Nostellaan tämänkin kun on jäänyt Q2 laittamatta

2 tykkäystä

Laitetaan tännekkin q4 2024

3 tykkäystä

D.localin kvartaalirapsa osoitti vahvaa kasvua ja enkkatason ltoimintaa.

Kokonaisvolyymi (TPV) nousi 41 prosenttia vuodentakaiseen verrattuna, ja liikevaihto kasvoi 13 prosenttia.

Käyttökate parani edelliseen kvartaaliin verrattuna, vaikka vuositasolla se kuitenkin laski hieman. Kassavarat lisääntyivät huomattavasti ja yhtiö saavutti 100 prosentin kassakonversion nettotuloksesta. Cross-border-maksut ylittivät 3 miljardin dollarin rajan.

Nettotulos laski, mikä johtui kuitenkin pääasiassa korkeammista rahoituskuluista. Yhtiö panosti teknologiaan ja maksujärjestelmiin mm. lanseeraten uusia palveluita. Johto on erityisen optimistinen pitkän aikavälin strategian suhteen. ![]()

https://x.com/AIStockSavvy/status/1856814763160080648

3 tykkäystä

Dlocal on ostamassa afrikkalaisen maksuvälittäjä AZA Financen, tarkoituksena vahvistaa preesensiä Afrikan markkinoilla. Linkki ohessa:

Ilmeisesti markkinat eivät ole tykänneet hinnasta tai hankinnasta, sillä osake on tätä kirjoittaessa n. 3% laskussa. En pikaisella googlauksella löytänyt mitään virallista tietoa tästä ostettavasta kohteesta. Edellisen viestin jälkeen Dlocal on raportoinut myös 2025 ykköskvartaalin tuloksensa. Tuolloin sekä EPS että liikevaihto ylittivät ennusteen. Dlocalilla on erittäin vahva kassa, ja tämä AZA financen osto pystytään rahoittamaan suoraan kassavarannoilla, eli velkaa ei tarvitse ottaa.

Tässä myös linkki Dlocalin omaan Q1 raporttiin: https://dlocal.gcs-web.com/news-releases/news-release-details/dlocal-reports-2025-first-quarter-financial-results

3 tykkäystä

2 tykkäystä

Alla oleva tviittiketjussa kerrotaan mm. miten dLocal on noussut vahvaksi toimijaksi kehittyvien markkinoiden maksuliikennepuolella palvellen jättiyhtiöitä kuten Amazonia ja Spotifyä.

Ketjussa kerrotaan mm. siitä, miten yhtiö kasvaa nopeasti, mutta marginaalien ja hinnoittelun paineet näkyvät.

Alla on linkki tviittiketjuun ja sen aloitusviestin. Sitten niiden alla on vielä linkki, josta voi suoraan lukea koko tviittiketjun läpi, vaikka ei olisi X-tunnuksia. ![]()

Alla olevassa tviittiketjussa kerrotaan, miten DLocalin tarina olisi kääntymässä uuteen nousuun ja tuossa ketjussa perustellaan, miksi näin voi käydä.

Osake on romahtanut huipuistaan, mutta nyt luvut, johto ja markkinat puhuvat tviittaajan mukaan puhuvat ns. toista kieltä. Mukana ketjus on tiivis, mutta hyvä katsaus kasvulukuihin, TPV-kehitykseen, marginaalien normalisoitumiseen ja miksi uusi kaveri Pedro Arnt saattaa olla juuri se, joka pystyy auttamaan yhtiön käänteessä. Hyvää jutussa on se, että lopussa mukana on myös bull/base/bear-skenaariot arvostukselle.

Alla on vielä linkki, josta voi suoraan lukea koko tviittiketjun läpi, vaikka ei olisi X-tunnuksia ja sen alla on linkki sitten taas suoraan Äxään, jos X-tunnukset omaava haluaa lukea sieltä. ![]()

https://twitter-thread.com/t/1948723093733564812

https://x.com/TacticzH/status/1948723061101838656

4 tykkäystä

Q2 ulkona, varsin mainioin tuloksin ![]()

In the second quarter of 2025, DLocal achieved a record Total Payment Volume (TPV) of $9.2 billion, marking a 53% year-over-year increase. The company also reported revenues of $256.5 million, up 50% from the previous year, driven by strong performance in Brazil and Mexico, as well as rapid growth in other regions. DLocal’s Adjusted EBITDA rose by 64% to $70.1 million, reflecting consistent operational leverage.

Key financial metrics highlighted in the report include a gross profit of $98.9 million, up 42% year-over-year, and a free cash flow of $48 million, demonstrating robust cash generation capabilities. The company’s net income for the quarter was $42.8 million, slightly down due to currency devaluation impacts, but operational improvements were evident with an 85% increase in operating profit.

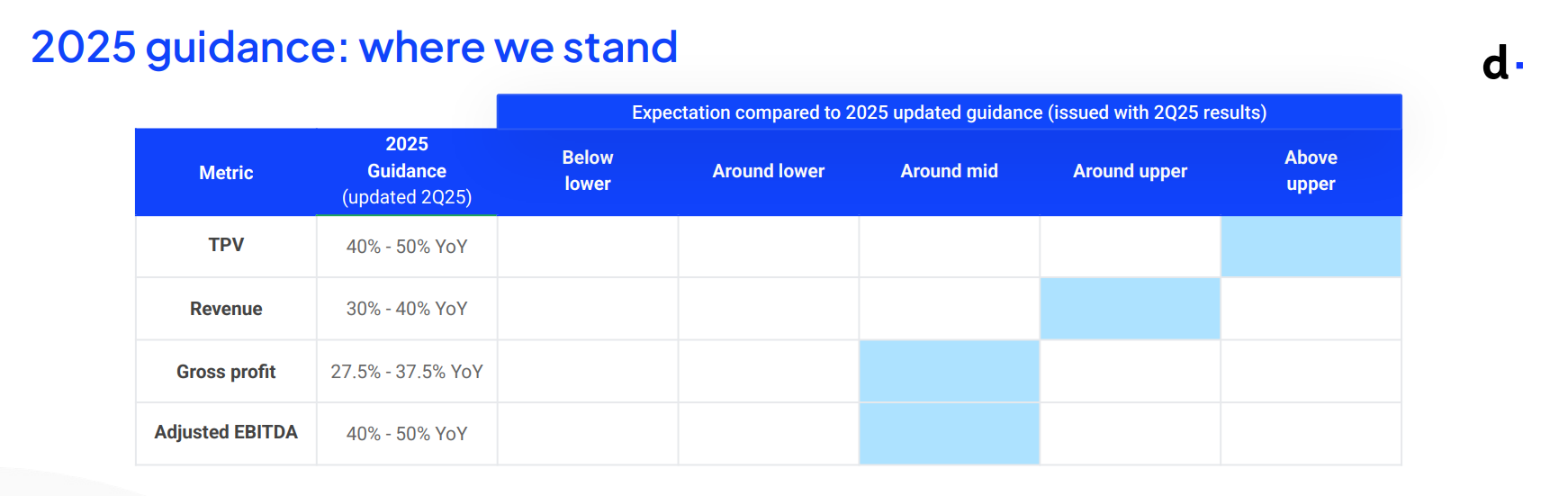

Looking ahead, DLocal has adjusted its full-year 2025 guidance upwards for TPV, revenue, gross profit, and Adjusted EBITDA, indicating confidence in sustained business momentum. The company is also making governance changes, including transitioning to a majority independent board and canceling treasury shares to return capital to shareholders.

lähde: DLocal Reports Strong Q2 2025 Financial Growth - TipRanks.com

dLocalin oma sijoittajapresis

Näkymiä nostettu reilusti

postmarket tuloksen jälkeen ![]()

11 tykkäystä

Oheisen linkin mukaan Dlocalin shorttaus on selkeästi noussut viimeisen kk aikana. En niin hyvin ymmärrä näitä, mutta premarket-action viittaa mielestäni hieman siihen, että olisiko tässä short squeeze rakenteilla? Ymmärtääkseni kannasta on n. 10% shortattuna. Lisäksi insiderit omistavat n. puolet osakkeista, joten vapailla markkinoilla osakkeita on tarjolla suhteellisen vähän. Jos ymmärsin oikein ![]()

https://www.nasdaq.com/market-activity/stocks/dlo/short-interest

3 tykkäystä

dLocal ja Tiendamia kumppanuuteen vauhdittamaan rajat ylittävän verkkokaupan kasvua Latinalaisessa Amerikassa

Kumppanuus laajentaa paikallisia maksuja viidellä keskeisellä Latinalaisen Amerikan markkina-alueella, antaen yrityksille mahdollisuuden kerätä ja maksaa tehokkaasti samalla kun tarjotaan ostajille nopeampia, kätevämpiä ja kattavampia maksukokemuksia.

3 tykkäystä

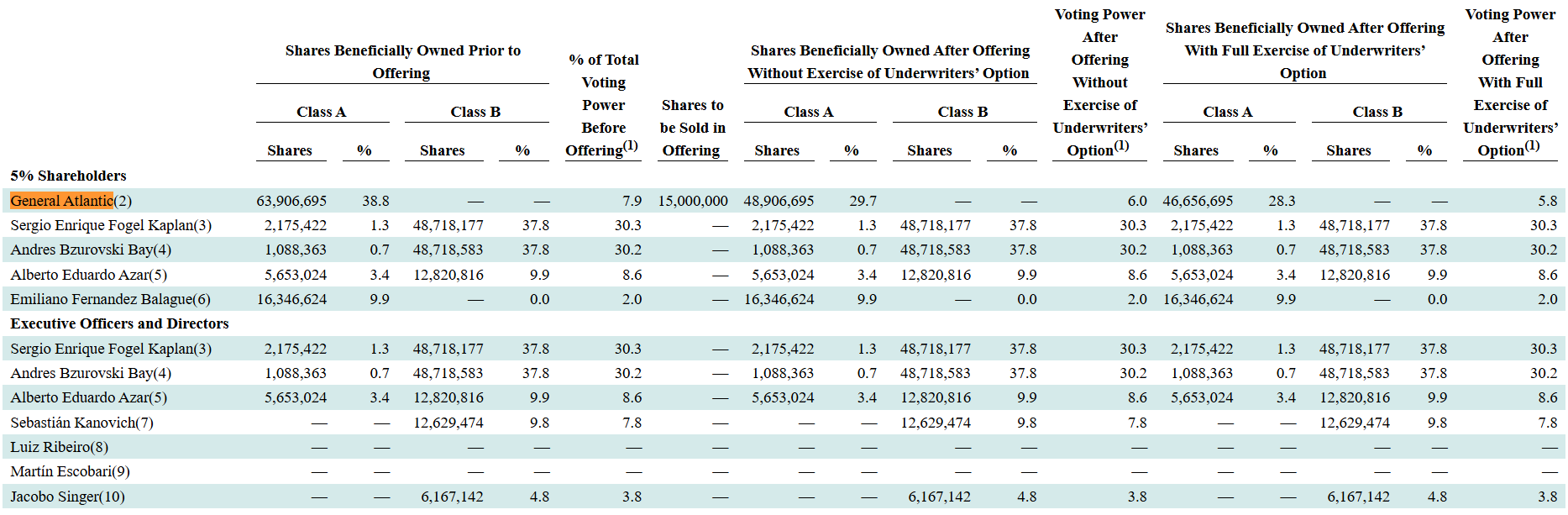

Isoin omistaja myy 15000000 lappua blokkikaupalla, lisäoptiona 2500000 jos hinta miellyttää.

Markkina ennakoi tietysti osakkeen laskulla, mutta usein vastaavat tilanteet on olleet hyviä ostopaikkoja.

Isoimmat omistukset tällä hetkellä ja myynnin jälkeen

2 tykkäystä

Syyskuussa ilmestynyt deep dive, mielestäni kiteyttää hyvin osaltaan tätäkin viestiketjua tapahtumista, shorttirapsoista ja muista syytöksistä, jotka ymmärrykseni mukaan jäivät perättömiksi, ja viimeisimmästä noususta Q2 tuloksen jälkeen. Kilpailua, riskejä ja potentiaalia tuotu esille ja omat DCF-laskelmat myös tuossa. Selkeää tekstiä, lukusuositus.

vilpukkaulpukka

5 tykkäystä

Hated Moats teki tästä myös tuoreita DCF-laskelmia

taustalaskelmat nähtävissä, jokainen saa arvioida oman makunsa mukaan ![]()

5 tykkäystä

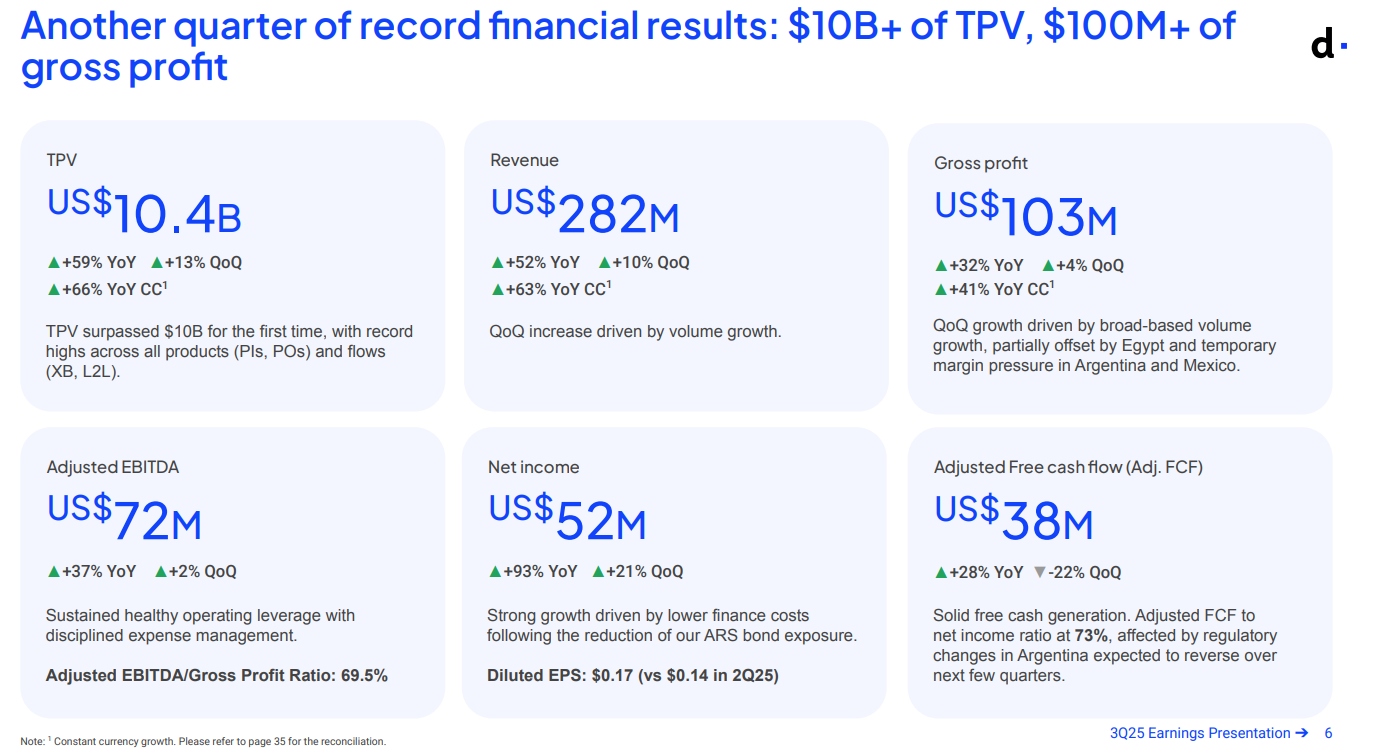

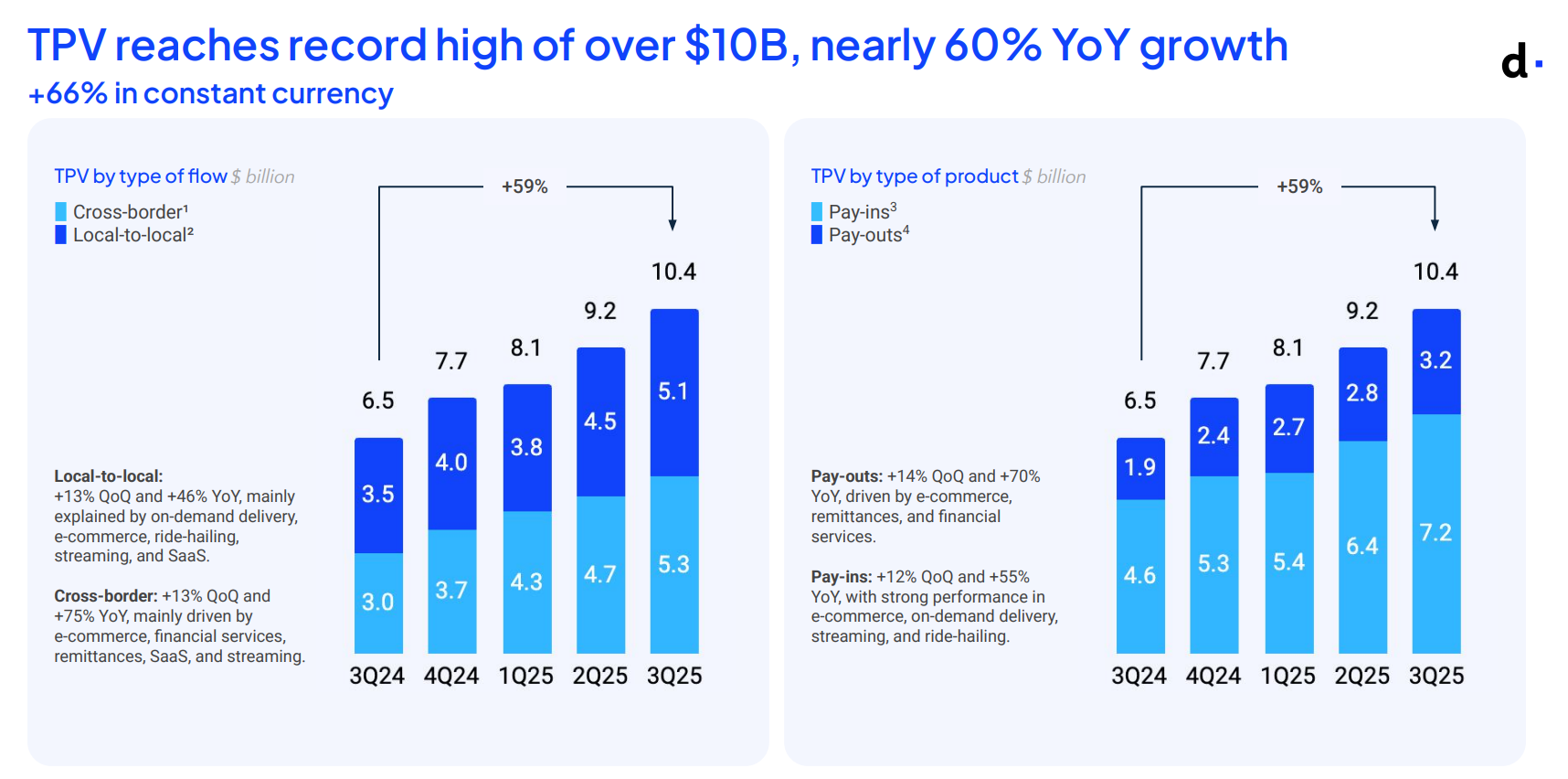

Q3 - kiteytetty copilotilla

- TPV (Total Payment Volume): 10,4 mrd USD → +59 % v/v

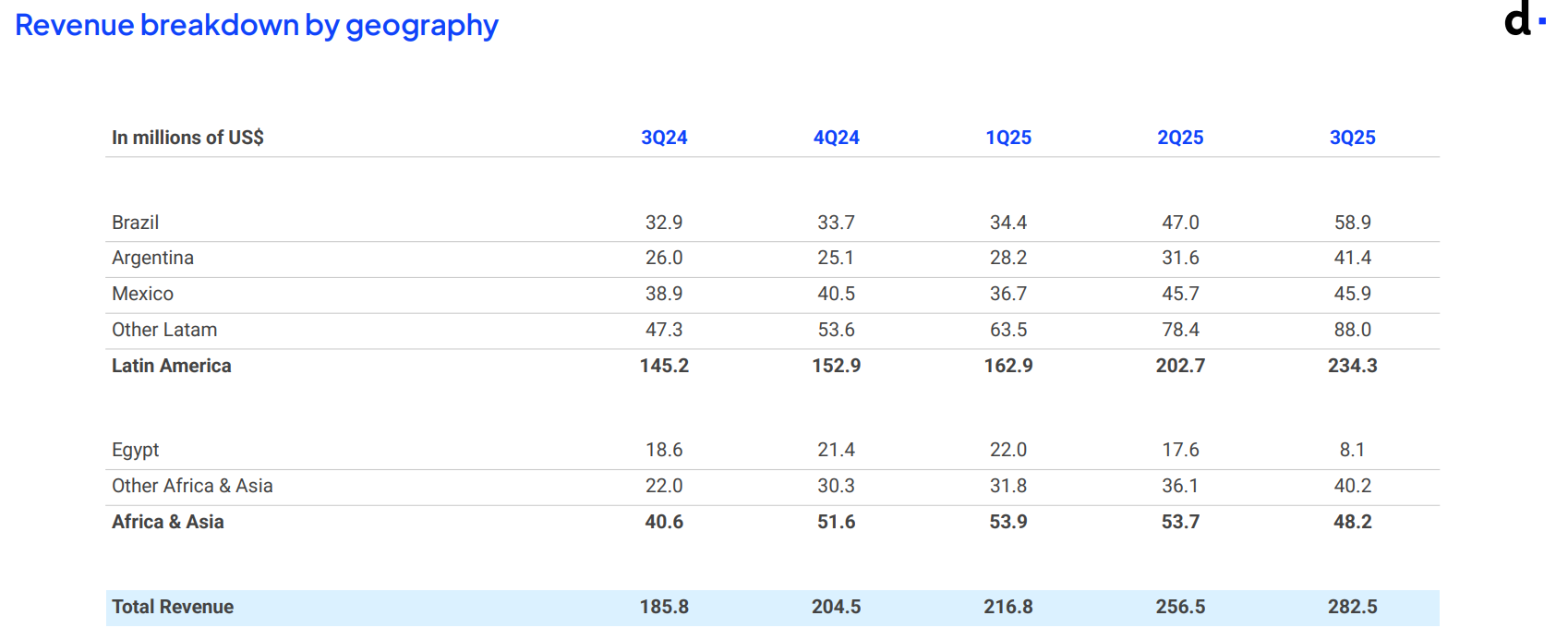

– Ennätystaso, vetureina erityisesti Kolumbia, Bolivia ja Nigeria. - Liikevaihto: 282,5 milj. USD → +52 % v/v

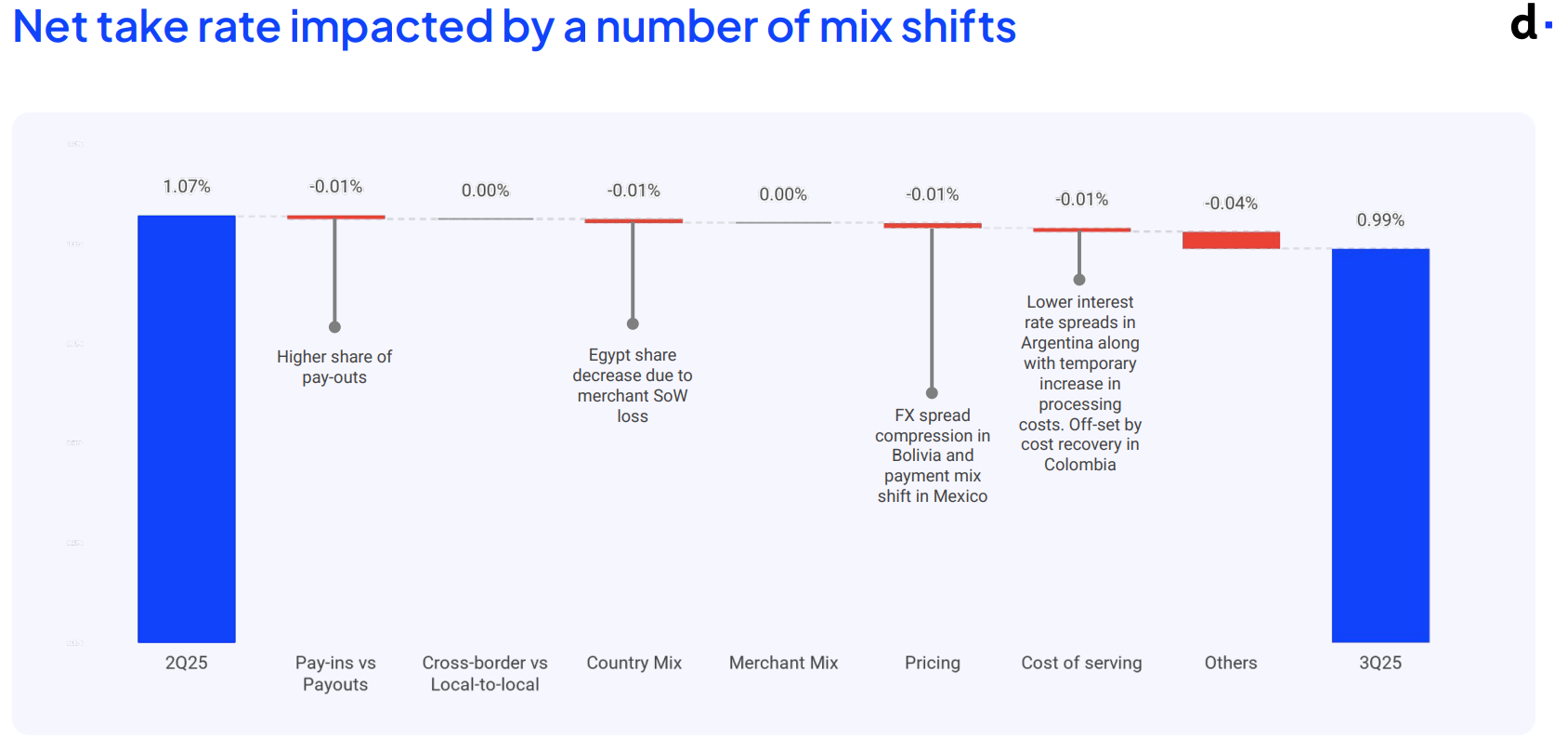

– Kasvua volyymien noususta, etenkin LatAm ja Afrikka. - Bruttokate: 103,2 milj. USD → +32 % v/v

– Marginaalia painoivat Meksikon maksutapamuutokset, Argentiinan korkotuottojen lasku ja kustannusten nousu. - Bruttokatemarginaali: 37 % (vs. 42 % vuotta aiemmin)

- Käyttökate (EBITDA): 71,7 milj. USD → +37 % v/v

– EBITDA-marginaali 25 % (vs. 28 % vuotta aiemmin). - Liikevoitto: 55,6 milj. USD → +35 % v/v

- Nettotulos: 51,8 milj. USD → +93 % v/v

– 0,17 USD/osake. Hyötyi pienemmistä rahoituskuluista, kun yhtiö vähensi Argentiinan peso-sidonnaisia velkainstrumentteja. - Vapaa kassavirta: 37,6 milj. USD → +28 % v/v, mutta -22 % Q2:een verrattuna.

– Tilapäinen vaikutus Argentiinan rahavirtojen kotiuttamisesta johtuvista rakenteellisista muutoksista. - Käteinen: 604,5 milj. USD (corporate cash 333,1 M USD) → vahva likviditeetti.

Yhteenveto:

dLocal toimitti jälleen erittäin vahvan kasvun kvartaaliin, mutta marginaalit ovat lievästi paineessa markkina- ja kustannustekijöiden vuoksi. Nettotulos kasvoi kuitenkin selvästi, ja kassatilanne on vahva. Yhtiö jatkaa investointeja teknologiaan ja myyntiin, mikä tukee kasvua tulevilla kvartaaleilla.

Edit: lainattu sisältö Yahoo ist Teil der Yahoo-Markenfamilie.

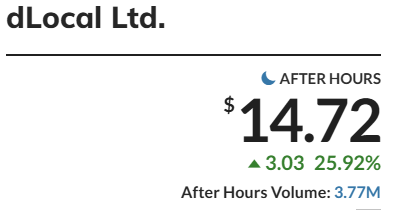

Jälkipörssi -8% tulosjulkistuksen jälkeen ![]()

8 tykkäystä

Vielä koko raportti:

Sekä sijoittajapresis, josta muutamat poiminnat

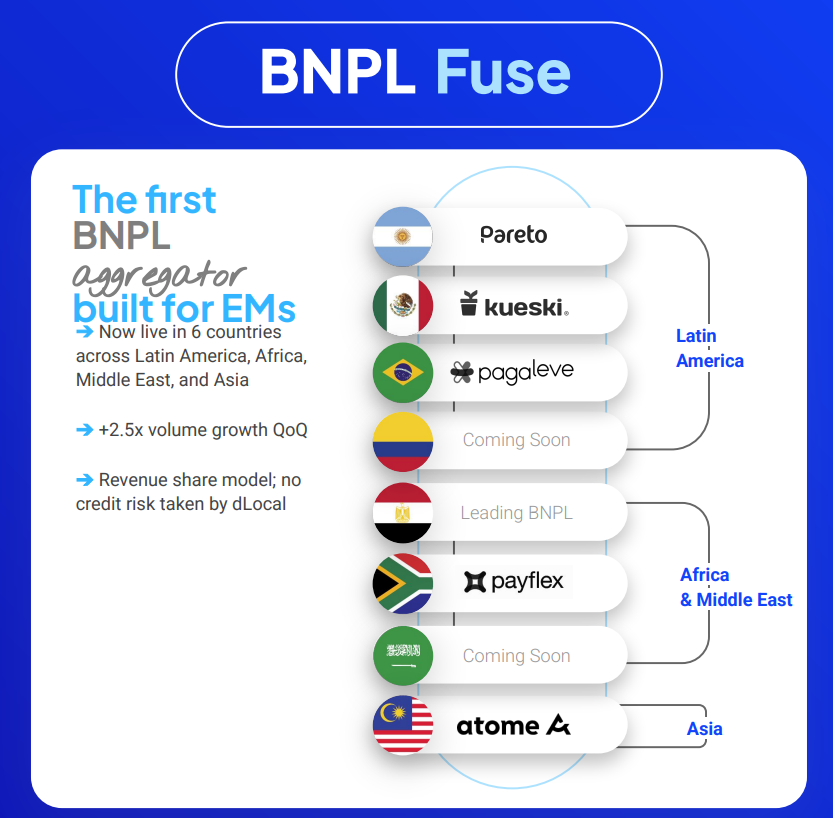

Buy now, pay later -malli laajenee

Tämä ilmeisesti se kurssiin vaikuttava slaidi

Menossa nostetun ohjeistuksen ylälaitaan

Ja Egyptissä poistui asiakas

7 tykkäystä

Erinomainen tulos. Pedro painottikin puhelussa pariin kertaan että TPV on tärkein mittari heidän kohdallaan ja se veti erittäin hyvin. Alla olevasta linkistä pääsee kuuntelemaan Q3 2025 tulospuhelun, puhelu alkaa n. ajassa 16:00 jos haluaa skipata striimerin löpinät:

Pari mielenkiintoista nostoa mitä itsellä tuli tuossa vastaan

- Dlocal on aloittanut BNPL (Buy now, pay later) -tuotteiden tarjoamisen, mutta käyttää tähän paikallisia kumppaneita eikä itse ota luottoriskiä. Lisäksi BNPL-tuotteista saadaan parempi kate, sillä myös tuo BNPL-tarjoaja maksaa Dlocalille

- 6/7 Mag7:n yhtiöistä on Dlocalin asiakkaita. Tämä tuo myös mukavaa kasvupolkua kun nämä jätit jatkavat kasvua kehittyvillä markkinoilla (24:00 ylläolevassa linkissä)

- Luin itse rivien välistä Pedron kommenteista ajassa 46:50, että kun voluumia tulee lisää ja firma kasvaa, niin näiden netotusmahdollisuuksien käyttö varmasti lisääntyy ja Dlocal saa isomman osuuden valuuttakurssien spreadista.

7 tykkäystä

Auttakaa toverit hyvä minua ymmärtämään markkinan reaktio. Bruttokatelaski “pienesti” ja net take rate pieneni.

Odottiko markkina oikeasti vielä vahvempaa tulosta? Oon aivan hämmilläni…

Edit: Itse näen kans että tuo TPV on huomattavasti tärkein mittari tällä hetkellä.

Katsoisin ensin normaalin aukioloajan markkinareaktion. Ainakin normaalina päivinä aftermarketin voluumi on ollut aivan olematonta. Lisäksi johdolla merkittävä osuus osakkeista, joten free float on pieni. Isommat pelurit tätäkin liikuttaa. Shorttaajien osuus on edelleen suuri, joten jos joku iso peluri alkaa ostamaan reippaammin niin saatetaan nähdä isoja liikkeitä päivän sisälläkin.

Hyvä paikka lisätä / tehdä entry mielestäni jos tämä on markkinoiden tuomio.

2 tykkäystä

Erinomainen Q3:n läpikäynti Cunhan tuttuun tyyliin.

mm. Net take rate -laskun syy avattu hyvin

2 tykkäystä

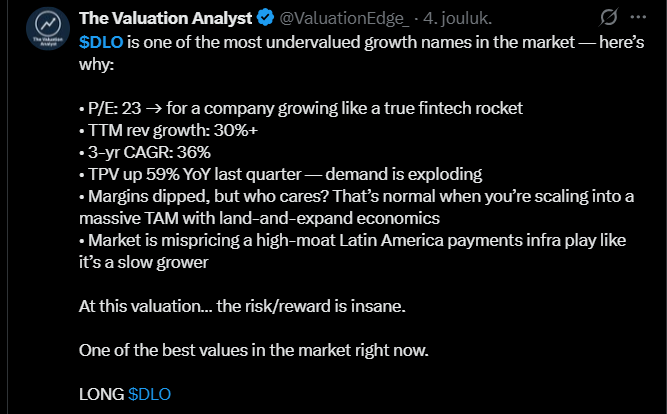

Tässä ajankohtaisessa pikakatsauksessa yhtiöön nostetaan esille, että DLocal on nopeasti kasvava fintech-yhtiö, jonka liikevaihto ja maksuhommat paahtavat kovaa vauhtia ylöspäin.

Kannattavuus on tviitin mukaan vain hetkellisesti paineessa skaalautumisen takia, mutta liiketoiminnalla on vahva vallihauta ja lisäksi markkina tviittaajan mukaan hinnoittelee sen yhä hitaaksi peruskasvajaksi, vaikka riskiin nähden tuottopotentiaali on hänen mukaansa todella houkutteleva. ![]()

https://x.com/ValuationEdge_/status/1996570464072659043

2 tykkäystä