Gofore alkaa olla kasvanut sellaiseen kokoluokkaan että se ansaitsee oman ketjunsa. Viimeaikaisista haasteista huolimatta kyseessä lienee yksi sektorinsa laadukkaimmista yhtiöistä. Vuoden työnantajabrändi 2020!

Gofore alkaa olla kasvanut sellaiseen kokoluokkaan että se ansaitsee oman ketjunsa. Viimeaikaisista haasteista huolimatta kyseessä lienee yksi sektorinsa laadukkaimmista yhtiöistä. Vuoden työnantajabrändi 2020!

Tässä on Goforen tuoreen toimitusjohtajan Mikaelin ROAST🔥 tammikuulta.

Silloin ei vielä koronasta puhuttu eikä briteistä lähdetty, mutta videon pitäisi muutoin kestää aikaa melko hyvin.

Goforehan on kasvanut hyvin myös koronan aikana.

Kyllä se taitaa ennemmin olla go for ![]()

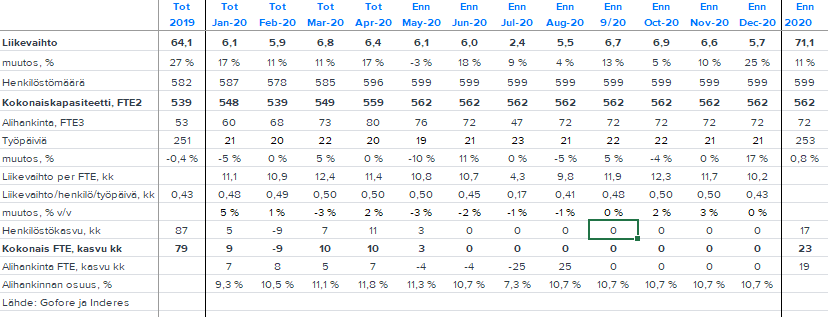

Perinteisesti toukokuu on ollut Goforen H1 vahvimpia kuukausia ja sen jälkeen pientä laskettelua kesä- sekä erityisesti heinäkuussa. Mielenkiintoista että Joni uskoo liikevaihdon laskun jatkuvan syyskuuhun(Edit: toukokuussa) ja henkilöstön kasvun menevän nollaan loppuvuodeksi. Oma näkemys hieman positiivisempi lähitulevaisuudesta, erityisesti henkilöstömäärän kasvusta, kun taas syksyyn liittyy enemmän epävarmuutta.

Olisiko @Joni_Gronqvist kommenttia asiaan ![]()

Terve,

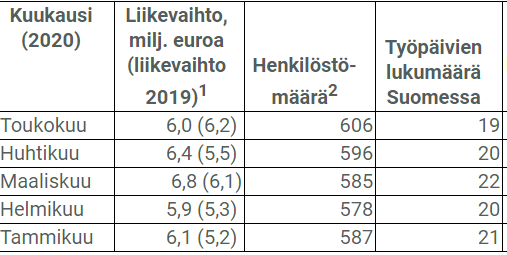

Liikevaihto laskee ennusteissamme hienoisesti toukokuussa (ei syyskuuhun asti) harvempien työpäivien (2 päivää tai 10 %) painamana ja vahvasta keskihinta/laskutusaste vertailukaudesta johtuen.

Keskihinta/laskutusaste laskee sen sijaan vertailukaudista toukokuu-elokuu ennusteissamme, johtuen pääasiassa hintapaineesta. Lisäksi ennusteemme sisältää siis 3 henkilön rekrytoinnin toukokuussa ja tämän jälkeen olemme ennustaneet henkilöstömäärän olevan stabiili vuoden loppuun. Alla vielä huhtikuun lukujen jälkeiset numerot ja linkki kommenttiin.

Toivottavasti tämä selvensi odotuksiamme!

Hops, meni kuukaudet sekaisin edellisessä viestissä. Syytän tästä suomen kieltä jossa kaikissa kuukausissa on sama pääte -kuu ![]()

Kiitos vastauksesta Joni!

Rekryilmoitusten määrä ja uusien luonti viittaisivat siihen että henkilömäärää halutaan vielä kasvattaa nykyisessäkin taloustilanteessa ja olen tämän takia härkämainen verrattuna ennusteisiin ja yrityksen kykyyn ylläpitää korkeampaa laskutusastetta. Esimerkiksi

8.5 julkaistu rekryilmoitus alkaa seuraavanlaisesti:

Gofore perustettiin Tampereella vuonna 2001, listauduimme pörssiin 2017 ja Turkuun saavuimme syksyllä 2018. Kasvoimme Aurajoen rannoilla nopeasti muun muassa verkostojemme voimalla pariinkymmeneen henkeen ja nyt tavoittelemme kolmeakymppiä! Haluaisimme rekrytoida sinut osaksi kokeneiden ohjelmistoammattilaisten joukkoamme.

Uskon että ellei syksyllä tule isompaa dippiä niin rekryt jatkuvat läpi vuoden. Toki rekrytoinnin onnistuminen ei ole taattua, vaikka haku onkin päällä.

Goforessa olen tullut arvostamaan sitä, että ymmärretään luoda omistaja-arvoa omien takaisinostolla silloin, kun osake on selvästi edullinen.

Omien osakkeiden hankinnasta:

Hankittavien osakkeiden enimmäismäärä on 210 000 (tai 1,3 MEUR), joka vastaa noin 1,5 % yhtiön osakkeista. Omien osakkeiden hankinta aloitetaan aikaisintaan 25.3.2020 ja lopetetaan viimeistään 30.6.2020. Omien osakkeiden hankinta rahoitetaan yhtiön jakokelpoisella vapaalla omalla pääomalla.

Tällä hetkellä yhtiöllä on hiukkasen yli 20 000 kpl osakkeita, ja hankinnat jatkuvat arkipäivisin vähän yli 1000 osakkeen tahtia, eli hieman yksinkertaistaen osto-ohjelman päätteeksi yhtiö on ostanut n. 50 000 osaketta eli about 0,35% yhtiön osakekannasta. Kun osakkeen vaihto on luokkaa 2000 kpl päivässä, niin yhtiön ostot ovat aika merkittävä osa päivän kaupasta. Ostot ovat onneksi edullisella keskihinnalla, eikä yhtiö osta osakkeita hinnalla millä hyvänsä. Sinänsä kyllä kummallista että kurssi on jäätynyt nykytasolle Inderesin suosituksesta ja jatkuvista ostoista huolimatta.

No, näinkin, mutta Gofore on mörninyt pitkään.

Kun haluaa ylituottoa, silloin pitää löytää väärin hinnoiteltua tavaraa. Kuuluu tietyssä mielessä asiaan, että löytyy “kummallisesti hinnoiteltuja” yhtiöitä. Eihän poiminnassa olisi muuten mieltä.

Ja sitten jos yhtiö jossain mielessä onkin aliarvostettu ostohetkellä, sillä ei tästä huolimatta ole mitään velvollisuutta korjata arvostustaan millään nimetyllä aikavälillä.

Gofore työntekijämäärä yli 600 ja uutta sopimusta:

Uusista sopimuksista mainittakoon, että Suomen ympäristökeskus (SYKE) valitsi Goforen IT-asiantuntijapalveluidensa toteuttajaksi. Sopimus on voimassa 1.6.2020-31.12.2023. Sen avulla SYKE saa lisäresursseja ympäristötietojärjestelmiensä ja digitaalisten palveluidensa suunnitteluun, toteuttamiseen ja ylläpitoon. Sopimuskauden päätyttyä SYKE voi jatkaa sopimusta enintään vuoden mittaisella optiokaudella. Hankinnan arvioitu laajuus on 500-1 000 henkilötyöpäivää vuodessa.

Toukokuun liikevaihto oli itselleni pienoinen pettymys, vaikka työpäiviä oli vertailukautta vähemmän ja korona ymmärrettävästi häiritsi toimintaa. Rekrytahti tosin jatkui odotetun kovana ja avoimia työpaikkoja on vielä paljon auki, joten näyttää mielestäni siltä että markkinakysyntä jatkuu hyvänä loppuvuoden ja liikevaihdon kasvutahti kiihtyy loppuvuoden aikana.

Tuosta liiketoimintakatsauksesta vielä lyhyt otto:

“Liikevaihtomme oli toukokuussa 6,0 miljoonaa euroa. Se jäi viime vuoden toukokuun liikevaihdosta, koska työpäiviä oli peräti kolme vähemmän kuin vuotta aiemmin toukokuussa.

Ja uusi sopimuskin oli tehty ![]()

Onko tavoitehintaan tulossa päivitystä? @Joni_Gronqvist

Hyvältähän tuo toukokuu näytti. “Työpäivä korjatusti” liikevaihto kasvoi noin 10%

Eiks toi liikevaihto “työpäivä korjatusti” kasvanut yli 15%? Ihan hyvin joka tapauksessa ![]()

Jaahas väärään vuoteen tietenki vertasin ite lukuja ![]()

![]()

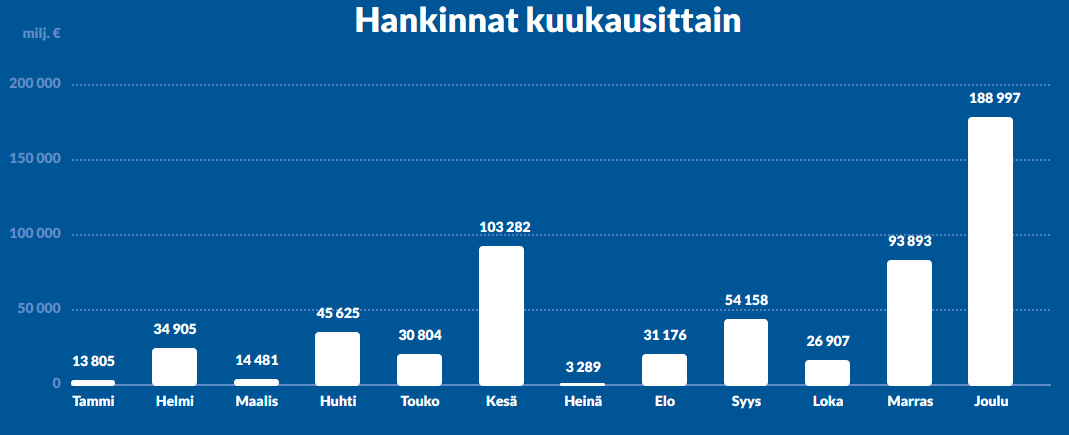

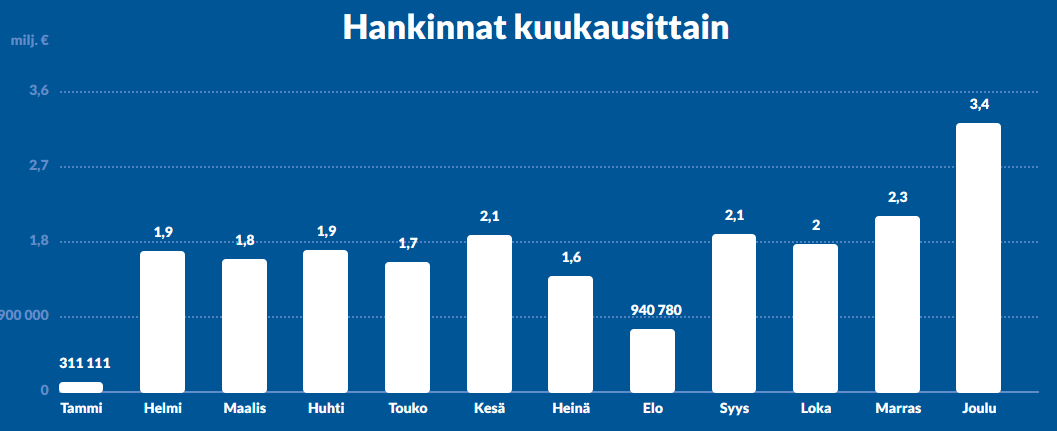

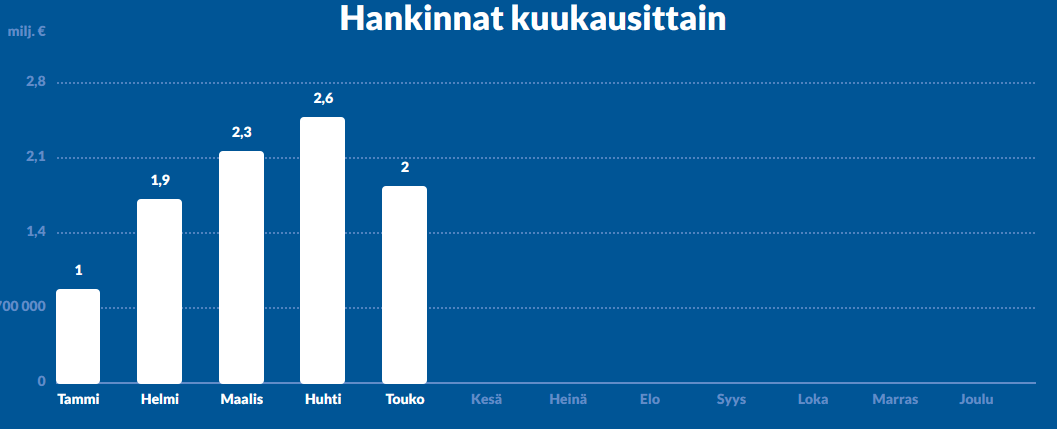

Jos odottaa vähemmän ja saa vähemmän niin silloin on tyytyväinen, mutta jos odottaa enemmän ja saa vähemmän niin on tietenkin tyytymätön. Tarkastellaampa valtion ja kuntien hankintamääriä 2019 vs 2020. Ohessa kolme kuvaa, joista ensimmäinen kuvaa Gofore Oyj:lta tehtyjä hankintoja kunnille 2019, toinen kuvaa hankintoja valtiolle 2019 ja kolmas 2020 tähän asti tehdyt valtion hankinnat. Kunnat eivät ole tehneet hankintoja ollenkaan vuonna 2020(!)

Valtionhankintojen kohonnut taso ja nouseva trendi latasivat ainakin allekirjoittaneelle toukokuun odotukset tappiin, jolloin perushyvä tulos oli pettymys. Toukokuun hankintojen tulos ja yhtiön liikevaihto olivat kyllä 2019 verrattuna hyviä. Tämän vuoden valtion hankinnat näyttävät olevan pysyvästi korkeammalla tasolla kuin viime vuonna, joten ainakin julkisen puolen osalta saa “hyvää” odottaa myös lisää ![]()

Mistä näiden kuvaajien takana oleva data on saatavilla?

Tutkihankintoja.fi. On tietenkin huomioitava että tuo ei kerro koko totuutta Goforen liiketoiminnasta, mutta se on yksi mittari mitä itse käytän. Rekryilmoitukset on esimerkki toisesta vastaavasta avoimesta datasta. Ylipäätään piensijoittajan kannattaa hakea informaatioetua vaihtoehtoisista tietolähteistä koska Pankkirii McPankkinaama ja Iines Insituutiosijoittaja eivät jaksa nähdä näin pienten yhtiöiden kohdalla yhtä paljon vaivaa.

Jonilta tuli uusi yhtiöraportti, jossa tavoitehintaa nostettu 9€:

https://www.inderes.fi/fi/kevat-sujunut-odotuksia-paremmin

@Joni_Gronqvist haluaisin kysyä tuosta loppuvuoden henkilöstömäärästä.

Raporttiin on laitettu riville Henkilöstökasvu, kk elo/syys/lokakuulle +2, mutta henkilöstömäärän on ennustettu pysyvän ennallaan? Miten tätä olisi syytä tulkita?