I don’t know if it’s the case that the other operator needs premises, and that involves rents and so on, and Fodelia doesn’t. However, the differences are so great that it probably doesn’t explain it nearly completely.

Or perhaps Compass made that offer with the mindset that they’re not really that interested, but let’s offer anyway. And if we win, then there will be big profits.

I “managed” to listen in Swedish. Good job @Isa_Hudd!

For those who didn’t manage, let’s briefly refer to the part concerning Fodelia. So this major investor only owns 5-7 stocks at a time, and indeed, Fodelia has been selected as one of them. He said that he thoroughly researches companies before making an investment decision, and discusses with the company’s management and even visits the company. I got the impression that he had done this with Fodelia as well. When it comes to a Finnish company, “google translate” comes into play when the language is “wrong”.

It would certainly be interesting to see what it looks like inside the company I “own.” For example, what the autoclaves look like and how big they might be, etc. It’s really intriguing. These probably can’t be shown much due to trade secrets.

Additionally, I’d be interested in, for example, the amount of potatoes. Are they bought and stored in the factory’s premises and warehouses, or do the farmers store them in their own bins and Fodelia buys them in batches, for example, a truckload at a time. There must be quite a potato mountain there.

Perhaps that information could also be found somewhere if one really put in the effort and searched. It’s nice to ponder such things

It’s been a couple of years since my last visit, but I recall the autoclave machines looking roughly like this (image from Google). Would the cylindrical device have a diameter of slightly over a meter? In the rack, food hermetically sealed in plastic is placed inside, which cooks in the autoclave. This stage is naturally preceded by another production line, where raw ingredients are dispensed into plastic on a conveyor belt and hermetically sealed.

The potato storages for snack production seemed relatively large to me, but I cannot estimate the inventory turnover time. Perhaps we can discuss this during the next visit.

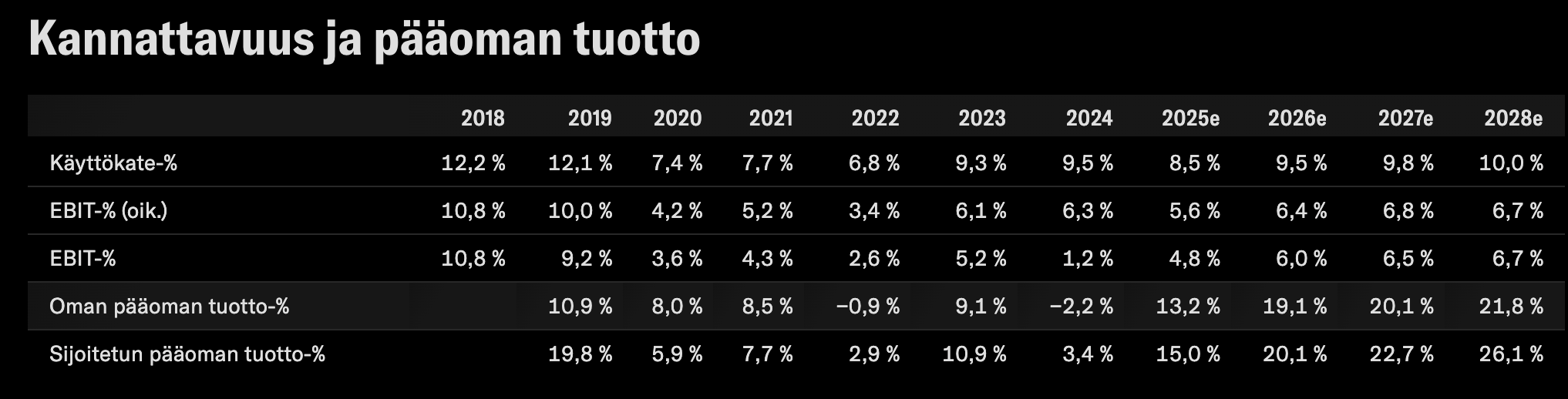

Fodelia has grown exemplarily since its listing in 2019, but capital has been allocated to bad acquisitions and administrative costs have ballooned. From a cluster of many companies, literally two gems can be found among the chips.

That was a nice video. Concise and full of info. Thank you.

The most interesting part was the discussion at the end about an acquisition, meaning some big company buying out all of Fodelia.

My own thoughts.

Conflicting thoughts. I don’t like big global companies. Or I like them and I don’t. From an economic and investor perspective, this would probably be a nice thing, if we’re only talking about money, productivity, etc.

Otherwise, I don’t fundamentally like it when big companies eat small ones. If we look at the retail sector, for example. We have the S- and K-groups, Lidl with about a 10% share, and crumbs for others. Is this nice now – yes and no. Prices can be squeezed down, but in a way, the culture suffers. Every municipality in Finland looks exactly the same. Absolutely every single one. Hypermarket hells a few kilometers from the center, and the same shops can be found everywhere. In smaller municipalities, an S-market and a small K-store. Not good. Not nice.

And about chips. The Oikia brand, in my opinion, would need a huge marketing campaign. Enormously big. It would cost a tremendous amount. To do it, or to struggle in the shadows of Taffel and Estrella. The product is excellent. I like it.

The main owner wrote this in 2022, when the company was criticized for a relatively young person bearing the Tahkola name from the second generation joining its board. I pondered the speculation mentioned in the video regarding Fodelia, i.e., could Fodelia be an acquisition target. I tried to recall if this had been asked directly in any interview, but I don’t remember such a thing.

From the main owner’s writing, one gets the impression, at least at that time, that a future is also being built for the family’s offspring. And this is not the only statement where I remember hearing such intergenerational thinking from the company’s main owner. Of course, since then, water has flowed in the Pyhännänjoki river, and as I understand it, a few people already got their own business to run from Pita Factory in Jokioinen. As one possibility, I have considered that since the ex-CEO has a long history with Real Snacks, it might be spun off for the offspring to run (if the shareholders so decided).

In the short term, I don’t see this as the most likely scenario, even though it is conceivable and undoubtedly becomes a more attractive option year by year, as the company gains more foothold in public catering and wins large tenders thanks to its cost-effective and public-funds-saving business model.

At the same time, I must tip my imaginary hat to Mikko for consistently driving the company forward, despite the headwinds and complications along the way. The company, despite not being among the best performers in my own portfolio (quite the opposite), is interesting to follow, and its business, etc., are easy to understand. Following companies like this teaches a great deal about both the companies themselves and society.

In many sectors, there are companies that have a price/quality ratio that gives them an advantage in tenders. However, few can imagine benefiting from continuous cuts and savings. Municipalities tend to employ “their own,” and kitchen staff are more likely to find coders or consultants (well, with a reservation). However, tightening regulations are pushing food services towards free market economy conditions, and on top of that, Fodbar is the domestic choice even among the tough competitors.

If expansion gains momentum, it could be seen as a very recession-proof defensiveness, because people cannot live long without eating. And yet, the industry is so dull and boring that not every rapper and ex-athlete is rushing in with their world-changing AI and savings.

However, the number of care institutions and their client numbers are growing, and everyone should be fed more efficiently.

Fodbar can certainly hire the same people who previously worked at the municipal enterprise. So, the municipality’s own people still get work. It’s unlikely that kitchen staff would want to travel very far to work.

On the other hand, heating Feelia’s products probably employs fewer people than preparing food entirely on site.

Hopefully, this possibility will also be highlighted when trying to negotiate deals with municipalities. It would get rid of one change-resistant bogeyman.

As a side note regarding the linked article, one can only wonder why municipalities don’t have a real desire to make significant savings in their finances. From the article: “The municipality estimates that the new model will achieve savings of 600,000 euros per year.” Horrendous money for a small municipality. One would think that promising such savings would already create a long queue at Fodbar’s door…

If residents were asked whether they want to keep 10 jobs in the kitchen or keep village schools open, they would probably always choose the village schools. So that saving could be made in quite a few municipalities if spending were presented to residents with a better alternative. And that question is relevant in quite a few municipalities, now and in the future. Of course, each in its own scale.

I like to own companies from which I benefit as an owner and a taxpayer. I guess the benefits of this company will eventually come to me as an owner too

Fodelia could be a classic turnaround company, where under the chips lies a real gem – the capital-light, fast-growing Feelia. The management team is being shaken up, and the previous building of a chip-kebab empire has shifted towards focusing on better business operations. That’s why I enticed Pauli a month ago to talk about it in a video, in case a wider audience would be interested in taking a look.

Pauli’s fresh comment on the management team changes.

On the other hand, the P/E is now around 20x, so this doesn’t look like a bargain bin case. But if one believes in strong growth in the coming years, it’s not necessarily bad.

The company’s wandering is clearly visible in how the excellent profitability (measured by return on capital) of the IPO year 2019 was allowed to collapse (a familiar phenomenon in Hesuli ). But there’s probably no reason why it couldn’t recover when things are done right again.

Addition. The more I’ve thought about artificial intelligence lately, the more companies that purely do software, tools, and expert work seem vulnerable. Fodelia hardly needs to stress about such technological changes, nor is the company’s autoclave technology likely to generate so much interest in California that competitors would start pouring hundreds of billions into autoclave equipment.

Fodelia hardly needs to stress about such technological changes, nor is the autoclave technology used by the company likely to arouse such great interest in California that competitors would start pouring hundreds of billions into autoclave equipment.

But is it enough for HKFoods and Atria to start pouring money into autoclave equipment? I don’t know, but I just threw the question out there.

Atria’s revenue last year was 1775 million euros, while Feelia’s was 35M€. Feelia’s revenue is a rounding error in Atria’s size class.

Yep. @Pauli_Lohi could comment on customer retention and switching costs. Can just anyone rush into the market after ordering an autoclave device home? Businesses like HK Foods, which make 5-10% return on capital, surely look favorably at Feelia’s +20% returns, although the scale is still negligible for them.

It’s easy to answer this provocative question by saying that challenging Feelia is not that simple. Below are points explaining why a business cannot be copied by simply buying a few autoclave devices.

-Recipes. Feelia’s selection includes over 200 different products. Recipes suitable for autoclaves also differ from other preparation methods. These recipes have been developed over years in cooperation with customers, such as kindergartens and hospitals, to meet precise nutritional requirements. Copying this cannot be done in an instant.

-Own ordering system FERP, through which Feelia already delivers about a quarter of its products. This is particularly popular among smaller customers who need an easy overall solution for food service instead of ordering different elements from a wholesaler themselves.

-Scale. Feelia already has relatively large delivery volumes in its own niche segment, which supports operational efficiency. A new player would have to start production from scratch, which would initially weigh down production profitability. In practice, a potential new player should focus only on individual products and sell them, for example, to wholesalers. I have not seen any signs of this.

-Operating models of larger competitors. Large food companies focus on high-volume products and channels, such as retail and restaurants. Investments are directed towards products for which there is already demand and clear distribution channels, so investments turn profitable relatively quickly. Developing new business models in a large organization is difficult. Copying Feelia would mean significant losses for a competitor in the first years of operation, which would be taken from elsewhere (e.g., dividends, investments) and would frustrate owners.

-Long-term profitability would be uncertain. However, the industry is not so large and profitable that it would necessarily provide a return exceeding WACC for several players simultaneously. Of course, the market potential is high, but it will only materialize gradually. As the market opens up, Feelia’s size and first-mover advantage will only grow.

Feelia’s plate model. What kind of sustainable plate model is there for tomorrow?

“More vegetables and fruits, less milk and meat. The pace of the former plate model was set by humans, but now it’s the environment’s turn. Because the world won’t be saved by mediocrity.”

This excerpt is indeed from Fodelia’s 2024 annual report and sustainability review. On page 39.

However, I would personally hope that humans and their nutritional needs are still primarily taken into account, especially considering that Feelia delivers meal portions to kindergartens for small children. In my opinion, the text in question, within quotation marks, is somewhat harmful, and I wonder if such a “sustainable plate model” truly serves Feelia’s customers?

Feelia’s selection is indeed extensive, and there are options for different needs. We just ordered meals home for us, who eat meat/mixed diet, as well as for our teenage daughters, who follow a vegan diet. More vegan options were found than in restaurants. And there was no impression of excessive climate fuss – the customer gets to choose, there are options.

How do you see Fodelia as an acquisition target in the future? Now that the main owners are no longer operationally involved, I personally believe it will increase their interest in selling.