Minulla on käsitys, että edge on keskeinen osa alue Cloudflarelle, mutta en nyt siihen mene syvemmin. Ja toden totta, varmasti on paljon firmoja jotka ovat eri tuotteissa edellä.

Liiketoimintaa Cloudflare osaa johtaa. Laitan alle kuvaajan 12 kk jaksolla juoksevasta vapaasta kassavirrasta per osake. Osakesijoittaja haluaa nähdä sen juuri tuollaisena. Vaikka nettotulos on tappiolla, niin vapaa kassavirta merkitsee yhtiön arvostukseen nettotulosta enemmän.

Usein puhun, että Cloudflare tahkoo tasaista tulosta. Tarkoitan juuri mitä alla näkyy.

Tviittaja on tyytyväinen, miten Cloudflaren johto on tasapainottanut liikevaihdon kasvun ja kannattavuuden.

Vuonna 2022 markkinat vaativat enemmän kannattavuutta ja yhtiön johto ilmoitti silloin selkeästi, että he hidastaisivat liikevaihdon kasvua parantaakseen kannattavuutta.

Kaaviossa näkyy, että vapaa kassavirta ( ja operatiivinen kassavirta ovat vahvistuneet samaan aikaan, kun liikevaihdon kasvu on vastaavasti hidastunut.

Tämä siis osoittaa käsittääkseni tviittaajan mukaan yhtiön hyvää talouden hallintaa ja kykyä mukautua markkinoiden odotuksiin (onko aina paras ratkaisu kauemmas katsoen… )

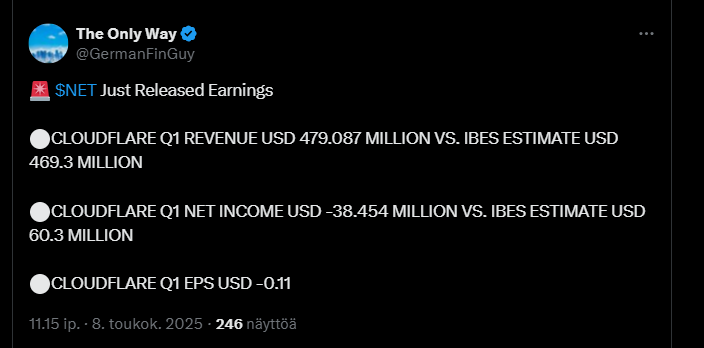

Alla on tviitti Cloudflaresta, joka on jokseenkin huomaamaton, mutta ilmeisesti voimakas toimija internetin infrastruktuurissa.

Se ei ole tviitin mukaan vain verkkoyhtiö tai kyberturvatoimija, vaan se mullistaa kuulemma tekoälyn käyttöönoton ja tietoturvan. Sen verkosto kattaa yli 310 kaupunkia mahdollistaen reaaliaikaisen tekoälyn ilman viiveitä. Tämä tuo tviittaajan mukaan sille merkittävän kilpailuedun ja tekee siitä keskeisen toimijan internetin seuraavassa kehitysvaiheessa.

Tuntuu aika hurjalle, eli BofA Securities nosti Cloudflaren suosituksen “osta”-tasolle ja tavoitehinnan 60 dollarista 160 dollariin. Kasvua tukevat heidän mukaansa AI-palveluiden vahva asema ja verkkoturvallisuusratkaisut.

Alla olevassa tviitissä kerrotaan, miten Cloudflare on ostanut kehittäjäystävällisen Outerbase-alustan vahvistaakseen tietokantatukea Workers-palvelussaan. Tavoitteena on helpottaa tekoälypohjaisten sovellusten kehitystä ja tukea ohjelmoijia ilman syvällistä SQL-osaamista.

Tässä toisessa saman tyypin tviitissä kerrotaan, miten Cloudflare on esitellyt Workers VPC:n ja VPC Private Linkin, joiden avulla kehittäjät voivat rakentaa turvallisesti globaaleja sovelluksia eri pilviympäristöissä.

Ratkaisut poistavat perinteisten VPC:iden alueelliset ja verkkotekniset rajoitteet sekä mahdollistavat yhteydet ulkoisiin järjestelmiin.

Cloudflare kertoi aloittaneensa vuoden vahvasti ja saavuttaneensa yhtiön historian suurimman yksittäisen sopimuksen, jonka taustalla on kehittäjille suunnattu Workers-alusta. Myös yhtiö solmi pisimmän SASE-sopimuksensa tähän mennessä, mikä vahvistaa sen asemaa kuulemma yritysasiakassegmentissä.

Näin on. Cloudflare on hyvä SaaS yhtiö sijoitajalle, koska yhtiön kasvu on erittäin tasaista; pikkasen liikevaihdon kasvu hiipuu, mutta 27% on edelleen hyvä tulos. Samoin marginaalit ja muutkin luvut ovat kvartaalista kvartaaliin kivan vakaita.

Alla olevaan tviittiin on koottu tulospuhelun tärkeimpiä kohtia. Tviitissä kerrotaan mm. se, miten tulosluvut olivat jo tiedossa, mutta tulospuhelu toi esiin siltikin kiinnostavia nostoja: Cloudflare solmi kaikkien aikojen suurimman, yli 100 miljoonan dollarin sopimuksen ja kasvatti merkittävästi suurasiakaskuntaansa.

Puhelussa kerrottiin myös, miten “myyntisyklit” lyhenivät, kilpailupaine keveni ja kassavirta pysyi vahvana. Fokus on nyt kurinalaisessa kasvussa ja kysyntävetoisissa investoinneissa.

Niimpä. Kellontarkasti yhtiö lisää asiakkaitaan, ja liikevaihto kasvaa suhteessa hieman kovempaa, koska vanhojen asiakkaiden NDR (net dollar retention) eli seuraavan vuoden ostot verrattuna nykyiseen on aina yli 100%, nyt taitaa olla luku 116%. Eli vaikka asiakkaita ei tulisi lisää, niin vanhoillakin saavutetaan 16% kasvu. Kun tuohon lisätään uudet asiakkaat, saadaan kaunis korkoa korolle efekti, kun kaikki tunnusluvat alkavat parantua kauniisti kiihtyen.

Olen pohtinut tuota yhtiön tasaista kehitystä. Arvioini asiasta on se, että yhtiö tekee paljon tuotekehitystä asiakkaiden tarpeiden mukaan, hieman perässä kysyntää vasten, eli hukkaa ei synny ja kaikki menee sitten luontevasti kaupaksi. Cloudflare on Cloudflare, tekee omaan duuniaan omalla tavallaan.

Cloudflare on lanseerannut “Pay per Crawl” -markkinapaikan.

Sen avulla verkkosivustojen omistajat voivat veloittaa tekoälyboteilta sivustonsa automaattisesta tietojen keräämisestä, määrittää hinnan tai sallia sen ilmaiseksi. He voivat myös estää tietojen keräämisen.

Jännä myös nähdä millainen kissa ja hiiri -leikki bottien ylläpitäjien ja Cloudflaren välille syntyy bottien tunnistamisessa, kun jatkossa datalla onkin hinta jos botti ei mene ihmisestä. Mutta tuo on kyllä jotenkin just tämän firman tyylinen ominaisuus. Ei tuone mitenkään merkittävää lisää bisnekseen sijoittajan näkökulmasta, mutta tukee tarinaa.

Kirjoitellaan tänne vähän kokemuksia Cloudflaren asiakkaana (ja tietysti myös omistajana).

Pääasialliset tuotteet joita käytämme lähinnä CDN / DNS / WAF / Zero Trust ja Workers cloudi lisäkilkkeineen.

Olen jo aikaisemmin tainnut komentoida ketjuun että Cloudflaren tuotteet ovat erinomaisia ja supportti on ollut ensi luokkaista. Supportin osalta paino sanalla “ollut”. Ei ole varsinaisesti enään.

Omat vastuut pääasiassa tuolla Workers hommien puolella. Tuotteet menevät mahtavalla vauhdilla eteenpäin ja ovat kohtuullisen yksinkertaisia käyttää, mutta ne myös muuttuvat sillä vauhdilla että turhanpäiväiseen ylläpitoon menee enemmän ja enemmän aikaa kun uusin versio tuotteesta x ei olekkaan yhteensopiva edellisen version kanssa. Samoin palveluiden saatavuudessa on alkanut olemaan enemmän ja enemmän katkoja ja pienempiä häiröitä jotka vaan usein kuitatataan hetkellisinä ongelmina.

Myös supportin osalta on vasteajat ovat kasvaneet ja kasvaneet vaikka olemme enterprise sopimuksen piirissä. Aiemmin viimeisenä oljenkortena ollut “kilauta account managerille” ei sekään näytä enää tepsivän.

En tiedä ovatko nämä vain hetkellisiä kasvukipuja ja sijoittajan kannalta posiitinen ongelma, vai yritetäänkö Cloudflarella harppoa vähän liian nopeasti eteenpäin. Palveluiden laatu pitäisi saada palautettua aiemmalle tasolle jos haluavat pitää nykyiset asiakkaat tyytyväisinä ja saada heidät siirtämään vielä enemmän liiketoimintaa cloudflaren alustalle.

Täysin ylihinnoitellulla osakkeella osavuosikatsaukseen. Ja mitä sieltä tulee: Liikevaihdon ja oikaistun osakekohtaisen tuloksen ylitykset sekä ennusteet mukavasti ylittävä Q3 ohjeistus. “Bisnekset rullaa eteenpäin kovaa vauhtia ja kysyntää riittää”.

Jälkimarkkinassa +5% (218$). Jos nousu toteutuu huomenna, osake sulkeutuu teknisesti ATH-lukemiin ja suunta jatkuu ylöspäin.

Nykytrendin mukaisesti, kun firma on AI, niin sijoittajan ei tarvitse olla PA

Uusimman osarin mukaan vanhan asiakaskannan uusostot näyttävät kasvaneen useamman vuoden laskun jälkeen, kuvassa ei näy lukemat, jotka ovat olleet aikaisempina vuosina jossain 120% tienoilla. Tuo S DBNR (alla) lienee yksi mittari asiakastyytyväisyydestä.:

Jep, hinnoittelu on ollut aina samanlaista Cloudflaren osalta. WallStreet tykkää yhtiöstä, omasta mielestäni seuraavista syistä:

100% SaaS yhtiö

Kellontarkkaa työtä kasvun ja tuloksen parantamisen suhteen. Vastahan rikkoontui vuositasolla 1 miljardin liikevaihto ja nyt rullaava liikevaihto on 2 miljardia.

Yhtiöstä puuttuu syklisyys. Karhumarkkinassakin 2022 ja 2023 yhtiö kasvoi 30-40% välillä.

tekee positiivista kassavirtaa ja vahva tase.

Lisäksi on uuden SW maailman yhtiö eli disruptoi

Q2 vahvisti em. asioita, vaikka kasvu olikin vain 28%. Mutta markkina ei koe 28% kasvua negatiivisesti.