Let’s post a summary of Q4 2025 here, even if it’s a bit late. For a change, it was actually a pretty good quarter.

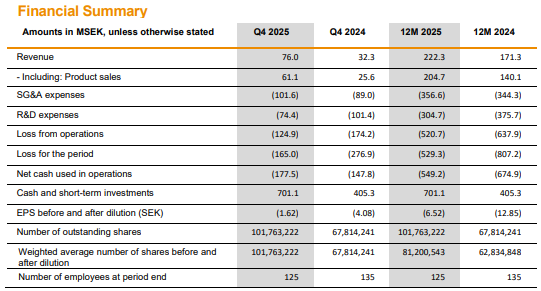

Revenue was 76 MSEK, of which product sales accounted for 61 MSEK, representing about twenty treated Idefirix patients. Full-year 2025 revenue grew by approximately 30% year-on-year. Q4 cash flow was still 178 MSEK in the red, and the full-year cash flow was -549 MSEK accordingly. Cash on hand was 701 MSEK.

Hansa gave guidance for a weaker Q1 2026 than the quarter just ended, and improvement could come in the latter half of the year. The US launch is planned for the end of the year (Q4), and hope for this was partly bolstered by Hansa reporting that the FDA accepted the BLA (Biologics License Application) for imlifidase on Feb 18.

Personally, I only skimmed through this report, although I still have some kind of Hansa position in my portfolio. However, I spotted something in Redeye’s Q&A section, according to which Redeye does not see the shortage of donated kidneys in the US market as a similar constraint as in Europe. According to analyst Richard Ramanius, the target group for imlifidase is prioritized in the US: “Hansa has an advantage in that US decision makers prioritise highly sensitised patients because they want to reduce dialysis dependence.” Redeye has certainly been quite off the mark with its Hansa analysis so far, so it’s hard to say what value this statement holds. At least the analyst has changed now.

Expectations still rest mainly on that US launch and the US market potential.