The annual report tells me of a company where the hype has worn off and which is, in its own segment, a steadily growing company with 37 employees working in international markets. Those aiming for quick profits (and who managed to grab them over a few years) have moved on to other targets. Company management has increased its own ownership stake. According to the CEO, the markets in 2023 were still disrupted by the consequences of the war in Ukraine and the pandemic.

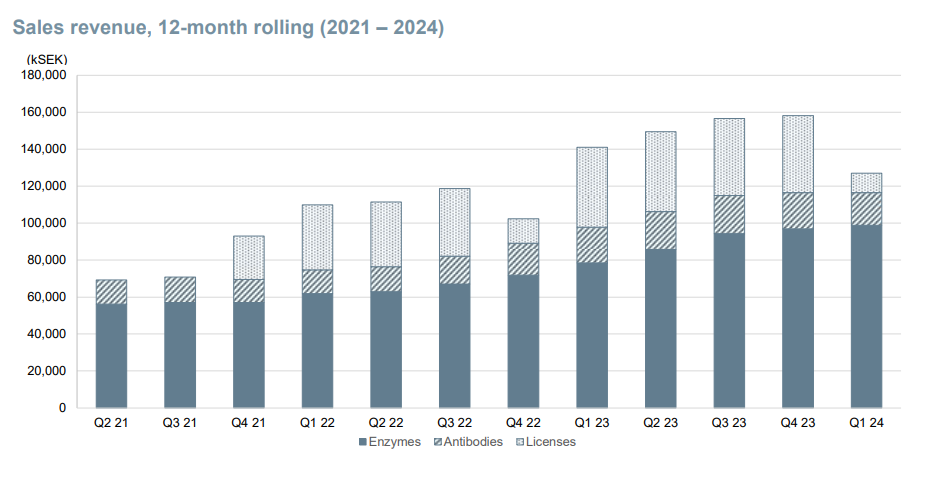

“Looking back at 2023, I can say that we have once again achieved our best performance to date. We increased our sales by 55% to SEK 158 million and our operating profit more than sixfold compared with the previous year. For the full year, the core business grew by 31%. Enzymes in analytics grew by 35% and the antibody business by 13%. At the same time that we moved the entire enzyme operation to new custom-built premises in Kävlinge, we have maintained our operational capacity, ensured the functionality of our new production facility and launched 4 new products.”

By the end of the year, Genovis has also found a use for AI (of course, by default, all players in the segment do so):

*"By the end of the year, we introduced Bioz Badges * on our website, an innovative tool that uses artificial intelligence to support researchers in their search and evaluation of scientific research and laboratory products such as our SmartEnzymes. Bioz Badges provide quick and reliable access to relevant scientific information about laboratory products and protocols, demonstrating our commitment to continuous innovation and improvement."

I’m still holding on to mine and considering adding more.

What’s the forum’s faith in Geno? The price just keeps falling, we’re already below the Red Eye Bear level. No news from the company, but there’s plenty of cash on hand?..

If I had extra cash, I would buy significantly more of this! It’s the largest holding in my portfolio, and if you have the patience to hold, you can’t help but succeed; all the key metrics are top-notch.

The core business is rock solid, and as we saw with Xork, news about licensing agreements could come at any time, which would give a big boost to the stock’s value.

Further comments from the CEO of Sequrna, extracted from that news piece:

CEO and Co-founder of SEQURNA, Björn Reinius (PhD), commented:

“My Co-founders and I are very pleased to onboard Genovis as a strategic partner. Since the launch of our first RNase inhibitor, things have been moving quickly and we see a strong demand for our product. We look forward to receiving the benefit of Genovis’ distribution platform and expertise in the industry, which will benefit SEQURNA’s growth and business development going forward.”

Sequrna was founded in 2022 and its products “provide customers with improved workflows, simplified storage and logistics, at a competitive price for the end user.” This seems like a very well-justified deal.

Genovis has an option to purchase the remaining shares of the company on June 30, 2027. 25% has now been transferred.

It would be interesting to know what part that antibody business has played in Genovis’s operations, i.e., how big a slice of the revenue will be carved out.

“We lower our 2024-2026 estimates by roughly 20%, reflecting revised projections following the report, the divestment of the antibody business, the removal of the anticipated follow-up for the 2019 bioprocess order, and some general fine-tuning. Consequently, our updated fair value range amounts to SEK24-102, with a base case of SEK52.”

“Historically, Genovis has traded at high multiples, and while it now trades at a significant discount compared to its historical levels”

“Genovis has been profitable since 2019, has a more or less debt-free balance sheet, and most key ratios point in the right direction. We expect the financial position to continue to strengthen during the coming years”

At least I’m not bothered by the sale of that Antipode business. Four years ago, when the company was acquired, I was a bit skeptical about how they would be able to handle and operate that US business from Sweden. Well, it never really took off, but fortunately, they’ve now gotten rid of that less profitable business area, and apparently for a pretty good price.

So, more cash in the coffers and a focus on the enzyme side. I assume the CEO’s comments from the previous reporting period about several negotiations with drug developers are still valid, so there could be positive surprises coming in the near future. If not, at least interest rates are coming down and the core business should roll along just fine.

As early as autumn 2019, prices were higher than they are now, so this has been pretty thoroughly beaten down. Back then, sales were 60 m, EBIT 10 m (vs. the current forecast of approx. 130 / 30). Danske also trimmed the target price slightly from 38->34, while still maintaining the buy recommendation.

I added a bit, but before making any larger additions, I’d like to see some insider buying.

Edit: Heh, well that purchase by Fredde came just at the right time. That was enough for me, thanks.

There are some purchases, not very large ones, but something nonetheless.

Genovis CEO buys shares for 0.3 million kronor

today at 12:22 ∙ Finwire Smallcap

Biotech company Genovis CEO Fredrik Olsson has on August 21st bought 12,500 shares. The shares were bought at a price of 24.88 kronor per share. The purchase price amounts to 311,000 kronor.

This is stated in the Swedish Financial Supervisory Authority’s (Finansinspektionen) insider register.

EDIT: And a second purchase as well.

Torben Jørgensen has on August 21st bought 10,350 shares in the biotech company Genovis, where he is the Chairman of the Board. The shares were bought at a price of 24.42 kronor per share. The purchase price amounts to 252,711 kronor.

This is stated in the Swedish Financial Supervisory Authority’s insider register.

The transaction took place on August 21st.

Jørgensen previously owns 105,000 shares in the company.

EDIT: And a third.

Magnus Långberg has today, August 23rd, bought 4,100 shares in the biotech company Genovis, where he is the CFO. The shares were bought at a price of 23.80 kronor per share. The purchase price amounts to 97,580 kronor.

This is stated in the Swedish Financial Supervisory Authority’s insider register.

Was it the news of the new enzyme update announced yesterday that boosted the share price by 14% today? The Q3 report isn’t due until November. It has been tough to own the stock and watch Geno’s decline during the period of COVID-19 and the war in Ukraine. At least SEB raised the target price to 30 SEK.

Genovis AB, a leading provider of innovative enzyme technologies, announce the launch of FabRICATOR® Xtra, the second generation of its widely used FabRICATOR (IdeS) enzyme. This newly developed enzyme is specifically designed to address the evolving needs of biopharmaceutical development by efficiently digesting next-generation antibody-based therapeutics with mutations designed to enhance their therapeutic properties. New generations of antibody-based therapeutics, designed with structural mutations, have posed a challenge to traditional enzyme technologies. These therapeutic antibodies, while offering enhanced efficacy and stability, could not be digested with legacy FabRICATOR® (IdeS), preventing researchers from utilizing the efficient middle-level workflows previously enabled by the enzyme.

"Our Best Quarter in the Enzyme Business: Strong Growth and improved profitability

July – September 2024

Genovis executed a strategic acquisition of a 25% stake in Sequrna AB

Genovis successfully completed a strategic divestment of its Antibody Business to Leinco Technologies Inc.

Net sales totaled SEK 32,895 (30,186) thousand, with a growth rate of 9%. Adjusted for currency effects, the growth was 13%. Net sales for the enzyme business (excluding the antibody business) amounted to SEK 31,625 (25,426) thousand, reflecting a 24% growth, or 28% when adjusted for currency effects.

Operating profit before depreciation and amortization (EBITDA) totaled SEK 24,566 (7,555). EBITDA for the enzyme business (excluding the antibody business) amounted to SEK 10,828 (6,801) thousand.

Operating profit (EBIT) totaled SEK 22,054 (4 488) thousand. EBIT for the enzyme business (excluding the antibody business) amounted to SEK 8,545 (4,405) thousand.

Profit for the period totaled SEK 13,798 (3,138) thousand.

Earnings per share totaled SEK 0.21 (0.05).

Comprehensive income for the period totaled SEK 14,570 (4,051) thousand.

Cash flow from operating activities was SEK 723 (9,611) thousand. Adjusted cash flow from operating activities excluding the antibody business was 4,937 thousand.

Cash and cash equivalents at the end of the period totaled SEK 155,534 (119,131) thousand."