Board member on the buying side for 4000 pcs.

14 Likes

Let’s put here too what I wrote in the Aktia thread:

“I agree that Aktia is hardly involved in any merger speculation right now. The question arises regarding eQ’s main owners, as they now received €65m from Aktia sales, whether that money is intended for acquisitions, i.e., practically for merging eQ with another player? Knowing the Rettigs and Ehrnrooths, the money is hardly intended to just sit in a savings account.”

1 Like

As Sauli pointed out in a Kauppalehti interview (regarding Aktia), if there were some larger project underway, the management would not be allowed to trade. An eQ board member bought shares less than two weeks ago, so there probably isn’t any project on the table.

5 Likes

The fact that owners discuss off-the-record among themselves about a possible merger or sound it out does not yet trigger an insider project that would prevent a board member’s share purchases. I still consider it likely that the €65m now received by eQ’s main owners will be used for something. So, it’s intended, but there’s unlikely to be any ‘decided’ merger that’s far along. Remains to be seen ![]()

6 Likes

Won’t eQ’s and the owners’ money get mixed up here? Additionally, it is very possible that eQ’s potential acquisition is with an unlisted company, into which it is more difficult for eQ’s owners’ money to be invested before a merger. I agree that the Aktia speculation is dead.

5 Likes

Here are Sale’s concise comments on Janne Larma making a comeback as eQ’s Chairman of the Board. ![]()

6 Likes

Comments from eQ’s private equity days - excerpt from eQ’s LinkedIn channel:

Our European private equity platform, focusing on lower middle market opportunities in Northern Europe, continues to show resilience, strong performance and increasing exit activity in a complex macro environment. With a focus on established managers and disciplined investment strategies, we continue to be well-positioned to capture value also going forward.

So, PE returns should start flowing in soon. There are only a little over 3 months left until the beginning of 2026, and if one believes the market looks at least 6 months ahead, then the share price should also start to show positive movement soon if there is optimism regarding these. At least the company itself is very confident, and the impact on earnings could be surprisingly large for 2026 if the logjam breaks, because so many structures will move into the scope of performance fees at once.

3 Likes

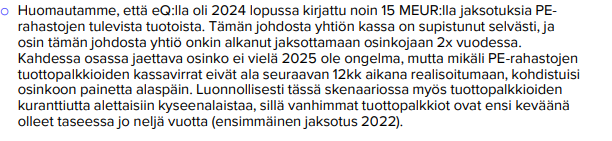

“eQ Group accrues the profit-sharing portion of performance fees from capital funds to the income statement, to the extent that it has been estimated that the amount of accrued recognized returns will not require significant reversal later. Accrual can be recognized from those eligible funds that are estimated to be cash-flow-wise within the scope of profit distribution within the next five years, whose investment period has ended, and for which eQ has received return estimates for the target funds’ final returns from the target funds’ management companies regarding their final return multiples.”

This means that carried interest could already have been recognized based on estimates. Individual exits do not have much impact on this. Performance would at least need to be better than estimated (

1 Like

I would like to remind that eQ has two angles in the realization of performance fees. 1) is the income statement, meaning that the amount of performance fees will grow significantly next year as several funds move to profit distribution. 2) is then what @Kermit mentioned, i.e., cash flow. The company has recognized significant performance fees through the income statement, but on the balance sheet, these are still receivables. The realization of these would naturally be very important. Attached are my comments from the previous report:

15 Likes

Yes. And Pölönen certainly has enough faith in the carries coming through, as he just placed a 12m€ bet with all his own and borrowed assets on the success of the matter (and of course, the company’s long-term success) ![]()

6 Likes

It was probably Finland’s highest quality

For eQ, positive news from the PE front for a change. IPOs in the EU finally seem to be waking up. Although eQ’s funds invest in slightly smaller companies that also have other exit channels than IPOs, this pick-up in the IPO market is important for general M&A activity, which should also be reflected in eQ’s funds. This supports our forecasts that next year eQ’s performance fees would start to grow significantly and previous performance fees booked upfront would materialize into cash flow.

https://www.cnbc.com/2025/09/22/europes-ipo-uptick-sparks-hopes-of-a-much-needed-rebound.html

20 Likes

eQ’s real estate fund returns visible ( eQ - Rahastot ), but monthly reviews are naturally not yet available. Social Real Estate is just under 1% in positive territory and Commercial Real Estate is marginally positive. In Social Real Estate, returns have been at zero/slightly positive since Q1’24, meaning the situation has clearly stabilized. Note that a large number of properties have been sold at the same time due to redemptions, so in my opinion, there is no significant concern that the sales will cause write-downs. In Commercial Real Estate, the situation is more difficult, and the slide has continued until Q2’25. Here, large property sales are also yet to be made, which naturally increases uncertainty.

Both returns are in line with our forecasts and give confidence that the worst is starting to be over regarding returns.

19 Likes

While writing eQ’s pre-commentary, their recent recruit Putkonen caught my eye:

One growth path seems to be selling products to international investors. This is not surprising, as many other peers have been doing this successfully for a longer time. The biggest difference between eQ’s and, for example, Mandatum’s, Evli’s, or Aktia’s international strategies is that eQ offers FoF (Fund of Funds) structures, whereas the previously mentioned houses started with “their own products” (yes, those PE funds are of course eQ’s products, but the underlying target funds are not). ![]()

11 Likes

Here are Sale’s comments as eQ reports its results next week on Tuesday. ![]()

The result is still on a downward trend due to challenges in real estate funds. The numbers are unlikely to offer major surprises this time either, and the greatest interest in the report focuses on the strategy update or related comments. Comments on the development of the real estate market are also of interest, as clear signs of recovery have been observed in the market.

7 Likes

Ja tässä Sale’s follow-up comments, or rather quick comments, on the Q3 results. ![]()

eQ published a slightly weaker Q3 report this morning than we expected. However, the miss in numbers was entirely due to the investment bank’s even weaker-than-expected quarter and the impact of the weakening dollar on PE fund fees, and thus the significance of the miss is very limited. The most important single item in the report was the information that the new strategy will be published in February in connection with the Q4 results, whereas we had previously expected the announcement already during the current year. Preliminarily, we estimate that the report will not lead to major forecast changes.

10 Likes

Asset management company Eq’s CEO Jouko Pölönen says that a corporate arrangement between Aktia bank and Eq, which has long been speculated in the financial world, makes no sense from the perspective of Eq’s owners.

“Asset management is a very capital-light business. Banking is very heavily regulated and has heavy capital requirements. In that sense, I don’t see the merger making sense for Eq’s shareholders.”

In an interview on Talousaamu, however, Pölönen did not rule out corporate arrangements.

“In Finland, there are quite a few small players in the financial sector, whether it’s the banking or asset management sector or the private equity sector. We want to look at all potentials for growth,” Pölönen says.

Primarily, however, Eq seeks growth organically.

8 Likes

Sale interviewed eQ’s new CEO Jouko Pölönen. ![]()

Topics:

00:00 Introduction

00:03 Q3 updates

02:00 Real estate

03:59 Private equity

07:02 Strategy work

09:03 Recruitments

10:53 Clients

13:38 Traditional asset management

8 Likes

Sale has published a new company report on eQ right after Q3 ![]()

eQ’s Q3 report was largely in line with our expectations, and the numbers remained on a downward trend as the company suffered particularly from challenges in the real estate market. Our earnings forecasts have remained unchanged, and we expect the company to return to strong earnings growth next year, driven by performance fees from private equity funds. We believe the stock is currently fairly priced, and due to the uncertainty related to earnings growth, we do not see the risk/reward ratio as sufficiently attractive. Therefore, we reiterate our reduce recommendation with a target price of 11 euros and await the publication of the new strategy in February.

Quoted from the report:

M&A still possible

The implementation of the strategy could be significantly accelerated by corporate acquisitions, and in our opinion, M&A will once again be much more strongly on the table than before. Although the share price has fallen sharply, the stock is still reasonable merchandise in terms of valuation, and we see it offering a good platform for creating shareholder value through corporate acquisitions.

3 Likes

eQ: a very good (and brave!) decision to start reporting real estate funds significantly more openly than before ![]() In practice, for the first time in history, an external party can make a reasonable analysis of the underlying assets. The report contains so much information that even @ValkoinenPeura is likely to be satisfied.

In practice, for the first time in history, an external party can make a reasonable analysis of the underlying assets. The report contains so much information that even @ValkoinenPeura is likely to be satisfied.

The decision has a big impact on the industry. In my opinion, it is obvious that all other open-ended real estate fund managers are now under immense pressure to increase their own transparency. Not everyone will certainly have the desire or even the ability (it requires a lot of work and data to print that report 4x/year) to do this, but pressure may force them to.

For eQ, the direct and immediate business impacts will likely remain small at first. However, this will certainly improve investor confidence in the funds, and in the longer term, it will certainly facilitate the sale of funds when the market eventually turns.

Why is eQ making this change then? The company certainly sees the indirect benefits I mentioned (customer trust, etc.), but another reason is also the fear of regulation mentioned in the press release. I myself have spoken with countless industry representatives during the autumn, and a common concern for almost everyone is that the regulator would make major changes to industry regulation to avoid a similar crisis in the future. For example, large liquidity buffers would weaken the attractiveness of these products as investment targets.

Our comment can be found here ![]()

42 Likes