Eezy had good slides, but I was left feeling a bit uneasy that the company couldn’t build a sufficiently concrete bridge of actions between the current situation and the 2028 targets.

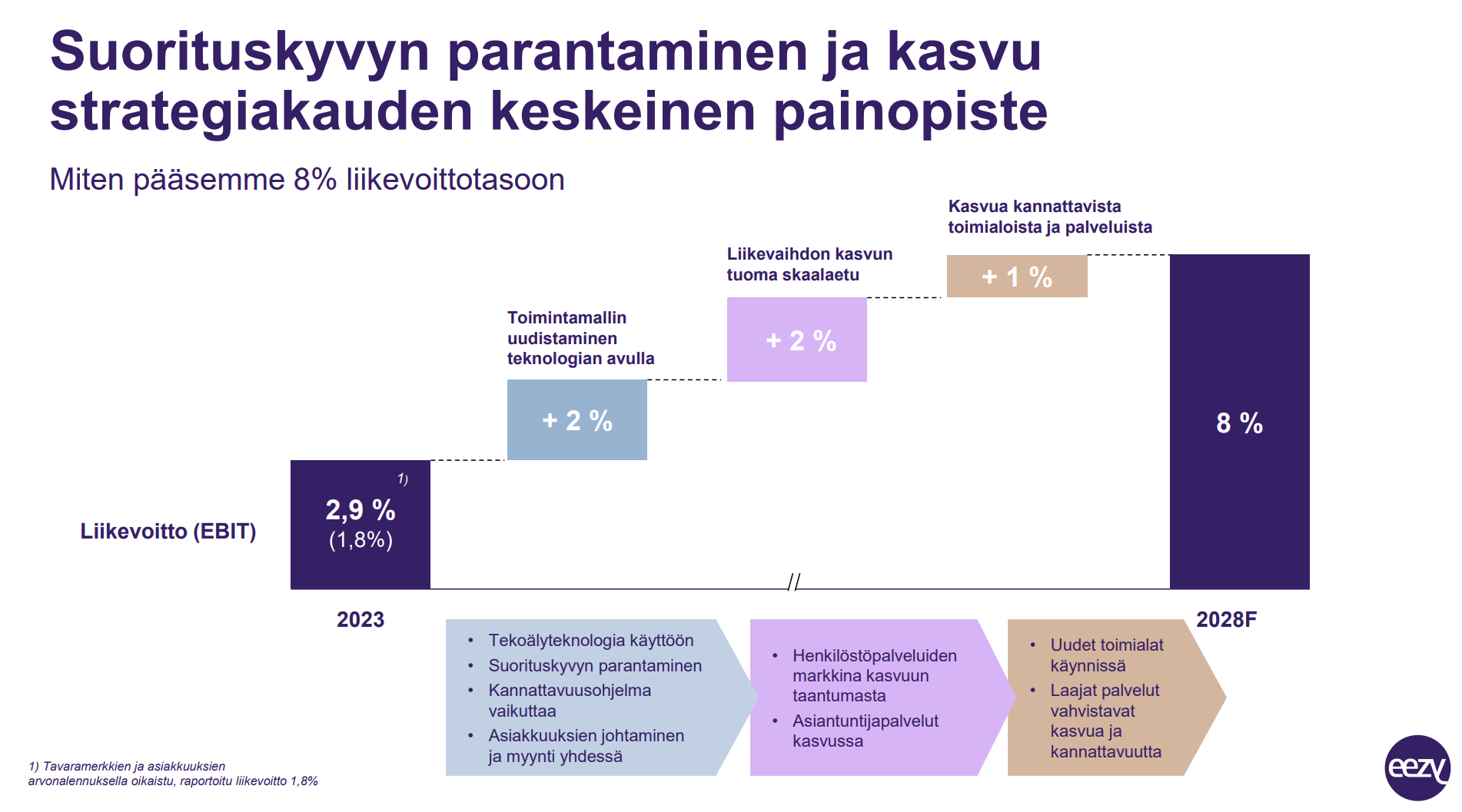

-2028: EBIT 8%

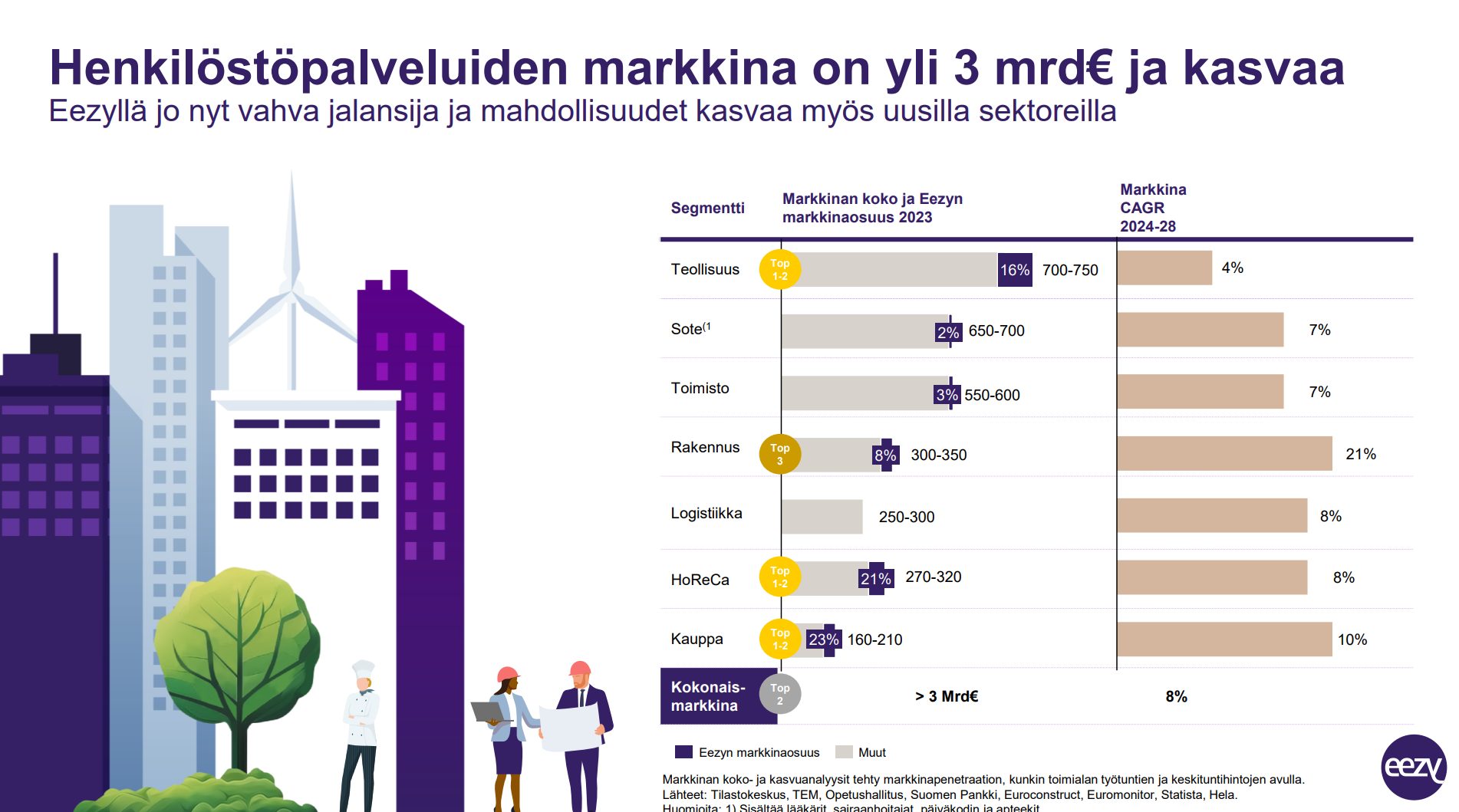

-staffing services (85% of the company) grow faster than the market. Stated CAGR 8%

-expert services (15% of the company): doubling, i.e., CAGR approx. 15%

In the shorter term, the company has stated that historically the industry starts to react quickly at a cyclical turnaround.

In my experience, targets and slides are easy to create, but what is difficult is: functional action plans, execution and its monitoring, and reacting effectively to both plan weaknesses and deviations.

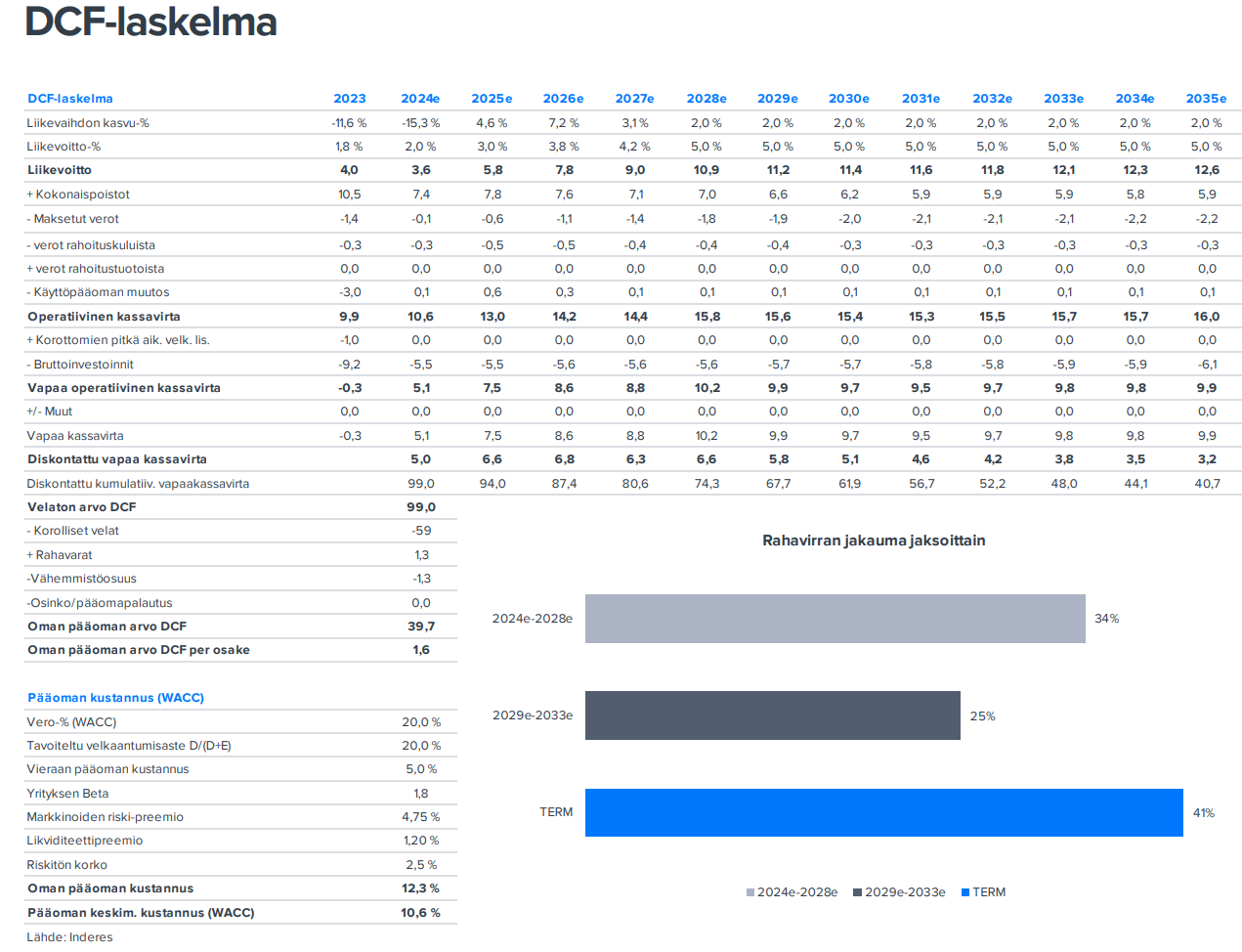

Based on the DCF valuation in the extensive report, you don’t seem to have enough faith in Eezy’s stories either, and judging by the stock’s valuation, neither does anyone else—not that the targets will be met, neither the top-line nor the bottom-line, let alone both.

Based on my own calculations, Eezy’s 2028 targets would lead to a revenue level of 275 MEUR and an EBIT level of 27 MEUR, making the EPS around 0.78 EUR/share.

Of course, from a shareholder’s perspective, it’s comforting that the report’s DCF valuation of 1.6 EUR is reached with the parameters used even with a significant target miss, i.e.:

-2028 revenue 218 MEUR (i.e., 2023 level)

-2028 EBIT 5.0%, i.e., 10.9 MEUR

-resulting in an EPS of around 0.25 EUR/share

Summa Summarum, the company doesn’t need to get anywhere near its targets for the valuation to indeed seem quite affordable. On the other hand, both revenue and earnings targets can fail reasonably, and the investment can still be decent.

Turnaround company or cyclical turnaround, both are good and preferably both.

https://keskustelut.inderes.fi/t/eezy-sijoituskohteena-ent-vmp/105/390?u=opa