Thanks for the report.

It seems that after the analyst change, Inderes’ view is pretty much unchanged

Someone more cynical might still suggest that both the old and the new analyst have an optimistic attitude towards the company. Exaggerating, they don’t first analyze the company neutrally and finally state whether it’s a good investment at the current price, but rather “the company has performed historically well and I like the company, so let’s look at things in a positive light.”

Is it really certain now that Etteplan’s operating model is somehow more advanced than Elomatic’s, Afry’s, Sweco’s, etc., etc.?

Utilizing AI is certainly an opportunity, but I somewhat doubt that every industrial company, design office, and IT company is also investing in this, so the relative competitive advantage quickly becomes ±0.

Is it certain now that the current profitability level is exceptionally weak and the highest profitability achieved during massive central bank stimulus is the “normal” to which we will return, and not the other way around?

You are right that there were no major U-turns in the analysis with the change of analyst. Of course, I looked at the company with fresh eyes and will continue to do so – expertise on the company naturally grows over time, as always in analysis. But I don’t think there were grounds for a completely different view, nor do I think it would be sensible just because the analyst changed and there’s a need to present a dramatically different angle. And I can assure you that valuation and investment cases are always approached with a clean slate (although it would be unrealistic to assume that an analyst would be immune to various verified investment-related cognitive biases).

Regarding that operating model, the tone in the report has, in my opinion, been changed relatively clearly. For example, the report states: “In our view, Etteplan has historically been a pioneer in managed services, but its lead has diminished as the model has become more common among competitors. For example, 75% of AFRY’s 2024 revenue came from ‘Project Business,’ where, similar to Etteplan’s managed services, payment is based on results (not billable hours) and billing can be ‘continuous’ in nature. Although the operating model has clear advantages over the traditional model, we do not believe it constitutes a sustainable competitive advantage.” In another section, it states: “Etteplan’s historical lead in the Managed Services model has also narrowed, and we no longer see the model as forming a competitive advantage today.” The operating model has indeed been discussed in the report, as before, because it is part of the business model discussion and one of the company’s financial objectives relates to this, but in my opinion, the tone has certainly been changed. And the part about the advanced operating model in the investment profile refers to the operating model versus traditional resource leasing. In any case, the tone is different.

Regarding AI, this is certainly the case, and it will be interesting to follow! In that regard, the report did not set out to declare Etteplan as any kind of future AI winner; instead, the report aimed to highlight both the opportunities and risks it brings.

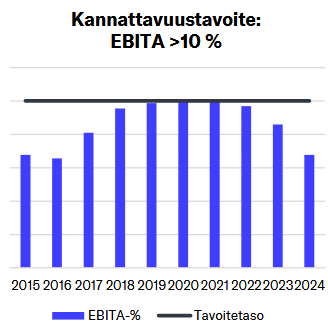

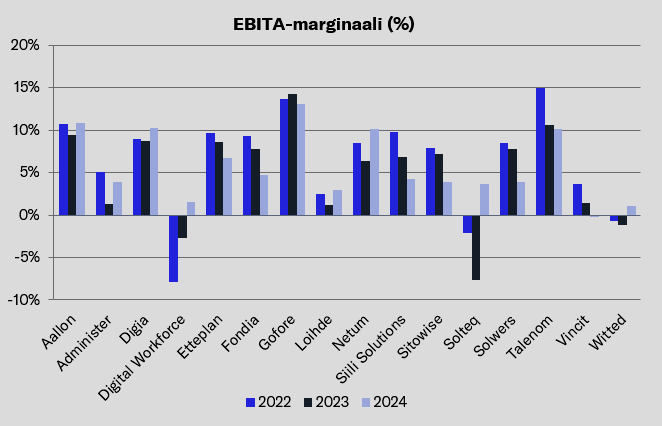

That profitability question is good and interesting. During the time when profitability was roughly at current levels, the company was significantly smaller, and its business relied more on traditional resource leasing. Additionally, the distribution of business by service area and geographically was different. Of course, a 10% EBITA-% was achieved during a reasonably good cycle, but it also included challenging times, such as the COVID-19 pandemic. And in my opinion, it is quite justified to argue that the last two years have also been exceptionally challenging years for the economies of Europe and Finland, and thus one could also argue that the past few years have not been “normal” either. Etteplan lives off its customers, so a turn for the better is partly dependent on how the economic environment and the business of the company’s customers pick up. The company’s guidance, which indicates improving profitability this year, even though there are no major reasons for celebration in the economy yet, partly communicates the profitability potential. And regarding that EBITA margin chart, it’s good to note that it reports EBITA-%, which was burdened by significant restructuring costs last year. Of course, there is also the possibility that the 10% margin levels were an exception – the risk factors indeed mention “Past years’ strong profitability proving to be an exception.” Of course, if an investor’s own view is that these were exceptions, the attractiveness of the investment case naturally suffers significantly.

I have never delved into Etteplan in super detail, and that profitability potential is, in my opinion, a very essential question for the company as an investment target, and one can then be optimistic or negative in the assessment. I personally like to take quite cautious views on forecasts. For example, in IT companies, the margins achieved during good times were the “new normal,” and then they had to improve from there. Now, for some time, everyone has been struggling. Apparently, Etteplan’s profile is slightly different, but as a point of comparison, Frans had commented on the profitability of expert companies:

Germany’s and the EU’s improving economy might pull demand upwards, but conversely, trade wars etc. can lock down investments and decrease Etteplan’s demand.

Profitability potential is a very essential question. However, I wouldn’t say that my forecasts are overly optimistic either – in a good scenario, I believe there could be potential for even better results. Of course, if the current economic downturn continues for longer, they might prove to be optimistic. Forecasts are always just one scenario, and it’s almost certain that the outcome will not be exactly as per my forecasts. After a couple of difficult years, I think it would also be quite bold to claim that the company is now permanently weaker and will no longer achieve previously proven profitability levels. Of course, for example, the effects of artificial intelligence on expert companies are still somewhat uncertain (and there will be company-specific differences), and thus it is not an impossible scenario that historical profitability levels will not recur. And as you said, trade wars also cause significant uncertainty at the moment, and generally, forecast risks are currently high. I significantly lowered the forecasts for the coming years in the report, and now they contain a bit more caution compared to before.

One more detail about the forecasts: In the forecasts, the company remains slightly below the 10% EBITA margin level for a few years during the forecast period at best, after which the level begins to weaken, and in the long-term forecasts, profitability remains at around 8%. Thus, if one looks at the DCF model and its indicated value, the long-term scenario is not overly optimistic in my opinion.

Here are Roni’s pre-earnings thoughts as the company publishes its Q1 results next Monday.

Etteplan will publish its Q1 results on Monday, May 5th, at approximately 1:00 PM. We expect the beginning of the year to have been difficult for the company and revenue to have slightly decreased despite the inorganic growth brought by acquisitions. At the same time, we also expect profitability to have been under pressure. Our attention in the report will be strongly focused on the outlook, which we estimate has inevitably been weakened to some extent by the trade war. The stimulus package planned by Germany is, in our estimation, a positive driver for the company, but its potential positive effects will only materialize in the medium term. Our comprehensive report on the company, recently published, can be read openly here.

Etteplan’s CEO Juha Näkki was interviewed by Roni right after the Q1 earnings release.

Topics:

00:00 Introduction

00:10 Q1 highlights

01:46 Weak result in the Technical Communication and Data service area

02:42 One-off costs weighed on the result

03:27 Uncertainty in customers’ investment decisions

04:42 Has the bottom been reached?

05:25 Guidance clarification

06:27 Germany’s stimulus package as a positive driver

07:37 Focus areas for the rest of the year

Roni has made a new company report on Etteplan after Q1.

Etteplan’s operational Q1 figures were slightly below our forecasts, and the reported earnings were further burdened by significant one-off items larger than we expected. The market outlook has further clouded due to the trade war, although the company does not expect any significant weakening from the current demand level. Guidance was revised downwards, and there is already an earnings warning risk associated with the guidance. With our forecasts anticipating this, we believe the valuation is moderate (2025e adj. EV/EBITA 11x) and supports staying invested in the stock despite high uncertainty.

Quoted from the report:

With Etteplan’s current multiples at a neutral level, we believe the stock’s expected return relies particularly on our forecasted earnings growth (with our forecasts, adj. EPS growth 2025-2028 around 15%). However, this requires a return to growth, which also enables a recovery in profitability. The dividend yield is at 2-4%, which provides some support for the expected return.

You don’t have to look very closely at the bullied person’s LinkedIn profile to see that the trail leads to Etteplan. It’s not very good publicity for Etteplan that such a bullying case exists within their company. What’s more, the bullying is recognized, but it’s implied that if the bullied person changes their own behavior, the bullying might perhaps stop.

According to the new estimate, revenue is expected to be 365-385 million euros and operating profit (EBIT) is expected to be 19-24 million euros. Previous estimates from the beginning of May were 365-395 M€ and 23-28 M€.

@Roni_Peuranheimo was really on the ball here. From the company report:

We expect

the company's revenue to grow by 3% this year to EUR 371 million and

operating profit to reach EUR 21.4 million, which would mean a decrease in guidance.

Frans and Atte have commented on Etteplan and its negative outlook.

Etteplan lowered its guidance and provided preliminary information on its Q2 results. Our 2025 earnings estimate was already at the level of the new lowered guidance, so it did not come as a big surprise in an uncertain environment colored by trade war. However, the Q2 result fell short of our forecasts in light of the preliminary information. Overall, the profit warning was not particularly dramatic, and the stock’s valuation is moderate even with this year’s earnings estimate (adj. EV/EBITA 11x). The stock’s moderate price reaction yesterday (-3.2%) also partly indicates this.

Here are Roni’s preliminary comments as Etteplan reports its results on Wednesday.

Etteplan issued a negative profit warning last week and preliminary information regarding its Q2 figures, so there should be no major surprises in them. In any case, the company has had a weak quarter. The difficult market environment has continued, and the trade war has further slowed down customer decision-making. The company’s own visibility also appears weak at the moment, but we aim to gain more clarity on these from the report.

Group revenue decreased by 1.3 percent to EUR 91.4 (4-6/2024: 92.6) million. At comparable exchange rates, revenue decreased by 1.9 percent.

Operating profit (EBITA) decreased by 12.1 percent to EUR 6.0 (6.8) million, or 6.6 (7.4) percent of revenue.

Operating profit (EBIT) decreased by 17.8 percent to EUR 4.4 (5.3) million, or 4.8 (5.8) percent of revenue.

The combined impact of non-recurring items on operating profit (EBITA) and operating profit (EBIT) was EUR -0.9 (-0.4) million in April-June.

Cash flow from operations weakened and was EUR 6.9 (9.0) million.

Undiluted earnings per share were EUR 0.10 (0.13).

At the end of June, the share of AI-based service solutions developed by Etteplan in revenue grew to 4 percent.

Etteplan issued a profit warning on July 28, 2025, and lowered its previous estimate for its 2025 revenue and operating profit (EBIT) due to market demand uncertainty and weaker-than-expected business development. According to the new estimate, revenue is expected to be EUR 365-385 (2024: 361.0) million and operating profit (EBIT) is expected to be EUR 19-24 (2024: 18.4) million. In connection with the profit warning, Etteplan provided preliminary information on its second-quarter revenue and operating profit (EBIT).

Key figures in January-June 2025

Group revenue decreased by 1.8 percent to EUR 186.3 (1-6/2024: 189.7) million. At comparable exchange rates, revenue decreased by 2.3 percent.

Operating profit (EBITA) decreased by 21.5 percent to EUR 11.8 (15.0) million, or 6.3 (7.9) percent of revenue.

Operating profit (EBIT) decreased by 29.0 percent to EUR 8.5 (12.0) million, or 4.6 (6.3) percent of revenue.

The combined impact of non-recurring items on operating profit (EBITA) and operating profit (EBIT) was EUR -2.3 (-0.7) million in January-June.

Cash flow from operations weakened and was EUR 12.0 (17.0) million.

Undiluted earnings per share were EUR 0.19 (0.29).

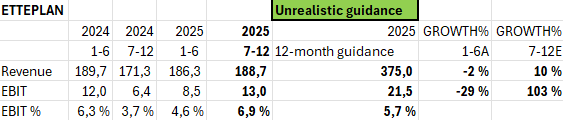

There’s work to do in the year-end. I wouldn’t be surprised by a new profit warning. In the latter half of the year, revenue should be 10% above last year’s latter half, while in the first half it was -2%. This might still be possible, but EBIT should be 103% above last year’s latter half. I’m using the midpoint of the full-year guidance.

00:00 Start

00:11 Negative profit warning

01:12 Projects have been postponed

02:25 Differences between sectors

03:07 No major investments in engineering workshops

04:04 Q2 figures

04:57 Restructuring

05:39 Development of service offering

06:42 Impact of AI solutions

Roni has published a new company report on Etteplan right after Q2.

Etteplan’s Q2 key figures held no major surprises given the preliminary information, although the weak result was explained especially by large restructuring costs, and operationally, profitability was moderate. The outlook is foggy and subdued. The new guidance requires an improving trend for the rest of the year, and a new profit warning is not ruled out if the market situation deteriorates further. From an investor’s perspective, it is positive that the valuation is reasonable even with a weak earnings level.

Here are Roni’s comments on Etteplan’s small acquisition in Sweden.

Etteplan announced that it is acquiring Swedish automation solutions provider Eltech Automation AB. The acquisition is small in size (less than 1% of revenue), but strengthens Etteplan’s service offering and geographical position in Sweden. The deal does not necessitate immediate forecast changes.

According to Evli, Etteplan has had a more difficult time now because customers have been more cautious and projects have been postponed “forward”.

However, a pick-up and an improvement in results are expected for the end of the year. The company has adjusted its costs and made acquisitions that can help, and in the long term, Evli still sees good potential in Etteplan.

EDIT: Etteplan will publish its results on 29.10. (@Juha_Kinnunen, thanks! :D, that sentence previously said Evli instead of Etteplan )