“If you have enough money that you could quit your job any day, then it’s a choice. And when you have that option, life looks quite different.” This is how millionaire Jenni Kynnös beautifully summarized the idea of financial freedom in the latest Finanssiflikat podcast, and let this also be the start of this new thread.

According to studies, we women are successful investors, but still relatively few in number. Especially here on this forum, we would like women’s voices to be heard more strongly, and we, along with the women of Inderes, thought that perhaps a dedicated thread could help. In this thread, you can bring forth a female perspective and ask or tell anything under the sun related to investing. We Inderes employees (me, @Kaisa_Vanha-Perttula, @Pia_Maljanen, @Sara_Antonacci, and @Isa_Hudd) will actively participate in the discussion and provide peer support as your money sisters. We will also publish new and interesting content related to money talk here. First, we recommend listening to the first two episodes of the Finanssiflikat podcast. We hope to generate active discussion here on the journey towards each of our own financial freedom

Both Finanssiflikat episodes listened to!

I must say that from my own experience, the mention in the first episode about how women are encouraged more to save than to invest really hit home. I was born in the 80s and received a “housewife” upbringing. For example, I’ve been told that a man’s job is to bring home the bacon and a woman’s job is to take care of the home. Additionally, I was even advised to find a rich man!

However, I am independent and want to succeed and get rich myself

Investing has always interested me, though I can’t really say where that interest comes from, certainly not from home. I opened a brokerage account as soon as I turned 18. I started with funds, but later sold them because choosing stocks myself was more appealing. Nowadays, my portfolio contains a few stocks and also funds. Trading is a hobby I enjoy, that I want to focus on and learn more about

I do think that this is about a fairly significant cultural evolution.

“Stay-at-home motherhood” has been a relatively short period, and all parties are struggling a bit with what the new norm will be in these matters in the future.

How responsibility is shared and how it is taken.

This could make quite a long story when considering the cultural revolution of family structures and its impact on taking responsibility for one’s own finances. General societal enrichment, etc.

Quite few women are prominent in discussions about money. It’s still quite a taboo. I don’t know if partner selection criteria affect what each person prefers to talk about openly.

But yeah.

I guess the number of investors will level out more here, as current elderly people divide their assets equally among all their children and both parents take increasingly equal responsibility for parenthood; equality is progressing rapidly due to the labor shortage.

Current women investors are probably those daring pioneers, which might slightly skew the statistics.

A guidance counselor once told me that research shows that representatives of a minority in a field are often in that field for the right reasons, not just because of a herd instinct driven by gender. They typically also have the motivation to demonstrate their expertise. That’s why they do well in the field. This applies to both women in male-dominated fields and men in female-dominated fields.

Good morning! Phew, that advice to find a rich man is quite a path to life and financial management but it’s great @TradingLady that you’re finding your own way and are here writing now. I didn’t get encouragement for investing in my upbringing either, mainly for saving. Through my own work, I then learned everything I’ve learned so far, when I started at 27. And learning definitely continues

And @Aili, that guidance counselor’s idea is indeed interesting and probably holds true. I guess the first major cultural breakthrough in financial equality was women’s participation in working life, the second then this wealth accumulation and financial management (i.e., more than just saving tips). There’s still work to be done, but we’re moving in a better direction

I pondered for a moment whether to respond to this. But since I lack self-preservation instincts, I’ve decided to challenge it a bit.

Reading history itself is somewhat imprecise, as history is often written as the history of the victors, of great men and wars. History is also often told differently depending slightly on the narrators’ perspective.

The “Dark Ages” were named from the perspective of Renaissance-era people. During the Renaissance, ancient philosophy was “rediscovered.” The Dark Ages were the period between the Renaissance and antiquity. If one critically examines the changes in people’s lives during the Middle Ages, some might disagree on whether the Middle Ages were truly so much darker and devoid of inventions than the Renaissance era that gave the period its name.

If we really think about it, what kind of good picture would one get of this era if one were to describe the present day through Trump and Putin? Through Emmanuel Macron and Xi Jinping.

The historical perception of Finns of our generation is also distorted by the recession of the 1990s. At that time, it was particularly rare for both parents to have jobs. Too often, neither did.

Regarding women working…

If we compare, for example, to the US before World War II, in the working class, everyone was at least part-time employed. In the middle class, most women left working life after getting married, and homemaking was desirable.

However, being middle class was rarer than being working class. The size of the middle class nevertheless grew in the 1920s until the Great Depression of the 1930s.

Before World War II, Finland was an agricultural country. On a farm, women’s work was as significant as men’s; it was about the division of labor. They were not officially registered for any jobs, but their daily contribution played a significant role in the family’s livelihood.

As I’ve recently delved into my own family history, while the leisure activities of notable men after their workday in the early 20th century involved the Civil Guards (Suojeluskunnat) and politics, women also participated in politics, and from the early 1920s onwards, their organization was Lotta Svärd.

Especially in the textile industry, young women were employed because of their small fingers. Of course, industrialization had not yet properly begun in Finland as it had elsewhere in the world.

According to narrative literature, Finnish women did not remain idle after their workday but played an active role in society.

I still remember from history lessons a propaganda video promoting Finland’s pension system. In it, an 80-year-old solitary woman was still working with her last strength in a match factory. A needs-based pension system was indeed established in Finland as early as 1937.

When World War II broke out, Lotta Svärd ran many functions essential for the war. The army was equipped under Lotta Svärd’s orchestration. Nursing and knitting mittens are often highlighted, but I know my grandmother worked at Finlayson’s bullet factory, and stories of Russian prisoners of war also stem from there. My other grandmother, in turn, managed a farm with her siblings and mother. In addition to the farm’s produce, a local black market for fabrics, which was valuable currency during the war, was operated in the attic.

After the war, Lotta Svärd was disbanded as part of the peace terms, and prominent figures of Lotta Svärd did not receive official recognition. They were not allowed to be invited to the Independence Day Presidential Ball (Linnanjuhlat) like war heroes until after the collapse of the Soviet Union. Voluntary defense of the homeland was branded as fascist by the left, even though the long-term existence of the Civil Guards (Suojeluskunnat) and Lotta Svärd was a critical resource in wartime struggles. It hasn’t been a particularly long time since their reputation was restored.

Unlike in the US, Europe entered a period of reconstruction after the wars. The war had significantly reduced the number of working-age men, and war reparations also had to be paid.

Whereas in the US, “Rosie Riveter” - women were encouraged to leave their posts and let men return to their old jobs. European women were simply needed as part of the workforce. There weren’t enough people to get everything done.

Although Lotta Svärd had been disbanded, during the war, women had been able to demonstrate their abilities and, according to family memoirs at least, integrated well into working life.

In addition to reconstruction, Finland had to industrialize. Up until the eighties, I myself have mostly heard of a positive attitude towards work, and looking at my family tree, almost all women also had a profession.

Somehow, I don’t recognize this in Finnish women, at least not up to the parents of the baby boomer generation, that it would have been a particular custom in Finland for women to stay home to care for children upon getting married.

In the 1950s, a strong “nuclear family” ideal emerged in the US, which significantly slowed women’s return to the labor market. The return to the labor market accelerated in the United States only in the 1960s and 1970s with feminist and equality issues.

In the United States, the female employment rate was 33%, most of whom were in part-time and low-wage jobs. In Finland, the measured employment rate in 1950 was 52%. To my knowledge, this figure does not include housewives working on farms. By 1990, the female employment rate rose to one of the highest in the world, reaching 72 percent.

For comparison, Finland’s overall employment rate in 2024 was 74 percent.

Then came the year of the Black Swan, and the overall employment rate plummeted to about 56%. In my opinion, this percentage should be viewed critically, as efforts were made to artificially boost the employment rate with various job center training programs. I personally guess and speculate that the actual employment rate has been even lower.

By 1999, the employment rate for both Finnish women and American women rose to 60%.

For Finnish women, because Finland began to recover from a difficult recession. For American women, because their education level and attitudes had changed.

Therefore, in my opinion, the bias in women’s investment enthusiasm and wealth development is not explained by women’s participation in working life.

If I remember correctly, in ancient times, salary was determined more by how you negotiated it for yourself. It was also thought that an older person should be paid more.

Perhaps it was also seen that if the man was still the main provider for the family, there would be more mouths to feed. If the man were paid more, his wife could theoretically more flexibly stay at home. The loss of income would not be as great.

Nowadays, companies have sought to dismantle the structure and base salaries and salary development more on tasks and performance. Age no longer affects your salary as decisively in a trend-like manner, but rather the responsibility you bear. Of course, with age, more responsibility tends to come.

It’s fair game that efforts have been made to equalize differences between genders, and fathers’ parental leaves also last almost as long as mothers’. It wasn’t long ago that there was apprehension when hiring young women, fearing they would soon go on parental leave, even if they weren’t planning to. I don’t know what the situation is today.

In my opinion, perhaps the biggest changes have occurred in mindset. Property is no longer seen as family property, typically managed by the father, with daily purchases overseen by the mother. Nowadays, property and wealth are seen as an individual’s personal assets.

A good change for everyone, in my opinion.

In summary of this long message: In my opinion, women’s participation in working life does not explain Finnish women’s more moderate participation in investment discussions.

This is probably my first longer post here on the Forum, and that’s why I thought a small introduction of myself as an investor might also be in order

My investment history goes back five years to the corona year 2020, when I decided to buy my first fund units. Looking back, one can say that’s where the spark for stock investing really ignited. Later that same year, I made my first stock picks, even though at that point I didn’t know much about stock investing. But you had to start somewhere

Somehow I managed to turn a hobby that had become important to me into a job, and before my career at Inderes, I worked at Nordnet with Finnish private investors. At the same time, I became interested in company fundamentals (business, industry, and other similar factors), and that’s how the fundamental analysis bug bit me Nowadays, I work with the same topic here at Inderes as an analyst.

During my short investment history, I have noticed that for me, one of the most important things about this hobby is the community. Being able to spar, get peer support, and valuable lessons from other investors has been extremely important!

As @Marianne_Palmu previously stated, we women are still underrepresented in the stock market (at least for now). Namely, according to studies, the proportion of women stock investors has remained around one-third (12/2024: ~35%) over the last decade, even though the total number of stock investors has grown rapidly.

So there’s plenty of room for women in the stock market, meaning we need action! I strongly believe that social interaction, peer support, and the examples of other women are important for female investors and at the same time promote women’s interest in investing. We at Inderes intend to work towards this.

Hopefully, many women interested in investing, and especially stock investing, will find this thread!

Speaking of fundamental analysis, I also wrote an article on the topic. The idea behind stock picking is to achieve better returns than the market, but on what basis should one actually pick stocks? There are several ways to pick stocks, but the majority of investors aim to find investment targets specifically based on fundamental analysis

In fundamental analysis, one examines:

the company’s business operations

industry dynamics and competitive factors

the company’s competitive advantage

the company’s historical performance in light of key figures, and

management and other similar real-world factors.

Based on these factors and the company’s historical key figures, forecasts are made regarding, for example, future earnings development and cash flows. Based on these forecasts, the aim is to determine the company’s “fair value”, key value drivers, and risks.

Fundamental analysis thus differs significantly from, for example, technical analysis, which focuses on the stock’s price development on the stock exchange and investor behavior. If one considers examples of fundamental analysis, these include, for instance, Inderes’ comprehensive reports.

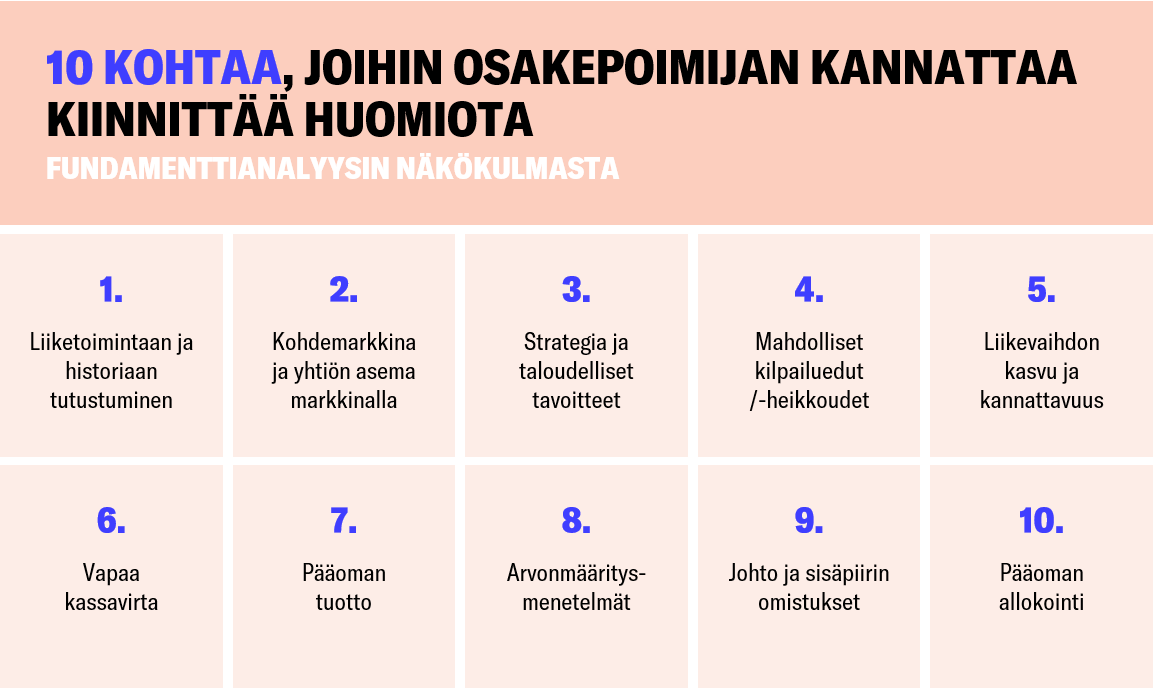

What all should one pay attention to before making an investment decision? And where can one find the necessary information to support decision-making? I have listed 10 points below that can help in finding a suitable investment target specifically from the perspective of fundamental analysis

1. Familiarizing oneself with the business and history

In what industry does the company operate and what is the business’s earning logic? How has the company developed historically and what does its current financial situation look like?

2. Target market and the company’s position in the market

How large is the relevant market and what is the company’s market share? Is it possible to create value in the market? What is the expected growth rate and general profitability level? Does the company need to gain market share to sustain growth?

3. Strategy and financial targets

How does the company aim to differentiate itself from competitors and create value within the industry? Are the financial targets aligned with the strategy? How realistic are the targets?

4. Potential competitive advantages/weaknesses

One of the most essential tasks for a stock picker is to assess whether the company has competitive advantages. However, genuine and sustainable competitive advantages can be surprisingly difficult to identify, and evaluating them requires digging deeper than the surface.

What are the company’s competitive advantages (e.g., business key figures, market leadership, pricing power, strong brand, product differentiation) based on, and are they sustainable? Additionally, it is important for a stock picker to assess the company’s most significant weaknesses and risks.

5. Revenue growth and profitability

Is the company’s revenue growing or stagnating? Is the growth sustainable and does it also reflect in the company’s profitability? Is revenue growth visible in the lower lines of the income statement, or does growth destroy shareholder value?

6. Free cash flow

In short, this figure is particularly important for a stock picker because a company can use free cash flow for dividend payments, share buybacks, acquisitions, or alternatively, for debt reduction or strengthening the balance sheet.

Free cash flow often also provides a more realistic picture of a company’s financial situation compared to the income statement, which can be adjusted through accounting tricks. By examining cash flow, one can detect potential problems before they are reflected in the income statement.

7. Return on capital

Creating shareholder value is one of the most important tasks of a listed company. A stock picker should therefore examine the company’s return on capital. A high return on capital relative to the industry often indicates a company’s potential competitive advantage and thus quality.

8. Valuation methods

Several different methods are available for valuation, but the best known are valuation multiples, the DCF model, and sum-of-the-parts. Among investors, the most commonly used methods are valuation multiples.

Valuation multiples provide indications of whether a stock can be considered cheap or expensive compared to historical levels or relevant peers. There is an abundance of material on valuation methods worldwide; there are many perspectives, and one can always learn more.

9. Management and insider ownership

The company’s management plays a significant role in its success, and attention should be paid to their expertise and the quality of their leadership. The role of the owner is also important, as ultimately the owners determine the direction in which the company is to be taken.

10. Capital allocation

For a company’s long-term success, successful capital allocation is critical. A stock picker should therefore examine how the company uses its retained earnings — for growth investments or profit distribution?

In the long term, a good measure of capital allocation is the total return of the stock, although in the short term, the stock price and its valuation are primarily driven by market forces.

–

Here is a small overview of what a stock picker should pay attention to from the perspective of fundamental analysis. As I mentioned earlier, there are several ways to pick stocks, and fundamental analysis is just one of them

I myself, in the midst of the corona pandemic, had to temporarily put my entire business on hold due to an industry sensitive to restrictions, and do some grunt work in between. There was a lot of downtime, and I was happily getting paid while listening to Jasmin Hamid on my headphones and thinking, what the hell, girl, why not.

As a journalist’s daughter, I’ve always watched world events with a keen eye and liked to play with the idea of ‘weak signs of the future today’.

It didn’t start very rosy for my own savings, as the stock market immediately took a big dive, but a little later, a small inheritance came through, and things were already a bit more under control anyway.

Graphs and activities related to comparing numbers are interesting, and for entertainment, I prefer to lurk here on the forum vs other social media platforms; content that is factual, informative, and not so emotionally provocative (as long as you let certain threads be ). Let the wiser ones comment, I read and learn.

I am certainly no analyst, and surely better returns could be achieved if one focused on those numbers even more precisely, but I’m not completely clueless either. In my opinion, I have a good balance of risk and security in my portfolio, and it’s always fun to play with the idea that one of those riskier, small-cap stocks with good future potential in my eyes would really rocket like a shuttle to Venus and so on.

If not, no big deal; it’s fun entertainment, and it seems to accumulate inevitably over time. I make actual moves quite rarely; I’m more of a patient long-term holder than an eager short-term trader.

From this story, one can see that the more women who invest speak up, the more others will dare to join in. It wouldn’t have even crossed my mind before, even though I have a commercial education and everything.

I thought it was something for ‘suit men’ where you’d definitely get burned, but it hasn’t gone too badly so far.

Exactly, and more generally, that people have more opportunities to identify with others.

I’m such a terrible and mischievous person that whenever someone justifies their role by saying,

“This is so terribly difficult and there are too many moving parts now. Let me handle it.”

Silently smiling, I wonder if this person is really in the right role if things feel so difficult, or if they are so easy that they fear I’ll soon do their job better.

In the beginning, all tasks feel difficult and make you sweat as you try to figure out how things work. Investing is something that is scary to learn because there’s a good chance of losing money along the way.

Inderes already stands out positively from the rest of the banking world, as they wear hoodies instead of blazers.

It’s one thing to recognize the limits of one’s own skills. That’s quite easy to do with this hobby. For me, bigger game-changing insights have been:

The bank won’t help me get rich.

Analysts live on the information given to them, which in some cases may even be less than the information of other workers.

Only my cat has a functional, all-encompassing, information-analyzing crystal ball using a modern AI algorithm with the mysticism of old times. Unfortunately, it’s sometimes broken too.

So, in the end, we all live on limited information.

Hi! No one is excluded from this thread, as we are also on the side of free speech. So, welcome to discuss investing and finance

Regarding Jasmin Hamid’s selection, that’s good news. I’ve been with her on a few joint projects (the latest being Yle’s Stock Market Day podcast from December), and she has good insights as a private investor. It remains to be seen what kind of form Rahapodi will take with Jasmin’s selection

I didn’t have any curfews as a child, but Salkkarit started at half past seven and the last bus before the night fare left at half past eleven.

Jasmin Hamid is a new and old role model. Her experience in hosting gigs related to investing is undeniable.

I’ll say directly what many others, in their political correctness, might not dare to.

Someone who has attended the Theatre Academy is not the traditional choice for a broker to speak about money. There has seemed to be a peculiar division in these matters. You speak on Yle like leftists, we speak with economists like rightists in our own forums. Then we fight when we accidentally meet.

Let’s be direct, my own openly critical attitude towards “suit men’s” comments on financial matters was born precisely from the criticism that Hamid, Mähkä, and other female figures on Instagram received at the time.

If investing is for everyone, doesn’t everyone have the right to talk about investing?

Jasmin Hamid seems like a straight-A student with extensive experience in performing and hosting, as well as personal experience in saving, investing, getting started, and the effects on personal finances.

Success, in my opinion, depends on how well the chemistry with the co-host works out and how captivating and timely topics they manage to choose.

Rahapodi already has many listeners, and Jasmin Hamid will surely appeal to a new kind of audience. I will follow with interest how Rahapodi develops.

I just read an interview with Jasmin in Talouselämä, where she mentioned that one’s investing style can vary depending on their life situation. We discussed similar things with Ronja Roms in a recent episode of Finanssiflikat. Ronja experienced a certain kind of pause, and I experienced a loss, which made me approach wealth accumulation in a new way. This was a really inspiring discussion and also opens up real estate investing. Let’s be cheerleaders for each other too

I just watched Ronja’s interview, and right at the beginning, she talked about how she was buying her first home but couldn’t get a loan from the bank. She felt belittled at the bank. I can relate to this myself when I was buying a home. I couldn’t even get a loan promise from my bank at the time, even though that bank’s advertisements for loan promises were heavily featured on TV. Of course, I asked for offers from other banks too and received an offer from each, from which I chose the best one. During the loan negotiations, I was very directly questioned about whether I really intended to buy a detached house alone and how I planned to manage, especially with renovations. If I hadn’t been so well prepared, I probably wouldn’t have gotten a loan from anywhere. I was just over twenty at the time and just stated that it was unlikely I would live there alone for long, and that went down well with the bank officials.

Around the same time, a couple of my male friends were also buying their first homes, but for them, it wasn’t a problem for the bank that they were buying alone.

I also had carefully prepared calculations of my income: what they would be if I became unemployed or had to switch to a lower-paying job. I had estimated potential expenses and renovation costs very thoroughly. It also helped that I was already in a permanent job in a male-dominated field, where salaries are on average better than in traditional women’s fields. Additionally, I can do some renovations myself, and I had stocks in my investment portfolio.

Another thing that stuck in my mind from Ronja’s speech was how much criticism she received for speaking openly. This is one reason why I don’t want to talk much about investing and trading on social media. Trading easily sparks confrontation, but it’s a passion for me and a way to relax in my free time, and I don’t need extra criticism for it. I don’t mean that one shouldn’t disagree and challenge constructively through discussion, but specifically, I couldn’t handle that kind of harsh criticism. However, I have dared to publish a few threads about trading on X, and it has been wonderful to notice that there has been encouragement and good feedback there.

I have sometimes tried to discuss investing at the coffee table at work. It wasn’t shot down, and I was even asked for more, but I guess I couldn’t explain it very well, because investing was perceived as a difficult and complicated thing that takes a lot of time to learn. Or perhaps the problem was that people didn’t want to bother finding out about things.

I fully subscribe to the idea that it would do everyone good to have 5 cheerleaders supporting them. Unfortunately, most often, you find those who doubt and say: “Are you really sure, it’s not worth it.”

The video also spoke excellently about the need to be able to explain things so that everyone understands, without using difficult terms. I struggle with this myself; I have a very poor memory and ADD, and terms just don’t stick in my head.

I want to highlight a few sentences from Ronja that I think apply to everyone: “We can have everything, but not everything at once.” “I invest so I can live the life I hope for.” “It’s okay for your goals to change, and they are allowed to change – that’s not a failure.” “The best day to start is today.”

Especially the idea of five cheerleaders resonated with me; everyone would truly benefit from a financial motivator who encourages them to invest/try. Inspired by that, I volunteer to be a cheerleader if anyone needs one!

Good idea to try a thread like this for women, even if we men can participate sometimes too. If there are any women here who are pondering their own identity and relationship with money and investing, I’d like to say something from a man’s perspective.

Generally, I don’t like it when people are separated into groups based on some characteristic and only the needs and benefits of one group are emphasized; it’s not equal, even if the intention is good. However, this is a sensitive topic: money and women, gender roles. It evokes emotions.

As long as women are belittled in these matters, and as has been stated earlier in this thread, there is no equality. That’s why I think it’s good that efforts are being made here to specifically encourage women to form their own identity in relation to money and to be able to be like men, to manage on their own. Inderes’ female employees are, in my opinion, excellent role models and examples for other women and girls, and why not for boys and men too! Such models inspire respect, at least in me, that one dares to stand for equality and knows one’s own worth. This also benefits men. An unequal society is not a well-being society.

One can frankly speak out against stupid jokes or comments made by men and women alike, and state that a woman is just as capable as a man of handling her own affairs, and in this case, investing. And as Marianne mentioned, women as a collective are better investors due to more controlled risks, less impulsive actions, and more rational decisions. A big reason is also humility towards the market and a lack of arrogance, which is more common in men. So, in this case, caution and skepticism are strengths.

In Finland, equality is relatively advanced, and Finnish women are, in my opinion, truly admirable types because they have taken their lives into their own hands more than elsewhere, roughly speaking. I say this because, conversely, prejudices and narrow molds for genders have also caused me shame about my own gender and that I should now be something specific. And role models can help combat this. Only a society where everyone has the same rules, expectations, and where everyone is treated equally can, in my opinion, function well in terms of individual freedom and psychological well-being. At least I don’t like it when I, as a man, and another, as a woman, have different “rules” and roles. Everyone is their own individual, regardless of gender, and does what they see fit within common rules. Together we can stand side by side more than alone.

Thanks for the encouragement. A couple of years ago, there was a survey on the Forum, according to which only about 6% of the Forum’s users are women. I would therefore view this thread purely as marketing for women. I don’t know if the percentages have changed in a couple of years, but when reading the coffee room, it still feels like men already have their own thread and topics of interest to women easily get lost there. So it’s good that something like this was created.

I already invest. So I wouldn’t necessarily need encouragement to start. Instead, I haven’t told anyone that I invest. It’s encouraging when some women dare to talk about investing with their own names and faces, and not from behind a nickname, like the undersigned. It would be nice if this thread could become its own virtual community.

Thanks for this post! I’m an 80s kid too, and I recognize a lot of things from your answer. As an Ostrobothnian, for example, I’ve been advised to learn enough herring recipes so I could get married.. …

I also still remember how my study friend in Germany wanted to tell me something important. Her message was: “before you go back home to Finland: find yourself a rich German man! (since Finland is such a poor country)”… Then you’ll always be able to afford horses."

I remember answering “Ich kann meine eigene Geld verdienen”… To which my study friend, almost offended, stated that she didn’t mean any harm at all. She just wanted to help, and give good advice.

Another excellent episode from Finanssiflikat, thank you!

Marianne’s important point that saving goals shouldn’t be set in stone particularly stuck with me. We have a life to live, and that’s why it’s good to be prepared, but also to be kind to oneself at the same time.

Pia nicely said that life situations change, and that’s why investment goals and strategies should be reviewed regularly. The reasons and values for investing can vary at different stages of life, so it’s completely natural to make changes to investing as well.

Sara brought up an important reminder for young people: starting to invest early allows one to focus on other things later in life.

Isa’s story about stopping and realizing that money doesn’t just appear in the account, but expenses keep running, and starting to think about how to secure one’s future, was particularly important. Even if you can’t save large sums, even a small saving is valuable. You never know what life will bring.

Returning to the piggy bank saving mentioned at the beginning of the episode, it brought back good childhood memories for me. I was perhaps 4–5 years old when I saw a small electronic handheld game in the village shop, where you had to dodge cars by changing lanes, and as the game progressed, it sped up. I wanted it badly, but my parents said that I had to save the money and buy it myself.

I remember well how frustrated I was that the piggy bank was filling up sooooo slowly, and at the same time, I was afraid someone would buy that game because it was the only one left.

After what felt like an eternity, the piggy bank was full. My mother and I went to Postipankki to empty it, and I received my first banknotes: blue ones, and one red 50 markka note, because as a spirited girl, I had told the bank clerk I wanted a red note (Red was my favorite color at the time. Although I originally meant a 500 markka note, I didn’t understand then that there weren’t such sums in my piggy bank ).

From the bank, we headed straight to the village shop by bicycle. I was excited but didn’t understand the value of money, nor did I know how much I should give to the shopkeeper. Bursting with excitement, I pulled out my velcro wallet and handed over banknotes one by one, until the shopkeeper laughed and said that was enough. I would even get change back! The game became one of my favorite toys, and certainly part of the reason was that I had saved the money myself to buy it

This is my earliest money-related memory. How about others, what is your first money memory?