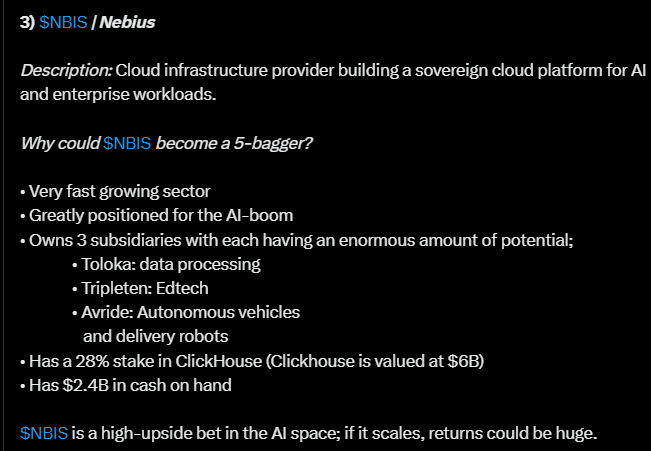

Here’s a view on Nebius spotted from the tweet thread “10 stocks which could become 5-baggers”.

The tweet highlights already familiar things, such as how Nebius offers cloud infrastructure for AI and enterprise applications and operates in a rapidly growing sector.

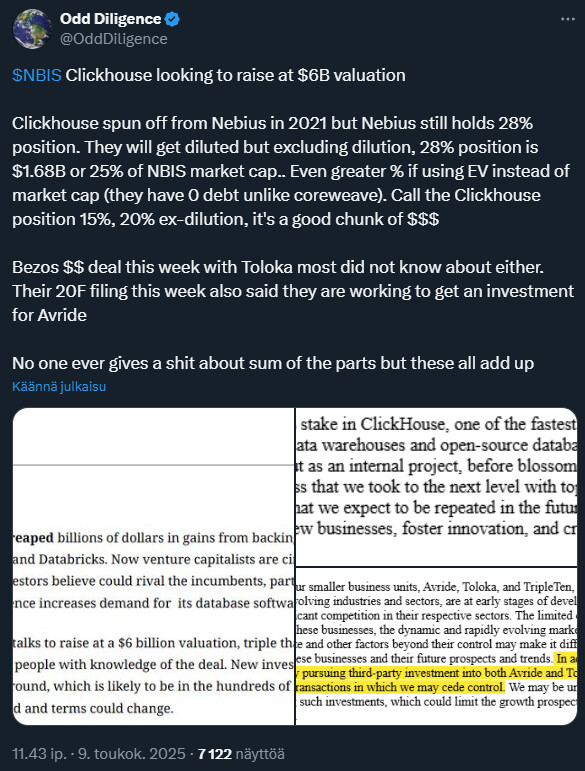

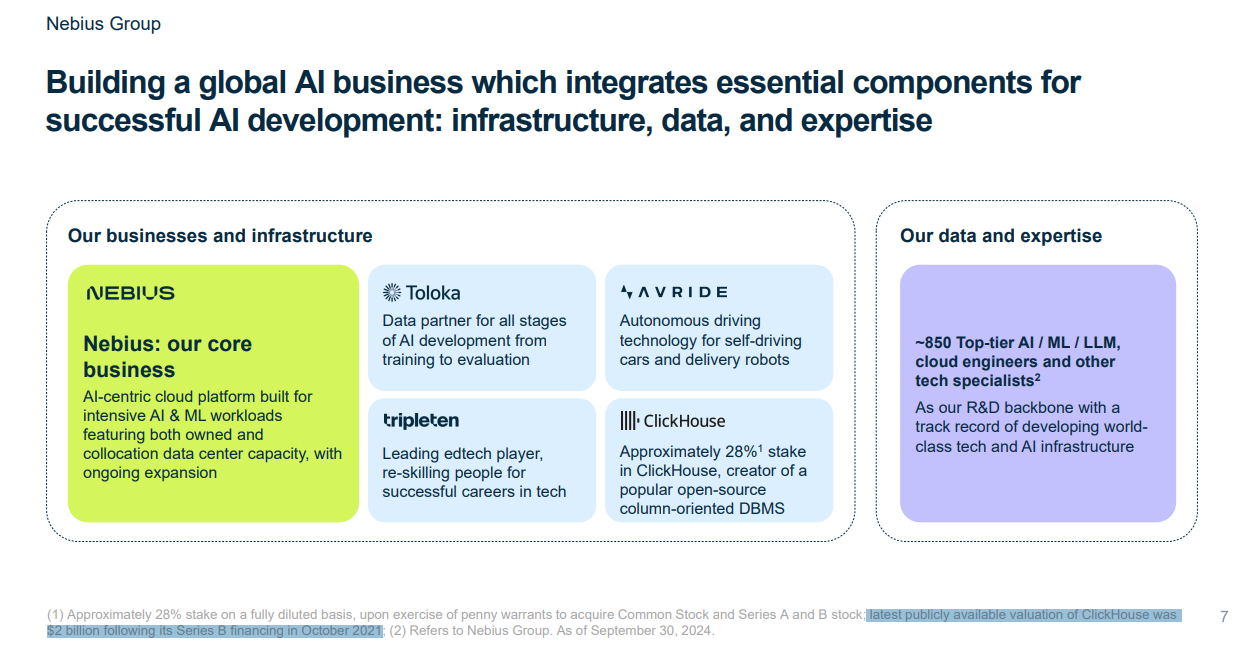

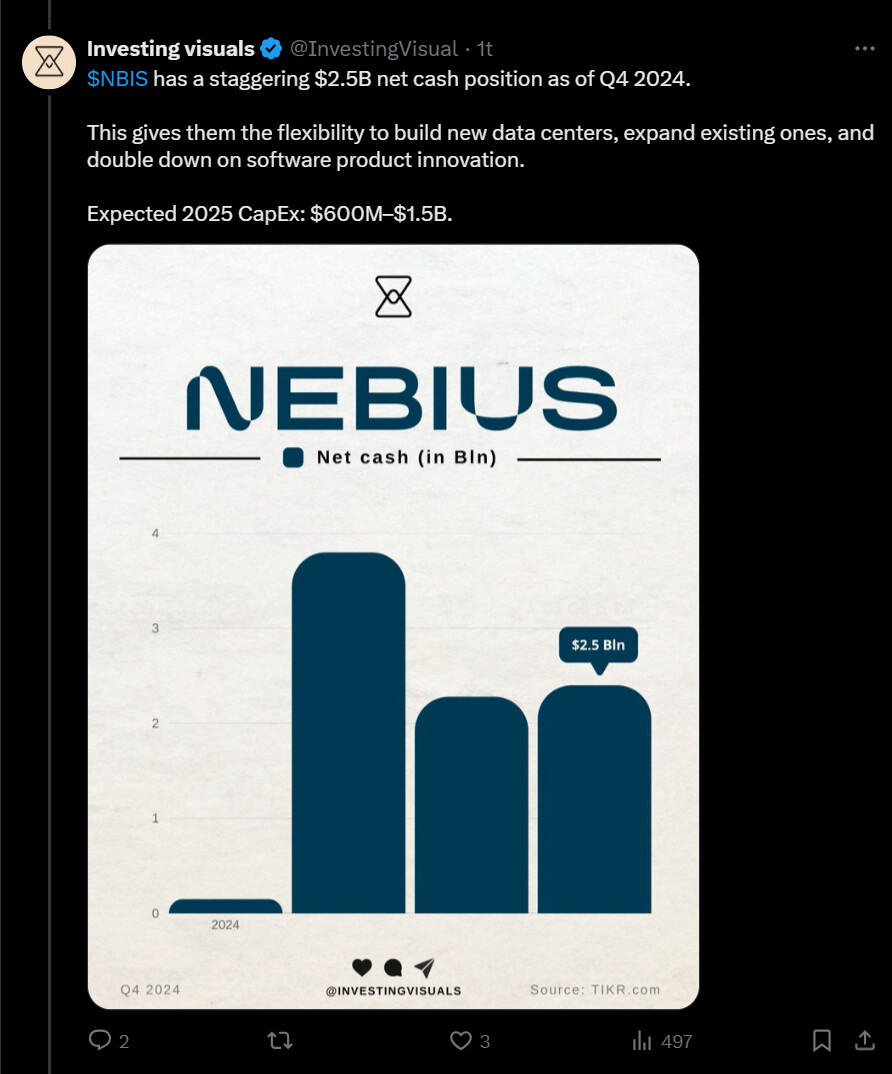

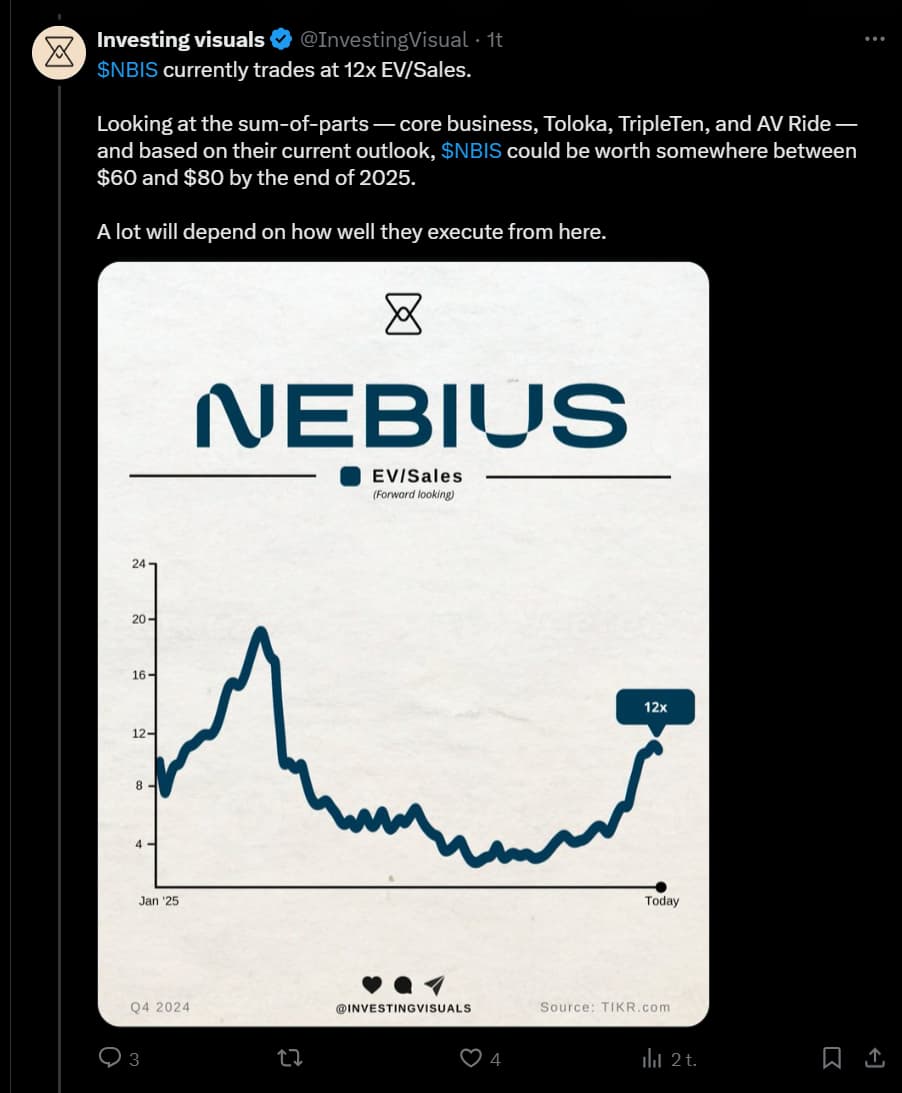

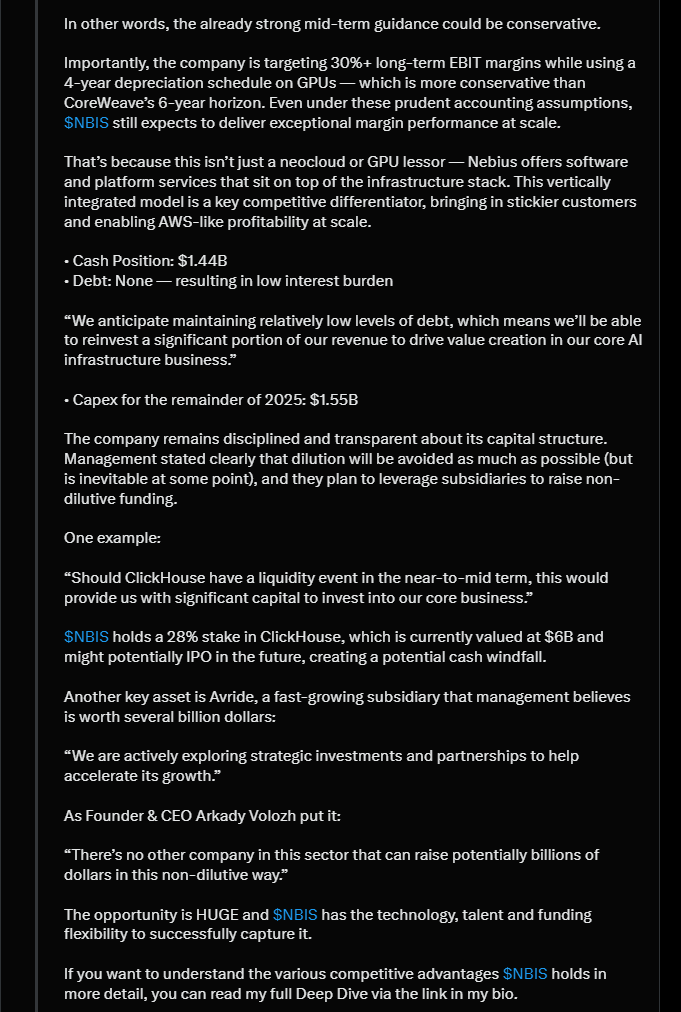

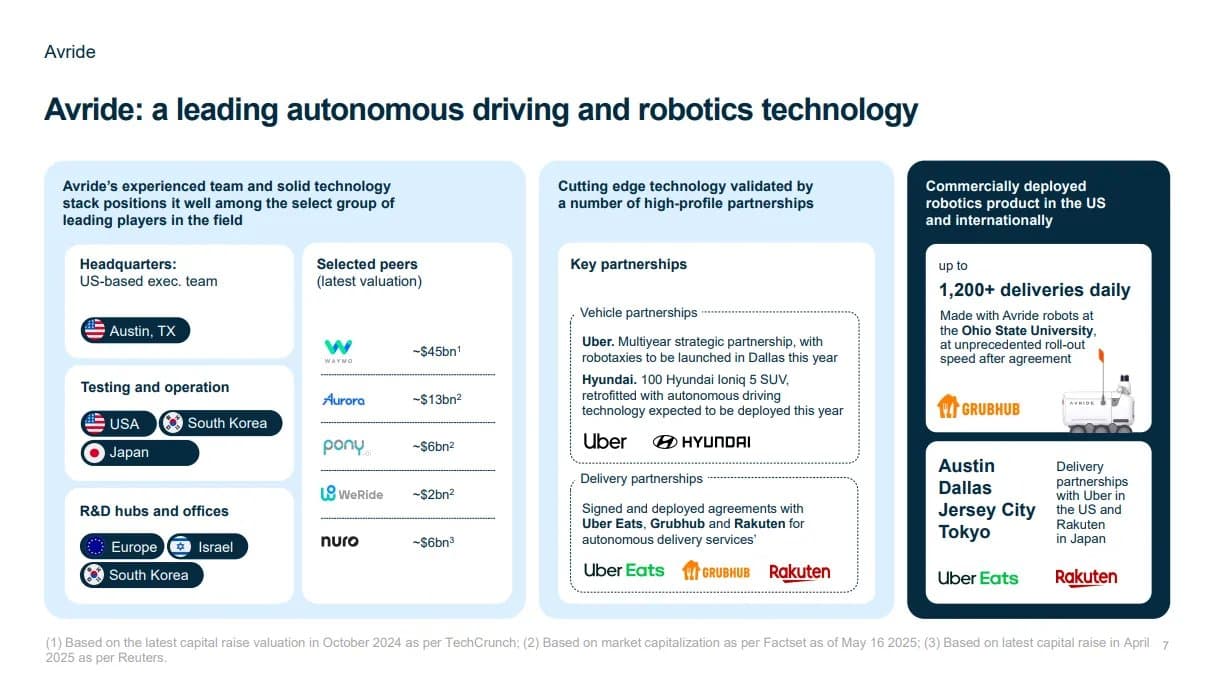

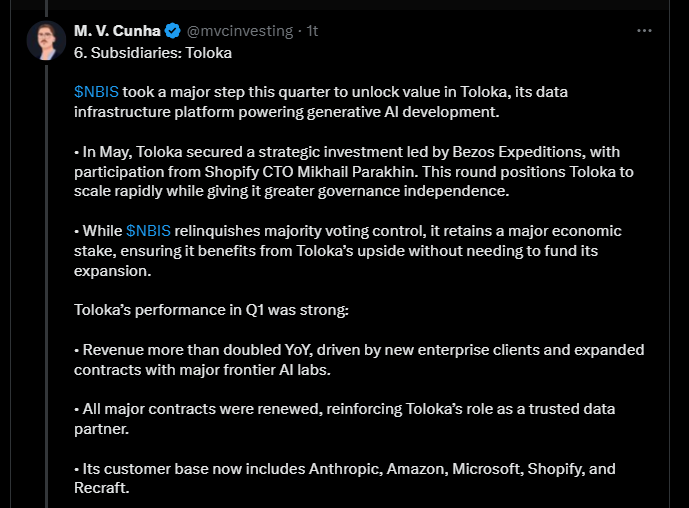

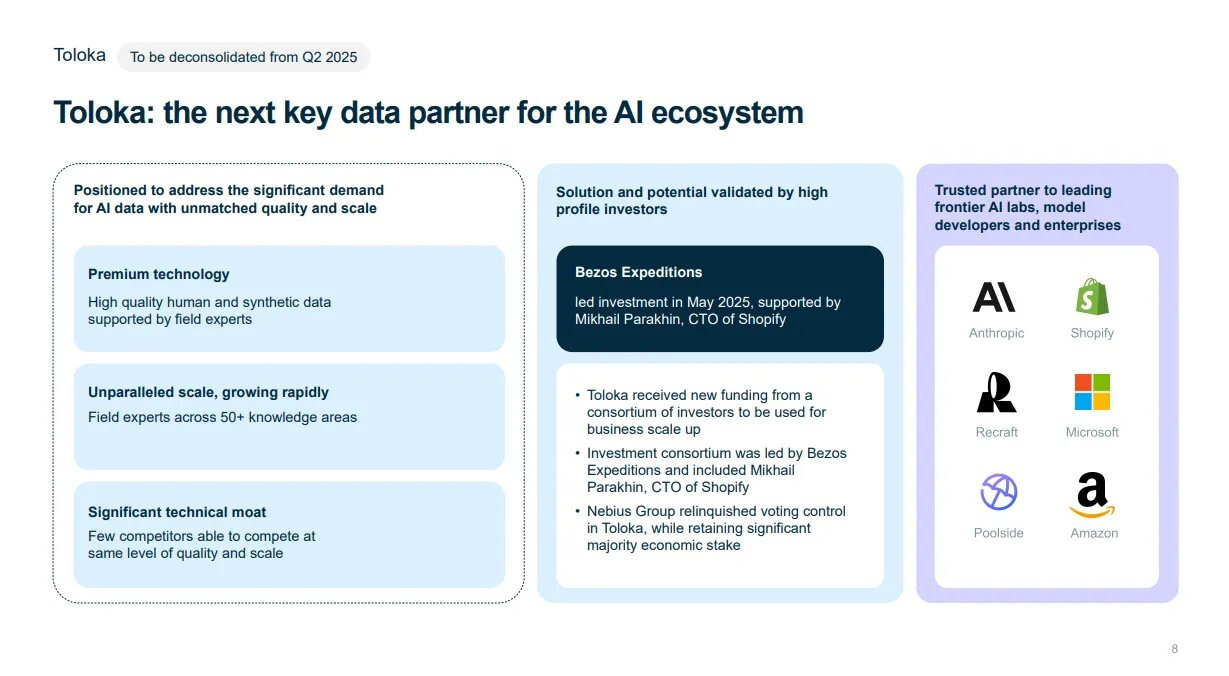

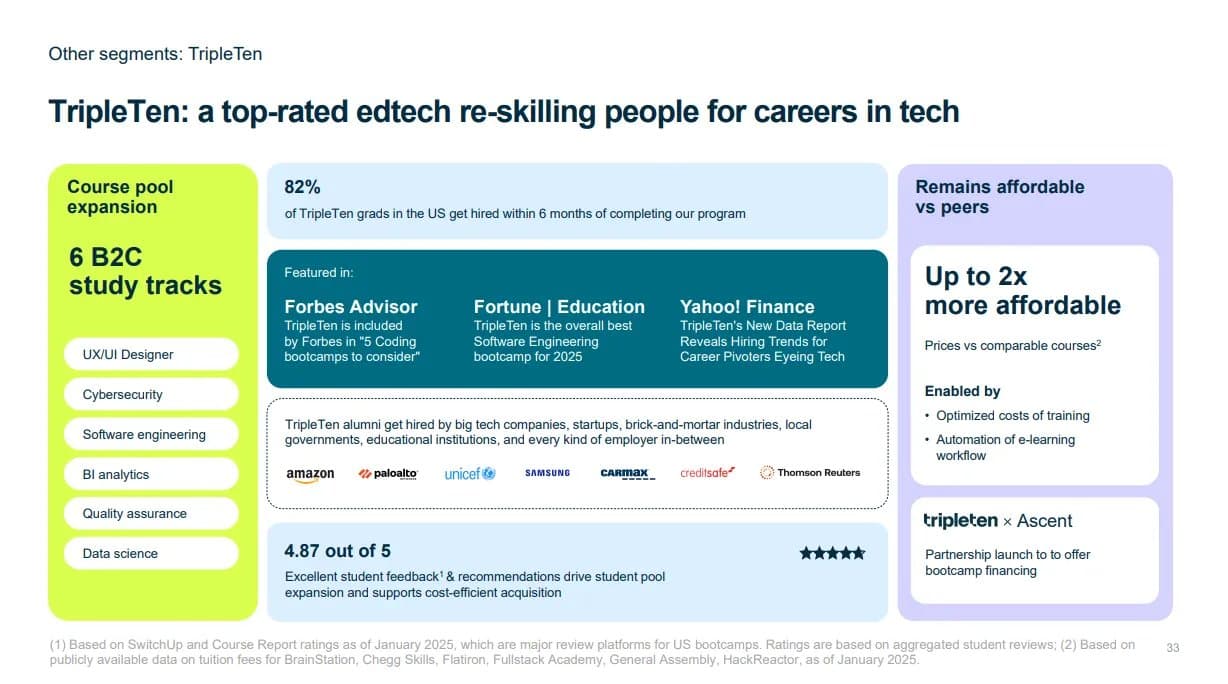

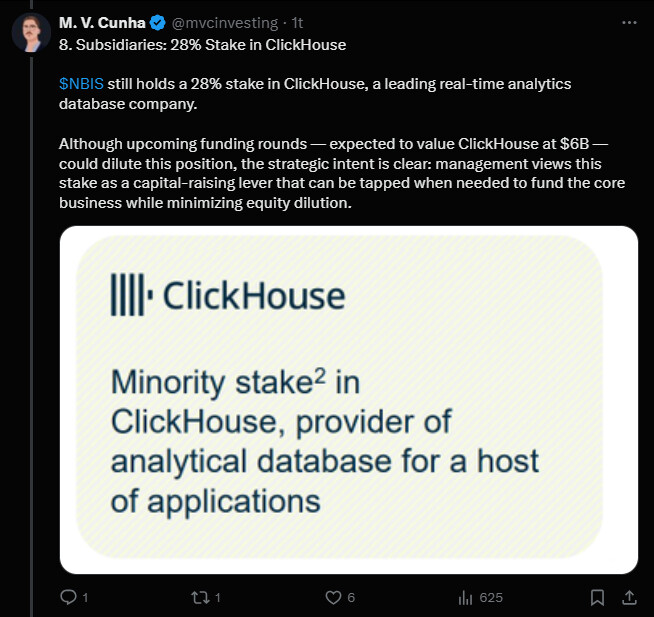

The tweeter points out how the company owns three promising subsidiaries: Toloka (data processing), Tripleten (edtech), and Avride (autonomous vehicles), as well as a 28 percent ownership in the $6 billion-valued ClickHouse and $2.4 billion in cash.

Quite a lot of stories about this company pop up here and there - unprompted. Often, these naturally bring up the same things, but it’s nice to see what is particularly emphasized, etc.

Nebius has its earnings report on Tuesday before the US market opens.

A kind of comparable for Nebius is Coreweave, which had its earnings report on May 14th, and Coreweave has risen nicely since then. Nebius is a debt-free company (2.4 billion dollars in cash), unlike the indebted Coreweave; however, guidance will be the deciding factor here. In the last month, Nebius has risen 80% (Coreweave 100%).

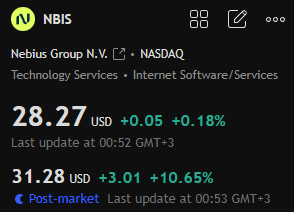

Nebius’s stock closed on Friday at approximately 37 dollars; about 7% of the stock is shorted, and a large portion of the owners are small investors, which certainly increases volatility.

I personally have Nebius shares with about a 25 percent return, and I intend to hold them through the earnings report.

I have Nebius with a 79% return, and I recently halved my position. The reason for halving was partly to realize profits, but I thought about it for a long time before selling. Part of the reason was precisely the share of retail investors, and since there are quite a few players on the short side as well, I thought that a possible disappointment in some part of the earnings report could drop the stock price “somewhat.” Of course, there are quite high expectations for Nebius, and these have been partly fueled by some recent positive news related to the company’s operations. Well, if the earnings report drives the price down and the reason for the drop would be temporary/acceptable for a longer hold, then one could buy it back. However, I will leave the unsold other half of the original position in my portfolio, which I bought at an average price of 20.63 USD.

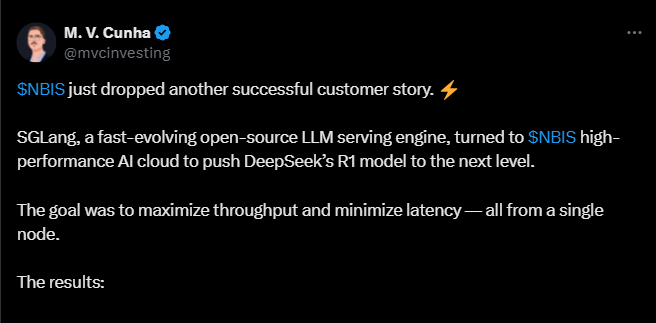

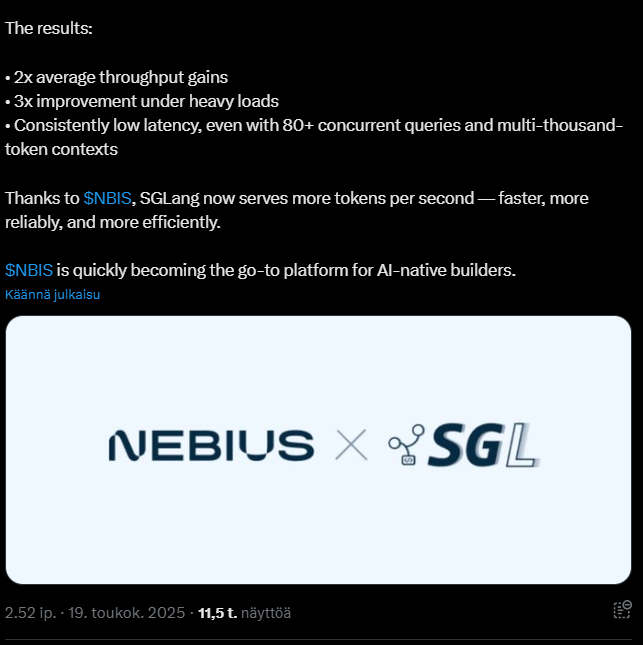

Nebius published a new “customer story” about SGLang, which used Nebius’ high-performance AI cloud service to power the DeepSeek R1 model.

The goal was to maximize throughput and minimize latency. The result was a twofold performance improvement and a threefold improvement in heavier “loads”.

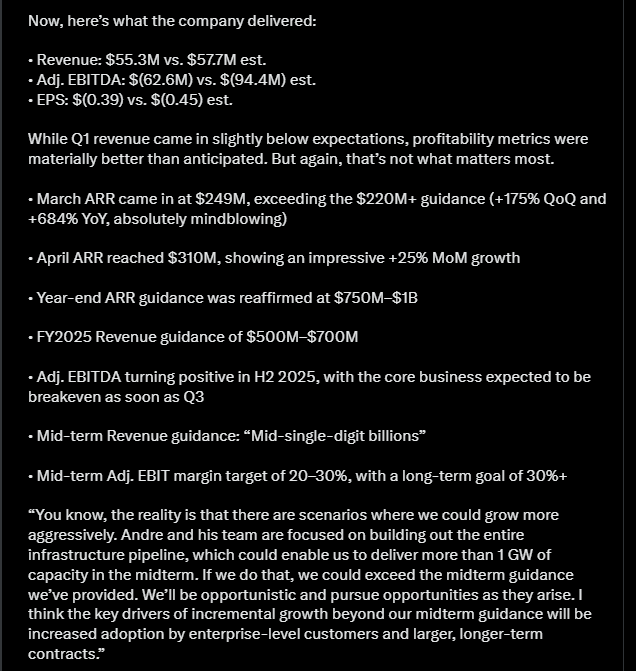

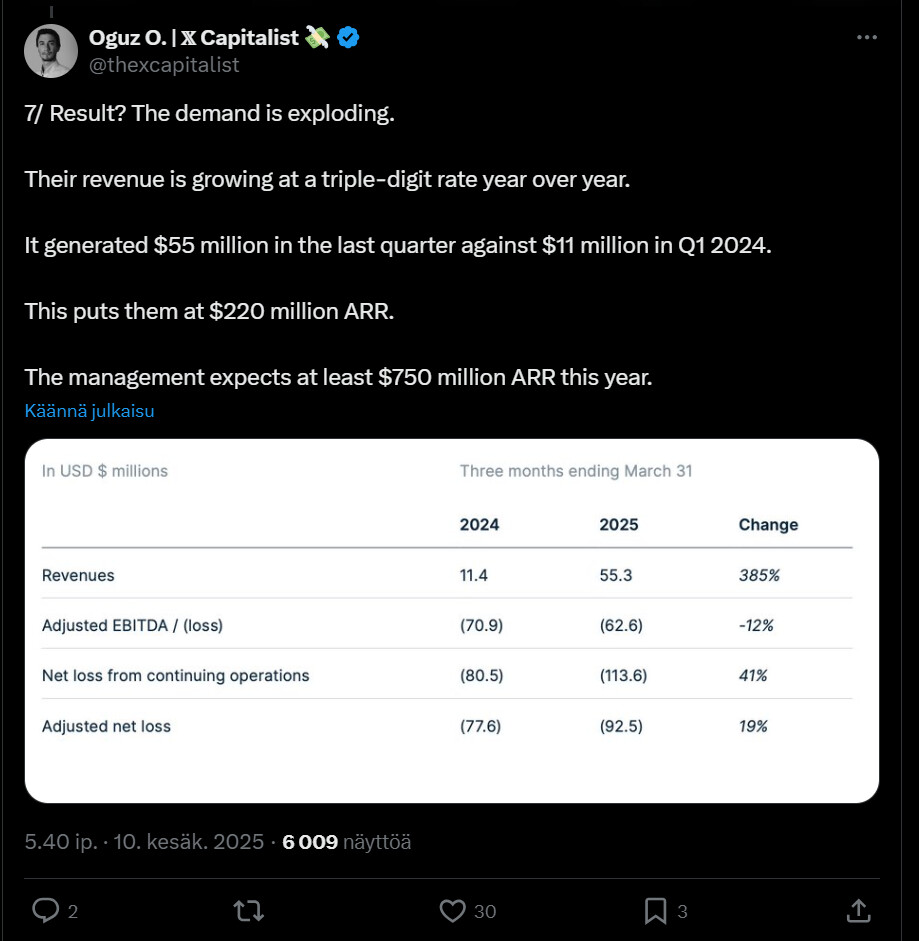

Nebius Group N.V. announces first quarter 2025 financial results

Amsterdam, May 20, 2025 – Nebius Group N.V. (“Nebius Group”, the

“Group” or the “Company”; NASDAQ: NBIS),(1) a leading AI infrastructure

company, today announced its unaudited financial results for the first quarter

ended March 31, 2025.

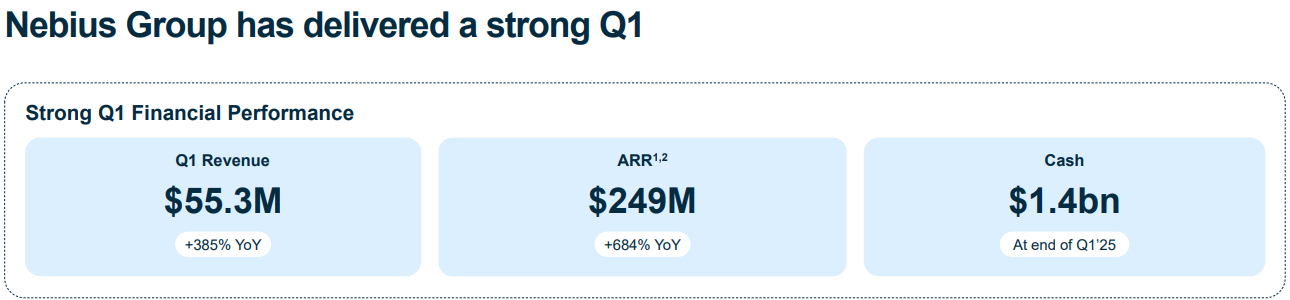

In Q1 2025, the Group’s revenue of $55.3 million increased 385% year over

year, driven primarily by the core AI infrastructure business. Adjusted EBITDA

loss in Q1 2025 was $62.6 million and net loss from continuing operations

was $113.6 million.

The Company also today published an inaugural quarterly shareholder letter

from founder and CEO Arkady Volozh, and an accompanying presentation

with key business and financial updates. These items can be found on the

Company’s investor relations site at group.nebius.com/investor-hub

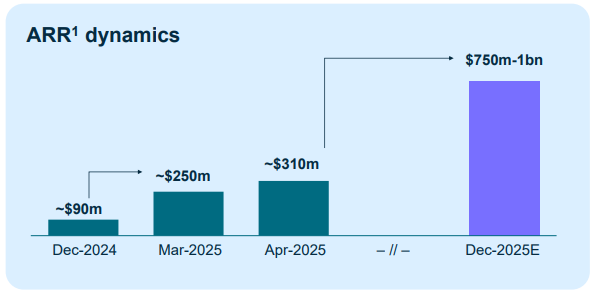

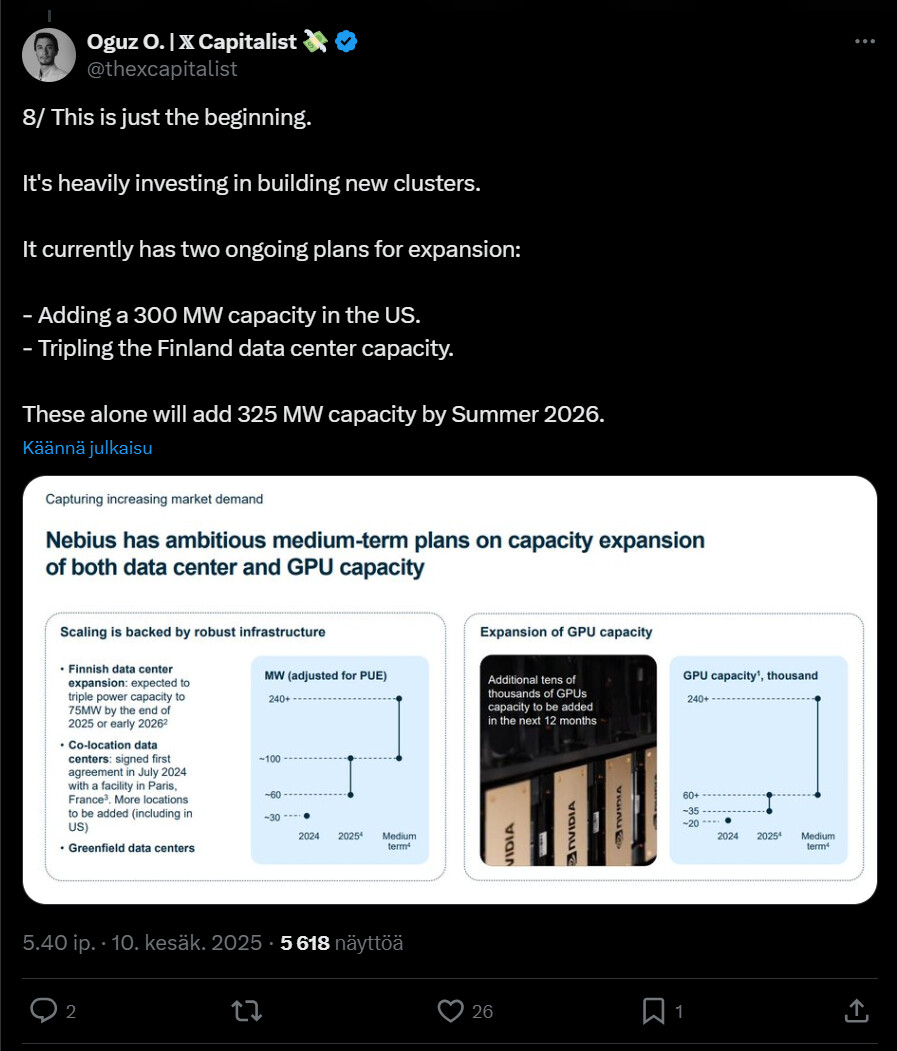

In graphical form:

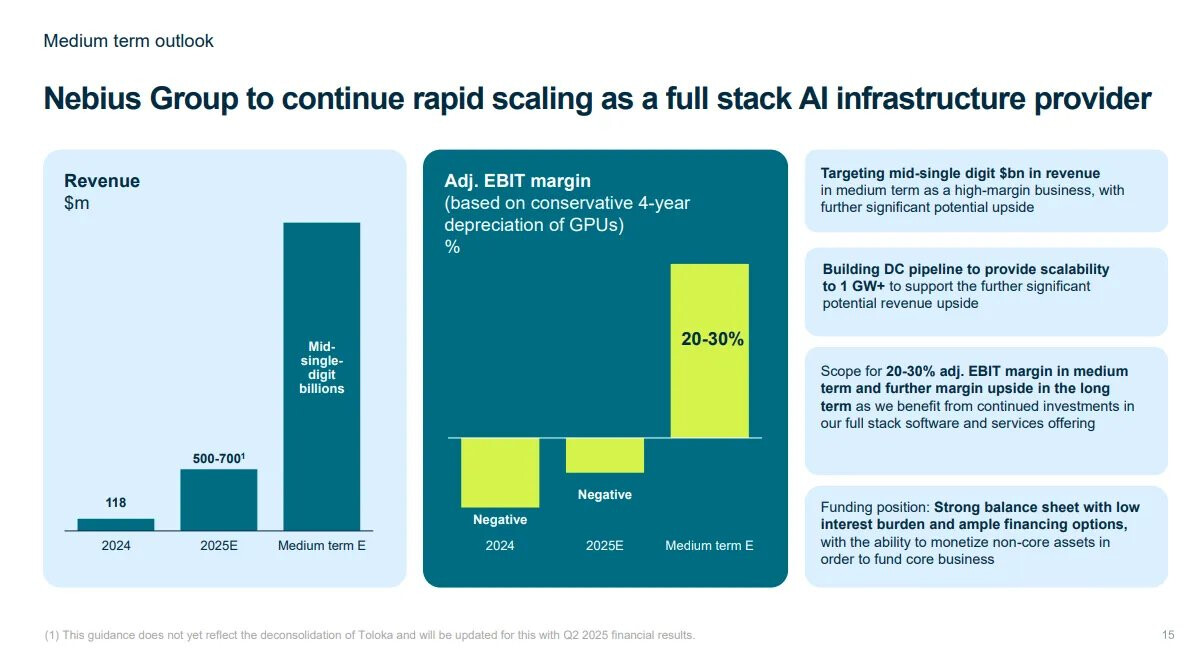

Strong growth figures, considering they started almost from scratch again

There’s still work to be done to reach a billion ARR

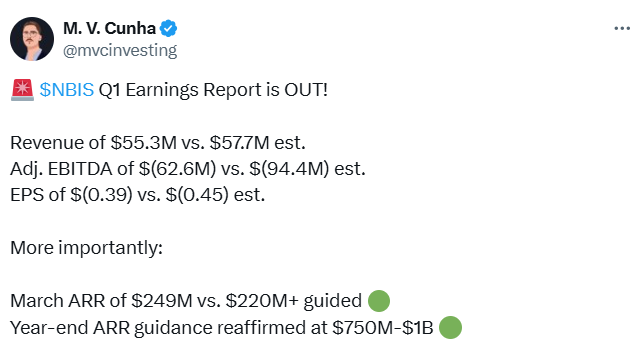

M.V Cunha’s comments already out

According to these, revenue fell slightly short of forecasts

Let’s still hope for a careful consolidation so that even the slow Häme people can get on this train. The earnings report is good, but hopefully, the money will move with great force to CoreWeave.

Here is a really comprehensive tweet thread that I’m almost treating as an analysis.

The thread already has good information about the result, but I’m still posting this because it contained so much good information with justifications.

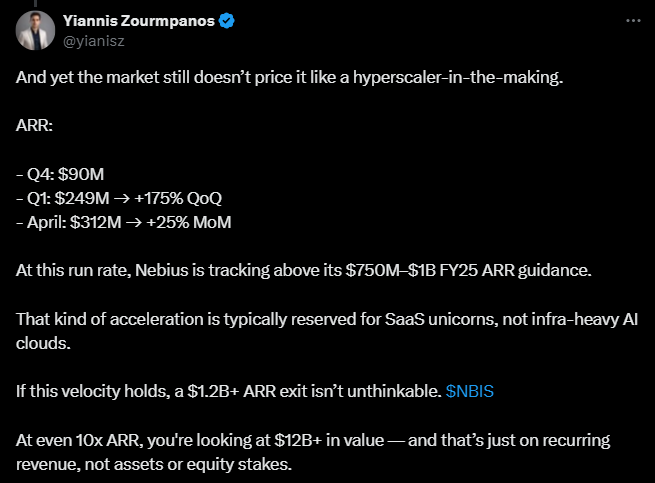

Many have emphasized that recurring revenue; here’s one highlight stating that Nebius is growing rapidly, but the market still doesn’t price it as a hyperscaler, which many nonetheless expect from the company.

The tweet also states that revenue is growing fast, which is typically characteristic of SaaS companies, but not exactly for so-called heavy AI cloud services.

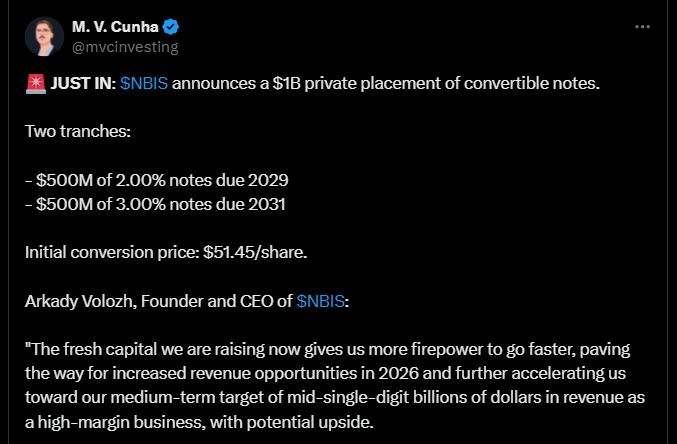

The tweets below announce how Nebius has declared a billion-dollar convertible note, divided into two parts: a $500 million note with a 2 percent interest rate, and another note of the same amount with a 3 percent interest rate.

The goal is to finance the development of the company’s AI infrastructure and accelerate revenue growth. According to Nebius’s CEO, the company’s strong cash position and low debt burden enable profitable growth.

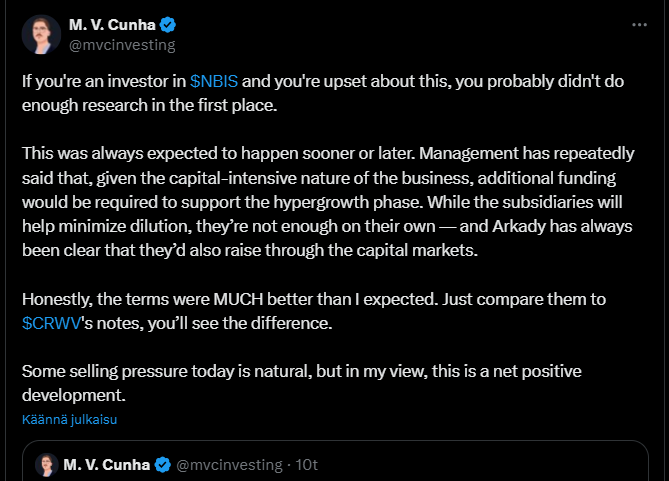

Statements made by Nebius change quickly, although this was predictable as building AI infrastructure is expensive.

Before the quarterly report: We have 2.55 billion in cash, which will last well into next year, we are debt-free, we are developing all our segments. We use 600 - 1.5 billion / year mainly for AI centers.

1 month after the quarterly report: 1.44 billion cash remaining (a drop of over a billion in a quarter), side businesses are being developed for sale, so we can get money for the core business, we are a “low-debt” company.

Coreweave shows a frightening example of how much one must continuously invest when processors cost a fortune and new, ever more powerful processors come to market from Nvidia every few months. In the latest funding round, Coreweave already has to pay 9.25% interest on its loan. Nebius only pays 2% and 3%, and because it largely does everything possible itself, it gets value for money, but it is clear that Nebius will take on significantly more debt and sell off parts of itself still this year, if it wants to grow at the same pace as it has in the beginning of the year.

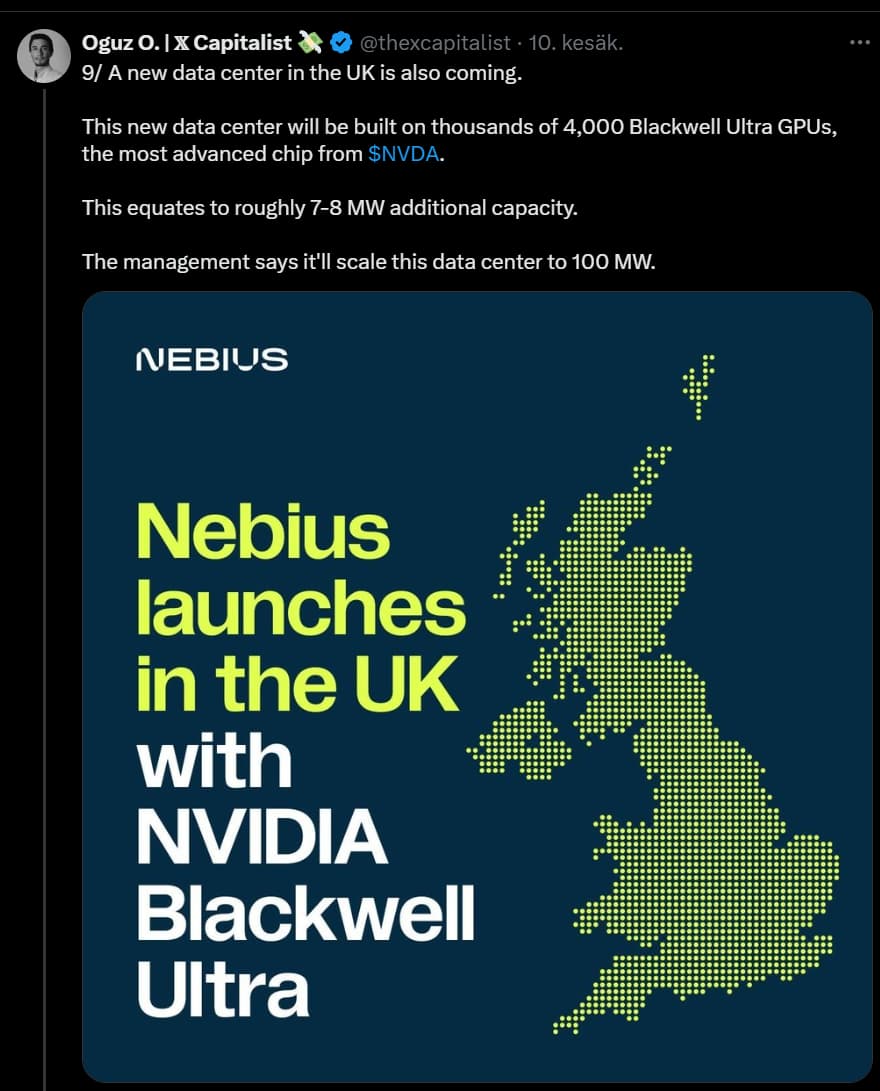

Nebius opens its first AI factory in the UK, deploying 4,000 NVIDIA Blackwell GPUs.

The goal, in short, is to provide powerful and scalable AI capacity for research, the public sector, and the NHS. This should strengthen Britain’s position as a leading AI nation and support local innovation.

Here’s another good tweet thread about Nebius, naturally with quite a bit of overlap with previous messages.

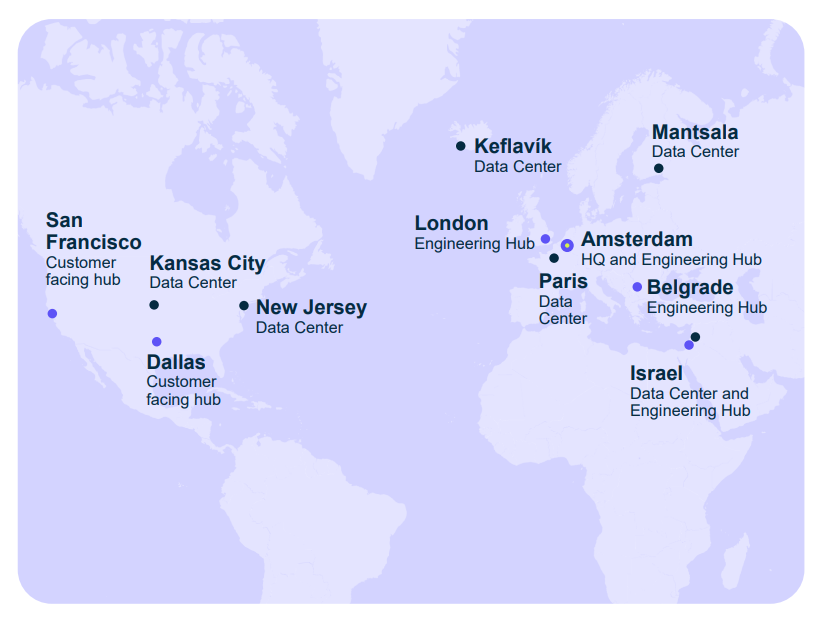

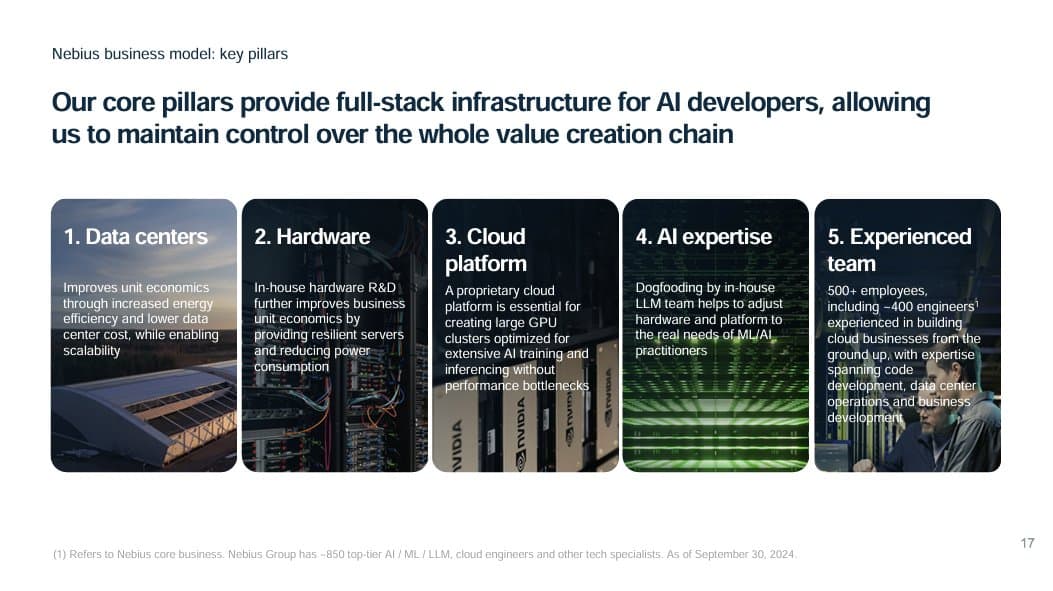

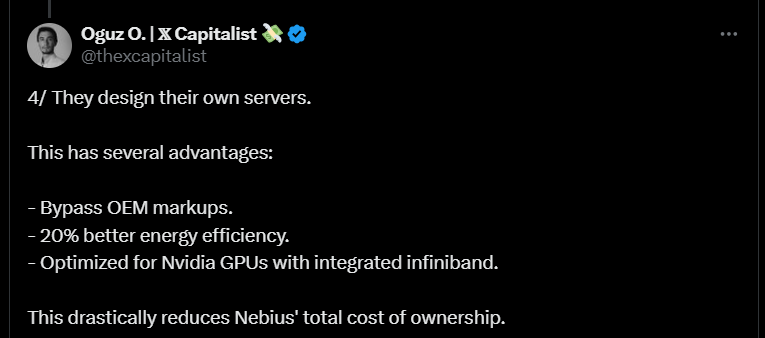

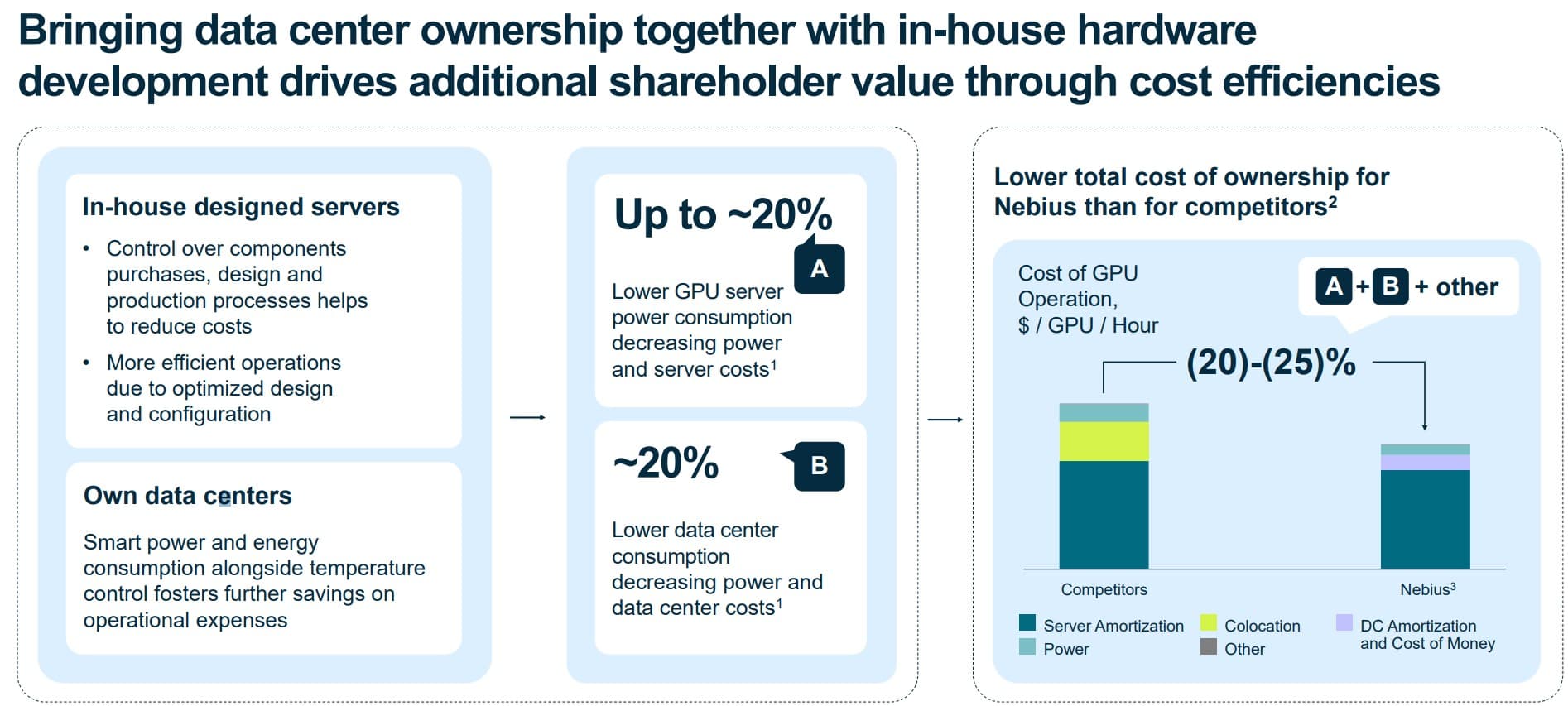

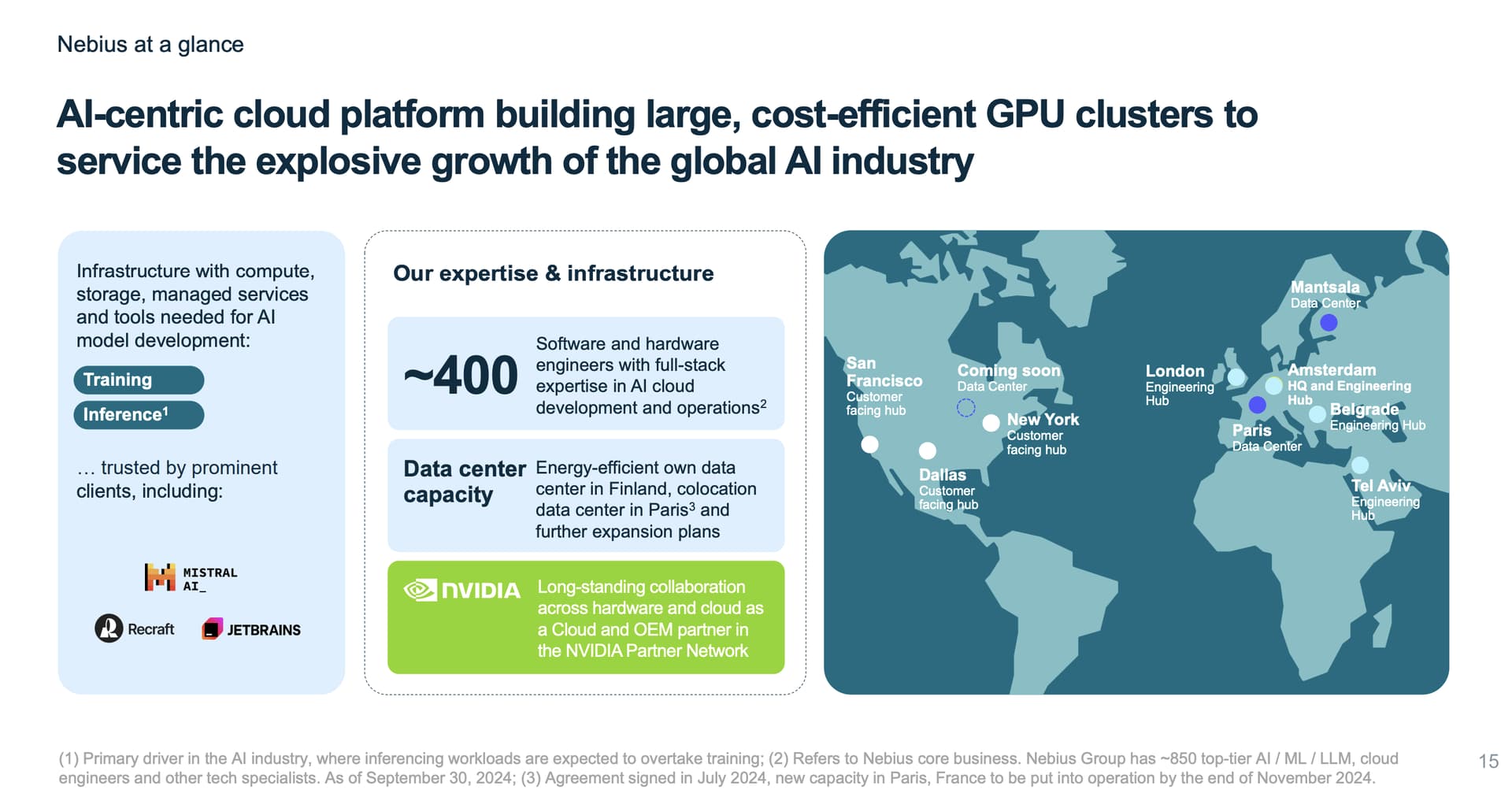

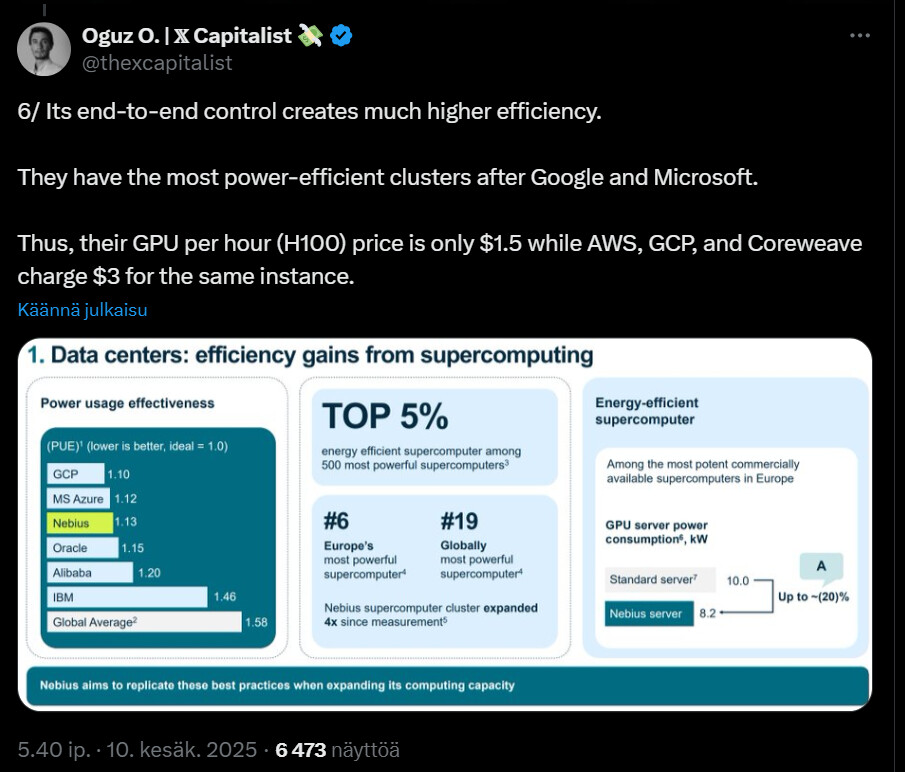

The main message of the tweet thread is (“surprise”) that Nebius is growing rapidly, driven by the demand for AI and cloud services. The company builds its own servers and data centers in Europe, which streamlines operations and lowers costs, plus they control the entire value chain themselves.

Indian data center companies are trying to attract new types of cloud service companies to offer cost-effective AI computing.

According to the tweet below, Nebius’s focus is still in North America and Europe, so expansion into India is only a matter of time. The company has already, however, announced its expansion into Asia, starting first in Singapore.

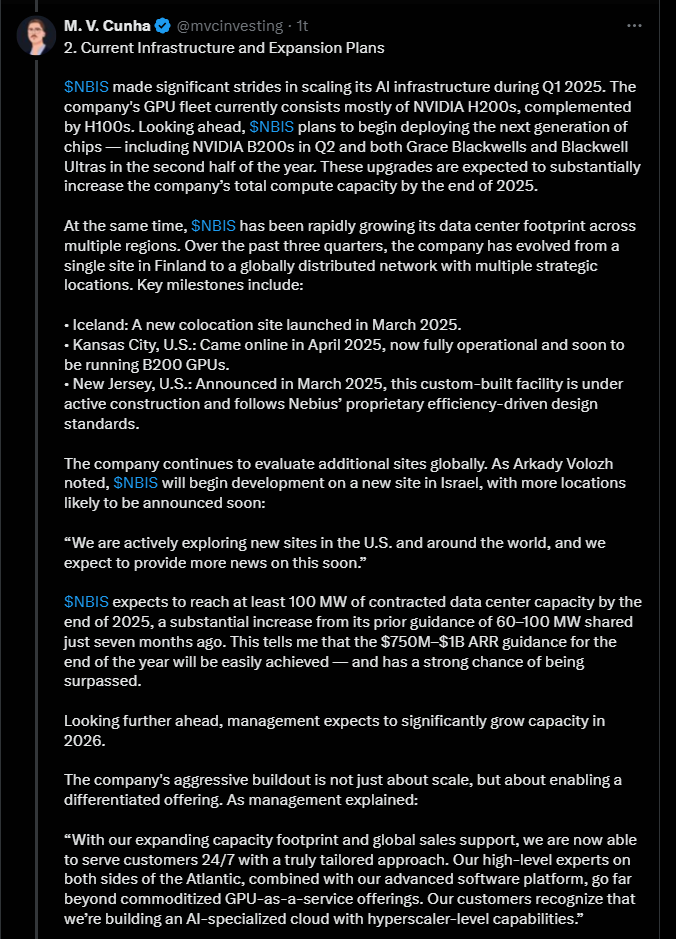

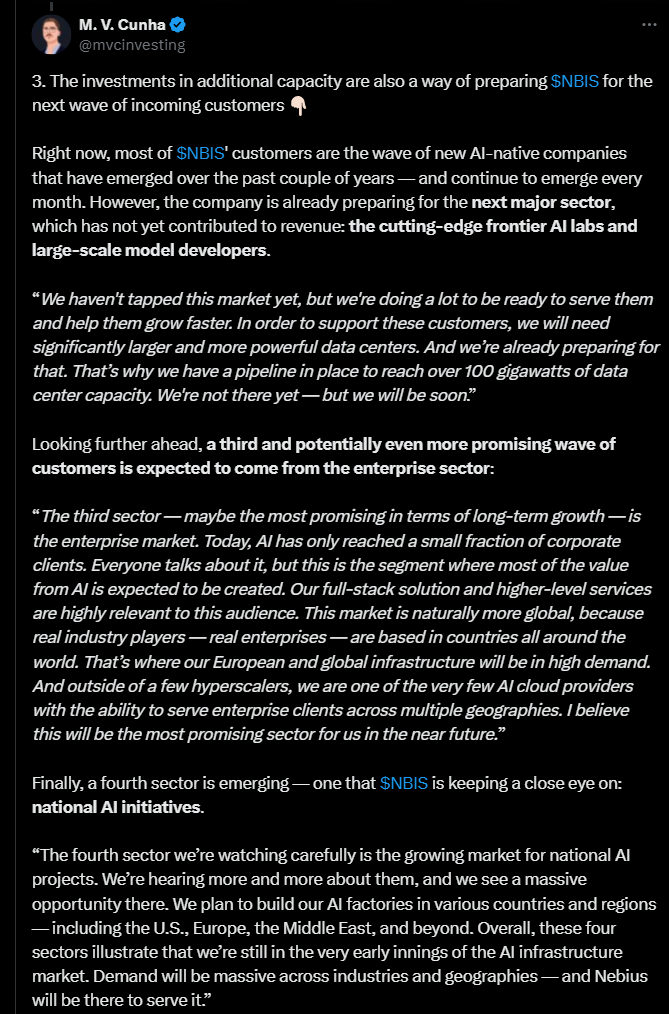

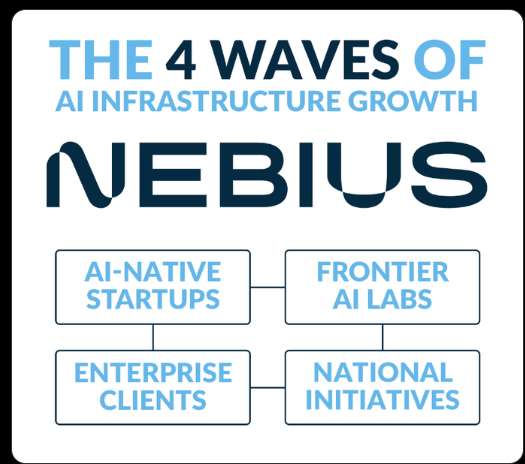

The tweeter states that Nebius is building its growth on four customer waves, the first of which consists of AI-driven startups. They need efficient, scalable infrastructure for model training and deployment. The second wave consists of top-tier AI labs and “large model developers,” whose requirements are significantly greater. For this purpose, Nebius is significantly expanding its capacity.

The third and reportedly most economically significant wave is enterprise customers, many of whom are still in the early stages of leveraging AI. The tweet notes that the company’s so-called global presence and enterprise-level services offer a competitive advantage in this area.

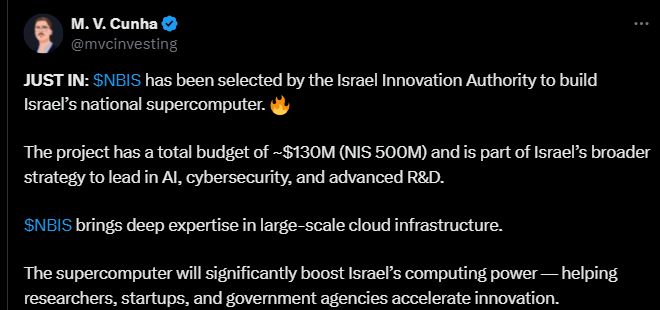

The fourth wave covers national AI projects, such as Israel’s supercomputer project, where Nebius supports governmental AI objectives worldwide.

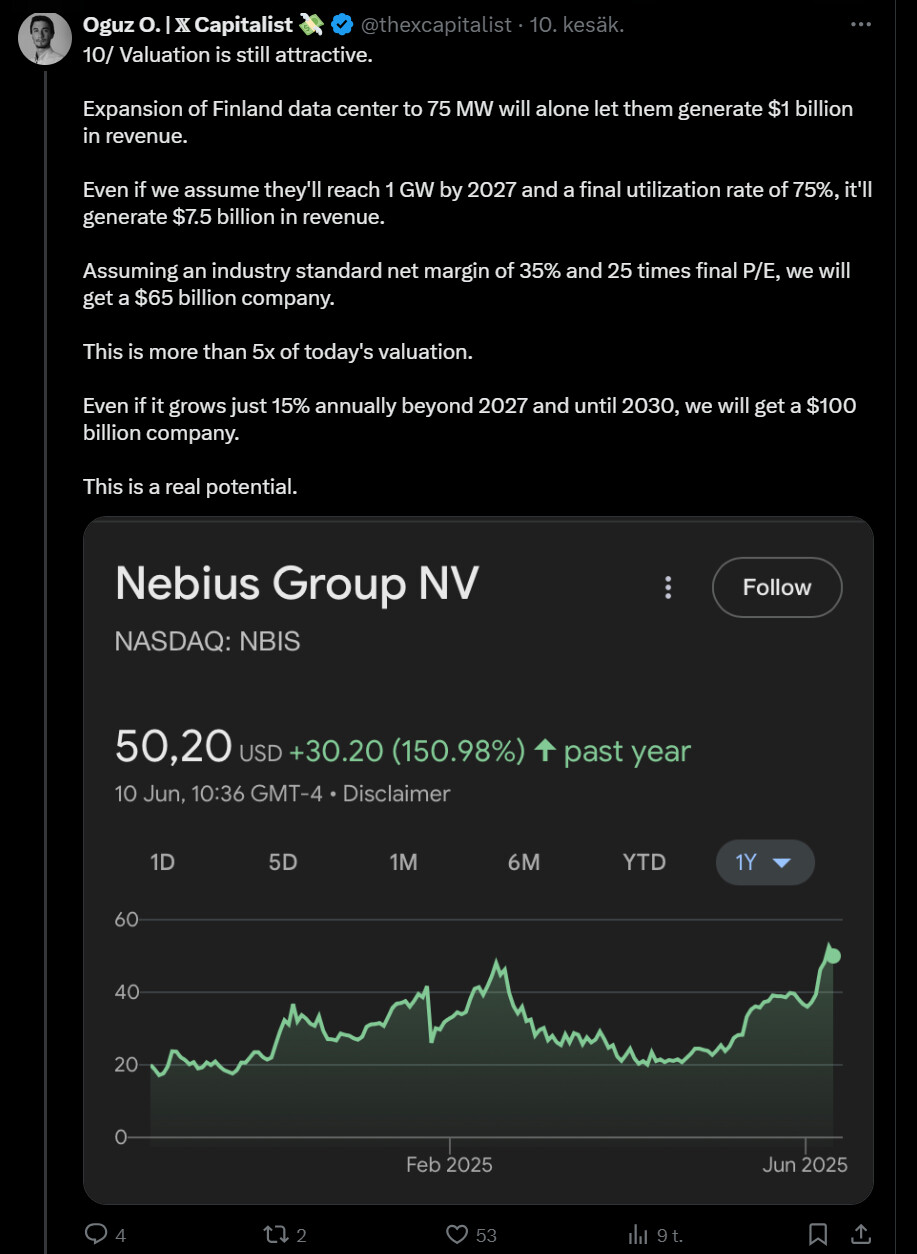

NEBIUS on noussut jo yli 150 prosenttia kevään pohjilta, mutta tämän jutun kirjoittajan mukaan iso osa “tarinasta” on vielä edessä.

Kirjoituksessa käydään läpi tärkeimmät lyhyen ja keskipitkän aikavälin ajurit, kuten esim. datakeskushankkeet, ClickHouse-omistus, Avriden rahoituskierros ja laajentuminen Aasiaan + Eurooppaan. Ihan hyvää settiä, tämän kaverin juttuja on ennenkin ollut täällä, kuten esim. tuossa yläpuolella.

One of the biggest reasons NBIS remains under the radar — even after its recent rally — is a simple but powerful one: limited institutional awareness.

Due to the unconventional route Nebius took to go public, the company currently lacks broad sell-side coverage. It’s barely visible on major financial media platforms, and few Wall Street analysts have given attention to the business. As of today, NBIS is covered only by a handful of small firms: DA Davidson, Northland, Arete Research, and BWS Financial — all of which have issued Buy ratings.