Diilejä tullut viime aikoina. Jokohan on aika alkaa tarkastelemaan ennusteita?

Ukrainan jälleenrakennus on mielenkiintoisen kokoinen mahdollisuus Honkarakenteen kokoiselle firmalle (Mcap 18me). Honkarakenteella on vuosikymmenten kokemusta viennistä.

“Aiesopimus on voimassa seitsemän vuotta, ja sen voimassaoloa voidaan jatkaa osapuolten yhteisellä sopimuksella”

2 tykkäystä

Tässä on Aten kommentit Honkarakenteen tuosta “Ukrainan aiesopimuksesta”. ![]()

EDIT:

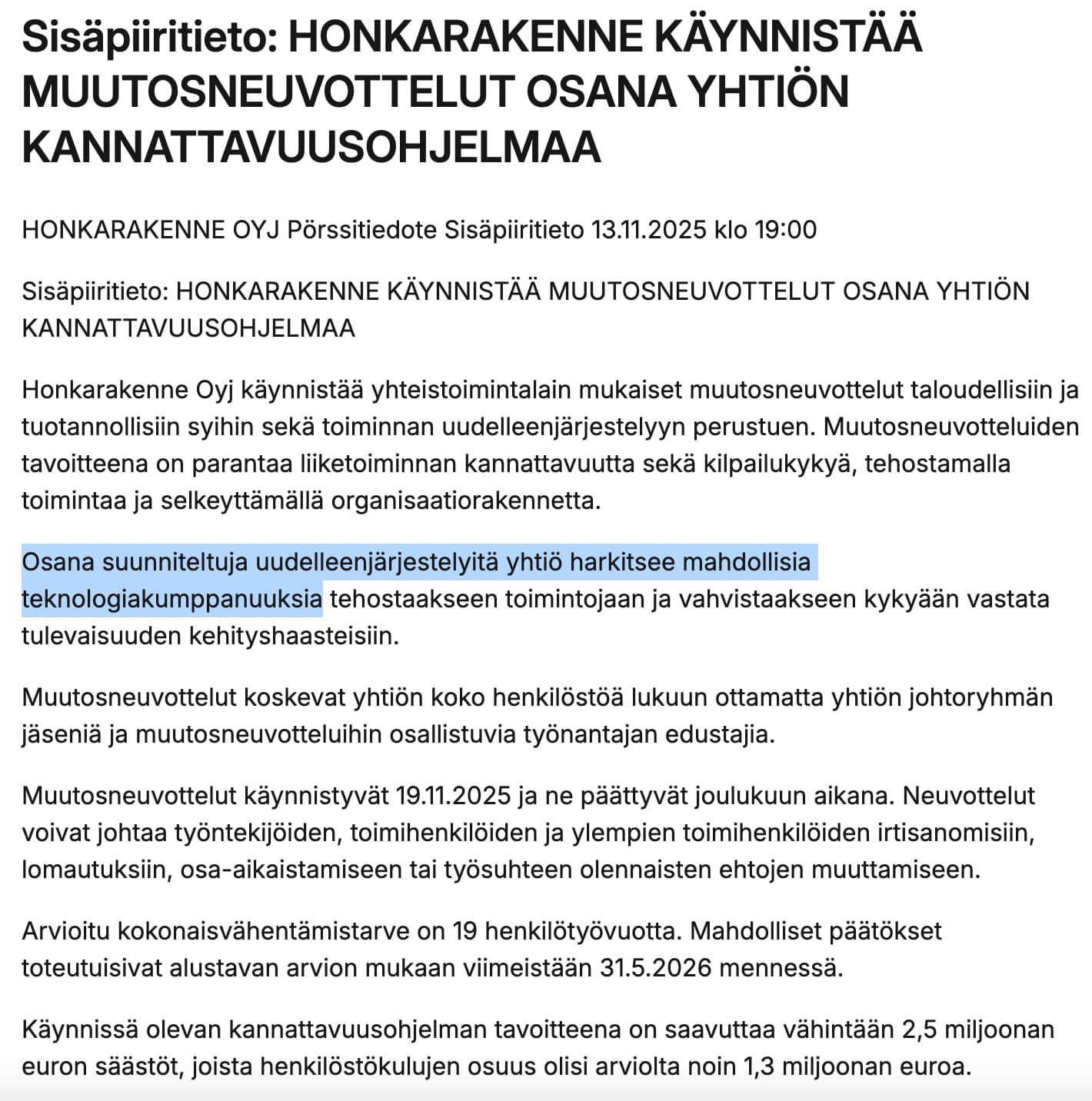

Tässä on Aten kommentit myös siitä, kunHonkarakenne käynnistää muutosneuvottelut.

2 tykkäystä

Atte on tehnyt uuden yhtiöraportin Honkarakenteesta. ![]()

Honkarakenteen kuluva vuosi jää tuloksen osalta heikoksi vallitsevan markkinatilanteen johdosta. Myöskään näkymät lähitulevaisuudessa eivät viittaa tilanteen paranemiseen, minkä seurauksena olemme tarkistaneet vuoden 2026 ennusteitamme alaspäin. Ennusteissamme yhtiön kannattavuus kuitenkin vahvistuu tulevina vuosina viennin kasvavan osuuden sekä toteutettavien tehostustoimenpiteiden ansiosta. Parantuva tuloskehitys normalisoi arvostuksen neutraalimmalle tasolle vuoteen 2027 mennessä. Toistamme 2,7 euron tavoitehintamme ja vähennä-suosituksemme.

1 tykkäys

2 tykkäystä

Siitä vähän Karstulan tehtaan esittelyä => https://www.youtube.com/watch?v=oG5mEgd6AY0

3 tykkäystä

Tässä on Aten kommentit Honkarakenteen eilen tiedottamasta negarista.

Honkarakenne antoi torstaina tulosvaroituksen ja laski vuoden 2025 taloudellista ohjeistustaan. Ohjeistuksen laskun taustalla on toimitusten siirtyminen loppuvuodelta 2025 vuoteen 2026 asiakkaiden lupa- ja rahoitusehtojen pitkittymisen vuoksi. Uusi ohjeistus jää aiemmista ennusteistamme, mikä luo laskupainetta vuoden 2025 ennusteisiimme. Tulosvaroituksen vaikutus näkemykseemme on rajallinen, sillä kuluva vuosi on Honkarakenteelle joka tapauksessa välivuosi. Toimitusten siirtyminen ensi vuodelle tukee myös odotuksiamme kannattavuuden paranemisesta. Päivitämme yhtiön ennusteet lähiaikoina.

2 tykkäystä

Tässä on Atelta yhtiöraportti negarin jälkeen. ![]()

Honkarakenne laski viime viikolla vuoden 2025 ohjeistustaan liikevaihdon ja liikevoiton osalta. Laskun taustalla oli ajoitukselliset tekijät kun aiemmin joulukuulle suunnitellut viennin toimitukset siirtyvät ensi vuodelle johtuen asiakkaiden lupa- ja rahoitusehtojen pitkittymisestä. Olemme laskeneet kuluvan vuoden ennusteitamme tulosvaroituksen johdosta. Korkeamman katteen viennin toimitusten siirtyminen ensi vuodelle sekä yhtiön tehostustoimet tukevat kuitenkin ennustettamme ensi vuoden tuloskäänteelle. Vuosien 2026-2027 EV/EBIT-kerroin asettuu ennusteillamme noin 8x tasolle, mikä sijoittuu hyväksyttävän arvostushaarukkamme (7–9x) sisälle. Hinnoittelu vaikuttaa täten neutraalilta, emmekä näe tuotto-odotusta vielä houkuttelevana käänteeseen liittyvät epävarmuustekijät huomioiden. Toistamme 2,7 euron tavoitehintamme ja vähennä-suosituksemme.

Laajennus hotelli busineksien pariin. Oisko seuraavana Rovaniemelle, joka kamppailee majoitusongelmien kanssa? https://www.inderes.fi/releases/tornio-haaparanta-nousee-lapin-seuraavaksi-matkailukeskittymaksi-honkarakenne-vastaa-kasvavaan-kysyntaan-suomen-suurimmalla-hirsihotellilla

4 tykkäystä

Atte on tehnyt Honkarakenteesta uuden laajan raportin. ![]() Tuttuun tapaan tämäkin laaja rapsa on kaikkien luettavissa.

Tuttuun tapaan tämäkin laaja rapsa on kaikkien luettavissa. ![]()

Honkarakenteen vuosi 2026 kääntyy ennusteissamme yhä laajalti välivuodeksi kotimaan markkinan säilyessä haastavana. Ennustamme yhtiön pääsevän merkittävämmin tuloskasvuun kiinni 2027-2028 viennin panostusten konkretisoituessa vahvemmin toimituksiksi. Lisäksi odotamme kotimaan markkinan elpyvän asteittain. Kuluvana vuonna vaatimaton tulostaso nostaa arvostuskertoimet erittäin korkeiksi. Ennusteillamme vuoteen 2027 katsottaessa kertoimet kuitenkin neutralisoituvat karkeasti hyväksyttävän arvostushaarukan sisälle. Etenkin viennissä onnistumiseen liittyvien epävarmuuksien vuoksi riski/tuotto-suhde on kuitenkin näkemyksemme mukaan vielä epäedullinen. Toisaalta vahva tase toimii yhä puskurina heikommassa skenaariossa. Säilytämme tavoitehintamme 2,7 eurossa ja suosituksemme vähennä-tasolla.

Rapsasta lainattua:

Käännetarina hakee yhä konkretiaa

Kuluvan vuoden jäädessä suurilta osin välivuodeksi painotamme arvonmäärityksessämme vuoden 2027 ennusteitamme. Osakkeen arvostus ei saa tukea kuluvan vuoden päivitetyistä ennusteistamme tulostason jäädessä yhä vaisuksi. Honkarakenteen arvostustaso on tulevina vuosina näkemyksemme mukaan kohtuullinen ottaen huomioon ennustamamme huomattavan tulosparannuksen syklin pohjilta. Kuitenkin riskikorjattu tuotto-odotus jää vaisuksi, huomioiden käänteeseen liittyvät epävarmuudet koskien kotimaan markkinatilannetta, yhtiön onnistumista vientikaupassa sekä tavoiteltujen kulusäästöjen toteutumista. Osakkeen odotuksiamme suurempi nousupotentiaali seuraavan vuoden aikana edellyttäisi ennusteitamme voimakkaampaa käännettä niin kotimarkkinalla kuin viennissäkin. Toisaalta merkittävämpää riskiä alaspäin rajaa näkemyksemme mukaan edelleen yhtiön vahva taseasema.

2 tykkäystä

“Hyvä kehitys on jatkunut tänä vuonna: tammikuun myynti oli jo kuun puolivälissä 50 prosenttia edellä koko viime vuoden tammikuun myyntiä”

Varsin positiivisen kuuloinen kommentti kotimaista raksaa ajatellen DEN Finlandilta:

3 tykkäystä

Atte ja Iikka keskustelivat Honkarakenteesta uuden laajan rapsan tiimoilta. ![]()

Aiheet:

00:00 Aloitus

00:12 Honkarakenteen sijoitusprofiili

02:00 Markkinat ja liiketoimintamalli

04:03 Kilpailutilanne

05:40 Vientikauppa

07:09 Iso tappiopuskuri vähentynyt

08:04 Ennusteet

09:25 Suositus on vähennä

4 tykkäystä

" Rakennustutkimus RTS Oy 1.1.2026 julkaistun Hirsitalomarkkinat 2022–2025 -raportin mukaan teollisen hirren tilauskanta kasvoi euromääräisesti peräti 46 prosenttia edellisvuoteen verrattuna."

3 tykkäystä

Toimitusjohtaja vaihtuu. Jokohan saataisiin ulkopuolinen toimitusjohtaja.

https://www.inderes.fi/analyst-comments/honkarakenne-toimitusjohtaja-vaihtuu

2 tykkäystä

Tässä on Aten ennakkokommentit, kun Honkarakenne kertoo H2-tuloksestaan torstaina 12.2.2026 ![]()

Odotamme yhtiön raportoivan joulukuussa annetun tulosvaroituksen mukaisen tappiollisen tuloksen, jota painoivat loppuvuodelta kuluvalle vuodelle siirtyneet merkittävät vientitoimitukset. Katseet raportissa kohdistuvat erityisesti tilauskannan kehitykseen sekä näkymään vuodelle 2026.

Pari kommenttia tämän ketjun viimeisimpiin uutisiin, itsellä on tuttu hirsialalla ja häneltä saan kyllä aina hyviä mielipiteitä/näkemyksiä.

Tämä taisi olla lähinnä Ollikaisen mainostiedote. Hienoa Ollikaiselle, heillä näyttäis menevän ihan hyvin. Yleisesti alalla ei todellakaan ole tällä hetkellä mitään hurlumheitä. Joo, Lappiin menee mökkejä ja okt-rakentaminen on pahimmasta koomasta herännyt mutta ei tuo 46% kasvu ole vielä tarpeeksi kun pohja on ollut niin syvällä. Pitää myös muistaa että kasvu ei paljoa lämmitä jos sillä ei saada katetta. Fakta on se että Kontiolla on iso tehdas vajaakäytöllä ja heidän pitää saada sinne myyntiä → katetta poljetaan naurettavan alas. Kontio on isoissa vaikeuksissa, talvella ollut taas lomautuksia, vuosi sitten 25% yhtiöstä myytiin osakeannilla 3 miljoonan hintaan Asko Schreylle. Itse olen käsittänyt että juuri Kontion tilanne aiheuttaa sen että hirren hinta on matala, joten kaikki saa kamppailla kannattavuuden kanssa. Hirren kysyntä on kovaa kun sitä halvalla saa, kauppaa saa kyllä ne jotka suostuu halvalla myymään. Miksi ostaa puutaloa kun hirsitalokin on kohtuuhintainen? Talonrakentajalle on ehdottomasti hirsipaketeissa ostajan markkinat.

Saarelainen on ollut hyvä toimari Honkarakenteelle, yhtiö kärsi kilpailijoihin verrattuna enemmän venäjän hyökkäyksestä. Tämän oman tuttuni mukaan hirsialalla toimarin kannattaa olla talon sisältä, on erittäin tärkeää että toimarilla on hyvä näppituntuma asiakkaisiin, tuotantoon, markkinaan, myyntiin yms. Parhaita tuloksia alalla tekee yrittäjävetoiset firmat. Eri alalta tulleella toimarilla on usein nätisti sanottuna haasteita pysyä tilanteen päällä. Itse osakkeenomistajana toivoisin että talon sisältä löytyisi joku pätevä ja intohimoinen tyyppi luotsaamaan laivaa.

En Honkarakenteen tilannetta erityisen hyvin tunne juuri nyt, mutta itse en näennäisesti hyvien uutisten tai kilpailijan spinnauksen perusteella kiirehtisi ostonapille.

3 tykkäystä

Tässä on Atelta tuore yhtiöraportti Honkarakenteesta H2:n tiimoilta. ![]()

Honkarakenteen toisen vuosipuoliskon tulos oli odotetun heikko ja karkeasti linjassa yhtiön joulukuussa antaman tulosvaroituksen kanssa. Ohjeistus oli pitkälti odotustemme mukainen joskin kannattavuuden ohjeistushaarukka vielä ennusteitamme pehmeämpi. Vuosi 2026 oli jo aiemmissa ennusteissamme välivuosi, emmekä ole tehneet merkittäviä muutoksia pidemmän aikavälin ennusteisiin. Säilytämme tavoitehinnan 2,7 eurossa ja suosituksen vähennä-tasolla.

1 tykkäys

Tässä on Aten kommentit siitä, kun nykyinen toimari siirtyy Honka Japanin johtoon. ![]()

Honkarakenne tiedotti torstaina yllättävästä käänteestä koskien toimitusjohtaja Marko Saarelaisen tulevaa roolia ja yhtiön hallituskokoonpanoa. Saarelainen ei olekaan käytettävissä yhtiön hallitukseen tai sen puheenjohtajaksi, vaan hän siirtyy konsernin toimitusjohtajan tehtävästään suoraan Japanin tytäryhtiön Honka Japan Inc:n toimitusjohtajaksi. Pidämme muutosta yllättävänä suhteessa aiempaan nimitystoimikunnan ehdotukseen, mutta siirto on looginen Saarelaisen vahvan Japani-osaamisen vuoksi yhtiön tavoitellessa sieltä kasvua. Näkemyksemme mukaan tilanne on kuitenkin epävarma, sillä yhtiölle ei ole toistaiseksi nimitetty tulevaa toimitusjohtajaa eikä hallituksen puheenjohtajaa.

1 tykkäys

Tässä on Atelta kommentit uudesta Honkarekenteen toimarin nimityksestä.

Honkarakenne tiedotti maanantaina nimittäneensä Magnus Hindströmin yhtiön uudeksi toimitusjohtajaksi. Hindström aloittaa tehtävässään 3.8.2026 ja siirtyy Honkarakenteelle Metsä Woodin Kerto LVL -myynnin johtotehtävistä. Pidämme nimitystä onnistuneena ja loogisena askeleena, sillä Hindströmin vahva kokemus kansainvälisestä puutuotekaupasta tukee yhtiön strategiaa hakea kasvua vientimarkkinoilta. Samalla nimitys hälventää yhtiön johdon ympärille syntynyttä epävarmuutta sen jälkeen, kun edellinen toimitusjohtaja Marko Saarelainen ilmoitti siirtyvänsä pois toimitusjohtajan tehtävistä aiemmin tänä vuonna.

1 tykkäys