The CEO’s first paragraph gives the impression that things didn’t go completely south.

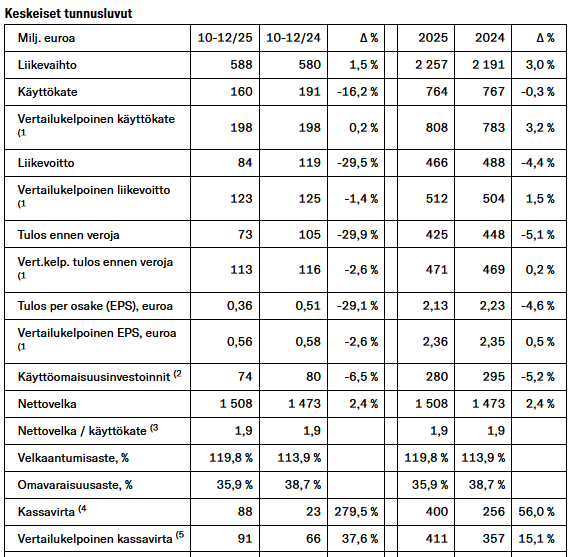

“In the fourth quarter, revenue grew by 1.5 per cent to EUR 588 million. Growth was mainly driven by revenue from international software services and mobile services, as well as equipment sales. EBITDA was at the previous year’s level: EUR 198 million. Comparable cash flow grew by 38 per cent. Strong growth was bolstered by a positive change in net working capital and management of capital expenditure. Full-year 2025 revenue grew by 3 per cent to EUR 2.3 billion. Both comparable EBITDA and operating profit were at all-time highs: EUR 808 (783) million and EUR 512 (504) million. Full-year comparable cash flow was the largest ever: EUR 411 million. Growth from the previous year was 15 per cent.”

Key figures for the fourth quarter of 2025

Revenue increased by EUR 9 million to EUR 588 million, mainly due to growth in mobile services and international software services.

Mobile service revenue grew by 2.4 per cent to EUR 261 million.

Comparable EBITDA was at the previous year’s level: EUR 198 million.

Comparable operating profit decreased by EUR 2 million to EUR 123 million.

Comparable cash flow increased by EUR 25 million to EUR 91 million.

In Finland, mobile postpaid ARPU was EUR 24.3 (24.3 in the previous quarter) and mobile postpaid churn rose to 23.0 per cent (22.3).

The number of mobile postpaid subscriptions decreased by 2,200 subscriptions during the quarter. The number of M2M and IoT subscriptions grew by 18,800 subscriptions.

In Finland, the consumer voice subscription base remained stable.

The number of prepaid subscriptions decreased by 9,100 during the quarter.

The number of fixed broadband subscriptions increased by 6,000 during the quarter.

The Board of Directors proposes to the Annual General Meeting that the profit for the 2025 financial year be added to retained earnings and that a dividend of a maximum of EUR 2.40 per share be paid based on the balance sheet approved by the AGM on 31 December 2025. According to the proposal, the dividend will be paid in four installments as follows:

The first dividend installment of EUR 0.60 per share is proposed to be paid to shareholders who are registered in the company’s shareholder register maintained by Euroclear Finland Oy on the record date for the first dividend payment, 7 April 2026. The Board proposes that the first dividend installment be paid on 15 April 2026.

In addition, the Board proposes that the Annual General Meeting authorizes the Board to decide later at its discretion on the distribution of a dividend of up to EUR 1.80 per share in total. The authorization would be valid until the start of the next Annual General Meeting.

Unless the Board decides otherwise for a justified reason, the authorization will be used to distribute dividends in three equal installments during the period of validity of the authorization. The Board will make separate decisions on each dividend distribution so that the preliminary record and payment dates for each dividend distribution are as set out below. The company will announce each such decision separately.

Preliminary record dates Preliminary payment dates Preliminary amounts

20.7.2026 29.7.2026 0.60 euro/share

26.10.2026 4.11.2026 0.60 euro/share

10.2.2027 17.2.2027 0.60 euro/share

The Board also decided to propose to the Annual General Meeting that the Board be given authorization to acquire a maximum of five million of its own shares, which represents 3 per cent of the total number of shares.

It’s not really a cut, an annual dividend of €2.40. The payment schedule is stretching a bit; these are tough times, after all. Maybe I’ll nibble a bit more around €34. We’ll see.

Elisa is switching to quarterly dividends, but in practice, one quarter’s (Q1/2026) dividend will be skipped. 167m * 0.60 = 100 million less in dividends will be paid until things return to “normal”.

Pretty good result and a small dividend hike. Quarterly dividends are also a good thing, and they indeed hold onto that last installment for a bit longer. For example, Kesko already pays it at the beginning of January.

I see Elisa having quite good opportunities for proper growth. Now, once the data centers start filling up with data being repatriated from the US, things will be good.

Quite a sharp share price reaction… a one-off 350-person layoff / 20m worsened the '25 figures, the '26 guidance is quite bold in my opinion – if it holds, I’d expect it to edge upwards quarter by quarter from the '26 reports… at this price, a 7% dividend… adding more…

What do you think about the plan to potentially buy back shares? Is it meant to compensate for the missing dividend installment this year as they transition to quarterly payments?

This has worked quite well in Nordea’s case, for example. The stock is cheap, and at the same time, it doesn’t look as bad as paying out large dividends during difficult times. So, it’s an excellent way to use the cash for the benefit of shareholders.

A certain number of shares are needed every year to pay for share-based rewards… now at prices from roughly 10 years ago, back then the dividend was 1.4, now it’s 2.4.

Authorization for share buybacks is obtained every year. The authorization is now exactly the same size as it was a year ago. Obtaining the authorization doesn’t signal that massive share buybacks are about to start, or that there are even any plans regarding the matter.

Competition is truly cutthroat. I’d say there’s some degree of a race to the bottom going on in the mobile sector. Through my work, I’ve seen the prices at which Telia will be selling subscriptions to the public sector in the future, and I have no idea how anyone can make any margin at those prices.

Is Veli-Matti Mattila’s departure starting to show? Mattila built a significant lead over Telia during his tenure, and now perhaps we are returning to parity. Well, okay, Telia also bungled quite a few things by overextending into side projects, but still.

Could Starlink still threaten operators in the long run? It’s a bit of a far-fetched idea if it does, but Elisa’s biggest asset and moat is the backbone network buried in domestic soil. If this turns out not to be such a big deal in the future, then heaven help Elisa investors.

Cybersecurity is a good spearhead, but I doubt it can become something companies would pay for in the same proportion as network connections. In my opinion, this is partly because cybersecurity providers are happy to sell technology and services, but the responsibility always ultimately remains with the customer.

Well, I only have this as a small position in one portfolio, so I’m just watching it calmly, but I wouldn’t be adding more as I think there are too many grey clouds.

Elisa’s Q4 report released this morning was largely in line with our expectations. Revenue grew slightly and the comparable result met our expectations, but there were more cost adjustments than we had previously estimated. Competition intensified as expected in Q4, but it seems that Elisa has performed relatively better than its closest competitor in the Finnish market. In the big picture, the guidance was in line with our expectations, as was the dividend amount proposed by the Board.

There is also a small detail regarding quarterly dividends: it is easier to decide not to pay a single installment, as happened with Tokmanni when results weaken.

In theory, a 7% dividend sounds great on paper, but there are no guarantees of its payment if the result weakens.

That -29.5% drop in operating profit is absolutely staggering for a company like Elisa, and in the beginning of the year, EBITDA will take another hit as people switch to cheaper subscriptions or competitors. If and when the next quarterly report is just as bad, it might be that Manner will not continue in his role for very long.

Of course, it’s worth remembering that there were large one-off items this quarter. Comparable operating profit fell by 2 million to 113 million, which is less than 2%.

On the other hand, one might ask whether this was it for the one-off items and restructuring. I’m afraid not, if competition intensifies further. The screws will have to be tightened even more, which means new restructuring measures. This way, one-off items start to accumulate much like Tieto’s, where they become more the rule than the exception.

This Q4 encapsulates why Elisa is one of my largest direct investments (approx. 3% of my portfolio): even in a difficult market, they are able to deliver results in line with well-founded expectations. Nothing more this time, but nothing less either. I would guess that the market (currently around -4%) will recover fairly soon.

The slight drop in consumer postpaid subscription numbers was surprising. Elisa has managed to hold its ground in the price war or has compensated for voice subscription churn by selling affordable data SIM cards, e.g., 100Mb subscriptions. In the autumn, the market saw promotions such as “SIM card for a laptop for a couple of euros a month.” A good defense, but I’m perhaps a bit wary about what the actual situation was.

Mobile ARPU development was in line with expectations. ARPU growth stopped and remained at the level of the previous quarter, as I previously anticipated. It is worth noting what I’ve mentioned before: low prices for new sales will be reflected in revenue and thus in ARPU with a lag. Example: Elisa customer Pekka takes a subscription from DNA in early December—billing for this only starts at the end of December and affects revenue only from then onwards.

Additionally, Elisa charges relatively high one-time fees for new subscriptions. This provides a buffer for months with slightly higher churn at the end of the year, but since it only helps on a one-time basis, the ARPU boost it provides will no longer help in Q1.

In Q1, Elisa’s most profitable business segment (mobile, consumer mobile subscriptions) will therefore see a drop in revenue. What happens after that depends on price development—which, in fact, is showing very slight signs of recovery…

Previously, you could earn S-bonuses from Elisa contracts. Nowadays, this is no longer the case; instead, the S Group’s bonus partner is the operator Moi, which uses DNA’s network. Quite a few people have switched operators for this reason.

It’s great to have another Helsinki Stock Exchange company join the ranks of quarterly dividend payers, but exceptionally, this left me with a bit of a mixed feeling.

If the change had been made during good times, it would be a purely positive thing. Now I have a sneaking suspicion that the move to quarterly payments was just a way to cut the dividend without actually cutting it.

Furthermore, the tightening competition is unlikely to be just a matter of a few months; it could last much longer. Even though Elisa is certainly of higher quality compared to other players, it’s not much of a consolation if the entire industry is being flushed down the toilet. (Perhaps a bit of a dramatic way to put it)