@Geologiopiskelija had accurately identified the reasons why I, too, find this company interesting, but this IPO doesn’t appeal to me. For the European expansion, the balance sheet should have been strengthened much more to my liking, meaning a proportionally larger share issue should have been done. Now, this is primarily a greedy share sale.

The valuation relative to the previous fiscal year’s figures and even pro-forma figures is particularly shocking, but the management practically guides that the profit will double in the current fiscal year (Tecno Globe + 15% organic growth + significant reduction in financing costs), which would bring the forward-looking P/E ratio to around 20. But that’s a promised figure, and still, in my opinion, too much, especially since we don’t know what kind of guide the company’s management is: do they have a good outlook on future results, can their word be trusted, etc. The company has not yet proven itself to the markets for such high multiples to be accepted with just a shrug. There’s little room for error. If growth falters in the current fiscal year, the stock will recoil significantly downwards.

The preceding was my opinion. Now for the factual part of the message.

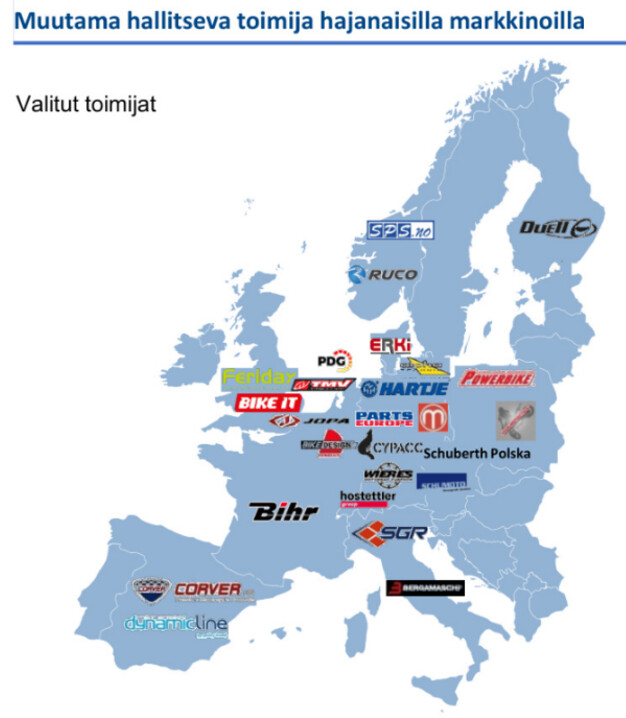

Duell, Bihr, and Parts Europe are the three major players in Europe, with revenues exceeding 100 million euros. All of Duell’s competitors are private companies, but I tried to find their financial data with varying success.

Here is an article about Bihr, a leading player in France:

Bihr employs 400 people, including 240 in France and 100 in Spain, and turns over 140 million EUR, of which the largest share of 120 million EUR is generated through the sale of spare parts and accessories, and 20 million through protective clothing and helmets. Operating in the B2B segment, the company supplies more than 14,000 dealers across Europe with over 200,000 brand-name articles.

Additionally, I found information that Bihr’s revenue in 2019 was 102 million and profit was 3.1 million.

Parts Europe is a leading player in Germany. In 2020, revenue was 109 million euros. Gross margin 31%. EBIT 3%. Profit 1.7 million. Revenue growth 16.4%.

Swiss Hostettler has 950 employees, but it is only partially a competitor to Duell.

In the Benelux countries, a major player is apparently Powersports Distribution Group, which advertises itself as “Europe’s fastest-growing motorcycle parts distributor.” The company has made many acquisitions in recent years.

The financial data of all Norwegian and British private companies can be found online for free. Here are the financial data for some (smaller) competitors for 2020:

- Ruco Scandinavia. Revenue 13.6 million euros. Gross margin 30%. EBIT 8%. Profit 0.7 million euros. Revenue growth 13%.

- Spare Parts Service AS. Revenue 6.2 million euros. Gross margin 38%. EBIT 14%. Profit 0.6 million euros. Revenue growth 11%.

- Feridax Group Limited. Revenue 16 million euros. Gross margin 35%. EBIT 17%. Profit 2.3 million euros. Revenue growth 0%.

- Bike It International Limited. Revenue 8.6 million euros. Gross margin 23%. EBIT 0.8%. Profit 50,000 euros. Revenue growth 15%.

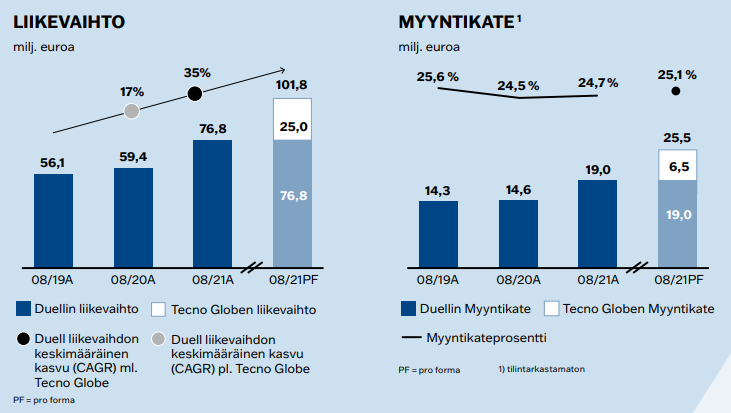

For comparison, Duell’s 2020 figures: Revenue 59 million euros. Gross margin 25%. EBIT 7%. Profit 1.7 million euros. Revenue growth 6%.

This is a somewhat mixed and, of course, incomplete sample, but at least a couple of observations can be made:

- All companies have grown significantly in a market that reportedly grows only 2% annually.

- Duell’s gross margin is lower than almost all competitors. Is the secret to Duell’s success that they just sell goods cheaper? One would think that as a wholesaler, this would at least gain market share. A more negative explanation would be that it’s not a pricing strategy, but rather Duell is compelled for some reason to sell goods cheaper than all its competitors.

It would be worthwhile to examine the competitors’ figures in more detail, and I realized that these figures probably should have been compiled into a table, but I’ll do that sometime later. I encourage others considering investing in this company to conduct a comparative analysis relative to competitors.