In physics lectures, when trying to explain how magnetism works, it’s sometimes illustrated using rubber bands. This might help in understanding the very basics, but it is extremely harmful to a deeper understanding of the phenomenon. Depreciation and amortization (D&A) present a similar challenge among investors when they are taught too much through the lens of wear and tear on physical assets. D&A has nothing to do with maintenance or replacement investments, or wear and tear.

Let’s approach this from a bit further away. What is the difference between a cost and an investment? The time horizon. Investments are costs that are expected to generate results in future fiscal years, which is why, from an income statement perspective, it is appropriate to try to smooth these costs over a longer period. The net result specifically should carry the weight of history with it to provide a sufficiently universal figure for evaluating any company’s general profitability, regardless of the year under review. Cash flow is not suitable for this purpose because it can fluctuate very wildly from one fiscal year to the next.

The key is that time horizon. For example, the salary costs used for programming in a small Finnish software firm as development expenses are an investment that can, under certain conditions, be capitalized on the balance sheet. After this, these previously cash-paid, otherwise quite ordinary salaries, will start to run as amortization in the coming years. It doesn’t matter if the same kind of development work needs to be done again in five years, or if the code is in use for a hundred years, or if the code has maintenance costs. What matters is the accrual of expenses and income so that the link between them is at least somewhat maintained in the income statement.

Now we get back to Duell. An acquisition is fundamentally an investment in the future income stream of the target, so it must be treated just like any other investment. The challenge arises because an increasing part of companies’ earnings power is directed toward intangible assets, and we lack auditing methods to smartly evaluate the value of intangible assets. How do you value good management, excellent customer relationships, exceptional pricing power, a world-class brand, and everything else valuable and intangible that comes with an acquisition on the balance sheet? This is where shortcuts are taken, assuming management pays the market price for all these vague, hard-to-value intangibles, which can simply be assumed to be the difference between the purchase price and the acquired assets. Unless some concrete justification is found for this goodwill to anchor it to the balance sheet, amortization must begin, and since the income is spread over several future years, the amortization must also be done over several future years.

So, we finally get to the essential question. If you want to adjust the result in this regard and make it logically inconsistent with the rest of the income statement, what are your justifications? There are, of course, good reasons, but if the negative weight of these past “investment sins” in the result bothers you, then the net result is entirely the wrong figure for you to use, because that’s kind of the point of that figure ![]()

I don’t want to defend the income statement and the auditors, as I certainly have plenty of criticism and development ideas, and it feels like those pencil-pushers nowadays are just messing up our work as investors—but if you really want a cash flow figure, then by all means, look at the cash flow instead of the net result.

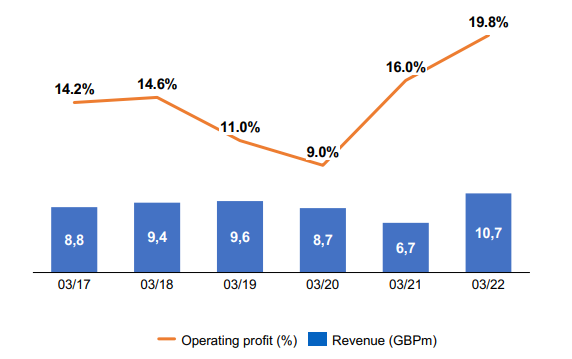

In a normal year, Tran-Am has an op. profit of less than 1.5 million pounds, and in a bad year, closer to 1 million pounds. If one assumes the following years will be weaker and that indebtedness and the cost of equity will grow as a result of the acquisition, it becomes quite difficult to create value for investors.

The same thing happened last year with PowerFactory, which might look like a good deal based on peak year figures, but if you use the lower figures of more normal years, a different picture emerges.

Yeah, yeah, you can protest with synergy benefits and that the acquisition target has undergone a transformation in recent years, etc.

It can’t really be proven either way, but the acquisitions have hit the peak demand years quite “nicely,” and now that a recession and cuts are ahead, Duell no longer has the firepower to buy at the genuinely cheaper multiples of weaker demand years.