Quoted from the CEO’s review in the financial statement release

“Nearly 80 percent of our software development work is either entirely AI-generated or AI-assisted, which has shortened development cycle durations to less than half in 2025.”

This is interesting in the sense of whether this development work can be converted into revenue or alternatively into improved profitability at the same rate. As we learn to utilize AI even more as a tool, will the development cycle be cut in half again, and then by half again..

F-Secure CEO Timo Laaksonen was interviewed by Atte.

Topics:

00:00 Introduction

00:12 Fiscal year summary

03:32 Cash flow development

04:07 Tier 1 operator contracts

06:15 Negotiations for a significant contract

08:04 Direct sales

10:30 Guidance and targets

Great job Sari, and good that you’ve still got your gloves on.

I’m probably a bit simple-minded, as in my view, the first announcement about a potential new customer was specifically a status update. Surely it’s nothing new that a listed company engaged in commercial activities tries to gain new commercial partners or customers? And some of them might be approaching the signing phase? And in that status update, it was implied that the contract would be signed roughly at the turn of the year.

From an investor’s perspective, the situation is more or less that R&D investments have been made specifically to get this deal signed and for the collaboration to begin during Q2. Since we are 5 weeks past the estimated schedule and presumably 40% of the Q2 buffer has been eaten up, the risk of the customer relationship not materializing in the end has increased—or if it were to luckily happen that the signing occurs, a Q2 launch is, if not implausible, at least something that will put the organization under a lot of strain.

And that’s a bad thing for a speculator like me, who believed that a status update isn’t given unless they are 99.9% sure about it.

“We reiterate our Accumulate recommendation for F-Secure, but revise the target price to EUR 1.9 (prev. EUR 2.0) in line with lowered earnings forecasts. F-Secure’s growth is accelerating this year, driven by new major Tier 1 partners, but unfortunately, this is still reflected negatively in the earnings figures due to the investments required to serve these large partners. The lack of earnings growth is also visible in the stock’s low valuation (2026e P/E 11x), and so far, the wait has been long. However, the Tier 1 strategy is now truly getting underway this year, and there is clear potential for growth acceleration in the coming years. Thus, the risk-reward ratio still favors waiting for the growth to accelerate with a cautiously positive outlook.”

–

OP reiterates BUY and lowers the target price to 2.10 (prev. 2.20)

We agree that the November announcement was unfortunate. We would absolutely prefer to communicate only about certain and finalized matters. Atte has already commented on this here previously. In accordance with our disclosure policy, this agreement is so large that it required an insider project. As negotiations moved to the fine-tuning stage of the contract, it became apparent that there were several third parties who knew (or more accurately: were able to deduce) that we had “won” the tender. We were therefore no longer able to ensure that the information would remain confidential. We discussed the situation with both the stock exchange and the Financial Supervisory Authority and decided to announce the situation. The situation is, of course, unfortunate – but it is part of our strategy where sales to consumers take place through partners. Consequently, there are many things we cannot control ourselves. There are always two parties involved in fine-tuning an agreement. We will provide an update as soon as there is relevant new information to share.

I’m still on the cautious side myself. I don’t see the product quality as being better than competitors, and I’m not quite sure I understand the potential competitive advantage brought by the chosen strategy. After all, there have been a few years of weak stock performance and expectations have been raised before.

On a general level regarding that interview, can anyone estimate what the market potential is for, say, the (signed) Tier 1 client relationship mentioned in the interview?

Reasons why I am cautious:

Qualitatively, I see little difference between the quality of F-Secure’s products and those of its competitors. I would guess that F-Secure is better on Windows devices, but partly weaker than competitors on Apple devices and mobile. The password app is the weakest, quite “stone-age”, the VPN is okay, the security side is likely good, and being European is definitely a plus. In terms of reputation or capability, I don’t recognize any unique competitive advantage.

The idea of Total back in the day was likely that you buy one product and use it to protect computers, tablets, phones, and even IoT (Sense). This also seems to be quite central to competitors’ offerings. The idea that in the future, one would buy a separate security app for their phone, computer, TV, and sports watch through the device manufacturer or operator fits quite poorly with this. Maybe it could go that way, but as long as there is a single security app and password bank that works seamlessly cross-platform, it’s hard to see how such a strategy could gain a broader foothold.

Just as a practical example as a Total user – I don’t want an Elisa subscription with forced security features. Why would I pay twice when I’m already paying? I understand, of course, that there might be scam call blocking or other additional features, but from a market perspective, that sounds a bit like only heads of state or doomsday preppers are in the market for building such a digital bunker. For the average Joe, it sounds like overkill.

My own view is that the cybersecurity market is consolidating and multi-platform comprehensive solutions for consumers, like Total, are the future winners. Therefore, it is concerning that it doesn’t really seem to have a future in the company’s strategy – it’s mainly something used to generate cash flow for debt repayment and for building the Tier 1 partner market.

As an investor, I wonder whether F-Secure intends to sell directly to consumers via Tier 1 partners (the signed agreement mentioned in the interview), through partnerships where the operator automatically bundles the solution into its product (the upcoming agreement), or purely by improving the security level of Tier 1 partners, where the partner benefit comes, for example, from operator customers receiving less scams and spam, and the operator/manufacturer consequently having less mess and issues to resolve in customer service?

Good post, the doubts are well-founded and plausible. On a general level, one might wonder whether a separate security software suite is even needed or if it just comes with the device. On the other hand, I read yesterday about a cyberattack on Polish power plants. F-Secure’s price is quite moderate for me right now, considering it ensures heating, electricity, and the internet stay on, and a state-sponsored actor can’t mess with my devices. Looking at how things are going in America, we might not be far from a situation where I accidentally “like” the wrong Trump video and face the same kind of harassment. I ask, what security options do I have after that?

There is confrontation in the world, and it causes distrust. Finns are still considered trustworthy and a desired partner. In contrast, Chinese people may have distrust even toward their own government. A guy in China might want a European VPN simply to see what is happening in the world.

In my opinion, F-Secure has the potential to operate in larger markets than any other player. A trade agreement was just made with India. It won’t please the Russians or Trump. Indians may have a need to protect their own systems. They have gotten a foot in the door in the US. The European advantage was already mentioned there. Hyppönen is very, very well-known globally. I’m not saying F-Secure has a competitive advantage, but the potential customer base and growth opportunity are significantly larger than for many other security companies.

Looking at the competitors, I don’t think anyone wants Kaspersky anymore, for example. You hardly see Norton/Symantec anywhere anymore. McAfee is pushed on Windows machines, but I personally don’t know who would use it.

I had the McAfee security suite for 1+2 years while living in Vietnam because it came with the computer—first a free year (I think) + a 2-year offer—and I was quite satisfied with its performance. The best part about it is the file shredder, which lets you shred sensitive data, but I didn’t get it again after moving back to Finland. I also had F-Secure Total for a while, but there were some issues with it and I gave it up once the two-year license expired (I got it out of a sense of duty as a shareholder). Now I’m “going naked” (i.e., using Microsoft’s Windows Security) since I haven’t been an owner for a couple of years (sold out in autumn 2023).

Of course, one reason I got McAfee was the Stonesoft acquisition offer, and I paid my debt of honor with that two-year license.

This would also fit in another thread, but I think it will be of interest in this one at least.

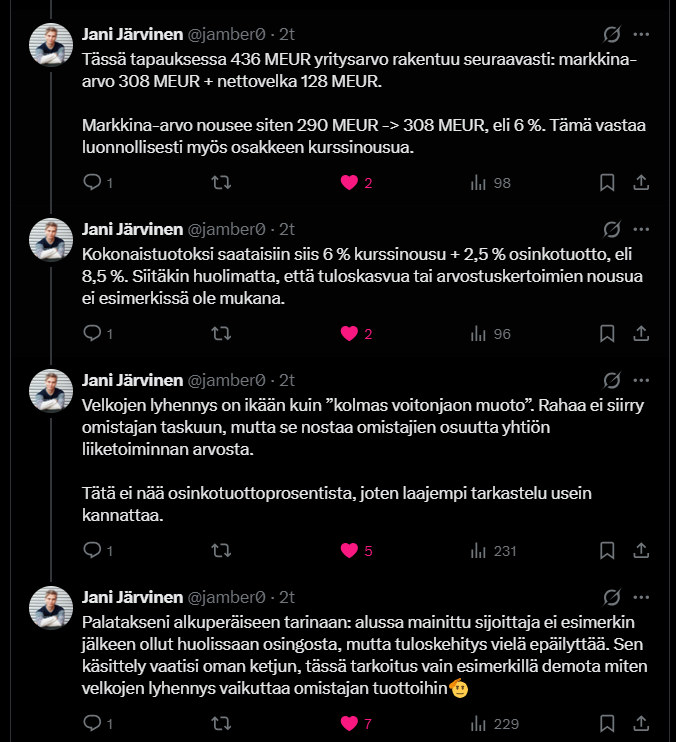

Debt repayment is like a “third form of profit distribution”. Money doesn’t move into the owner’s pocket, but it increases the owners’ share of the company’s enterprise value.

As a seasoned bottom fisher, I just had to buy into these rising prices following the news

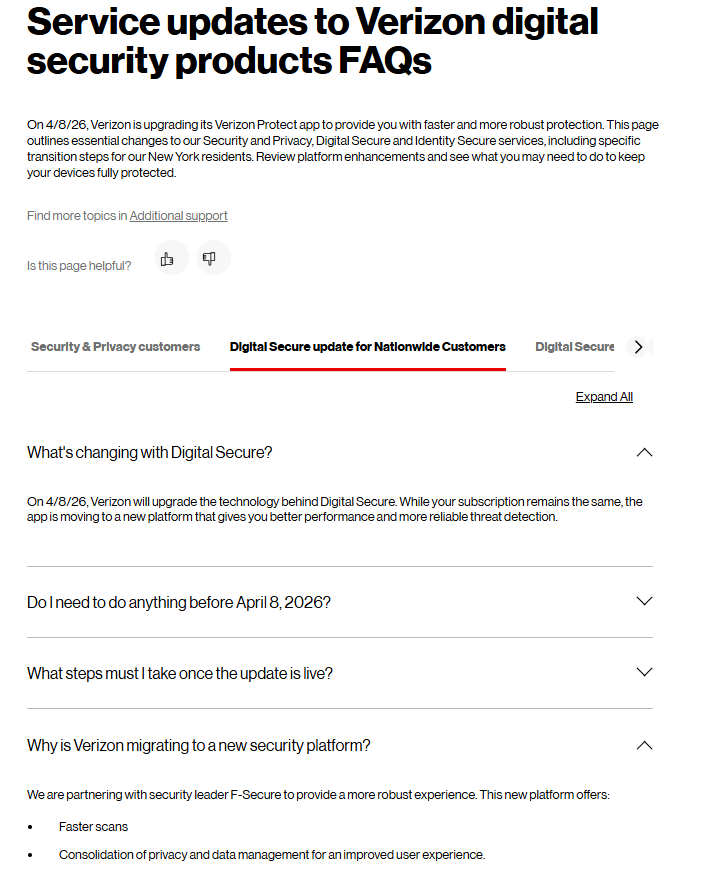

There is still a long way to go, as first all the signatures need to be on the papers, then the service has to be rolled out at a level approved by Verizon, and only then does the milking phase begin! But IF things don’t fall through in those earlier stages and the service runs as intended—meaning that running the service after initial approvals brings hardly any costs to F-Secure—then the +13 MEUR revenue will flow quite nicely down to the bottom line.

Sure, there are concerns about AI (AI taking everyone’s jobs, software firms’ margins collapsing, etc., etc.), geopolitics (oil prices up, uncertainty up → inflation, interest rates and, above all, weak consumer confidence and money not being spent on “anything”), etc., but all kinds of bad news was already priced into F-Secure’s stock. In that light, the +7% rise is somewhat modest:

I haven’t delved into how much exchange rates are affecting F-Secure’s figures, but looking at it in euros, Inderes forecasts revenue of 152.8 MEUR for this year.

Without any currency adjustments, the lower end of the new guidance is 155.9 MEUR. That is the lower end, and revenue only accrues for part of the year. From next year onwards, revenue will accrue for the full year and much more revenue will flow into the results.

Based on current forecasts, the stock is at 2027 P/E(adj)=9.3 and 2027 EV/EBIT(adj)=9.0, and by all logic, the forecasts must be raised. The pricing looks quite modest

We reiterate our Accumulate recommendation for F-Secure and revise our target price to EUR 2.0 (previously EUR 1.9). F-Secure announced on Tuesday a partnership with Verizon and, due to the large scale of the agreement, also raised its revenue outlook for this year. Earnings guidance was kept unchanged for now, but in light of our increased estimates, development is heading towards the upper end of the current range, and in a favorable scenario, earnings guidance could still be raised during the year. Yesterday’s news confirms that F-Secure’s Tier 1 strategy is gaining real momentum this year, which offers clear earnings growth potential for the coming years. In view of this, the stock’s current valuation (2026e P/E 10.5) is, in our opinion, very moderate.

Indeed, these were reported as acquisitions, but given the quantities, they might be compensations. Here are a couple of examples. The CEO also acquired a larger quantity.