One can’t help but analyze this. Of individual companies, I have spent by far the most working hours on this, even though the result is meager. For instance, with the timing of Faron, Hims, and Optomed, I’ve succeeded significantly better than with holding this, but what can you do…

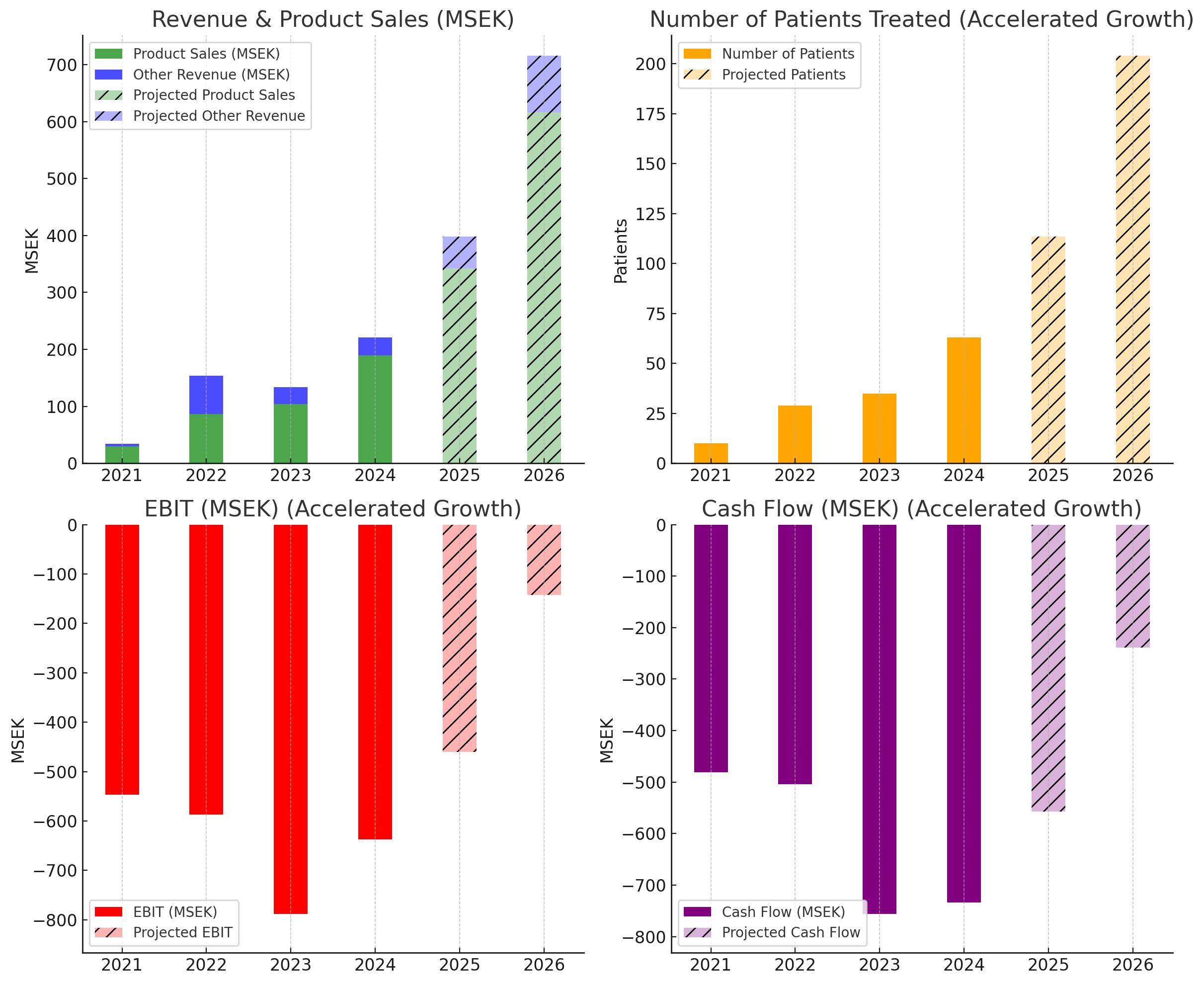

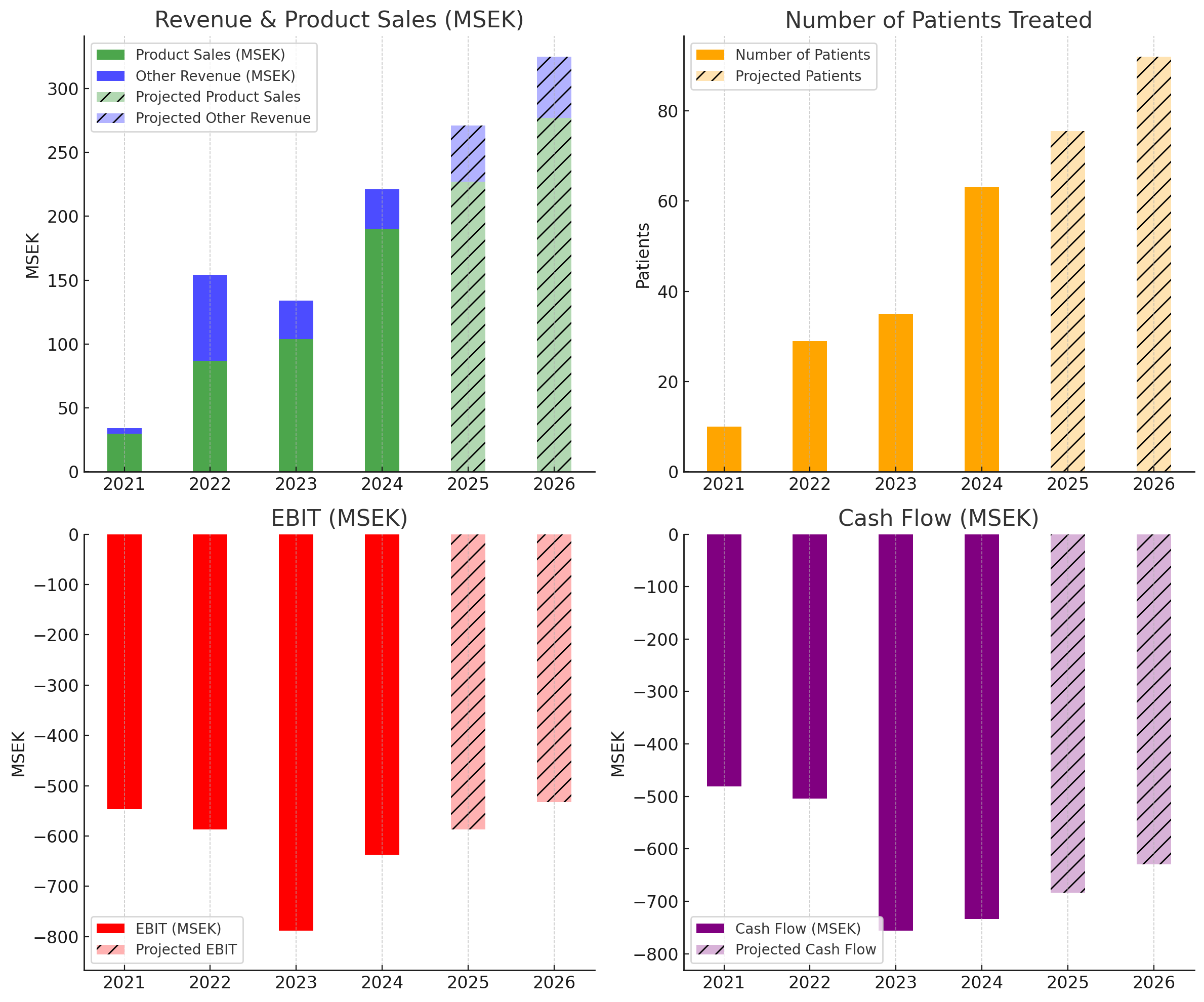

In any case, I ventured to make a small estimate of Hansa’s development over the next couple of years.

I assume here that in Europe, talk of an S-curve can be forgotten, and imlifidaasi sales will develop more linearly when viewed on an annual basis. At the quarterly level, there is so much fluctuation that an analysis is not meaningful. I also believe that peak sales in Europe for kidney transplants will remain significantly lower than analysts have predicted. In my opinion, Hansa’s development looks like a struggle for survival until 2027, but after that, the company still has a chance to meet expectations. I would see that, quite credibly, with US sales, there are opportunities for much better and faster success than in Europe, but that is a matter for a different review from 2027 onwards.

Assumptions:

Anti-GBM Launch 2027

Kidney transplantation USA Launch 2027

DMD Launch 2027

GBS Launch 2028

Product sales and revenue are assumed to grow trend-wise in 2025-2026 based on the development in 2021-2024. Additionally, the growth in revenue and product sales is assumed to transfer as such to profit and cash flow in 2025-2026, meaning costs remain unchanged.

It’s difficult to see significant leaps in the next couple of years, but Sarepta’s milestone payments might bring “unforeseen” good, which may not be fully reflected here. On the other hand, total costs remaining unchanged is also quite an optimistic simplification, even if R&D costs might temporarily decrease slightly in the coming quarters. Things should then start happening in 2027-2030, but it’s a long way off. Of those 2027 launches, a few might, in the best case, be in 2026, but actual sales will likely only come in 2027 at best. Things can always shift further into the future.

The cash position is indeed SEK 400m. Hansa still states that funding is sufficient until 2026. That doesn’t align with my analysis at all, meaning one of us is wrong. Hopefully me ![]()

Disclaimer: the analysis is entirely my own; errors may exist.

Edit: I was still thinking about Hansa’s forecast for cash sufficiency until 2026 and the S-curve – which has now been removed from Hansa’s presentations. Here is a bullish version of the curves. Assumptions are otherwise the same, but here, the development between 2023-2024 has been emphasized, and an assumption has been made that sales development will continue to accelerate based on this, following an S-curve. I personally believe more in the first version, but it will be interesting to see which one 2025 follows.