Crocs (CROX) is one of the world’s most recognized manufacturers of affordable footwear for men, women, and children, and most of us have surely seen someone wearing Crocs at some point. My goal is to spark discussion about this company, which is familiar to many in the form of its shoes, but perhaps not as an investment.

Crocs shoes are sold in over 90 different countries, and over 720 million pairs of shoes have been sold. The company’s sales are fairly evenly split between Direct-To-Consumer (DTC) sales and wholesale.

Link to the latest presentation from March 2021: https://s22.q4cdn.com/133460125/files/doc_presentations/2021/03/Crocs_NDR-Presentation_vFF-2021.02.28.pdf

HEYDUDE

What may not be familiar to everyone is that Crocs now owns the HEYDUDE shoe brand.

Crocs acquired the HEYDUDE shoe brand for $2.5 billion, financing this acquisition with a loan ($2.05 billion) and Crocs shares ($450 million). HEYDUDE also has a very strong brand and is popular with consumers. This can be observed, for example, on TikTok and Amazon. Incidentally, 7 of the top 15 best-selling shoes on Amazon are either HEYDUDE or Crocs shoes.

Below is what Crocs’ management had to say about HEYDUDE:

"With the acquisition of HEYDUDE, we are thrilled to add another high-growth, highly profitable brand to our portfolio," said Andrew Rees, Chief Executive Officer of Crocs. “We believe HEYDUDE’s casual, comfortable and lightweight products are aligned to long-term consumer trends and are a perfect fit for Crocs. We intend to leverage our global presence, best-in-class marketing and scale infrastructure to build upon HEYDUDE’s strong foundation and create significant shareholder value. We truly admire the business that founder Alessandro Rosano has built and are honored to welcome the HEYDUDE team to Crocs.”

HEYDUDE founder and Chief Executive Officer, Alessandro Rosano said, "We founded HEYDUDE in Italy in 2008, to develop comfortable, versatile and accessible footwear. We are proud of the brand we built and are honored to become a part of Crocs, a company perfectly positioned to take HEYDUDE to the next level. We have long admired the Crocs business and are excited to have them bring HEYDUDE’s comfort, craftsmanship, and style to consumers globally."

Crocs Executive Vice President and Chief Financial Officer, Anne Mehlman said, “HEYDUDE has experienced incredible growth in revenue and profits over the past few years. HEYDUDE is expected to be immediately accretive to our high revenue growth, industry-leading operating margins and earnings. We expect the combined business to generate significant free cash flow, enabling us to quickly deleverage while investing to support future growth. We are excited about the combination and are confident in our ability to deliver long-term shareholder value.”

When the HEYDUDE acquisition was announced, Crocs’ share price was above $130, and since then, the price has declined. Prior to this transaction, Crocs had aggressively bought back its own shares from the market, and the market liked this. However, own shares will no longer be bought back until the debt level has been sufficiently reduced.

What I like about both of these brands is that both products are customizable and can be made in any way cost-effectively. Management has also clearly indicated that they expect to make HEYDUDE sales more profitable once the products are included in Crocs’ distribution network.

Numbers

(Figures in thousands)

In 2021, the gross margin was 61.3% and the operating margin was 29.5%. These are, in my opinion, truly strong figures.

Q2 2022

Here is a link to the Q2 2022 press release: https://investors.crocs.com/news-and-events/press-releases/press-release-details/2022/Crocs-Inc.-Reports-Record-Second-Quarter-Revenues-Up-51/default.aspx

The company’s total revenue was $964.6 million, an increase of 50.5% compared to the same period in 2021. Such significant growth is due to the integration of HEYDUDE into the figures. Gross margin decreased slightly from 2021 figures, pressured by supply chain issues and exceptionally high air freight costs. Q2 gross margin was 51.6%.

The Crocs brand’s revenue was $732.2 million, growing 19.4% compared to 2021 figures, excluding currency exchange rate effects. Especially strong growth was seen in the EMEALA segment. Crocs’ digital sales accounted for 37.2% of revenue, compared to 36.4% in the previous year. 32.4 million pairs of Crocs were sold, an increase of 3.3 million pairs compared to Q2 2021. The Crocs brand’s gross margin was 57.7%.

HEYDUDE’s Q2 revenue was $232.4 million, an increase of 96% compared to 2021. This also exceeded Crocs’ management’s own forecasts for the HEYDUDE brand. 8.1 million pairs of shoes were sold. HEYDUDE’s gross margin was 32.4%. Management aims to improve this by integrating the products into Crocs’ distribution network. HEYDUDE’s digital sales accounted for 31.5% of total sales.

Forecasts were exceeded, but the share price fell by over 10 percent after the announcement because the 2022 EPS forecast was slightly lowered to a range of $9.50 - $10.30. Management justified this with uncertainty in consumer behavior due to inflation and the global economic situation.

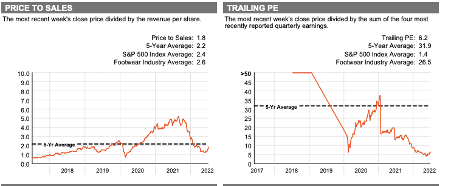

Valuation

I consider Crocs’ valuation to be very low; if management’s EPS forecast hits the lower end of the range, the FY22 P/E is below 8 at this price. Crocs guides for 2022 revenue to be between $2.545 billion and $2.615 billion. If Crocs hits the upper end of its 2022 forecasts ($2.615 billion) and their target for the Crocs brand’s 2026 revenue is $5 billion, this implies approximately 17% annual growth. The company thus offers good and profitable growth with just the Crocs brand.

I believe the reasons for this low valuation are fear of a recession and the large debt incurred from HEYDUDE. However, Crocs can repay the debt with the free cash flow generated by the company. One problem here is that the company will no longer buy back its own shares from the market until enough debt has been repaid. The company wants the gross leverage ratio to be below 2 (it was 2.6), after which they have communicated they will resume share buybacks.

Now I need the forum’s collective intelligence to understand why Crocs is valued at such low multiples and if I am falling into a value trap here. This was not a perfect introduction to the company, and there are certainly things I overlooked, but I hope to spark a discussion about this interesting company.