Eipä ollut bingokortissa, että tällaisestakin asiasta syntyy vastaväitteitä.

Eli mielestäsi ei ole epäeettistä Helsingin kaupungilta, siis julkiselta sektorilta, myydä kuluttajille asuntoja, ilman kunnollisia taustatietoja ja käyttää hyväksi asemaa julkisena (luotettavaksi koettuna) toimijana?

Oli tai ei, se toinen, merkittävämpi asia. HeKa on julkista asuntotuotantoa, ja toiminnan rahoitus tulee verovaroista ja maksetuista vuokrista suoraan tai välillisesti. Se että nyt HeKa joutuu kattamaan hoitokuluja ja rahoituskuluja valmistuneiden yhtiöiden yli 100:sta tyhjästä asunnosta, tulee lopulta myös verovaroista ja asukkaiden selkänahasta. Miksi ihmeessä näitä asuntoja ei siis OIKEASTI yritetä myydä. Julkiset varat tehokkaassa käytössä jne.

Täysin irrelevanttia mikä on itsestäänselvää kenellekin. Miksi ilmoituksella edes ylipäätään ilmoitetaan tehdyt remontit, kun pitäisi olla itsestäänselvää, että 80-luvun yhtiössä ei ole putkiremonttia tehty? Ja näkeehän sen kuvistakin millainen katto yhtiössä on tai asunnon pinnat ovat. Ei varmastikaan tarvitse erikseen ilmoittaa minä vuonna pintaremontti tai kylpyhuoneremontti on tehty. Jos nyt vielä jäi epäselväksi, nämä myynti-ilmoitukset ovat aivan ala-arvoisia, ei siis ihme että asunnot ovat myymättä.

En ole eri mieltä siitä että pitäisikö tästä tulla seuraamuksia, huomautan vain että niitä seuraamuksia ei valitettavasti tule. Helsingin kaupunkiin kannattaa suhtautua äärimmäisellä varovaisuudella, etenkin asunto- ja palkka-asioissa.

EDIT: myös Etuovi/Oikotie -akseli voi olla vaikea polku käydä palautteen kanssa. On tietty mahdollista että maailma on muuttunut, mutta aiemmat kokemukset keskusteluista on ollut sitä että näitä toimijoita kiinnostaa ensisijaisesti se kuinka paljon (turhiakin) klikkauksia ostetut ilmoitukset saavat. Jos käyttäjänä koetat ehdottaa esim. parempaa filtteröintiä tai tiukempia sääntöjä ilmoitukseen, palaute otetaan varmaan vastaan ystävällisesti maksamattomien asiakkaiden palautekäsittelyyn - eli silppuriin.

Toivotan vilpittömästä onnea ja menestystä jos koetat saada Helsingin kaupungin, Etuoven ja/tai Oikotien toimimaan eettisesti oikein.

Kun satuit löytämään tontin osuuden, niin sattuiko silmääsi samalla mitään tietoa vuokrasopparista? Itse kävin esitteet läpi ja mitään muuta en löytänyt kuin vuokran hinta nyt.

Koska vuokrasopparia ei ole saatavilla, siinä lienee jotain piiloteltavaa. Tämä voisi selittää asuntojen liikkumattomuuden täysin.

En itse asiassa katsonut sen tarkempaa. Olettaisin ilman parempaa tietoa, että on luokkaa 50v soppari, jossa indeksitarkistukset normaalisti. Mielestäni hinnasto/vastike-esite oli päivätty elokuun tiedoilla. Vuokran jälkeen hoitovastikkeeksi jäi 4€/m2, joka mielestäni melko neutraali (voi olla hieman alakanttiin). En siis usko, että on sen isompaa koiraa haudattuna tuohon vastikkeeseen.

Omalta osaltani kohteesta ajattelen, että en olisi valmis ostamaan noilla hinnoilla kerrostaloasuntoa noilta sijainneilta.

Ei tässä nyt mistään seuraamuksista ole kyse ;DD vaan siitä että jälleen julkisella rahalla tehdään asiat silmät kiinni, vasemmalla kädellä ja kädet kaverin taskuissa, eikä omissa. Veronmaksajat kiittää jälleen ylimääräisistä korkokuluista ja menetetyistä tuloista, kun kaupunki ei edes yritä myydä asuntoja.

En rehellisesti ymmärrä mistä vedät johtopäätöksen, että tavoitteena olisi tämä

Tilastokeskukselta uutta dataa vanhojen omakotitalojen hinnoista.

Tilastokeskuksen mukaan vanhojen omakotitalojen hinnat laskivat koko maassa 9,5 % vuoden takaisesta ja 6,1 % edellisestä vuosineljänneksestä heinä-syyskuussa 2025. Vanhojen omakotitalojen kauppoja tehtiin 2,6 % enemmän kuin vuotta aikaisemmin.

Tällä kertaa hintoja painaa yli 100.000asukkaan kuntien markkinat:

Yli 100 000 asukkaan kunnissa vanhojen omakotitalojen hinnat laskivat 10,9 %.

“Tilastokeskuksen ennakkotietojen mukaan vanhojen osakeasuntojen hinnat laskivat koko maassa 2,4 % edellisestä vuodesta lokakuussa 2025. Edelliseen kuukauteen verrattuna hinnat pysyivät samalla tasolla. Hinnat laskivat vuoden takaisesta kaikissa suurissa kaupungeissa. Hintojen lasku oli suurinta Espoossa (-6,6 %) ja Vantaalla (-6,4 %).”

Oulussa lievää arvostustason muutosta luvassa, kun yliopisto ilmoitti halunsa muuttaa OYSin viereen toiselle puolen kaupunkia.

Nykyisellä kampusalueella Linnanmaalla on huomattava määrä opiskelija-asuntoja, kovan rahan (opiskelija-)asuntoja ja palvelut ovat hyvässä kunnossa.

Aiemmissa suunnitelmissa ratikkalinjan olisi pitänyt tulla OYSin ja Linnanmaan yliopistokampuksen välille, mutta Oulun ”johtavat” poliitikot ovat vahvasti ampuneet suunnitelmat alas.

Jos kampus jää tyhjäksi ja purkavaa uudisrakentamista nähdään, niin ratikan kanssa alueella olisi vielä varsin hyvät muotoutua arvonsa säilyttäväksi alueeksi. Muuten voi olla nähtävissä varsin tiukkaa arvostuksen laskua, kun tuhannet opiskelijat ja lähialueilla asuvat työntekijätkin miettivät mahdollisesti sijaintiaan uudestaan.

Kymmenen vuoden rakentamisen projekti on edessä ja muutos lienee varsin hidas, mutta päätösten jälkeen ensivaikutukset nähtäneen pian.

Onkohan Suomessa vastaavasta esimerkkejä? Mittakaava lienee sitä kokoa, että keskussairaalan, yliopiston tai ehkä kokonaisen AMK:n siirron vaikutukset olisivat vertailukelpoisia. Oulussakin on aiemmin nähty AMK:n osien siirtymistä, kuten myös yliopiston osien, mutta ei näin suuressa mittakaavassa aiemmin.

Lähinnä mieleen tulee pienemmässä mittakaavassa Savonlinna, jossa koulutuspaikkoja ja sairaalan tehtäviä on vähennetty. Sairaala roikkuu vielä ilmeisesti löysässä hirressä. Siinä luonnollisesti vuokra-asujat (opiskelijat) niiden myötä. Ei näin pikkutunneilla jouda penkoa syvemmälti, mutta maikkarin vanhahkosta (2021) uutisesta saa tuntumaa:

Siinä lähti iso osa opiskelijoita ja henkilöstöä. Savonlinna on siinä mielessä epätyypillinen kaupunki, että se on kohdannut näin ison iskun, joka kohdistuu nimenomaan korkeakoulutettuihin ihmisiin.

Isku näkyy katukuvassa. Pois lähteneet käyttivät aktiivisesti esimerkiksi kulttuuripalveluja.

– Tämän seurauksena Savonlinnassa on nyt purettu vuokra-asuntoja, jotta ylitarjontaa saataisiin vähennettyä ja asuntomarkkinat terveemmiksi, Siltanen sanoo.

Vuoranantajien tietopankista ainakin voisi löytyä tilastoja, joista ilmenee konkreettista vaikutusta vuokra- ja asuntomarkkinaan.

Napakka 12min video(englanniksi) siitä mistä lähdettiin ja mihin on tultu asuntojen hinnoissa ja miksi.

Lähtötasolta jossa asunnon hinta on alle 3x maan mediaaniansion on tultu tasolle jossa hinta ylittää monin paikoin jopa 10x tason. Miten se vaikuttaa koko talouteen kun ihmisillä ei ole vara muuttaa alueille missä on töitä tarjolla tai miten se vaikuttaa ihmisten käyttäytymiseen on tietää ettei omaan asuntoon tule koskaan olemaan varaa. Lopussa myös ratkaisuehdotuksia hintojen nousun hillitsemiseen, kavvoituksesta sijoittajat ulos rajaaviin ostorajoituksiin asti.

Verkkouutiset lainannut hesaria, luulen että alkuperäinen uutinen maksumuurin takana.

Asuntojen neliöhinta on pudonnut vuodesta 2022 vuoteen 2024 euromääräisesti selvästi eniten Uudellamaalla, peräti 433 euroa

Koko maassa neliöhinnasta hävisi HS:n mukaan kahdessa vuodessa keskimäärin hieman yli 200 euroa.

Reaalihinnoissa olemme koko maan tasolla noin vuosituhannen alun tasolla. Pääkaupunkiseudulla reaalihinnat ovat noin vuoden 2008 tasolla, Keskinen sanoo.

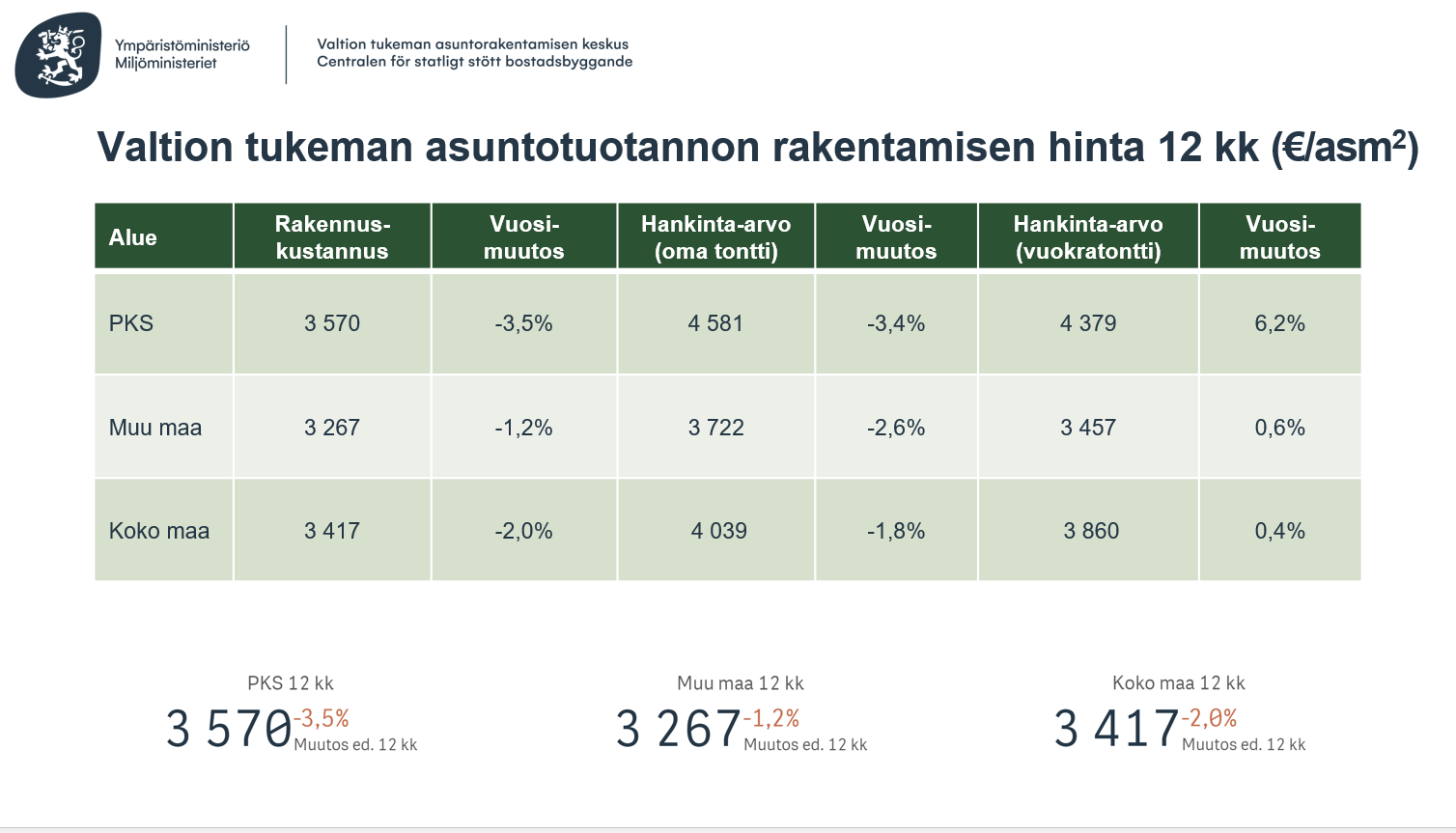

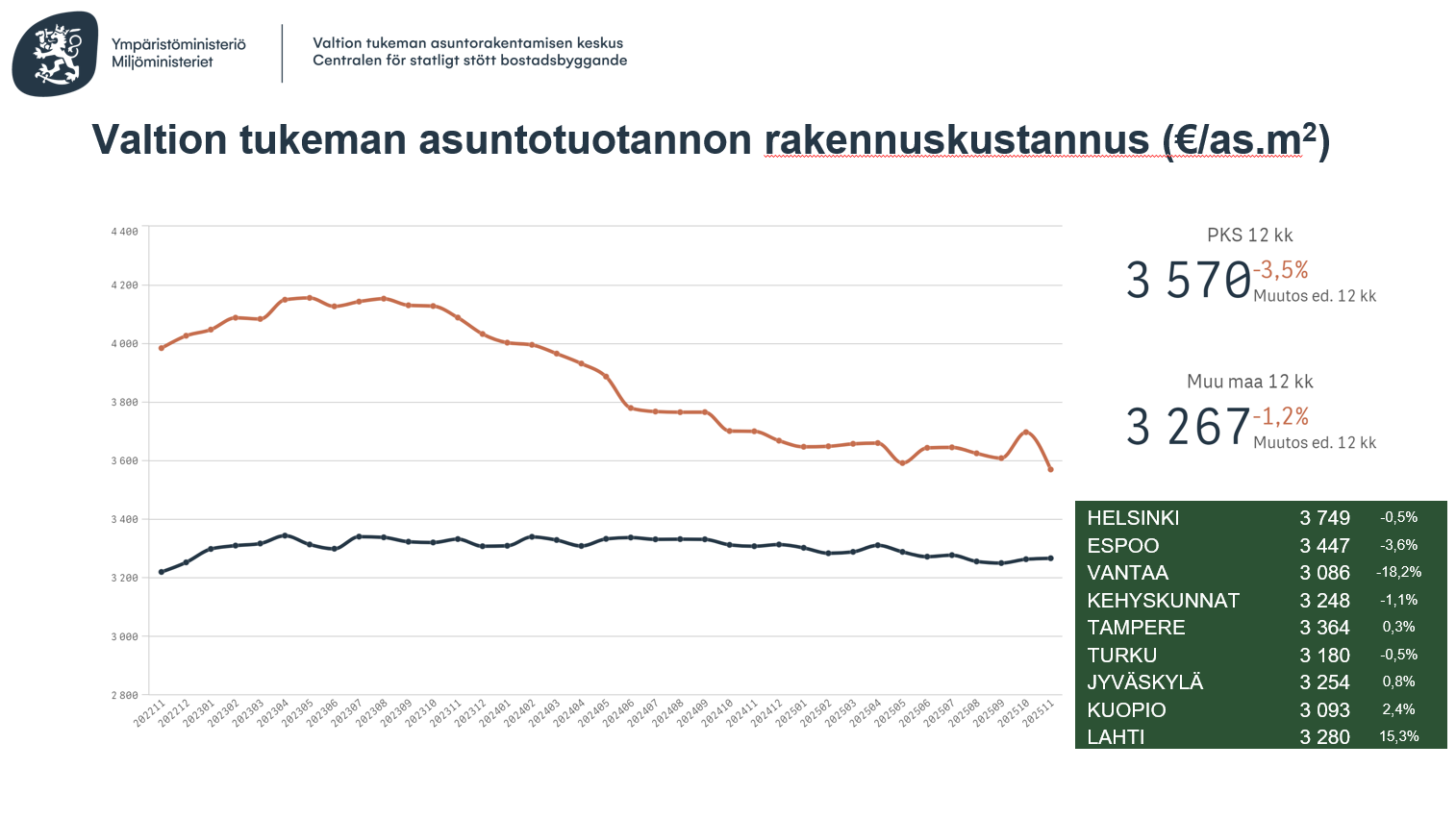

Asuntojen rakentamisesta on tullut hirvittävän kallista. Hesarin jutussa keravalaisen vuokratalon rakentamiskustannus oli 3093 euroa/neliö ja Jätkäsaaressa 4446 e/m2. Ja tämä hinta ei tietenkään sisällä tonttia.

Kutistuvien maakuntien Suomessa tämä tarkoittaa että uusien kerrostalojen (ja muidenkin talotyyppien) rakentaminen on kannattavaa ainoastaan kasvukeskuksissa. Ja siellä taas ne ovat todella kalliita kun huomioi rakennuskustannukset, kalliin tonttimaan ja kovan rahan hankkeen katteet.

Samaan aikaan puuhataan kallista ”tunninjunaa” ja radanvarren kunnat laskeskelevat että rataan käytetyt eurot saadaan takaisin kaavoittamalla tonttimaata uusien asemien ympäristöön. Kallista tulee kun homma tehdään rahan kerääminen edellä. Aikaisemmin kunnat yrittivät sentään kaavoitushankkeita joiden tavoitteena oli saada kuntaan ns. hyviä veronmaksajia, nyt tavoitteena vaikuttaa olevan vain tonttimaan arvon maksimointi.

Pääkaupunkiseutu näyttäytyy ihan älyvapaana muiden kustannusten osalta. VARKE tuotannossa hankinta-arvon ja rakennuskustannusten ero tulee liittymis- ja autopaikoituskustannuksista ja maapohjankustannuksista(omalla tontilla tontin hinta, vuokratontilla rakentamisaikainen tonttivuokra). Pääkaupunkiseudulla rakennuskustannukset ovat keskimäärin 81% hankinta-arvosta vuokratonteilla ja 78% omilla tonteilla. Muu maa vastaavat ovat 95% ja 88%.

Pääkaupunkiseudulla on rakennettu aika paljon vanhoille satamille meren rannalla. Jos noi pitää sisällään maanmuokkauskuluja (puhdistus), perustukset (paalutus, meren läheisyys) ja infraan kytkemisen (kaukolämpö, keskitetty jätteiden kerääminen) niin ei kai ero ole yllättävä? Päälle vielä keskimäärin korkeammat ja tiiviimmät alueet jotka tuskin ovat halvempia rakentaa…

Maanrakennuksen kustannukset ovat sisällä rakennuskustannuksissa. Liittymismaksut esim kaukolämpö, vesi ja sähkö ovat yksi osa-alue mikä ei sisälly rakennuskustannuksiin VARKEn tilastoissa. Aika tyypillisesti liittymismaksut ovat 1-2% luokkaa koko hankinta-arvosta. Autopaikoitus varmaan on yksi iso tekijä. Halliin rakennettuna autopaikoitus voi kustantaa tuohon eriteltynä about saman kuin tontti ja liittymismaksut yhteensä. Ehkä pääkaupunkiseutua enemmän muualla rakennetaan autopaikoitus katoksiin.

Laitetaanpa tämä tännekin. Esitys käsittelee tosin kiinteistöalaa yleisesti eli ei vain asuntoja. Kesto 27 min.

Aiheet:

00:00 Transaktiovolyymi Suomessa

01:18 Kv-sijoittajien osuus ostoista

02:37 Liiketilat ja hotellit vaihdetuin tilatyyppi

09:58 Vapaan toimistotilan määrän kasvu

11:17 Useampia isoja toimitilahankkeita käynnissä pk-seudulla

13:03 Eri tilatyyppien Prime-tuottovaatimukset

19:50 Asuntorakentaminen on historiallisen matalalla tasolla Suomessa

20:45 Pk-seudun vuokrakehitys jäänyt Tampereen ja Turun vauhdista

23:04 Kiinteistöjen ja korkojen välinen yield gap

24:59 Ammattimainen kiinteistösijoitusmarkkina

26:09 Suhdannekäyrä