Here are Petri’s comments on the staffing services industry’s July.

According to the staffing sector’s revenue survey, the revenue of the 20 largest companies in the sector was approximately EUR 116 million in July, which corresponds to a decrease of just under 10% from the previous year. The overall market development is essentially linked to temporary staffing services, which accounted for approximately 84% of the largest players’ revenue in July. Consequently, the revenue from temporary staffing services was EUR 100 million, which corresponds to a decrease of nearly 9% from the comparison period.

Here are Petri’s comments on the staffing industry for August.

According to the staffing industry’s revenue survey, the revenue of the industry’s 20 largest companies in August was approximately EUR 121 million, which represents a solid 9% decrease year-on-year. The overall market development is essentially linked to temporary staffing services, which accounted for approximately 83% of the largest players’ revenue in August. Thus, the revenue from temporary staffing services was EUR 100 million, which also represents a 9% decrease from the comparison period.

Petri has prepared a pre-report as Eezy publishes its Q3 report on Thursday.

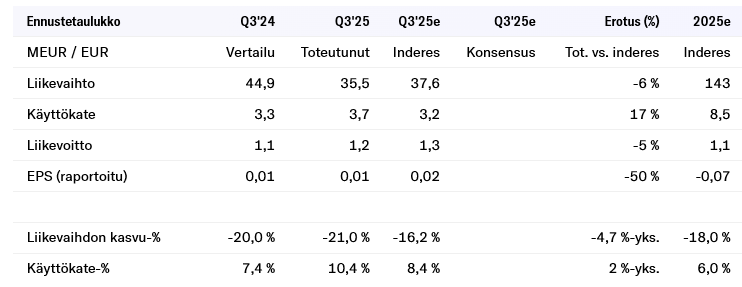

Eezy will publish its Q3 report next Thursday around 9:00 AM. We have made cuts to our forecasts for the coming years, as market development based on statistics has fallen short of our expectations, and expectations for a market turnaround also seem to be shifting further into the future, in line with economic and employment development. The stock’s valuation for the coming years is high, which, together with the current debt situation, creates a weak return-risk ratio. Thus, we reiterate our Reduce recommendation and lower our target price to EUR 0.80 (previously EUR 0.82).

Covenant terms were met in 3Q2025 and are estimated to be met in 4Q2025. However, the quarterly covenant terms for 2026 (net gearing, ratio of interest-bearing net debt to adjusted EBITDA, and minimum cash reserves) are “challenging”. This means they are presumably tightening in 2026, and there are no clear signs that the business turnaround from a downward spiral would be straightening out. However, the extent of the tightening is also unknown.

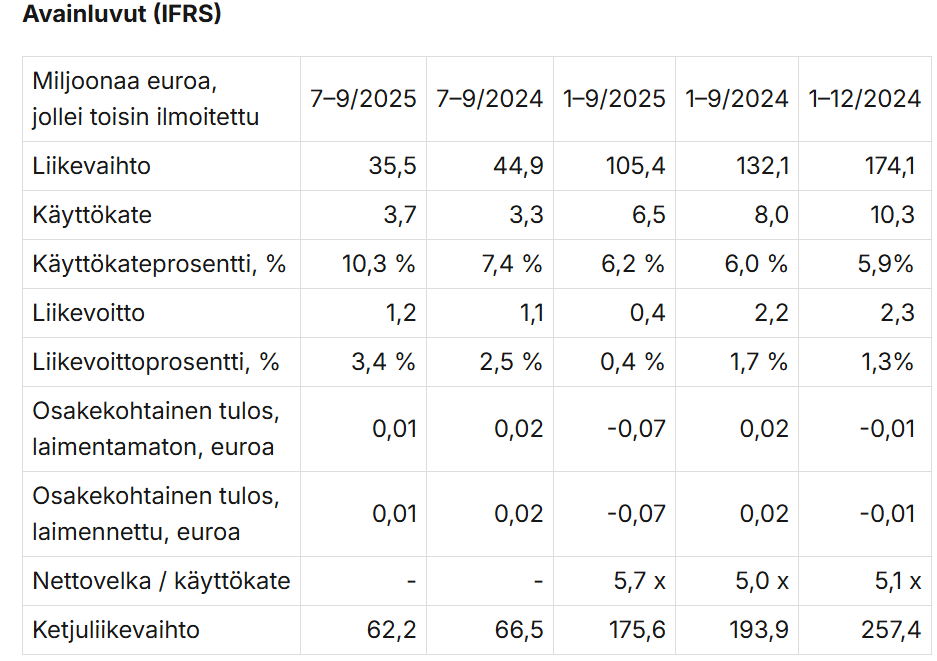

July–September 2025

Chain revenue\*, which also includes the revenue of franchise entrepreneurs, was EUR 62.2 million (EUR 66.5 million in July–September 2024). Chain revenue decreased by 6%. (\*more detailed calculation formula in the interim report)

Group revenue was EUR 35.5 million (EUR 44.9 million in July–September 2025). Revenue decreased by 21%.

EBITDA was EUR 3.7 million (3.3).

Operating profit was EUR 1.2 million (1.1) and was 3.4% of revenue (2.5%).

The result included personnel expenses related to the termination of employment relationships EUR 0.4 (0.4) million and other non-recurring expenses EUR 0.6 million (0.6).

Earnings per share was EUR 0.01 (0.02) per share.

Savings measures from profit improvement programs were reflected in improved profitability.

The AI-assisted enterprise resource planning system for HR services is in use in all regions and industries; we have moved as planned from implementation to the continuous development phase.

The implementation of the new organization announced in June and the management model that places our customer’s decision-making at its core was continued.

For Eezy, light is really starting to appear at the end of the tunnel as the market decreased slightly less and profitability was very good. In Q2, development seemed to be still slightly worse than the market, meaning the trend is correct. If we look at the adjusted figures, the operating profit (EBITDA) would have been €4.3 million, or as much as 13%, without one-off expenses. Although these one-off items have been continuous now, at least the costs related to personnel reductions should end next year, provided that the decline in revenue stops as the economic situation improves. In the recent months’ business cycle barometer for the staffing industry, expectations for the future have already been quite firmly in positive territory. If Eezy’s own operations now seem to be in order (profitability, maintenance of market share), then concrete improvements can already be achieved next year. Of course, they must, as the financial position is so tight.

I listened to Eezy’s earnings webinar, and regarding the covenant levels, it was only stated that discussions would be held in good faith…

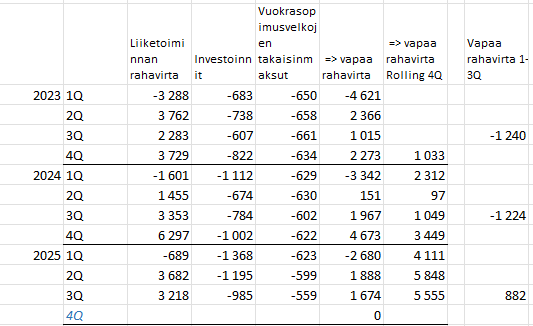

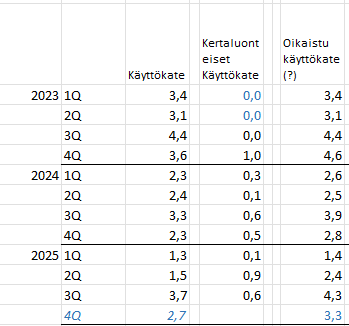

From the interim reports, I dug out the EBITDA, net debt including IFRS 16, and the net debt/EBITDA ratio. This is calculated by summing the rolling 12-month EBITDA and dividing it by the net debt including IFRS 16 at the end of the period.

If 1) the debt amount is kept / can be kept unchanged, and 2) EBITDA changes from the 3Q2025 level onwards as in the previous year, then, for example, a level of 5.0 does not require any special performance.

A level of 4.0 would require an EBITDA of 12.5 million euros with net debt including IFRS 16 of 50 million euros, and a level of 3.0 would require an EBITDA of 16.7 million euros.

So, the math is delicate when we are hovering near zero.

Of course, one could speculate that pushing the debt down to the 50.0 million euro level has required some effort with accounts receivable and accounts payable. Perhaps a better process for receivables, perhaps accounts receivable have been sold, perhaps longer payment terms have been agreed upon. Perhaps longer payment terms have been agreed upon for accounts payable, paid as late as the contract allows or with a delay, perhaps cash discount terms are not utilized, etc. Anyway, accounts receivable from a year ago -5.2 million euros, accounts payable +1.6 million euros. Mysteriously, the interim report also states that “The amount of operating free cash flow is temporarily affected by measures taken to optimize cash flow during January-September.” So, something has been done that

00:00 Introduction

00:12 Third quarter development

01:05 Background factors for the decline in HR services revenue

02:29 Cost structure and efficiency measures

04:52 What’s the status regarding the enterprise resource planning system?

06:57 Indebtedness and covenant levels

Well, indeed, it says there that adjusted EBITDA is used.

I calculated it using the EBITDA presented in the interim report, and indeed the result of the net debt/EBITDA calculation was the same as what is stated in the interim report. When EBITDA is a rolling 12 months and net debt includes IFRS at the end of the reporting period.

We probably don’t know what the adjusted EBITDA is, or what the covenant levels are now and in the future… perhaps the adjustment could then be those specifically mentioned, such as for Q3 2025:

The result included personnel costs related to the termination of employment relationships of EUR 0.4 (0.4) million and other non-recurring costs of EUR 0.6 (0.6) million.

I find it somewhat strange that financing negotiations were just held in the spring, and since then, the operating margin/cash flow development has been quite good. So how is it that we’re in a situation where next year will be tight with covenants again? What level of performance was expected, then?

“Eezy generated a free cash flow of 0.9 MEUR in Q1-Q3’25, which reflects the criticality of strengthening cash flow to bring down indebtedness.”

This cash flow was the best for the first 3 quarters since 2022 (even then, only lower investments made it better), and Eezy’s cash flow is generally weighted towards the last quarter. With the current cost structure, it seems that the cash flow will be strong this year as well, although the cash flow optimization measures have yielded some good results in these earlier quarters, which might take a little away from the last one.

Since efficiency measures with their one-off costs have been heavily implemented quarter after quarter, and now if these are not done in Q4, then the cash flow should be stronger in this respect as well, without those costs. Next year, the investment level can be expected to drop just a little, based on what I heard from the CEO in the webcast.

It seems that Eezy would have good prospects for future quarters, but those challenges regarding financing covenants

Free cash flow this year – if calculated as Operating cash flow - investments - lease liability repayments – has indeed been only 0.9 M€. However, that is clearly more than the -1.2 M€ of the corresponding periods in 2023 / 2024.

4Q2023 was 2.3 M€, and 4Q2024 was as much as 4.7 M€.

I interpreted that some cash flow pumping has been practiced during 2025, so I would be surprised if a setback like last year’s occurred. This is because quite many companies perform their pumping at the end of the year, perhaps Eezy also did it earlier.

On the other hand, “one-offs” have already accumulated this year to the extent of 2024, it remains to be seen whether operating cash flow needs to be burdened with them in 4Q2025… Well, perhaps, let’s see, the decline in turnover has continued and the first quarter is the year’s low point.

My own interpretation, as can be inferred from the interview, is that the covenants are tightening more than the situation is improving. Probably in the 1Q2025 covenant negotiations, the focus has been more on 2025 covenants than 2026, as well as the perception that the business environment would improve in 2H2025 or similar. This has been hoped for and expected for the entire national economy for a long time… EDIT: an addition to that, both Saksi and Westermark mention that historically, the staffing industry was among the first to rise when an upturn begins.

Yes, something has been pumped, and because of that, Q4 might not have as good cash flow as in previous years, but if you scroll through 5 years of Q4 reports, Q4 has always been by far the strongest quarter in terms of cash flow. So, relatively, it might not be as strong as in recent years, but I would be surprised if net debt isn’t also pushed down in the last quarter. And the strong operating profit margin already in Q3 doesn’t hurt in this regard for Q4.

While pondering this, I have now concluded that when negotiating during Q1, the assumption was that Q1 and Q2 would already perform better in terms of operating profit/revenue, and the trend would improve towards the end of the year. Then the market didn’t ease at all, and the expected improvements for 2026 now look challenging from the current level. Could they have expected a return to closer to the €15 million operating profit level in 2026? In any case, I’ve arrived at pretty much the same conclusion as you.

Tässä on Petrin kommentit henkilöstöpalvelualan laskumenosta lokakuussa.

*According to the staffing industry’s revenue survey, the revenue of the 20 largest companies in the sector was approximately EUR 120 million in October, which represents an 8% decrease year-on-year. The development of the overall market is essentially linked to temporary staffing

This has been in several threads today, but let’s save it in Eezy’s thread too, as we are sniffing out a turnaround in the economic situation. In October, the pick-up continued in both construction and industry. Retail sales figures were also good in October.

Unfortunately, this good buzz was not yet reflected in Hela’s October figures (Petri’s comments on this above in @Sijoittaja-alokas’s message) even though they already had growth expectations for this Q4.

Well, the goals are good, but when revenue and the stock price have been declining for a long time, and a couple of strategy rounds have had similar goals – it certainly requires effort to believe in these… And at the same time, to believe in the turnaround of the Finnish economy.

More details behind the link.

Eezy’s long-term goals 2028:

Over 330 million € chain revenue

Over 200 million € group revenue

Over 5% operating profit from group revenue

Eezy’s goal is to continue distributing 30–50 percent of the financial year’s profit as dividends.