Nitpicking, but can one say that Partnera is Oulu’s gift to the Helsinki stock exchange when it is not listed on the stock exchange but on a regulated market (First North)?

Tommi and Frans-Mikael made a video with a new concept, where they go through Partnera’s recent comprehensive report.

Topics:

00:00 Introduction

00:56 Partnera’s history

04:05 Business of Foamit Group subsidiary

10:15 Strategy and financial targets

18:00 Foam glass market

22:13 Financial situation

24:04 Analyst’s forecasts

25:57 Valuation, appraisal, and recommendation

Feedback on the new video concept is welcome - good and bad, and other development ideas.

3 Likes

Is there any scenario where EcoUp could transfer to Partnera or some kind of merger?

Synergies could perhaps be gained in sales, logistics, warehousing, and marketing.

Raw materials, on the other hand, seem to come from very different sources. I understand that Foamit gets a lot of raw material from consumer packaging (Rinki recycling), and also some from car repair shops. Perhaps window panes from building demolition sites. EcoUp, on the other hand, gets surplus insulation from construction sites, meaning raw materials come from different life cycle stages of buildings. The end-use also seems to be focused on infrastructure for Foamit, while Ekovilla focuses on building construction, even though foam glass is also used on house construction sites. EcoUp, to my understanding, has also at least had technology that needed to be licensed, whereas Foamit Group does not have unique technology / manufacturing process.

If Partnera wants to transform purely into Foamit Group and focus specifically on foam glass, this would not make sense. If Partnera, on the other hand, wants to be a building material manufacturer in general, with a circular economy angle, there could be an idea in a merger. Or could there be? I don’t know if this would be the most optimal option from investors’ perspective, but if Partnera were indeed to be built into a building materials manufacturer benefiting from the circular economy, there might perhaps be an idea here.

However, both require significant investments, so funds would have to be divided between both upon merging, or all resources used for one, forgetting the other. In that case, one would wither, and the other would grow at the expense of the other. On the other hand, a merger would bring additional size and bigger muscles.

Someone wiser than me could say how likely such a scenario is.

3 Likes

Here is a new company report from Tommi at Partnera after the latest announcement. ![]()

Partnera announced yesterday that it had acquired the minority stakes in its only operational subsidiary, Foamit Group. As a result of the arrangement, Partnera fully owns Foamit Group. The purchase price was close to the value we estimated for the minority stake, which means that the impact of the arrangement on the Partnera Group’s value remained, in our opinion, minor. We added the impact of the ownership arrangement to our forecasts, but we did not make any other forecast changes. We reiterate our target price of EUR 0.85 and our Reduce recommendation. Our recently published comprehensive report on Partnera is up-to-date, especially regarding Foamit Group, and can be read freely here.

1 Like

Quite good reflection. I myself have not considered this a likely scenario, but here are some thoughts that, in my opinion, argue against a merger

Factors decreasing the likelihood of a merger:

- Partnera’s strategy focuses specifically on Foamit Group and foam glass, and on growing this business. However, this is quite far from EcoUp’s business, even though both companies’ products are related to insulation.

- Partnera’s strategy mentions acquisitions, but also the expansion of the foam glass business into new markets. Thus, I think that acquisitions would primarily target new geographical areas.

- In Partnera’s strategy, investment company-like operations seem to be taking a smaller role, which makes a leap into completely new types of products seem unlikely.

- EcoUp recently divested Uudenmaan Imupalvelu, which, to my understanding, has sometimes blown foam glass into insulation targets, which would make synergies weaker than before.

The biggest supporting factor, in my opinion, is the likely divestment efforts of Partnera’s main owner, the City of Oulu, from its Partnera ownership, which would likely lead to a broad consideration of various options. On the other hand, a merger would not solve this ‘problem’ either, as the City of Oulu would fundamentally acquire shares in the merged company. EcoUp, on the other hand, does not have the financial firepower on its balance sheet to acquire Partnera’s Foamit Group, even if there were a desire to buy. In summary, I would consider a merger quite unlikely.

4 Likes

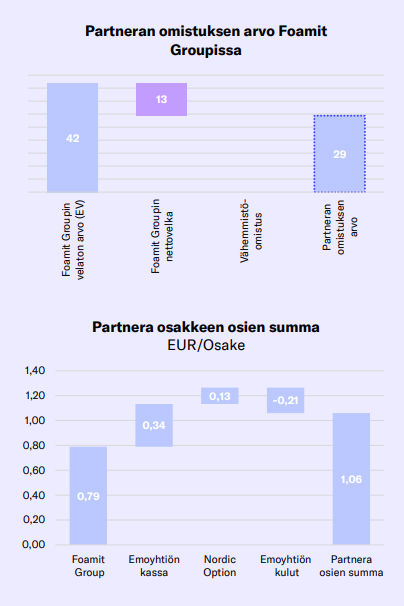

@Tommi_Saarinen I tried to get a grasp of Partnera, but I didn’t quite understand why the company report https://www.inderes.fi/files/e7ac8121-e65d-4208-bfda-18035fe90d7c talks about a significant net cash position, but the enterprise value is greater than the market value, shouldn’t it be the other way around? The same thing in the comprehensive report from May. In that case, are the valuation multiples, e.g., EV/EBITDA, also correct? Thanks in advance for clarifying this ![]()

1 Like

Here are Kaisa’s comments on Partnera’s new CEO. ![]()

Here is Tommi’s preview report, as Partnera publishes its H1 report this Thursday. ![]()

We expect Foamit Group to have achieved slight revenue growth and an improvement in profitability, supported by the favorable development of the infrastructure market. We made forecast revisions related to depreciation and completed ownership arrangements, which, however, did not affect our share valuation. Consequently, the risk-reward ratio remains subdued according to our assessment, and we reiterate our Reduce recommendation and our target price of 0.85 euros.

This is truly a company that flies under the radar; month after month the analyst has wrong figures in the analyses and no one corrects them ![]()

Hi, and apologies for the delay in response. I’ve been trying to take late holidays between these results.

In that report, I still kept Foamit’s debt and Partnera’s cash separate in the valuation, based on the previous sum-of-parts model and group structure.

You are right that talking about net cash in that context is misleading (one should talk about the parent company’s cash). ![]()

In the tables, the 2025 EV takes into account the investments I forecast during 2025, as well as Foamit Group’s debt, which, in the forecast, shifts the balance sheet to net debt.

The EV multiples in that report were “usable” with the exception of the Nordic Option ownership. The same applies to the latest report now, where we have moved away from the sum-of-parts as the group structure has become clearer.

From the June 19th report:

In the image, the parent company’s cash and Foamit Group’s net debt were roughly equal to each other, meaning the group’s net cash was close to zero.

2 Likes

Tomppa has prepared a new company report after Partnera’s H1. ![]()

Although Partnera’s H1 realized figures mostly fell short of our expectations, the strengthening of relative profitability and a higher order backlog than we expected compensated for the overall picture of the report. However, forecast changes were mostly negative. Tight short-term valuation keeps the risk-reward ratio subdued, which is why we reiterate our Reduce recommendation and our target price of 0.85 euros.

Quoted from the report:

The order backlog strengthened by approximately 6% from a year ago to EUR 23.8 million, and we expect the order backlog deliveries to be mainly scheduled for H2. Compared to the year-end figure of EUR 18.6 million, the growth in the order backlog is significant (~+30%). Consequently, we expect clear growth in delivery volumes for H2 compared to H1 levels.

2 Likes

SalkunRakentaja has published a comprehensive article about Partnera. ![]()

Partnera has purposefully transitioned from an investment company to an industrial circular economy player, and now the company’s value creation is practically entirely based on the development of Foamit Group. This has significantly clarified the stock’s investment profile as well.

Investors should focus specifically on Foamit’s business development and value creation in the coming years, rather than examining the stock in light of Partnera’s past history.

Note.

IR-ikkuna is a channel for SalkunRakentaja’s and Sijoittaja.fi’s corporate partners for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

1 Like

Soon we can change the thread name… here are Tommi’s comments on that. ![]()

3 Likes

Tommi’s comments on Foamit’s small order. ![]()

1 Like

Joint venture to Europe, foothold 50% stake in Reiling’s subsidiary Veriso, current revenue approx. 6m EUR

Inside Information: Foamit and Reiling signed a letter of intent for a joint venture project in Germany

Foamit Oyj (formerly Partnera Oyj) has today signed a letter of intent with the German company Reiling GmbH & Co. KG for cooperation in the foam glass business. According to the letter of intent, Foamit will negotiate the acquisition of a majority stake in Veriso GmbH & Co. KG, a foam glass manufacturing subsidiary of the German circular economy company Reiling.

Foamit’s goal is to acquire an ownership stake of over 50 percent in the joint venture project with an initial investment of approximately 3 million euros, with Reiling remaining the second owner of the joint venture. The joint venture project includes Veriso and its two existing foam glass factories, as well as a new foam glass factory to be built. The parties aim to sign the agreements related to the implementation of the joint venture project by the end of March 2026.

The aim of the cooperation is to develop and expand Veriso’s current production facilities for foam glass and to build a completely new foam glass factory in Germany. The joint venture project creates a fast expansion opportunity for Foamit into the Central European markets.

Veriso’s current revenue is approximately 6 million euros, and it manufactures foam glass in two production facilities, with a production capacity of approximately 100,000 cubic meters. The plan is to develop and expand Veriso’s existing production facilities, as well as build a completely new factory on an existing plot of land.

Foamit and Reiling are also exploring opportunities to increase cooperation in the recycling business in the Nordic countries.

From Germany to other parts of Central Europe

The acquisition of Veriso and the increase in production capacity create a good foundation for Foamit to quickly open markets in Germany. In addition, the goal is to export foam glass from Germany to other parts of Central Europe. Low-emission foam glass produced from recycled materials offers an environmentally friendly alternative for various infrastructure and building construction projects compared to currently commonly used products, e.g., plastic-based products.

“Cooperation with Reiling offers Foamit an excellent opportunity to increase revenue in the coming years. The joint venture project in Germany, in addition to the already implemented commissioning of new capacity in Norway and the investment in increasing the production capacity of small foam glass fractions in Finland, will promote the achievement of our growth targets,” states Erja Sankari, CEO of Foamit.

“Foamit has been a long-term partner for Reiling, and our mutual trust is a good basis for the new cooperation project. For us, foam glass production has been one of the areas of our extensive recycling business. I believe Foamit will bring much-needed strong technological expertise and the ability to further develop operations to Veriso,” says Tom Reiling, CEO of Reiling.

Reiling GmbH & Co. KG is a German family business and recycling expert, primarily serving industrial, commercial, and municipal sector customers. Reiling is one of the market leaders in glass recycling in Europe and also recycles plastic bottles, solar panels, and timber, among other things. Reiling has 12 production facilities in Germany and several units in the Netherlands, Denmark, Sweden, and Poland. Its revenue in 2024 was approximately 220 million euros, and it employed 690 people.

5 Likes

Here are Aapeli’s fresh comments regarding this latest news. ![]()

Foamit announced on Friday that it had signed a letter of intent to acquire a majority stake in Reiling’s German foam glass manufacturing subsidiary. We believe the arrangement is well in line with the company’s growth strategy and offers it the opportunity to expand into the Central European markets. The letter of intent has no immediate impact on our forecasts, and we will await the completion of negotiations.

7 Likes

Foamit’s CEO Erja Sankari spoke about her company at the Investor 2025 event ![]()

4 Likes

Tommi interviewed Foamit’s new CEO Erja Sankari. ![]()

Topics:

00:00 Introduction

01:05 New CEO

07:38 Partnera’s transformation into Foamit

13:39 Foam glass

17:58 Growth strategy

26:52 When is foam glass needed?

4 Likes

Here are Tommi’s comments as Foamit transitions from national FAS accounting to international IFRS reporting. ![]()

Foamit Oyj’s transition to international IFRS reporting is a strategically justified step that supports the company’s internationalization goals and improves the transparency of investor communications. While the change technically improves reported earnings figures, it does not significantly affect the company’s cash flow or the basis of its valuation. We will update our forecasts to IFRS format no later than in connection with the H2’25 preview commentary.

3 Likes

Foamit has started to interest me, and I now own a slice of it.

The product is, as I understand it, quite good. Foam glass is circular economy in construction at its best. Waste streams are used to manufacture a technically excellent product.

Foam glass can be used in similar applications as Leca gravel, which has been known and used in the industry for 70 years. To my surprise, the price of foam glass is in the same range as Leca gravel. A cubic meter bag from K-Rauta is about €230 for both. I can’t say about the price differences for full truckloads. Does anyone have an idea in which property foam glass would clearly lose out to Leca gravel? I’m trying to figure out why foam glass wouldn’t take market share from Leca gravel.

A few questions about the company that arose while reading the initiation report and getting to know the company. @Tommi_Saarinen

-

The City of Oulu is the largest owner. How should this be viewed? Is a city as an owner similar to the state?

-

Why is EBITDA reported instead of operating profit? Isn’t EBITDA “bullshit earnings”? What could the company’s 2028 target of 20% EBITDA correspond to in terms of EBIT %?

-

In my opinion, Foamit has a lot in common with LapWall. A technically good product that aims to take market share from an alternative way of building (Leca gravel). The price is competitive and the product’s eco-friendliness provides an advantage. There is room for improvement in brand awareness. Both are building product companies whose operations are based on modern factories. Foamit’s gross margin is 50%, while LapWall’s is 35%. Isn’t that 50% gross margin really good for a building product company?

I’m mainly trying to figure out whether those 2028 targets for the company are realistic or not.

Currently, in summary, Foamit appears as follows in my own thoughts:

- Good product and good gross margin

- Plenty of growth drivers

- Valuation is somewhat tight(?) in the short term, but the horizon is several years away.

- The transition from Partnera to a building product company muddies the picture.

6 Likes