CEO’s review from yesterday’s AGM! ![]()

9 Likes

Thomas interviewed Framery CEO Samu Hällfors and CFO Lauri Isotalo regarding Q1 ![]()

Topics:

00:00 Introduction

00:17 Sentiments after the listing

00:54 Differentiation in soundproof workspaces

04:02 First quarter development

04:51 Revenue growth

06:04 Impact of geopolitical uncertainty on customers

07:26 Largest customers

09:28 Opening a new factory in the United States

11:23 Market-specific differences in demand

7 Likes

Good morning to the thread!

Finally, we have initiated coverage on Framery!

We started with a target price of 8.5 euros and an Accumulate (lisää) recommendation.

We didn’t manage to catch the dip, but despite the recent share price rise, I think you can still get on board the story at a reasonable price. Normalizing orders from a major key account, coming down from an exceptionally high level, are expected to weigh on the company’s reported performance over a one-year horizon. However, during that time, I will personally focus more closely on the development of the rest of the customer base and, through that, the development of the company’s competitiveness. Personally, I believe that the new generation of pods launched in 2024 supports the company’s competitiveness, at least for the coming years (nominal prices were kept unchanged in the new generation, even though product quality and functionalities were improved).

Despite strong growth, the investment story also combines a generous profit distribution, where the distribution policy even flirts slightly with share buybacks. At the company’s ITF (Inderes Toy Factory) event, I questioned the heavy dividend distribution instead of more aggressive growth investments, but sparring with the management convinced me that it is not worth expanding the value chain position into more capital-intensive operations, where more capital could theoretically be sunk. One investment angle for the Framery story would, of course, be acquiring a smaller product house and scaling sales through Framery’s global distribution network, but I personally favor capital distribution over forced M&A deals.

In the report, I perhaps spent a bit too much space on the company’s services (pod rentals and smart office SaaS services), which are still in their infancy. However, these will play a key role in maintaining the company’s growth potential over the next 10 years. For now, Framery has an estimated 20% share of the pod market, so there, the company’s growth will inevitably approach the market growth rate.

48 Likes

Let’s hope on behalf of Finland and Finnish investors that the business progresses brilliantly or Blackstone buys the whole outfit in a month with a massive premium ![]()

Personally, I wouldn’t dare put my money into a company that makes fixed phone booths for dying offices (yes, an exaggeration).

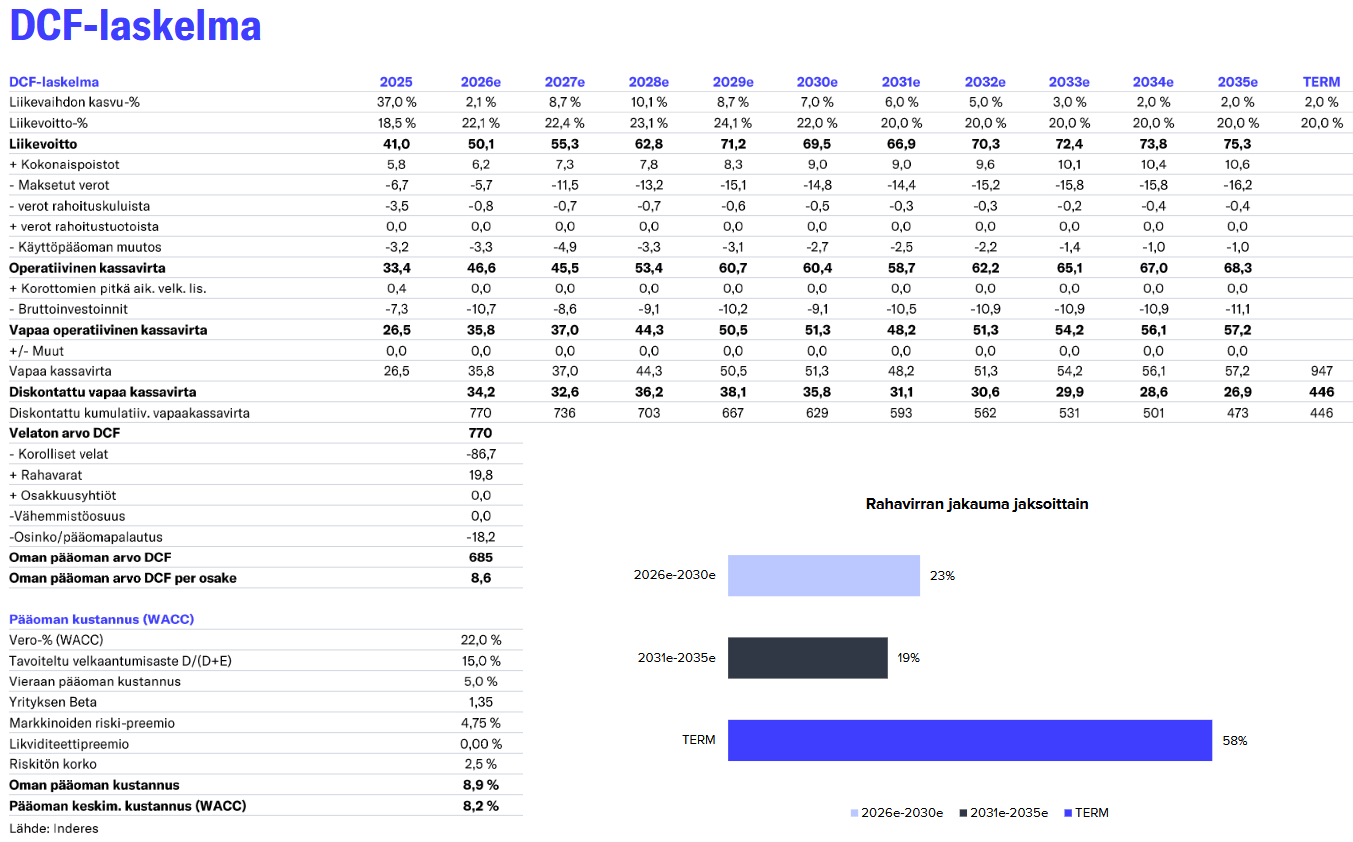

When you plug in:

- Low cost of equity (relatively)

- Low WACC (relatively)

- High growth assumptions

- High profitability assumptions

You get a small upside from the DCF model to the share price

![]()

The return on capital figures say quite a lot about the forecasts.

Harvia is one of the highest quality companies on the Helsinki Stock Exchange. The forecasts suggest that Framery will easily achieve a better return on capital than, for example, Harvia ![]()

9 Likes

I have to admit that based on our coverage, the expectations for Framery are certainly on the higher end, but then again, few companies can match their historical track record of value creation.

Of course, the “aggressiveness” of assumptions always depends on the benchmark. Relative to the company’s own track record? In our 2025–2035 forecasts, revenue grows by a total of 70%, whereas by comparison, it grew by 37% last year and averaged 21% between 2018–2025. In euro terms, the €154M growth in our forecasts is less than the €217M the company achieved during the previous decade. Granted, the category was in a hyper-growth phase then, and no one knows how many statistical outlier events helped the company’s success along the way.

Compared to the category’s projected growth figures of 12–15% reaching until 2030, my forecasts actually predict a loss of market share, although in the report, I expressed my own skepticism towards such strong market growth. Forecasting, especially further into the future, is very challenging, so time will tell.

They do say something about the forecasts, but also about the business model.

I agree with you regarding Harvia’s quality, and while quality correlates with return on capital, you cannot put an equals sign between them. In some businesses, a high return on capital is a characteristic of the business model. Rush Factory, which I previously followed, is probably a great example of this from its golden years.

Framery’s and Harvia’s business models differ in that Harvia carries out heavy production itself, whereas Framery only assembles its products and outsources the production of modules. Consequently, the company’s business model ties up less capital, which supports the return on capital. For context, Harvia’s Return on Invested Capital (ROIC) adjusted for goodwill was 41-43% in 2024–2025, while Framery’s corresponding figure was 93-131%. Does this indicate higher quality than Harvia? No, but it does signal that Framery’s business model is more capital-light.

15 Likes

We also made a video about Framery with Thomas. ![]()

16 Likes