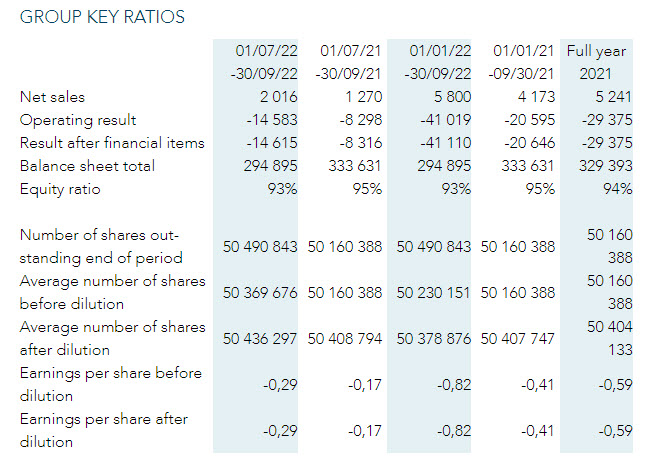

Intervacc’s Q2 result was (as expected) negative, although net sales did progress somewhat. The result is, of course, explained by the start-up phase of vaccine product sales, where expenses are still high and revenues are slower to come in. Steps forward have included extending the vaccine’s shelf life (sales period); they also mention that the US marketing authorization application is being initiated.

2 Likes

[quote=“veronmaksaja, post:112, topic:9361, full:true”]

Intervacc’s Q2 result was (as expected) negative, although net sales did improve somewhat. [/quote]

Net sales were, in my opinion, a huge disappointment. The vaccine was on sale in Sweden for the entire Q2 and in Denmark for just over a month, yet revenue grew by a pathetic 80 thousand euros compared to the same quarter last year. Despite the CEO’s words of praise, sales have been slow to start.

Horse owners are having a tough time now, as all costs are rising at a tremendous pace. Even though a lot of money is spent on horses anyway, there comes a pain threshold at some point, and it’s likely that savings will be made on all non-essential items.

Intervacc’s market capitalization is quite high if sales don’t pick up quickly. Also, the cash reserves will be depleted in less than a year at the current rate of losses.

Englanniksi:

“It is frustrating that it takes time to launch a new vaccine and to go from central approval by the EMA to sale in local markets. It is a process that I had hoped would go faster,”

“We expect to start sales in several European countries shortly.”

“Earlier this year, we started the application process for a sales permit in the US, but have not yet reached a stage where we can provide a time estimate for the completion of the regulatory process.”

1 Like

I understand your point of view and disappointment - however, Erik Penser Bank Sweden, which follows the company, commented that one should not have too high expectations yet, “Sales started in Sweden in March, in Denmark in May, and in the UK in mid-August.” and “Seasonally, horses are primarily vaccinated at the end of the year and we expect most of the year’s sales to occur in the fourth quarter.” Of course, it’s a gamble to estimate how the general economic sentiment will affect horse owners’ actions. The bank places the stock in the 92-102 SEK range.

https://docs.penser.se/a/3038/Intervacc_Q2.pdf

Erik Penser expects sales of SEK 31 million for this year, while ABG Sundal Collier expects SEK 43 million.

After the first half of the year, sales are only SEK 3.7 million, so there needs to be a big leap in the rest of the year. We’ll see how it goes. It’s really the worst possible time to launch any new product on the market right now.

1 Like

Of course, the times are not good for any new launch right now; consumer discretionary will suffer the most.

Healthcare (whether for oneself or a pet) is often among the last expenses to be cut when consumption needs to be prioritized.

Vaccination can also be thought of as “insurance,” where a small investment can prevent/alleviate very severe and costly consequences if a strangles epidemic starts spreading in one’s stable.

In the short term, the price will likely move a lot with sales development.

However, in the long game, the biggest driver for Ivacc, in my opinion, is the effort to move away from antibiotic marination in production animals. Even a vaccine that is only 20% effective would help a lot with this.

2 Likes

The company’s Q3 figures have been released. In my opinion, sales growth has been quite sluggish, and the negative trend has become even more pronounced. Of course, there are marketing expenses, and a bright spot is the start of sales in Central Europe, including Germany & France, on October 12, 2022. The company should significantly improve its figures, or perhaps Strangvac’s sales are weaker than anticipated.

I’m quoting myself from just over two months ago. Analysts seem to be completely off with this company too. Well, Intervacc seems to have ended its tracking agreement with at least ABG now.

During Q3, Sweden, Denmark, and the UK brought in 2 MSEK in sales. During Q4, a couple of new countries will be included, so will sales rise to as much as 4 MSEK? Then the total turnover for the year would be a whopping 10M. At the same time, the company’s market value is still 1700 MSEK… Cash will be empty in a year, meaning stock offerings are expected.

1 Like

This is quite a classic situation in the pharma/medical sector, where demand for the product can be considered certain (e.g., in this case, a competitor doesn’t even exist) and certain market shares can be calculated with a margin of error to arrive at quite high figures (current valuation), BUT it is extremely difficult to estimate how quickly revenue will reach the forecasted level.

Licensing processes, production, distribution channels, marketing—everything takes time and money. For example, in Finland, apparently this vaccine is not available yet, even for money.

Additionally, the company is likely going full throttle on new products, as patents aren’t eternal: Pipeline - Intervacc which, for its part, consumes cash.

In the livestock sector, a holy grail awaits if antibiotic consumption can be reduced.

2 Likes

The company itself has said that the demand for new products as a function of time is a gentle S-shaped curve, and I agree. That’s why not much can be concluded from these first figures yet. The most important thing is that the trend is upward.

Most vaccines are no-brainers for a rational actor. Covid has increased general awareness of the severity of infections and the benefits of vaccines. I believe that demand for this product does exist.

The market is justifiably concerned about cash sufficiency. Last time, a directed issue was organized. I will likely add at a price of 20 SEK (where the stock would be at roughly its 3-year OMXSGI level) and especially if a rights issue occurs.

2 Likes

2022 figures are out:

Revenue 9.7 M

Operating cash flow -70 M

45 M remaining in cash

Sales are still not picking up, and at this rate, the bottom of the cash reserves will be visible before Midsummer.

1 Like

It seems to be quite a slog. There seem to be plenty of launch-related expenses, and additionally, apparently some old SEK 1.9m from 2017 was written down. Mind you, net sales grew 84% from 2021 to 2022, so the operations haven’t been all for nothing; in Q4, the figure tripled compared to a year ago. But those big percentages aren’t game-changers if the underlying numbers are in the lilliputian category…

The company published its rough long-term sales targets for Strangvac for the first time: over SEK 1,000 million with a 65% gross margin. This roughly means that the usage of Strangvac would reach the level of the equine influenza vaccine.

Assuming a “long-term” period of 10 years and a 10% discount rate, the present value of that revenue is approximately SEK 400 million, resulting in a P/S of 2.5 at the current share price.

I haven’t bothered to update my DCF model, but the delay of the US launch and the current situation suggest a “back-of-the-envelope” fair value of SEK 30–40. The risk-free interest rate naturally has a massive impact on the pricing, and I did not expect the current environment.

Based on preliminary information, Strangvac is performing very well, and sales have started to gain momentum. These initial figures should not be extrapolated; instead, we should keep the S-curve in mind.

Naturally, other vaccine prototypes are excluded from the calculation.

My position is a good size, but I started buying at the SEK 20 level and have been adding at 10% intervals.

2 Likes

Interesting calculation. You would be willing to pay 1,500–2,000 MSEK for a company that has one product generating revenue with a present value of 400 MSEK? ![]()

The reason for today’s share price crash is likely Erik Penser, who halved their target price from a ridiculous level of 92–102 SEK to 48–54. Sales forecasts and margins fell drastically in their analysis, and cash flow positivity will be reached in 2025 at the earliest.

In my opinion, there is still more hot air in the stock than real future cash flow.

1 Like

Well, yeah, I guess no one uses that kind of “discounted P/S” very seriously; it was just a quick, back-of-the-envelope way to frame things. My buying decision is not related to that.

Sentiment around the stock is exceptionally depressed at the moment. A couple of years ago, it was the opposite when target prices of 100–300 SEK were being calculated. You have to buy stocks when they are cheap.

My long-term case with this relates to the effort to move away from the use of antibiotics in livestock and the company’s pipeline candidates related to that, and Strangvac provides a baseline for the stock’s valuation.

PS: Apparently you follow the company but don’t own it; have you made some kind of assessment of your own regarding its fair value?

1 Like

I used to own the stock, but I sold my shares when the company’s development started looking bad. I have regularly updated my own valuation based on actual figures. A couple of years ago, the company gave a significantly brighter outlook than it does currently. Based on that, I overestimated Strangvac’s sales many times over and underestimated the costs.

True. However, Intervacc is not cheap by any measure.

1 Like

Thanks for your opinion! Your decision to sell has clearly been the right one, at least for now. But at the same time, I suspect that valuing it based on historical sales makes this, like many other growth stocks, almost always look too expensive. That approach might be more applicable at the tail end of the S-curve.

In my view, you have to estimate long-term demand for the product, discount it, and add a decent margin of safety.

Today’s analysis from EPB isn’t bad at all. They used a 15% required rate of return.

1 Like

I do understand that realized sales figures are just the beginning and it’s not worth calculating any P/E ratios from them. The problem is simply that sales have started more sluggishly than expected. The amount of expenses is significantly higher than expected. Permitting processes have taken longer than estimated. These factors combined mean that we are well below the S-curve. Furthermore, worst of all, according to the company’s own announcement, the curve is lower than investors previously thought.