Vaikea uskoa että Mandatum olisi myynyt osakkeensa ilman että olisi saanut takuita siitä ettei ostotarjous ole kulman takana. Siis joku aikamääre, 6kk? 12kk?, minä aikana Otava tai Alma sitoutuu olemaan tarjoamatta korkeampaa hintaa osakkeista.

Ja vielä lisäys, itse olen kyllä Enentossa mukana ja uskon ettei Otava olisi moisia määriä osakkeita haalinut ellei joku järjestely olisi suunnitelmissa. En vaan jaksa uskoa sen kovin pikaiseen toteutumiseen.

Pahoittelut, kun vastaus tähän viivästyi. Ei tuota Goavaa sinänsä säännöllisesti ole yhtiön kanssa käyty läpi, sillä olihan se Enenton mittakaavassa pieni sijoitus. Mutta selvää on, että eihän tarina ole mennyt putkeen kun lukuja katsoo ja Enentokin kommentoinut, että sijoitus ei ole täyttänyt heidän odotuksia ja että se ei ole yhtiöön lisäsijoituksia suunnitellut. Siten en sijoittajana ainakaan nykytiedon valossa älyttömän paljon painoarvoa sille Enenton sijoitustarinassa antaisi (kunhan Enento ei lähde isommin pääomittamaan yhtiötä tappioiden jatkuessa). Siksi en myöskään sitä analyysissä mitenkään erityisen syvällisesti ole käsitellyt. Toki talousympäristön piristyessä aina on mahdollisuus myös positiivisiin yllätyksiin sijoituksen osalta, mutta tämä on lähtökohtaisesti kuitenkin mielestäni varsin pieni optio.

Ei kai siinä mitään ongelmaa ole sisäpiirisääntelyn suhteen, jos luvataan että ostetaan teidän osakkeet eikä tehdä ostotarjousta vuoden sisään.

Se olisi eri asia jos Otavalla olisi tietoa, että joku toinen taho olisi tekemässä ostotarjousta. Lisäksi luulen, että kauppojen teko olisi sinänsä mahdollista finanssivalvontaa konsultoiden, mikäli sisäpiiritietoa olisi molemmilla osapuolilla, mutta tähän on vaikea nähdä tilannetta jossa se olisi molempien osapuolien intresseissä.

Ehkä näin. Varovainen ainakin pitää suurimpana omistajana olla. Sinänsähän tiedotusvelvollisuus on (vain) yhtiöllä, ja omistajien välisestä transaktiosta yhtiöllä kai velvollisuus tiedottaa vain liputuksista. En tiedä pitäisikö jostain sitovista sopimuksista stten liputtaa - jos olisi sitoutunut ostamaan niin kai ainakin pitäisi.

Mutta niin tai näin, en ymmärrä miksi Otava johonkin rajoitukseen suostuisi? Siis ilmaiseksi? Miksi he vapaaehtoisesti sitoisivat omat kätensä? Eli Jos Manta olisi tuollaisen lupauksen edellyttänyt/saanut, niin varmaan hinta silloin olisi huonompi kuin se olisi voinut olla - ei kuulosta Mandatumilta. Eiköhän siinä ole paras mahdollinen hinta haettu.

Eli en tiedä onko Otavalla tai kenelläkään muullakaan kiinnostusta ostaa Enento kokonaan, mutta itse en ainkaan pysty uskomaan, että Mandatum-kaupan yhteyessä oltaisiin sitouduttu olemaan ostamatta.

Todellakin rikkoo AML 12§ ja räikeästi. Mikäli luvataan olla toteuttamatta jotain merkityksellistä kauppaa tulee siitä yhtiön selkeästi antaa tiedote, eikä sopi kahden kesken. Toki Mandatumin kauppa oli valtavan kokoinen ja se, että ei seuraavalla viikolla tarjousta tehdä on enemmän herrasmies sääntö, eikä laki.

Alma Median osake on nyt ATH-lukemissa eli 14,8 e. Enenton mörniessä luulisi, että esim. osakevaihdolla tehty transaktio alkaisi olemaan Alman kannalta optimaalista, jos Enento haluttaisiin integroida osaksi Almaa. Sitä ennen ylimääräinen osinko tullee maksuun lokakuun lopussa, kuten viimekin vuonna.

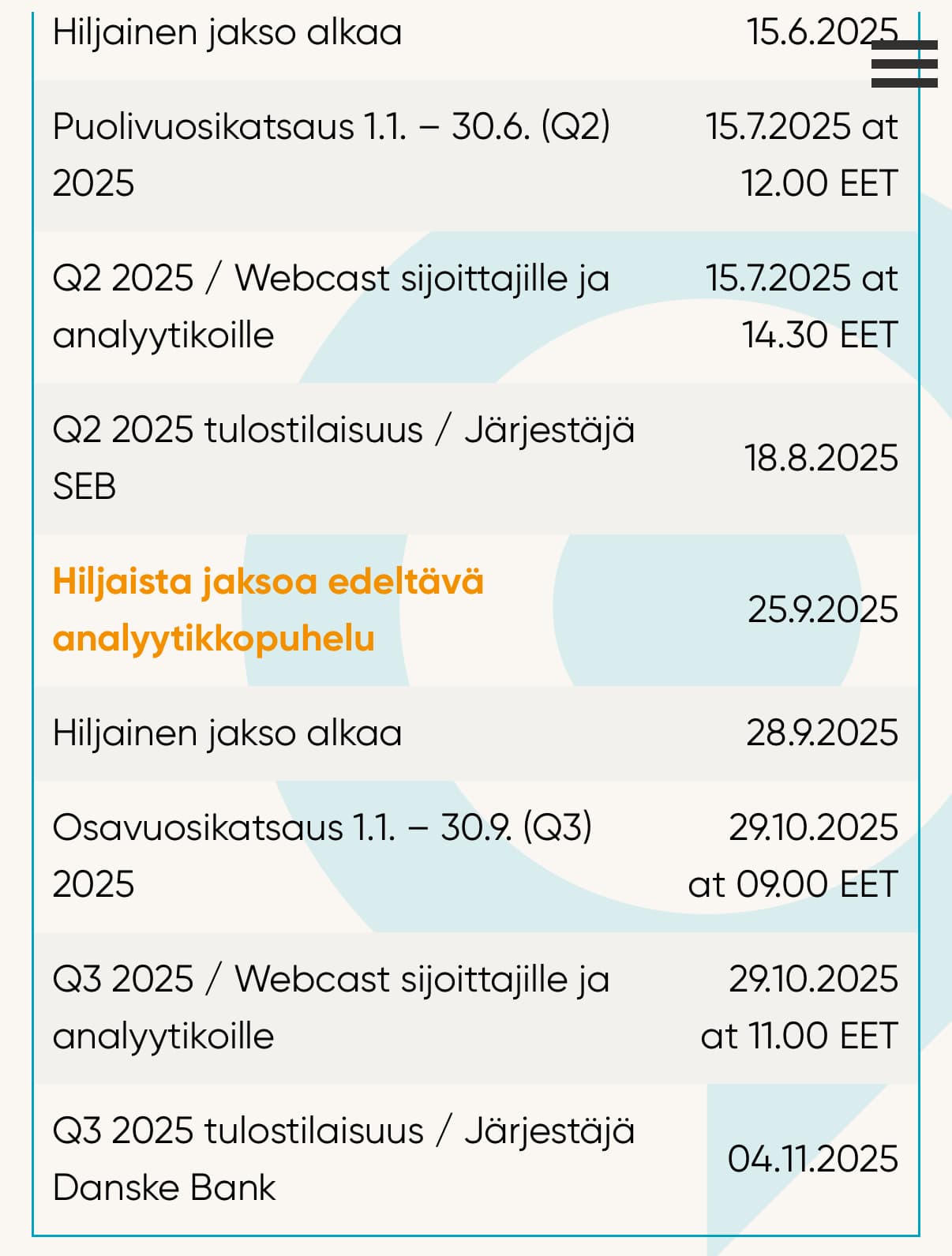

@Henrik.Soras.Enento Mistä näistä voi saada luotettavaa tietoa etukäteen milloin järjestetään? Nettisivujen kalenterissa tämäkin oli merkitty ensi viikolla pidettäväksi.

Sijoittajakalenterista. Meille on valitettavasti jäänyt sijoittajakalenteriin vanha päivämäärä (25.9), koska jouiduimme siirtämään puhelua nopealla aikataululla uuteen ajankohtaan (16.9). Eli pahoittelut siitä, että kalenteria ei oltu päivitetty - näin ei tietysti saisi käydä. Päivitämme sen asap.

Olipas JÄLLEEN kerran surullista kuultavaa analyytikkopuhelu. Todella harmi, että tarina ei kehity lainkaan eikä selvästikään ole sen kummempia suunnitelmia kuin puolustella marginaaleja ja ihmetellä maailman menoa.

Mikäli nyt ei olisi erikoistilanne käynnissä, myisin varmastikin puolet omistuksestani jo pois. 6% vuosikorko osinkojen muodossa ei itselleni riitä riskiin nähden, mutta koska tilanne on nyt voimakkaasti päällä ja huhtikuun lopusta asti ollaan uutta toimitusjohtajan nimitystä odotettu voisin kuvitella yrityskaupan tässä syksyn mittaan jo tapahtuvan, eli kyllä vuoden loppuun asti katselen tätä puolustusvoittojen ilotulitusta mikä Enenton agendana on.

Monta kertaa olen ihmetellyt aiemminkin tällä foorumilla, että on merkillistä ettei yhtiöllä ole kolmeen vuoteen ollut mitään järkevää suuntaa ja ollaan oltu kuin “kasvun rajat olisi tulleet vastaan”. Pohjoismaissakin on paljon voitettavaa, mutta sen ulkopuolella Euroopassa aivan hirmuisesti. Helppoahan se ei ole, mutta osaaminen, teknologia on kuitenkin melko harvinaista mitä Enentolla on joten on outoa ettei yhtään ponnistavaa yhtiötä ole Eurooppaan avattu. Taloudelliset resurssit siihen varsinkin antaisi sijaa, mutta ambitio on syöstä osinkoja niin paljon kuin mahdollista ulos ja ottaa velkaakin, jotta osinkovauhti ei vaan pääsisi hiipumaan.

Toivon, että loppuvuodesta saadaan upouusi loistava toimitusjohtaja, jolla vankka osaaminen ja kyky vetää kasvua tai toinen mahdollisuus on tietysti, että Enento viedään ulos pörssistä mikä myös alkaa tuntua yhä houkuttelevammalta vaihtoehdolta kuin tämän mörnimisen jännääminen.

Tässä on Ronin kommentit tiistaisesta hiljaista jaksoa edeltävästä analyytikkopuhelusta.

Enento järjesti tiistaina hiljaista jaksoa edeltävän analyytikkopuhelun. Tallenne tilaisuudesta on katsottavissa täältä. Puhelu ei tarjonnut nähdäksemme olennaisesti uutta informaatiota. Talousympäristö yhtiön toimintamaissa Suomessa ja Ruotsissa on säilynyt vaisuna, mikä on pitänyt yhtiön kasvu- ja kannattavuusnäkymät paineessa.

Tässä: Artikkeli (Asiakastieto), jossa esitellään uutta lakimuutosta, joka pakottaisi yritykset tarkastamaan asiakkaidensa tiedot positiivisesta luottotietorekisteristä. Mikäli tämä tulee voimaan, millainen vaikutus @Roni_Peuranheimo tällä voisi pahimmassa skenaariossa olla?

Pahimmassa skenaariossa toki voisi olla ikävä vaikutus, sillä onhan tuossa jälleen jonkin asteinen riski yhtiön palveluiden kannibalisaatiolle. Mutta en nyt vielä tässä vaiheessa lähtisi ennakoimaan pahinta skenaariota. Kuluttajien positiivisen luottotietorekisterin osalta yhtiöhän on onnistunut hyvin tarjooman kehittämisessä niin, että suurempaa kannibalisaatiota ei tapahtunut. Mutta toki tuon artikkelin sävykin jo paljastaa, ettei tuo yritysten julkinen luottotietorekisteri olisi yhtiölle toiveiden mukainen skenaario. Pitää tästä kysellä jatkossa hieman tarkemmin niin saadaan mahdollisista vaikutuksista vielä parempi käsitys.

Ei omistaja rekisterissä yllätyksiä. Reilu 21 600 lappua nousi 100 suurimman omistajan yhteismäärä, eli piensijoittajat ovat olleet hieman enemmän myyntilaidalla. Toki rahamääräisesti lukema käytännössä mitätön. Nyt sitten odotellaan Q3 raporttia!

Tutustuin hieman syvemmin Ruotsalaiseen kilpailijaan Roaring Group AB:hen. Yritys on kasvanut erinomaisesti keskimäärin 80% vuodessa. Siten, että liikevaihto reilu 4,6 milj. SEK 2020 ja nyt päättyneellä tilikaudella reilu 50 milj. SEK.

Yrityksellä on myynnissä paljon samanlaista dataa kuin Enentolla KYC & AML kategorioista omistajarekisteridataan ja paljon muuhun.

Roaring on laajentunut vauhdilla kaikkiin pohjoismaihin (pois.lukien Islanti) ja nyt myös Espanjaan. Tämä todistaa juurikin sen, että opittua teknologiaa on hyvinkin mahdollista kehittää eteenpäin ja skaalata ulkomaille. Espanjassa pienempi valikoima kuin muissa maissa, mutta sielläkin 8 tuotealuetta. Kysymys kuuluukin, kun pienet kilpailijatkin omaavat kyvykkyydet rakentaa operaatioita ulkoimaille miksi Enento pyörittelee päätä vain Pohjoismaissa? Suomi ei kasva yhtään, markkinaosuus jo valtava. Ruotsissalainsäädäntö lyönyt näpeille ja siitä toivutaan hitaasti. Norja ja Tanska kasvavat kohtuullisen hyvin mistä olenkin iloinen, mutta konsernitasolla kasvun merkitys kovin vähäinen. Siksi uusille kohdemarkkinoille siirtyminen olisikin luonnollinen ratkaisu.

Myös @Roni_Peuranheimo mitä mieltä olet siitä, että uudesta toimitusjohtajasta ei ole ollut mitään puhetta? Huhtikuussa ilmoitettiin Jägerin lähdöstä ja nyt Lokakuussa painetaan yhä ilman toimaria. Eikö tämä ole erittäin outo tilanne, jos mitään transaktioita ei olisi käynnissä? Ei kai tähän mökkiin pätevän kaverin löytyminen voi näin vaikeaa olla?

Tuo on vaikea kysymys sen osalta, että näkyvyyttä siihen mitä hallituksen sisällä pohditaan ei luonnollisesti ole. En kuitenkaan ajattelisi, että toimitusjohtajan etsimisen kesto indikoisi automaattisesti, että piipussa olisi jokin transaktio. Transaktioiden toteutuminen on aina epävarmaa aina diilin loppusuoralle asti ja olisi mielestäni erikoista, että toimitusjohtajan etsintä jäädytettäisiin tämän takia. Sitten kun jos diiliä ei saataisi aikaan niin lähdettäisiin uudelleen nollasta, mutta paljon myöhemmin. Myös aiemman toimitusjohtajan lähteminen juuri ennen jotain mahdollista diiliä olisi mielestäni jossain määrin erikoista.

Ei tuo alle puoli vuotta vielä mikään poikkeuksellisen pitkä aika ole. Odottelua se toki aiheuttaa, mutta tämän voi osaltaan viestiä myös positiivisena sen osalta, että hallitus tekee tarkkaa työtä eikä nappaa työhön ensimmäistä vastaantulijaa. Toisaalta myös hätää ei mielestäni odotellessa ole, sillä väliaikainen toimitusjohtaja Elina Stråhlman tuntee yhtiön hyvin ja on myös aiemminkin toiminut yhtiön väliaikaisena toimitusjohtajana.

Tässä on Ronin ennakkokommentit, kun Enento julkaisee ensi viikon keskiviikkona.

Odotamme liikevaihdossa matalaa valuuttavetoista kasvua ja operatiivisen tuloksen olleen suunnilleen vaisun vertailukauden tasolla. Toimintaympäristö on säilynyt varsin vaimeana, emmekä odota näkymissä suurempia muutoksia. Kommenttimme yhtiön hiljaista jaksoa edeltävästä analyytikkopuhelusta voi lukea täältä. Kiinnostuksen kohteena raportissa ovat muun muassa Ruotsin markkinan kehitys ja SME-liiketoiminnan transformaation vaikutukset sekä uusien kasvualueiden kehitys.

Oikaistu liikevoitto oli 30,4 milj. euroa (31,2 milj. euroa), laskua 2,7 % (vertailukelpoisin valuuttakurssein laskua 3,6 %).

Liikevoitto oli 18,3 milj. euroa (20,2 milj. euroa).

Hallitus on päättänyt 28.10.2025 toisen osinkoerän 0,50 euroa osakkeelta maksusta varsinaisen yhtiökokouksen 2025 antaman valtuutuksen nojalla. Osingonmaksun täsmäytyspäivä on 6.11.2025 ja maksupäivä 27.11.2025. Ensimmäinen osinkoerä 0,50 euroa osakkeelta maksettiin 8.4.2025.