How have you diversified between different asset classes? Or are you all-in on stocks?

My current diversification regarding investment assets:

Stocks and ETFs - Approximately 20%

Forest - Approximately 60%

Other real estate - Approximately 20%

Of course, I also have an apartment, but I don’t count that as an investment. One has to live somewhere.

My stock weighting will increase in the coming years.

That works too. Personally, over 75% of my net worth is in investment assets, so it doesn’t make much of an impact. But then again, I’m already middle-aged.

Already two deleted posts in this thread and access to the Masters’ Lounge Coal Cellar is drawing near. Could you, however, clarify the title so that it doesn’t refer to assets, but rather to investments?

Meaning: Diversification between different (not: asset classes, but) investment classes.

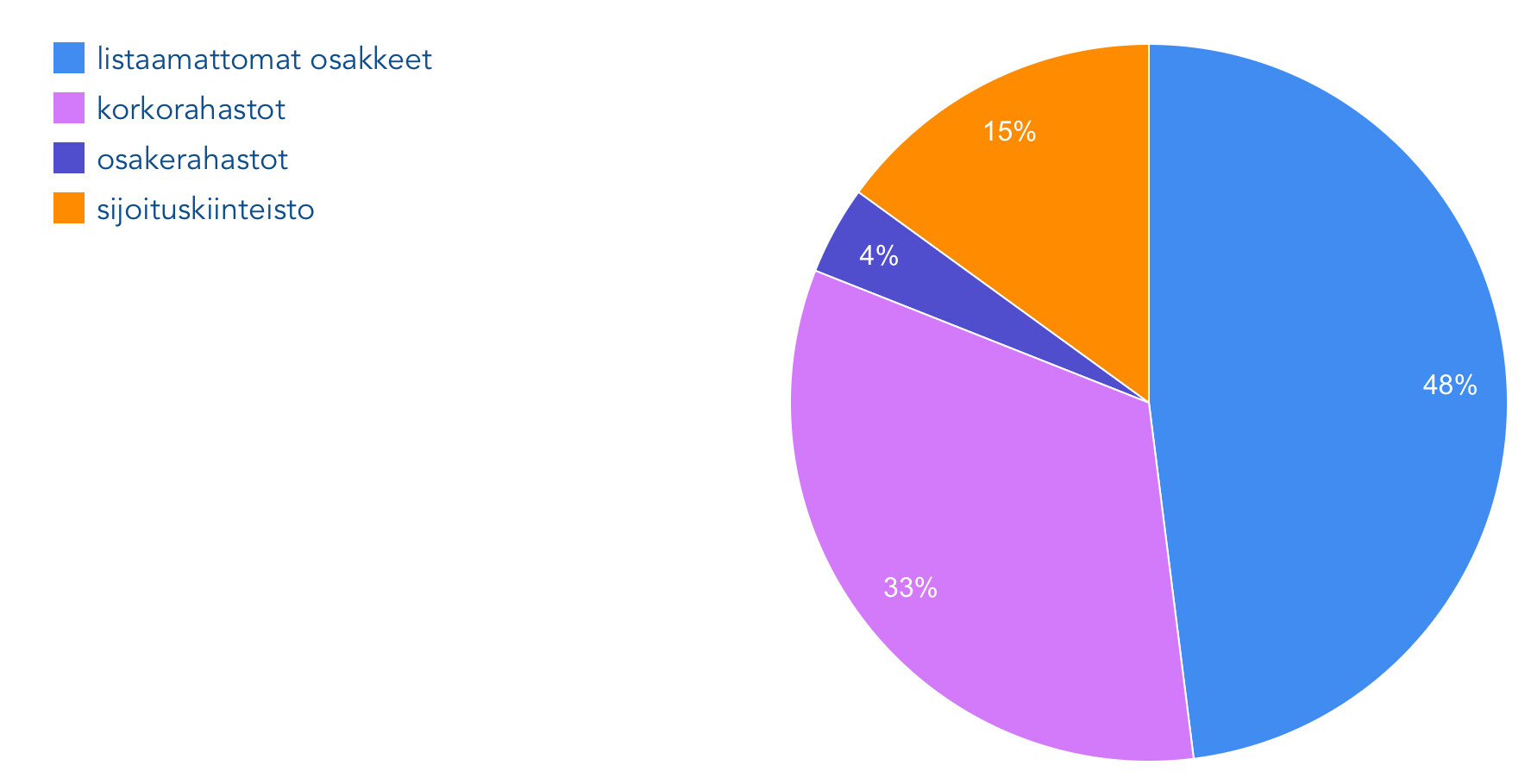

Stocks (and equity funds) 60%

Fixed income 10%

Unlisted shares and fixed income 10%

Investment properties 20%

The share of properties has decreased in recent years and will likely continue to decrease in the future, as I do not plan to acquire new ones. Unlisted investments will grow in the future through capital calls from fund investments. I might also include some new asset classes from the alternatives side. Otherwise, I am quite satisfied with this allocation.

Thanks to the OP for a topic that has also given me much to think about!

Background: I am in the “gentleman of leisure” phase of my life, and the ultimate goal is to enjoy my remaining healthy days to the fullest. Beyond that, the plan is to transfer all surplus wealth to the next generation gradually as early as possible and to be practically penniless (excluding a smaller owner-occupied apartment than my current one) when I’m no longer around, at which point my small future pension will suffice for the essentials. Age now 60.

Stocks (+1 interest rate) in ETFs: 20%

Real estate (2 plots and garages): 20%

Interest-bearing account: 10%

Apartment (half of the value, which I already count as an investment at this stage, as the intention is to eventually move to an apartment half the size): 50%

Yesterday, I posted in the “vapaaherra” (gentleman of leisure) thread regarding something that has been on my mind and is related to this thread (I don’t know how to link it here).

In that post, my real-life steps happened to show, in a “cherry-picking” style, that investing everything in stocks doesn’t always hit the mark, no matter how much average returns support it. Sometimes purchasing power is preserved better in “bricks and mortar” over a 10–15 year period.

It’s hard to grasp at what level of a “stock market crash” it would actually be worth making the move to sell the current apartment, buy one half the size, and put the difference into stocks. Or even to convert other real estate into stocks.

Although history is no guarantee of the future, the graph I would like to see is “the performance of a two-room apartment in central Helsinki as a preserver of real purchasing power vs. an investment in a stock index after costs and taxes,” e.g., for the last 40–50 years . Can more advanced AIs draw this yet? I might even pay a little for it.

The cause of a stock market crash can be a general economic recession, at which point even an apartment cannot be sold easily or for a sensible price. Regarding stocks, I have noticed that different companies perform differently as market conditions change. At one time, energy production was a shunned sector, and the market only accepted energy forms that met ESG criteria. Then Russia invaded Ukraine, and all kinds of LNG tankers and thermal coal burning were suddenly OK. Even if a recession hits, maybe people will still sign mobile phone contracts and buy beer from the store. In times of crisis, Americans buy handguns again.

This is how I think about diversification. Forestry differs from stocks, but it is raw material production for a decade ahead. Suddenly, spruce bark beetles and forest fire warnings start to become interesting. Studio apartments in university towns serve a certain consumer segment, and the real estate investor’s income and risks also depend on the economic success of that target group. So, if you swap one investment for another, you have to think about why the asset being sold is overvalued and why the one being bought is undervalued. Arguments that an asset’s value will just grow—insofar as it is not about the growth of the cash flows generated by the asset—is a view based on other investors’ increasing willingness to pay.

It makes me smile how, during the stock market bubble, asset managers advertised private equity diversification options like “a vineyard in France.” These do not have a listed market price or regulated reporting obligations, so you can tell stories about their returns and prices. The summer is sunny and the grapes are growing. The stock market crashed, but private equity didn’t go anywhere because we simply skipped the valuation. There should be some other point to diversification than just splashing your money here and there.

I am in a very similar situation to the original poster regarding investment allocation. My own breakdown:

Forestry 40 %

Jointly owned forest 25 %

Stocks, ETFs, funds 20 %

Precious metals (mostly gold) 10 %

Real estate investment 5 %

For several years now, my goal has been to increase the share of stock investments to 25–30% of investment assets. However, the rise in the price of forest land and wind power projects on my own properties have pushed the share of forestry investments perhaps a bit too high, even though I have been eagerly on the buy side during the bear market.