Det hittar man snabbt på Google och enkelt på Nordnet, men för att underlätta:

https://www.marketscreener.com/quote/stock/BETSSON-B-58602255/consensus/

Uppdateras enligt mig ganska snabbt, åtminstone på screenern.

Det hittar man snabbt på Google och enkelt på Nordnet, men för att underlätta:

https://www.marketscreener.com/quote/stock/BETSSON-B-58602255/consensus/

Uppdateras enligt mig ganska snabbt, åtminstone på screenern.

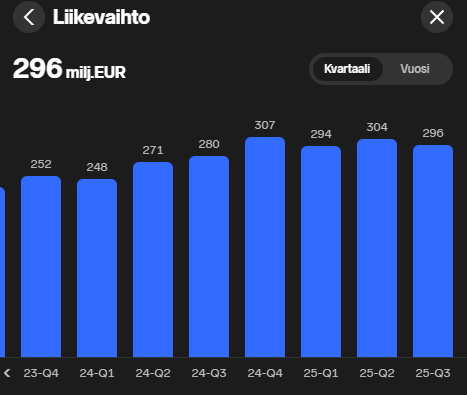

Vinstvarning från Betsson. Q4-intäkter 304m mot Factsets konsensusprognos på 318,4m (källa X). Det verkar inte ha varit inprisat i kursen ännu, då den är -13 % i skrivande stund ![]()

Var tvungen att trippla en position som gått med förlust. Med dessa rörelsevinstmultiplar blir det billiga alltså ännu billigare, och jag tror inte direkt att spelandet kommer att upphöra i världen än.

Med hänvisning till föregående kommentator också, kolla på jämförelseperioden (307 m€) och de nu rapporterade 304 m€. För ett år sedan stod aktien nästan 20 % högre än nu med i princip samma resultat. Det svider.

Här är en bra diskussion om Betsson-aktien. Själv ägde jag Betsson för ett tag sedan, men när Sverige gick över till en licensmarknad började Betssons resultat att försämras (trots att ledningen på förhand hade uttalat sig positivt om licensmarknaden). Är det någon som kommer ihåg den här tiden mer i detalj, och har ni funderat på vad som händer när Finland står inför samma övergång?

Det ser inte så ut. Det verkar dock som att mitt eget tålamod med den här aktien håller på att ta slut, även om det har gett bra utdelning och jag fortfarande ligger bra på plus.

Om man ser förbi sommarens fotbolls-VM och vilket resultat det ger, så kan det hända att min och Betssons gemensamma resa tar slut och att det bara återstår en kundrelation.

Var tvungen att sälja resten av mina kvarvarande Bittium för att tanka mer i den här. Min gamla position hade inte sjunkit till förlust än, den var bara ”bara” +70 %, men värderingen är ju återigen helt löjlig för ett bolag som i praktiken printar pengar. Man får förstås vara tålmodig med den här, nuvarande +70 % var vid något tillfälle i storleksordningen +240 %.

Får se om någon snart försöker röka ut Pontus igen, förmodligen med lika ”goda” resultat som senast.

Resultattappet var ganska kraftigt, EBIT 70 → 53 MEUR. Det finns flera förklarande faktorer. Den mest oroande av dem är förstås den rena vinstminskningen, då omsättningen i allt högre grad består av reglerad verksamhet och den reglerade delens marginal är tydligt lägre på grund av beskattningen.

Samtidigt meddelades det dock att omsättningen under början av året var en procent högre än i fjol, vilket å andra sidan är en bra situation då fjolårets omsättning för första kvartalet låg på en bra nivå.

Maskinen maler fortfarande på och genererar pengar, men resultattillväxten för det här året ser ut att sitta hårt inne.

Efter gårdagens kursfall till följd av vinstvarningen började jag titta närmare på bolaget först nu, och jag blev överraskad av Nordens lilla andel (12 %) av bolagets omsättning (Q3/25). Om Finland representerar till exempel 20–25 % av den andelen, tror jag inte att det kommer att ske några särskilt betydande förändringar i hela bolagets omsättning eller resultat därifrån.

Nordens inverkan på företagets omsättning har i själva verket rasat på några år, då andelen av omsättningen under Q4/23 och Q1/24 fortfarande låg kring 18–19 %. Tillväxten verkar för tillfället komma från Västeuropa och Latinamerika. Och samma utveckling har fortsatt i Q4/25.

Betydande kostnader verkar ha tillkommit genom företagsförvärv, bland annat i form av ökade personalkostnader. I Q3-rapporten var antalet anställda 2 800, jämfört med 2 350 året innan. Vid utgången av Q3 var siffran 2 900, mot 2 450 året innan. Man kan tänka sig att om resultatnivån sjunker permanent, kommer överlappande roller att rensas bort. Effekten var enligt gårdagens varning ca 7 miljoner euro under Q4.

En annan del av det försämrade resultatet beror på ökade skatter med ca 10 miljoner euro, vilket enligt bolaget beror på en rekordhög andel (68 %) på reglerade marknader. Detta ser jag personligen som en normal affärskostnad som man måste leva med.

Jag blev lite förvånad när jag bläddrade i Q3-rapporten över att bolaget har två obligationer som inte är särskilt billiga med något mått mätt: Euribor 3 månader + 4,6 % (71 miljoner euro, löptid 9/26) och Euribor 3 månader + 3,25 % (99 miljoner euro, löptid 9/27). När kassan uppgick till 394 miljoner euro känns det märkligt att behålla sådana räntekostnader. Kan det vara så att pengar i den här branschen generellt sett är dyrare än ”normalt”? En ny obligation på 75 miljoner euro är på väg ut med Euribor 3m + 2,75 %, så räntekostnaderna lär sjunka något när den dyraste obligationen byts ut mot en billigare.

Inderes bolagssida visar nu ett P/E-tal på 7,03. Jämfört med historiska värderingsmultiplar är det inte särskilt billigt, men i förhållande till den omgivande marknaden börjar det kännas tryggt. Jag försökte leta lite efter konkurrenter också, men hittade inget motsvarande hos andra företag. Varför har Betsson tilldelats så låga multiplar?

Utöver det rikliga utdelningsflödet pågår även återköp av egna aktier för 40 miljoner euro för att utveckla kapitalstrukturen. Är inte makulering också en del av att utveckla kapitalstrukturen? Har Betsson haft för vana att makulera dessa tidigare?

Detta som en inledande reflektion skriven som ett “stream of consciousness”, utifall att man orkar börja sätta sig in i bolaget mer noggrant. Taggen som svar på grund av det första stycket. Frågorna riktas till en bredare skara, ifall det finns forumanvändare här som har följt bolaget under en längre tid.

Nu när rörelseresultatet sjunker med ca 25 % från föregående år, kan man fortfarande tänka att Betsson har ett P/E på 7? Även om kursen föll med drygt 20 %, steg värderingen kanske till och med om man tror att denna svaghet fortsätter på samma sätt genom hela 2026. Själv tror jag inte på detta, men det skulle inte förvåna mig om svagheten fortsatte i ytterligare ett kvartal till. Det finns ju fler anställda även om tre månader jämfört med för ett år sedan, och man investerar nog också mer än tidigare. Kommer rörelseresultatet att vara trögt tills fotbolls-VM drar igång? Trumps utspel kan påverka Betsson negativt om riskerna realiseras, eftersom det redan har hörts tal om bojkotter. Om länder faktiskt skulle utebli från mästerskapet kan fotbolls-VM bli en total pannkaka och det skulle satsas mindre pengar.

Betsson börjar dock se ut som ett ganska lockande alternativ i mina ögon. Jag kanske plockar upp en liten post om raset fortsätter i början av veckan.

Resultatet var helt enligt prognoserna baserat på vad jag hittade efter en snabb googling. Förväntningarna var revenue 304 milj och ebit 53 milj

Edit. Inte så konstigt då det redan fanns förhandsinformation om detta![]()

Lönade det sig att köpa denna till aktiesparkontot (OST) med redemption share-upplägget, eller blir det dubbelbeskattning även där?