CEO Jaakko Sinnemaa discussed with Frans immediately after the Q3 business review. (Q3: 1.4.2025-30.6.)

Topics:

00:00 Start

00:11 Q3 summary

01:21 Extra maintenance fees and rental income

02:48 Earnings level and other one-off costs

04:32 Opportunities when no new apartments are under construction

05:51 Occupancy rates and market

07:37 Effects of the removal of housing benefits

08:57 Transaction volumes in Finland

10:24 Tallinn sales

Tässä on vielä Fransilta uusi yhtiöraportti Asuntosalkusta Q3:n jäljiltä. (Q3: 1.4.2025-30.6.)

Asuntosalkku’s Q3 review was slightly subdued in terms of figures, but clearly profitable apartment sales in Tallinn continued. The company has allocated these funds to share repurchases, which, with the current clear balance sheet reduction, we believe is value-creating activity for shareholders. We made small negative forecast changes based on the review. In the short term, sluggish cash flow is a key challenge, but share repurchases compensate for the low cash flow yield. The share price has been rising, but we still see the current valuation (2025e: P/NAV 0.70x) as an attractive level for further purchases, as we believe the housing sector is gradually moving towards a better cycle. We reiterate our ‘add’ recommendation and our target price of 92 euros.

Quoted from the report:

Yield-based analysis

In the yield-based analysis, we apply the EBITDA/EV method, which considers both operating profit and balance sheet structure. We forecast Asuntosalkku’s operating EBITDA to be EUR 8.6–9.0 million for fiscal years 2025–2026, which corresponds to an EBITDA/EV yield level of 3.8–3.9%. This remains below Kojamo’s and Balder’s average level of 4.3–4.4%, and the valuation appears tight. Considering net debt, the equity value is EUR 73/share. Applying Kojamo’s and Sato’s valuation multiples, the value would be EUR 56/share, which, together with high interest costs, limits the upside potential in the short term.

Asuntosalkku’s NAV discount is currently 28.6 percent at a share price of 85 euros, whereas in the last analysis in April it was 39 percent. For the company’s large peer, real estate investment company Kojamo, the corresponding NAV discount is currently 26.7 percent at a share price of 10.7 euros, whereas in April it was at the same level as Asuntosalkku. Kojamo’s occupancy rate improved to 93.6 percent in the summer, but is still clearly lower than Asuntosalkku’s occupancy rate in Finland, which was 98.2 percent in June.

Subheadings:

Operating business without sales generated zero profit

Profitable sales in Tallinn continued in July

Two risks removed

Prices in the Helsinki metropolitan area have decreased – transaction volumes have increased

Share buybacks seem wise

Short-term outlook and valuation

Note.

IR Window is a channel for corporate partners of SalkunRakentaja and Sijoittaja.fi for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

Major entrepreneur Jüri Käo states the matter directly.

We have hit rock bottom.

In Estonia, properties and forest plots are now being sold, often in a hurry and at a low price. However, no new investors are coming in their place, as attracting them is increasingly difficult.

In the current geopolitical situation, real estate and other fixed assets are a dead zone for investors, says real estate developer Jaanus Juss.

Frans is pre-gaming as Asuntosalkku reports its H2 results on Thursday.

Comparably, we expect net rental income to have remained stable, even though reported revenues decrease due to the harmonization of Estonian financial years. We do not yet expect the full benefit from falling interest rates to impact the result, which is why we estimate cash flow and adjusted earnings to remain low. We estimate changes in fair values to be very moderate after the declines in recent reports. The most interesting aspects of the report will be the new guidance, the progress of Estonian housing sales, and the development of the average interest rate on loans.

Here are Frans’s quick comments on Asuntosalkku’s H2 results.

Asuntosalkku published slightly better-than-expected H2’25 results. Comparably, net rental income remained stable, even though reported revenues decreased due to the harmonization of Estonian financial years. The decrease in interest rates materialized slightly better than we expected, and cash flow and profit developed slightly better than we expected, although they remained relatively low. Fair values also developed slightly positively and better than we expected after the declines in previous reports. The guidance was slightly better than we expected and points to a steady next year and opportunities to continue profitable apartment sales in Tallinn.

Frans interviewed Asuntosalkku’s CEO Jaakko Sinnemaa regarding H2.

Topics:

00:00 Introduction

00:12 Development during the review period

01:12 Development of average rents

03:25 Occupancy rates in Finland

04:48 Economic situation in Estonia

06:36 Fair values

07:59 Dividend proposal and share buyback

11:03 Realization of interest rate decline

12:48 Guidance and sale of apartments in Tallinn

Here is the update report. For those familiar with the company, H2 did not bring major upheavals, as is usually desirable for a residential real estate investment company Operational performance was slightly better than expected. The guidance for realized profit was quite strong, but it’s difficult to estimate how much of it includes profitable sales in Tallinn, which are expected to continue. Unless I have misjudged the balance sheet value, the situation is indeed interesting, as the company is able to sell apartments above valuation figures and buy back its own shares. In the short term, the impact of this is limited due to low liquidity, but in the long term, I believe this is a significant factor, and liquidity will likely strengthen if the stock remains at its current level and my thesis proves correct. Of course, I also don’t see why a tender offer aimed at the top 100 largest owners, similar to Lemonsoft, wouldn’t be possible.

In the case of Asuntosalkku, it is good to note that even though the NAV discount is so significant, I perceive the company’s investment profile more as a steady, low-risk residential real estate investment, which unfolds through share buybacks and apartment sales, and thus a gradual increase in valuation. In my opinion, a faster increase in valuation is still limited by low cash flow, Finland’s weak rental and housing market, and the low valuation levels of peers (especially Kojamo).

Positive signals for the future include Tallinn’s functioning sales market and the company’s profitable operation in the market, shrinking financing costs, as well as a decreasing inventory of ready, unsold apartments in the domestic market.

Subheadings:

Asuntosalkku published its fourth-quarter results for the fiscal year

Reported result close to zero – realized profit clearly positive

Profitable sales in Tallinn make the stock interesting

Market situation is expectant

Investor’s focus on the future

NOTE.

IR Window is a channel for corporate partners of SalkunRakentaja and Sijoittaja.fi for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

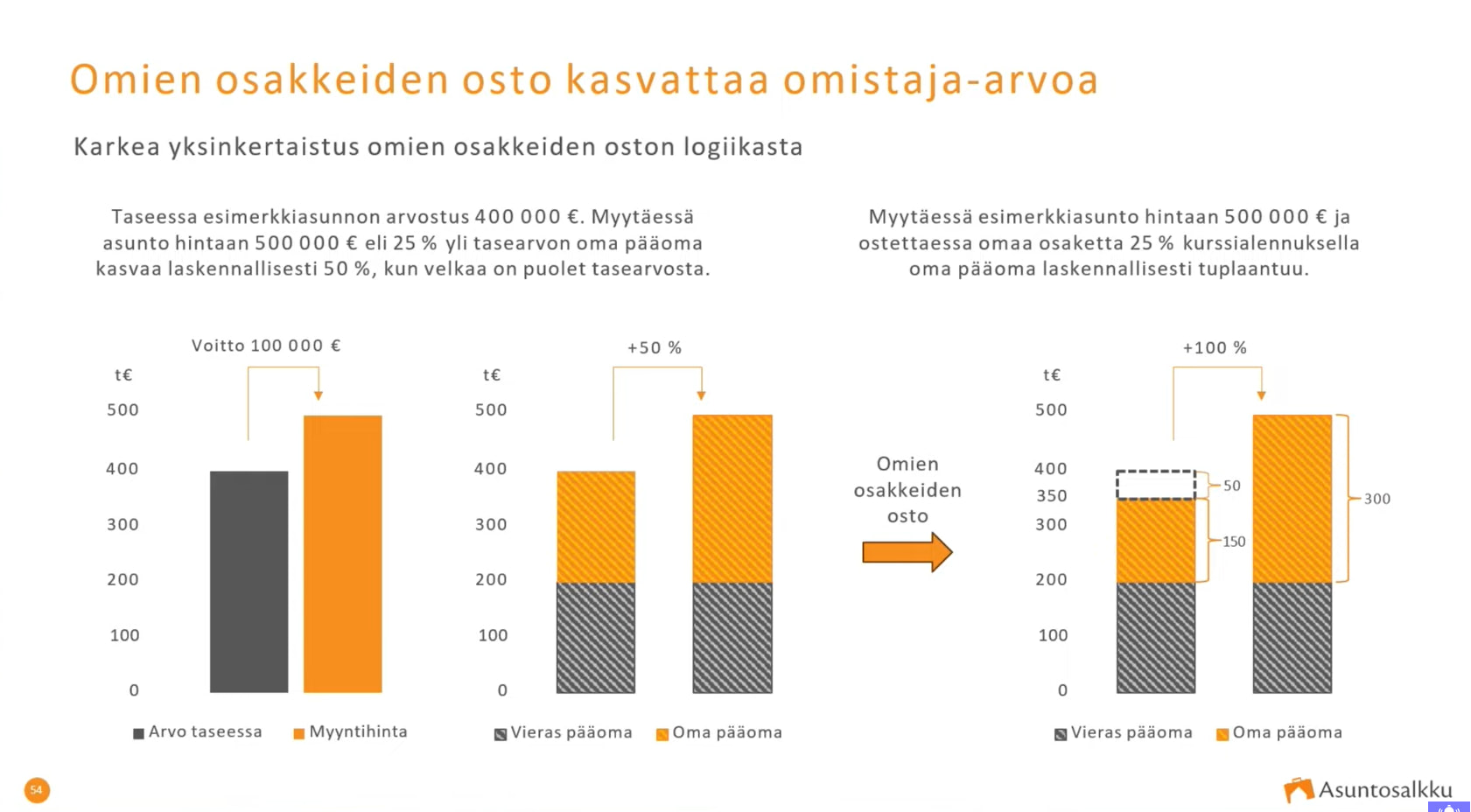

@Sijoittaja-alokas’s linked presentation included a good simplified illustration from the company on the impact of share buybacks in the real estate sector. In practice, currently, when buying its own shares, the company is buying its own apartments below their book value. Simple, yet beautiful. Once we reach larger volumes and get proof of the marketability of Finland’s housing stock, the equation looks excellent.

Here is also a link to the Real Estate Evening panel discussion. The themes of the housing sector included, among others:

Why has Finland’s housing price development still been the weakest in all of Europe, even though interest rates have been falling for quite some time now and our interest rates are variable?

Finland’s housing benefit system has been very generous, but now the support system has already been clearly tightened. How much has the Finnish housing market relied on the generous support system, and will these deteriorations cause long-lasting weak development on top of the already observed weak development?

How and when will the oversupply of rental apartments in the Helsinki metropolitan area be resolved?

Why does Finnish capital seem to be largely absent from the real estate market, even though one might imagine it’s currently quite a good buyer’s market?