AppLovin Corporation on yhdysvaltalainen mobiiliteknologiayritys, joka tarjoaa alustoja sovelluskehittäjille markkinointiin, analytiikkaan ja mainosansaintaan. Vuonna 2025 yhtiö ilmoitti kuitenkin luopuvansa pelinkehitystoiminnastaan ja keskittyvänsä mainosliiketoimintaan. AppLovin listautui Nasdaqiin vuonna 2021.

Yhtiö tarjoaa ohjelmistopohjaisen siis alustan sisällöntuottajien ja mainostajien markkinointiin ja kaupallistamiseen globaalisti. Yhtiö toimii kahdella liiketoiminta-alueella: mainonta ja sovellukset. Sen tuotteisiin kuuluvat muun muassa AppDiscovery-mainosalusta, MAX-huutokauppateknologia, Adjust-analytiikkatyökalu sekä Wurl, CTV-alusta suoratoistosisällön jakeluun ja mainontaan.

Lisäksi yhtiö tarjoaa SparkLabs-optimointipalvelua ja AppLovin Exchange -mainoshuutokauppaa. AppLovin kehittää myös ilmaispelejä ja palvelee sekä suuria että itsenäisiä kehittäjiä, mainostajia ja mobiilialan toimijoita.

Sijoittajan pohdintaa

AppLovin on kasvanut nopeasti johtavaksi toimijaksi mobiilimainonnan teknologiassa. Yhtiön tekoälypohjainen Axon-alusta ja ratkaisut, kuten MAX ja AppDiscovery tarjoavat mainostajille tehokkaita työkaluja kohdentamiseen ja tuoton optimointiin. Vahva taloudellinen asema ja kiinnostus strategisiin laajennuksiin, kuten TikTokin mahdollinen osto osoittavat sijoittajien mielestä aitoa kunnianhimoa ja kykyä tavoitella markkinajohtajuutta myös pelien ulkopuolella.

Toisaalta yhtiö on viime aikoina joutunut useiden shorttareiden kohteeksi, joissa syytetään sen mainosteknologiaa sääntöjen rikkomisesta ja käyttäjätietojen väärinkäytöstä. Näiden seurauksena osake on laskenut merkittävästi. Väitteet voivat heikentää luottamusta yhtiön eettisyyteen ja kestävyyteen, vaikka johto on kiistänyt väitteet ja käynnistänyt tutkinnan.

AppLovinilla on kovan luokan teknologiaa, sitten kasvupotentiaalia ja kunnianhimoa, mutta sitten tulee mieleen nämä kohonneet maine- ja sääntelyriskit. Läpinäkyvyyden ja luottamuksen säilyttäminen on nyt yhtiölle todella tärkeää, mutta kyllä epäilyttää shorttareiden innokkuus sekä nämä tietyt epäselvyydet.

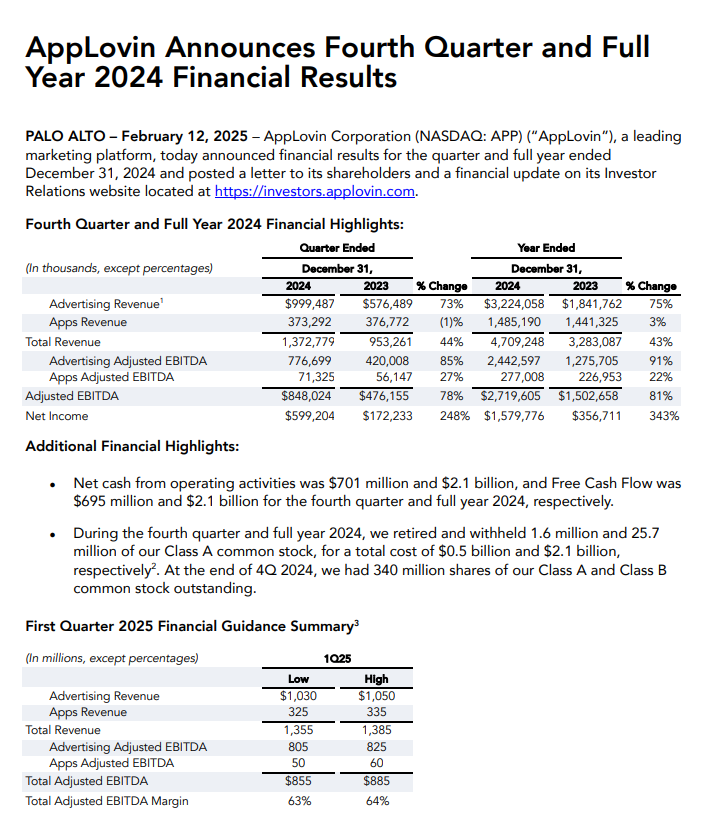

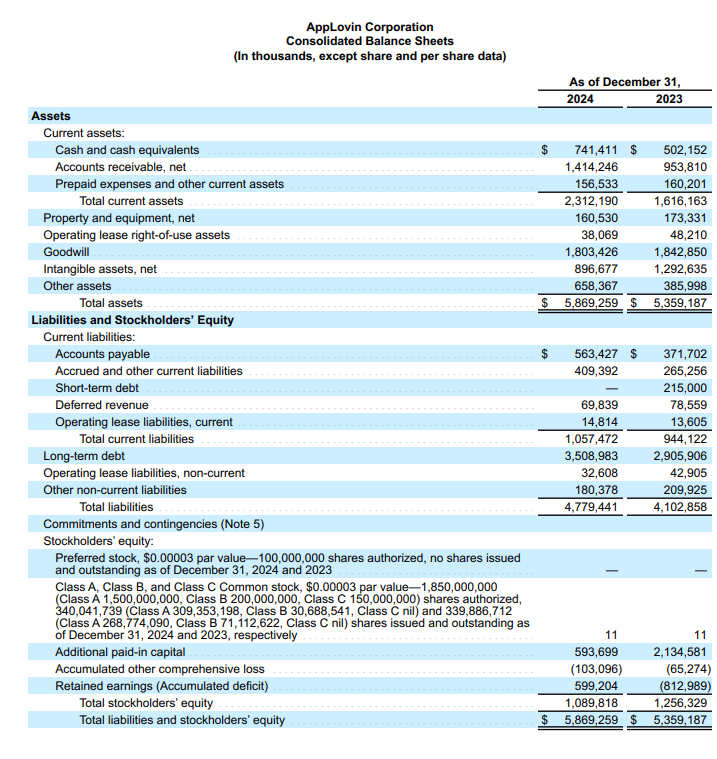

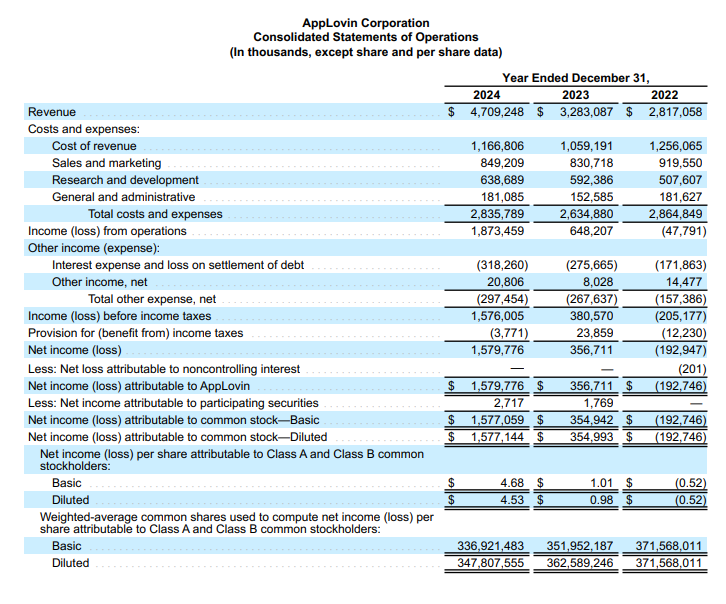

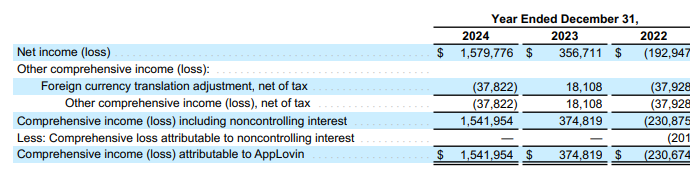

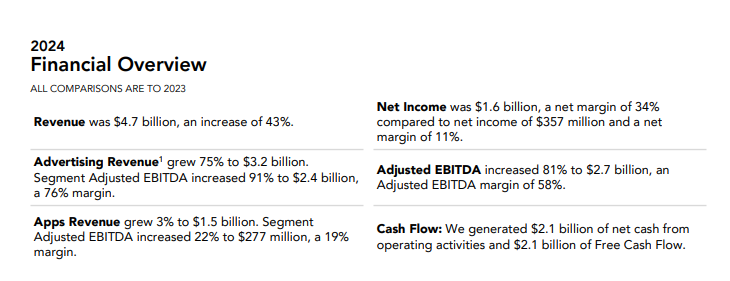

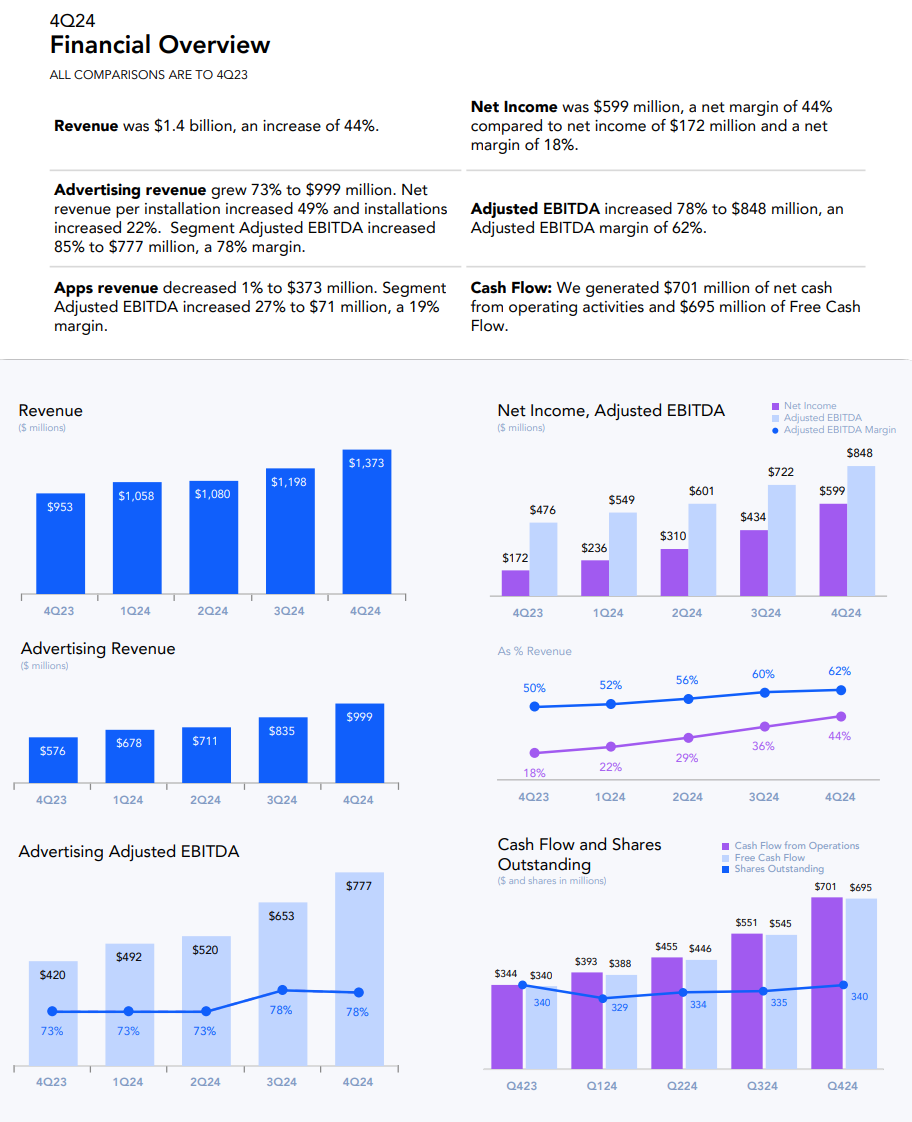

2024/Q4 ja vuosi 2024

| Tunnusluku |

Arvo |

| P/E-luku |

45,84 |

| ROA |

28,1 % |

| ROE |

134,4 % |

| Bruttokate |

75,2 % |

| Price/Book |

81,72 |

| EBITDA |

2,32 mrd. USD |

| EV/EBITDA |

39,55 |

| Markkina-arvo |

74,7 mrd. USD |

| Liikevaihto |

4,71 mrd. USD |

| EPS (osakekohtainen tulos) |

4,68 |

Tämän ketjun innoittajat:

Jackfinin haastattelu

Ja @Juha_Salminen

https://x.com/Ptjuhis/status/1908175058368958956

8 tykkäystä

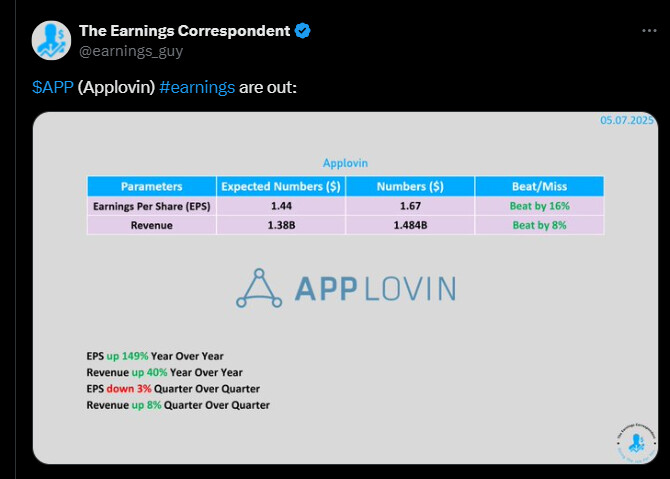

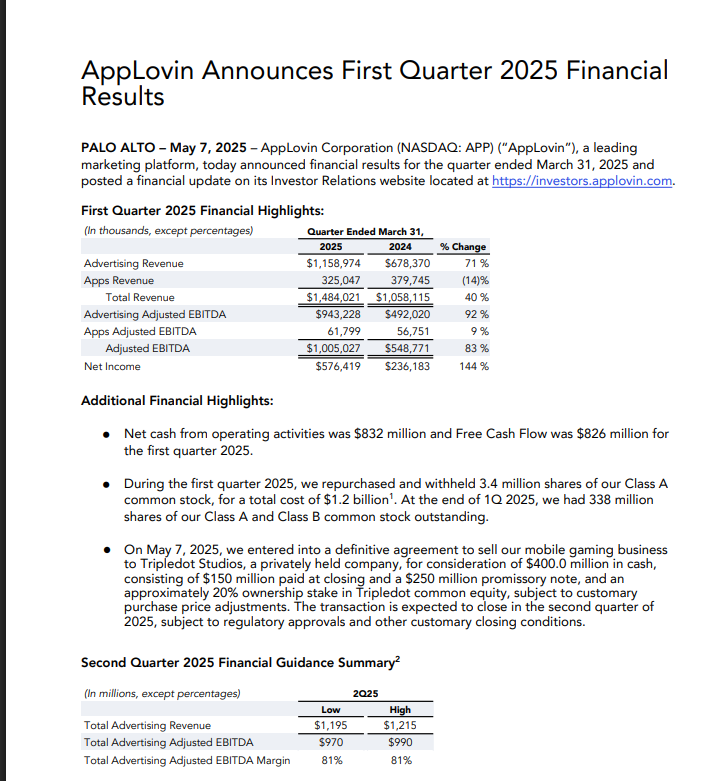

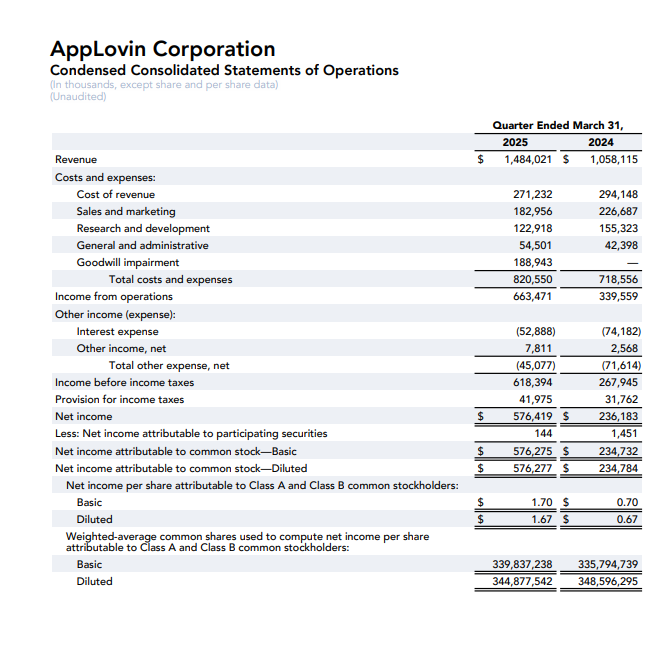

Yhtiö kertoi tuloksensa parantuneen ja liikevaihdon kasvaneen ekalla kvartaalilla

Applovin ilmoitti tehneensä sitovan sopimuksen myydä mobiilipeliliiketoimintansa jollekin yksityiselle yhtiölle. Vastikkeena se saa käteismaksun sekä merkittävän omistusosuuden ostavasta yhtiöstä. Kaupan odotetaan toteutuvan vuoden toisen neljänneksen aikana viranomaishyväksyntöjen ja muiden ehtojen täytyttyä.

AppLovinin mainosliiketoiminta kasvoi merkittävästi vuoden ensimmäisellä neljänneksellä ja yhtiö saavutti korkeat marginaalitkin mainosalustansa vahvuuden ansiosta.

Peliliiketoiminnan lasku jatkui, mutta sen tulos parani hieman. Yhtiö jatkaa strategista muutostaan kohti puhtaasti markkinointi- ja mainosteknologiayhtiötä. Vahva kassavirta mahdollisti mittavan omien osakkeiden takaisinoston, mikä osoittanee luottamusta tulevaan kasvuun.

https://x.com/earnings_guy/status/1920209893774000278

4 tykkäystä

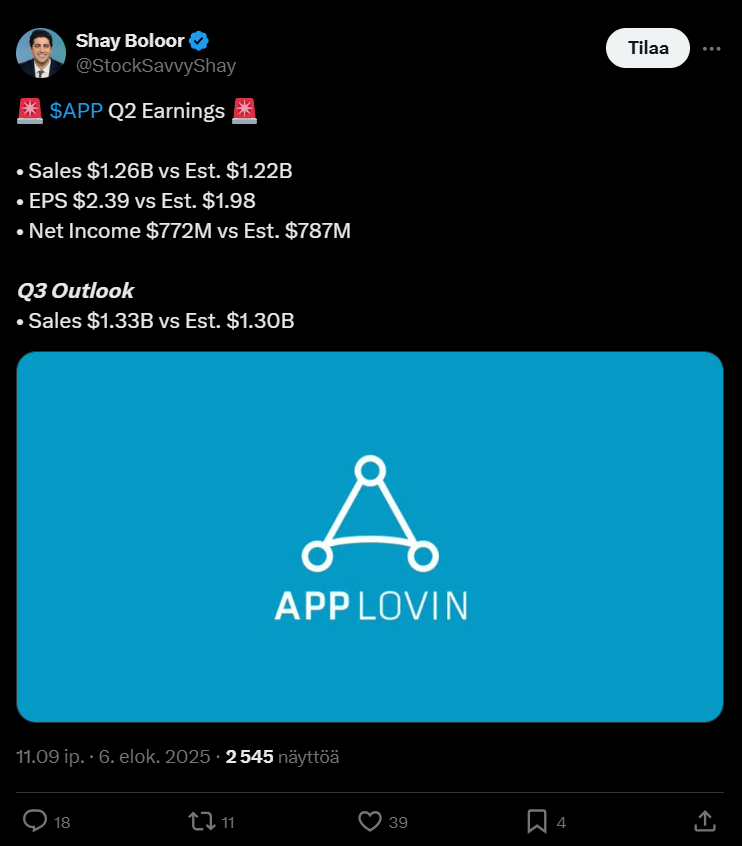

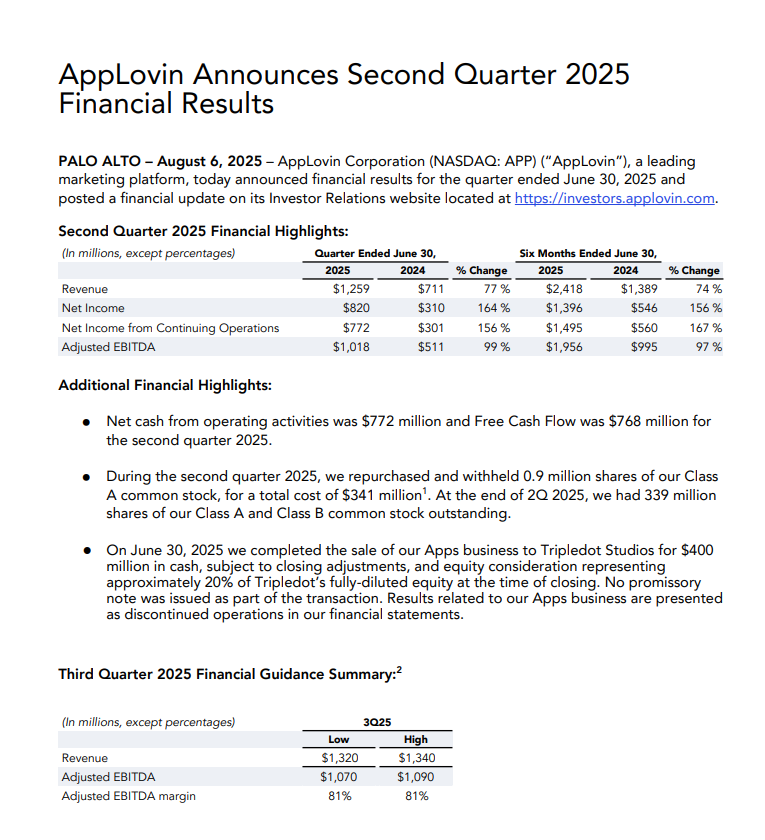

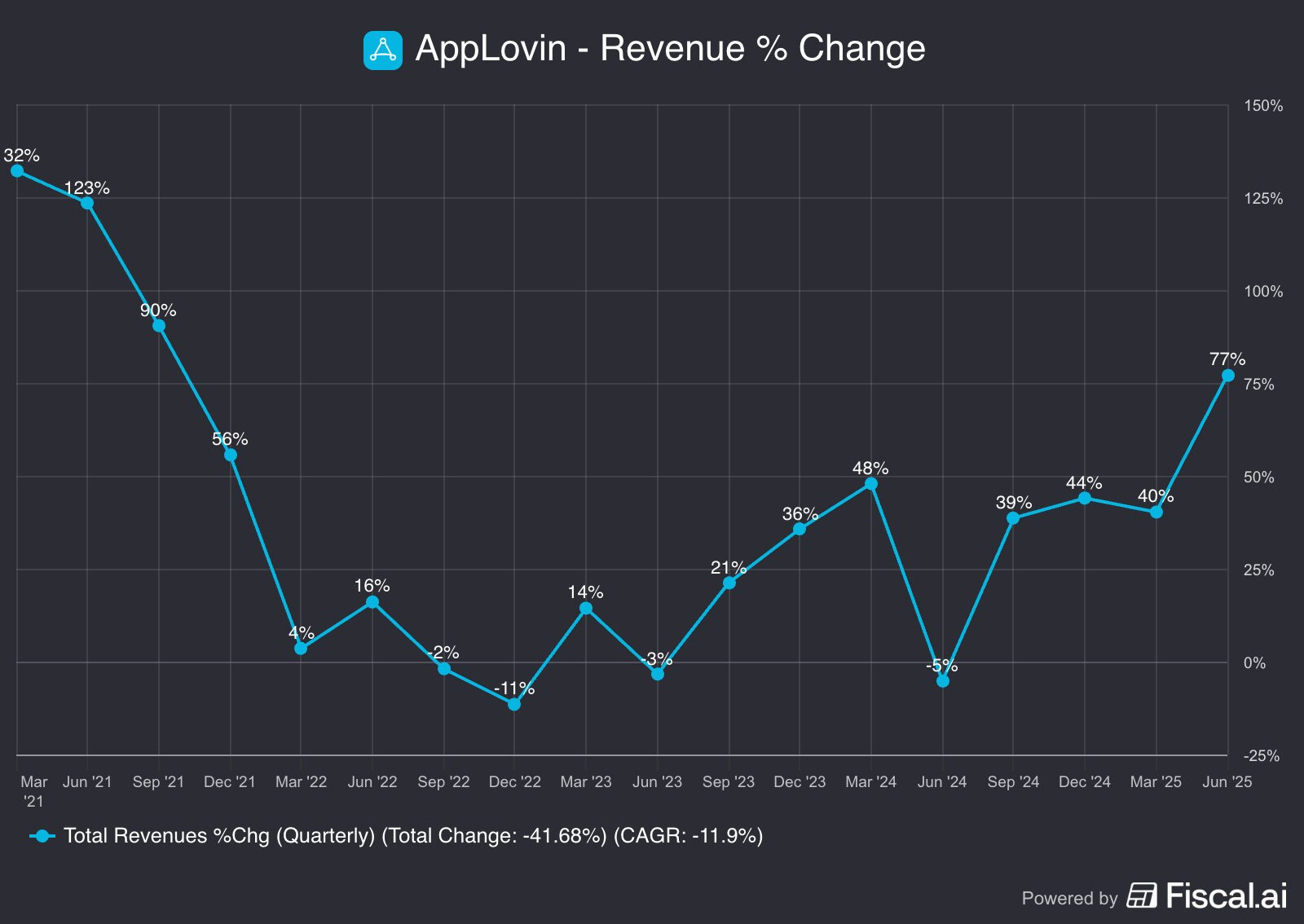

AppLovin raportoi kovasta kasvusta vuoden tokal kvartaalil; liikevaihto nousi 77 prosenttia ja nettotulos peräti 156 prosenttia vuoden takaisesta.

Yhtiö myi sovellusliiketoimintansa Tripledot Studiosille 400 miljoonalla dollarilla ja keskittyy nyt ihan täysillä mainontaan.

Yhtiön kannattavuus on hyvässä kunnossa esimerkiksi oikaistu käyttökate kasvoi lähes kaksinkertaiseksi ja kassassa on massia yli miljardi dollaria. Tulevaisuuden näkymät ovat kuulemma lupaavat, sillä Q3:lle odotetaan lisää kasvua ja hyviä katteita.

https://x.com/StockSavvyShay/status/1953186585803145404

AppLovin nappasi paikan S&P 500 -indeksistä Robinhoodin rinnalla. Yhtiön kurssi pomppasi uutisen jälkeen ja sijoittajat ovat nyt entistä kiinnostuneempia yhtiön menosta sekä meiningistä.

1 tykkäys

Applovinin kassa pullistelee ja historia kertoo heidänkin olleen kohtuullisen aktiivinen M&A markkinalla. Luopunut pelinkehitysliiketoilinnasta ja fokusoituu adtechiin. Mielestäni ajan kysymys, milloin Applovin saattaisi siirtää katseet Verven buy-outiin. Villi spekulaatio.

2 tykkäystä

Alla on tviittimuodossa jonkun poiminnat AppLovinin johdon höpinöistä.

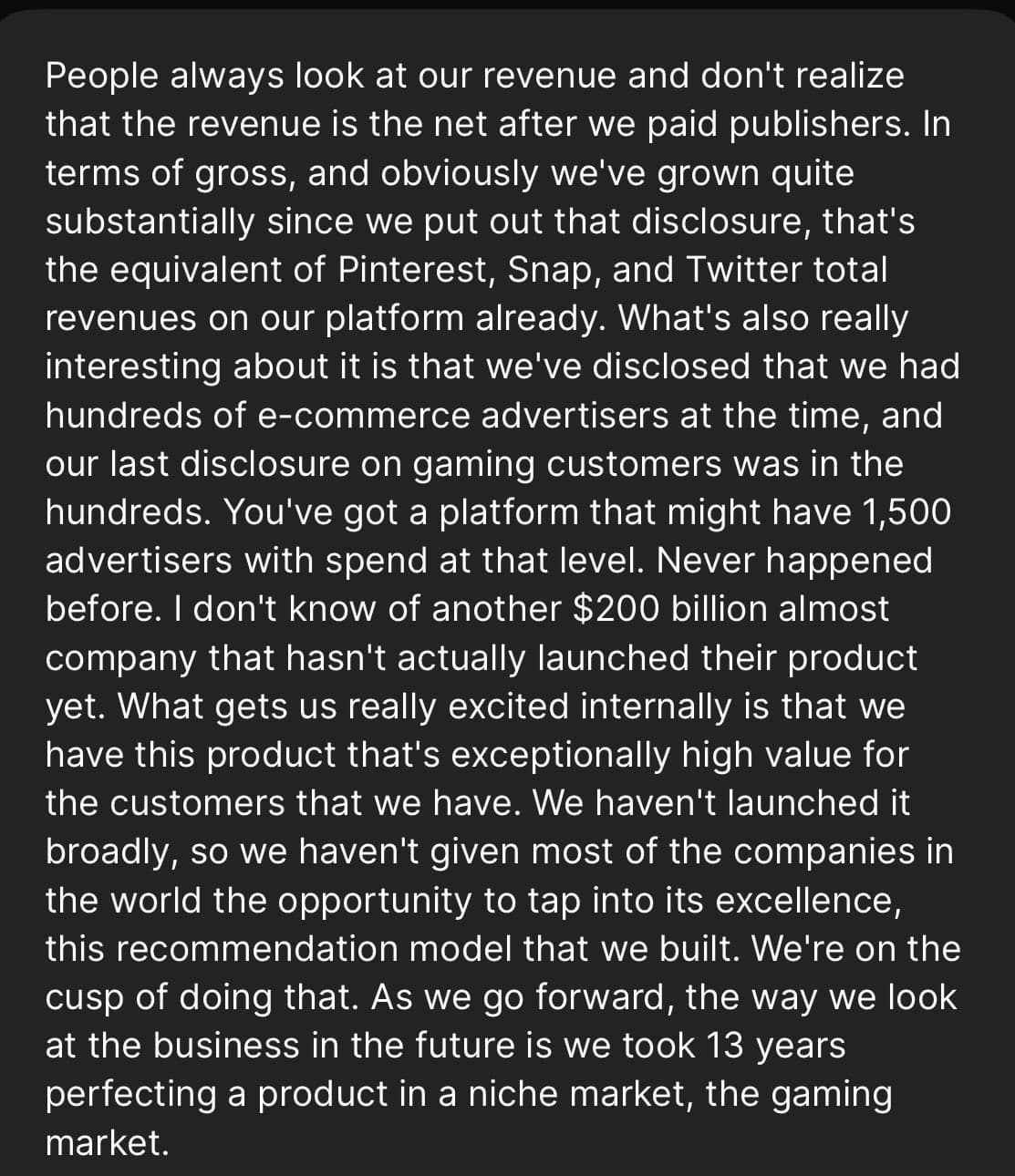

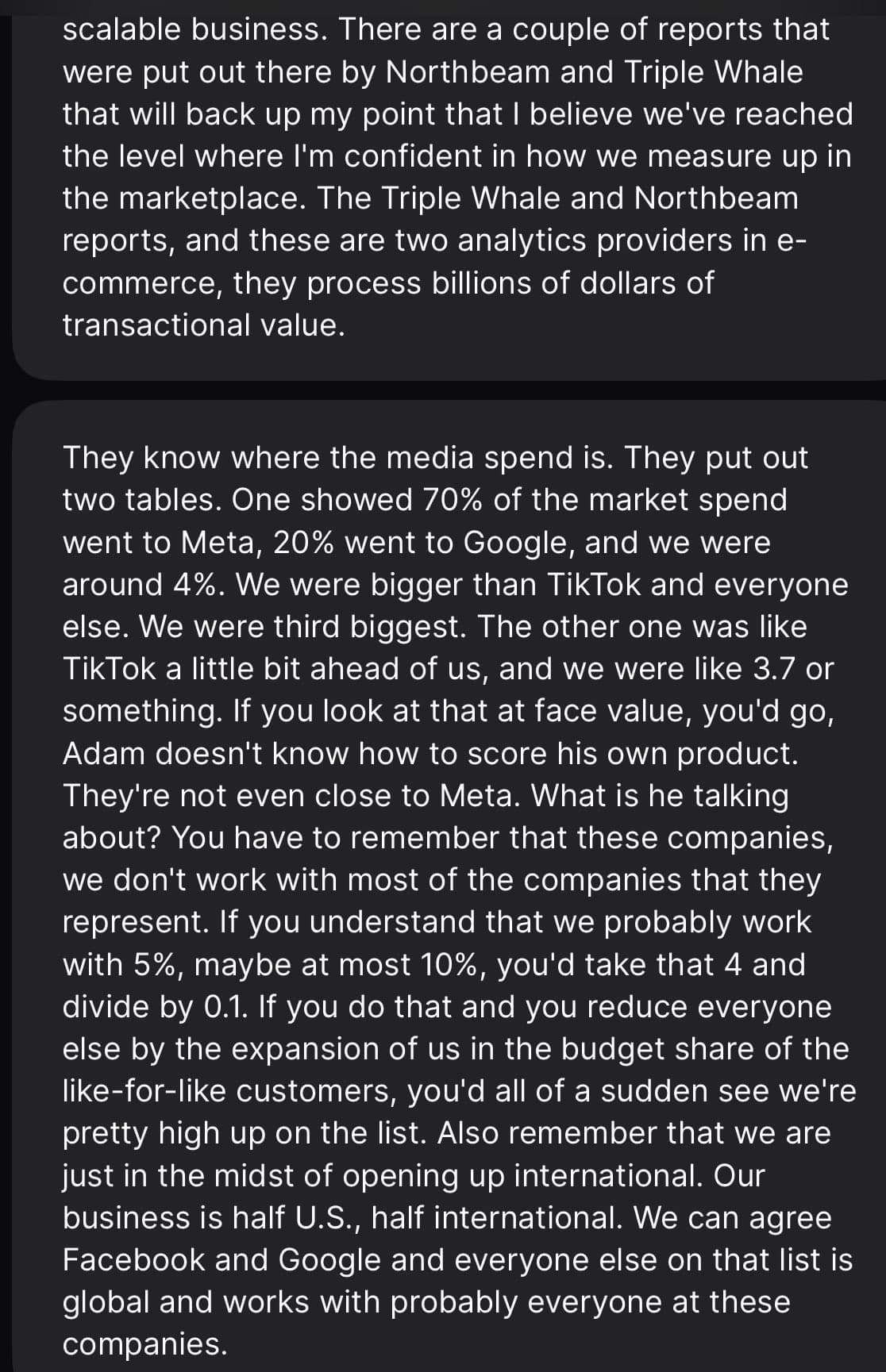

AppLovinin johto korosti konferenssissa vahvaa kasvua ja laajaa mainostajakuntaa erityisesti pelialalla. Yhtiöllä on tuhansia asiakkaita ja uusi “suositusmalli”, jota ei ole vielä laajasti lanseerattu, tarjoaa suurta lisäarvoa.

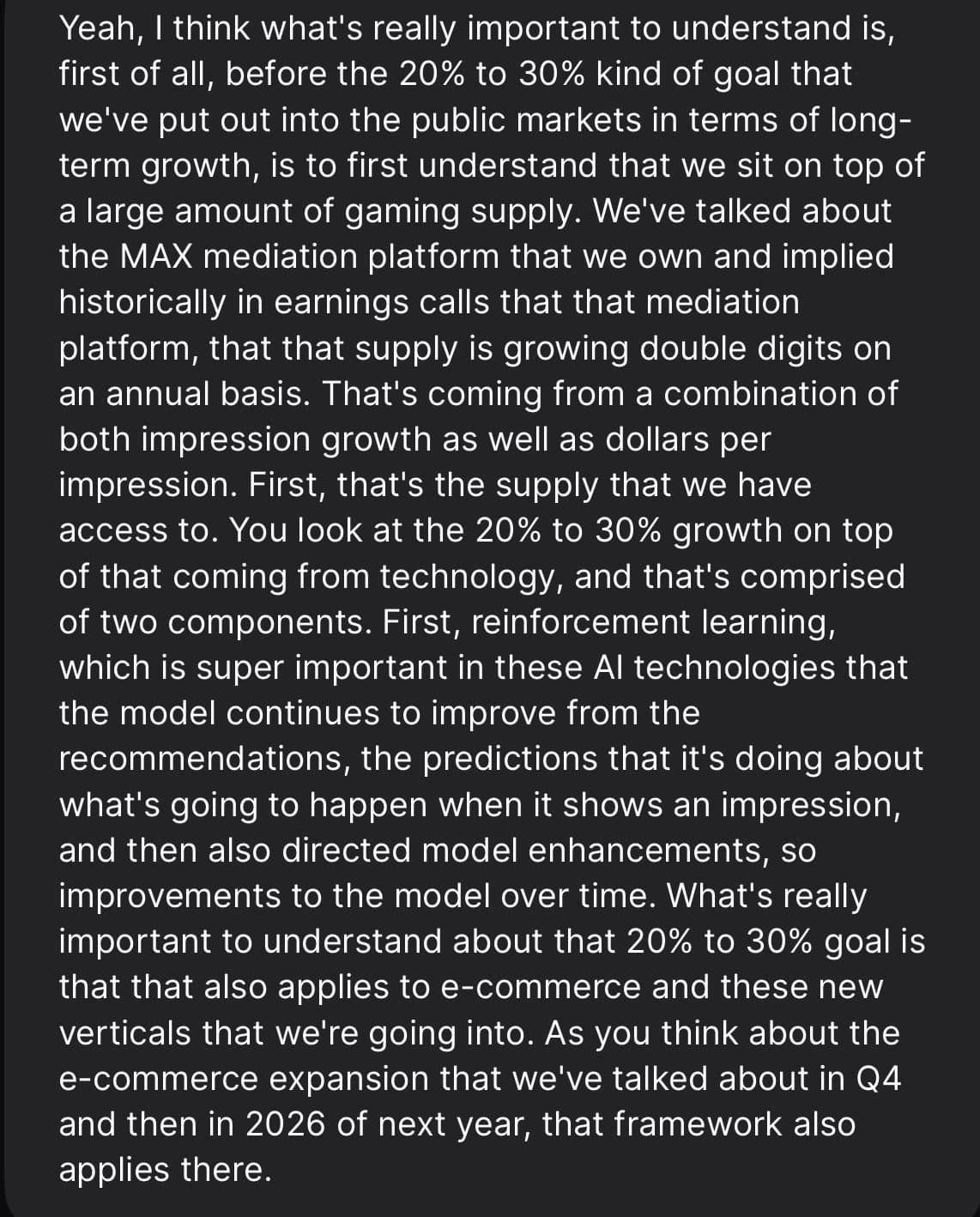

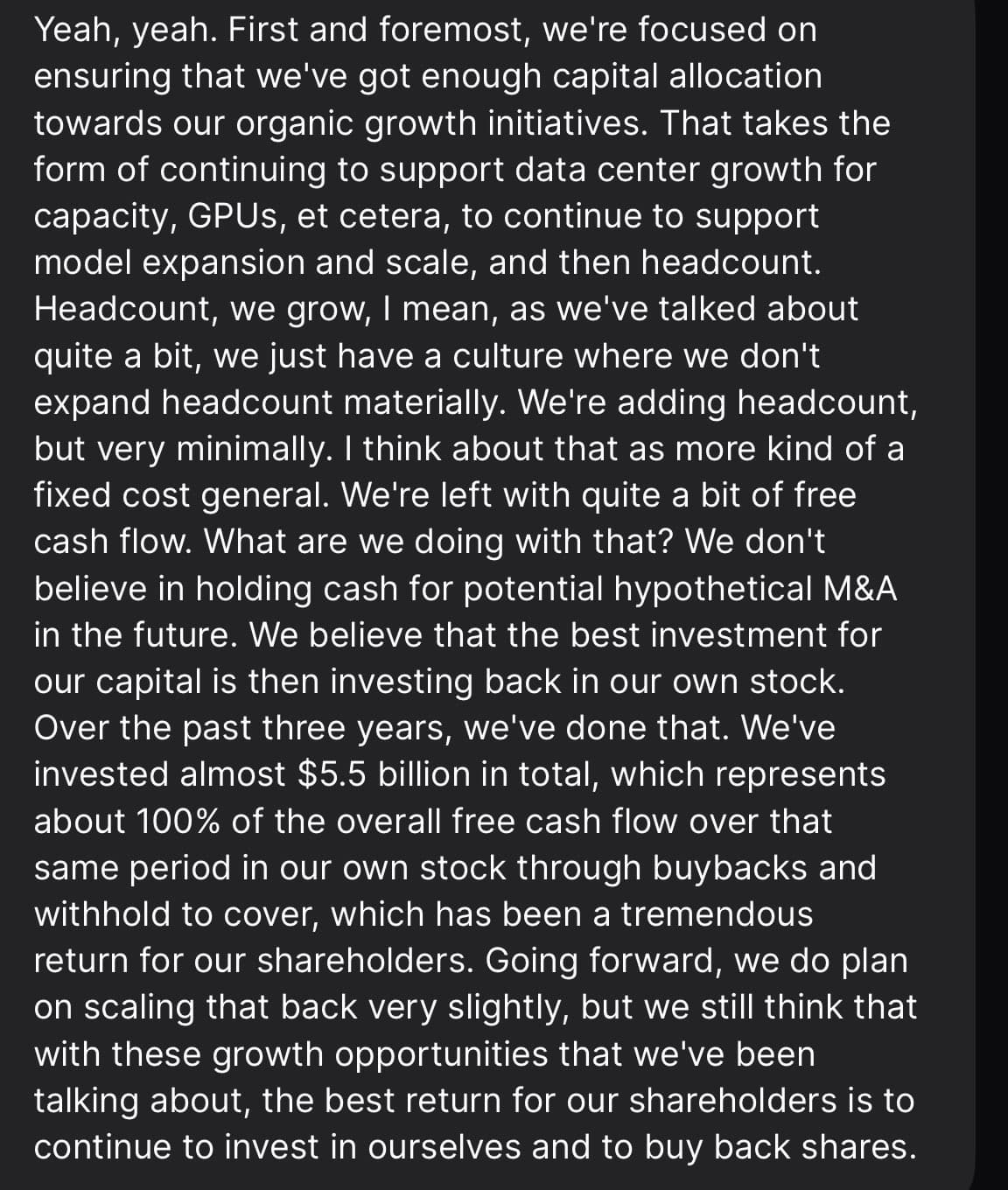

Tavoitteena on 20–30 prosentin vuosittainen kasvu, jota edesauttavat tekoälypohjaiset parannukset ja laajeneminen e-commerceen. Investoinnit kohdistuvat datakeskuksiin, GPU:ihin sekä omien osakkeiden takaisinostoihin, joihin on käytetty yli 5,5 miljardia dollaria.

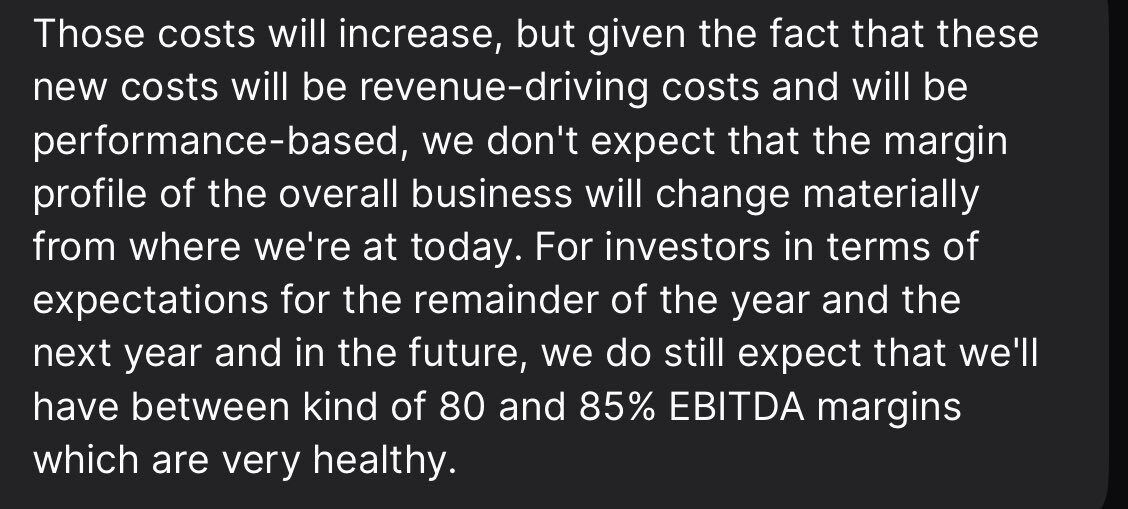

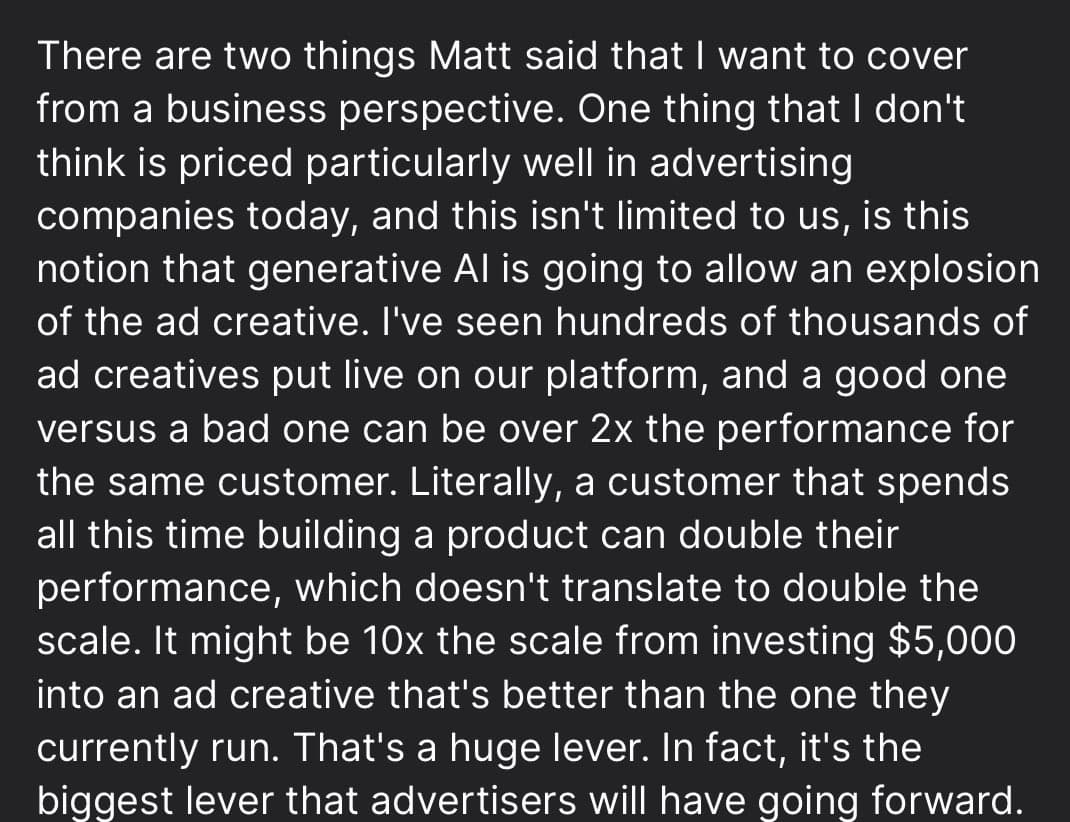

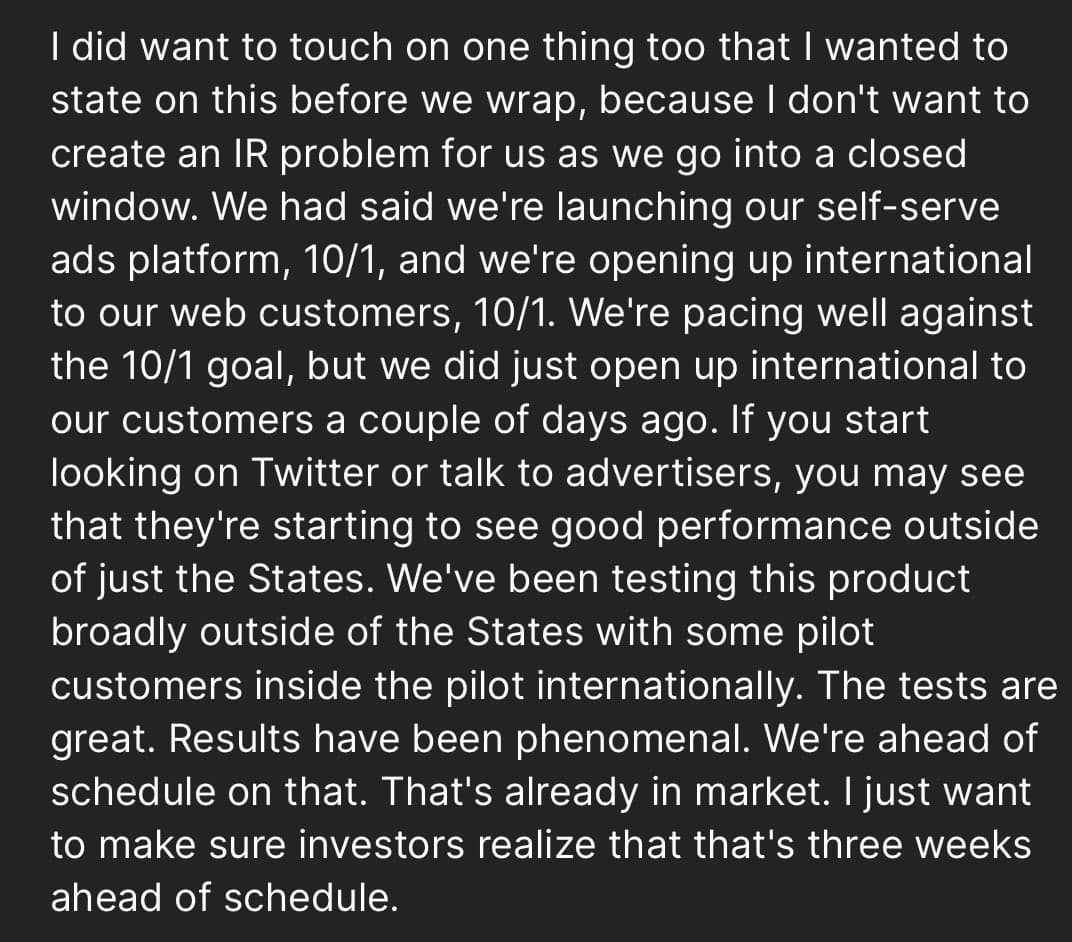

Yhtiö odottaa jatkossakin 80–85 prosentin EBITDA-marginaalia. Generatiivinen tekoäly nähdään merkittävänä kilpailuetuna mainonnassa ja lisäksi lokakuussa on tarkoitus laajentaa itsepalvelualusta myös kansainvälisille asiakkaille.

https://x.com/The_StockDoc/status/1965841267008668130

Oppenheimer nosti AppLovinin tavoitehinnan 740 dollariin, perustellen arviotaan vahvemmilla näkymillä non-gaming-mainonnassa ja pitkän aikavälin kasvutekijöillä.

Yhtiön mukaan liikevaihto voi nousta vuoteen 2027 mennessä 8,6 miljardiin dollariin ja lisäksi myös lähiajan kysyntä vaikuttaa vilkastuvan etenkin tulevaa juhlakautta kohti. Uudet asiakkuudetkin ja käyttöliittymäuudistuksetkin tukevat yhtiön kasvua.

https://www.investing.com/news/stock-market-news/applovin-target-lifted-by-240-at-oppenheimer-on-nongaming-advertising-growth-4251755

1 tykkäys

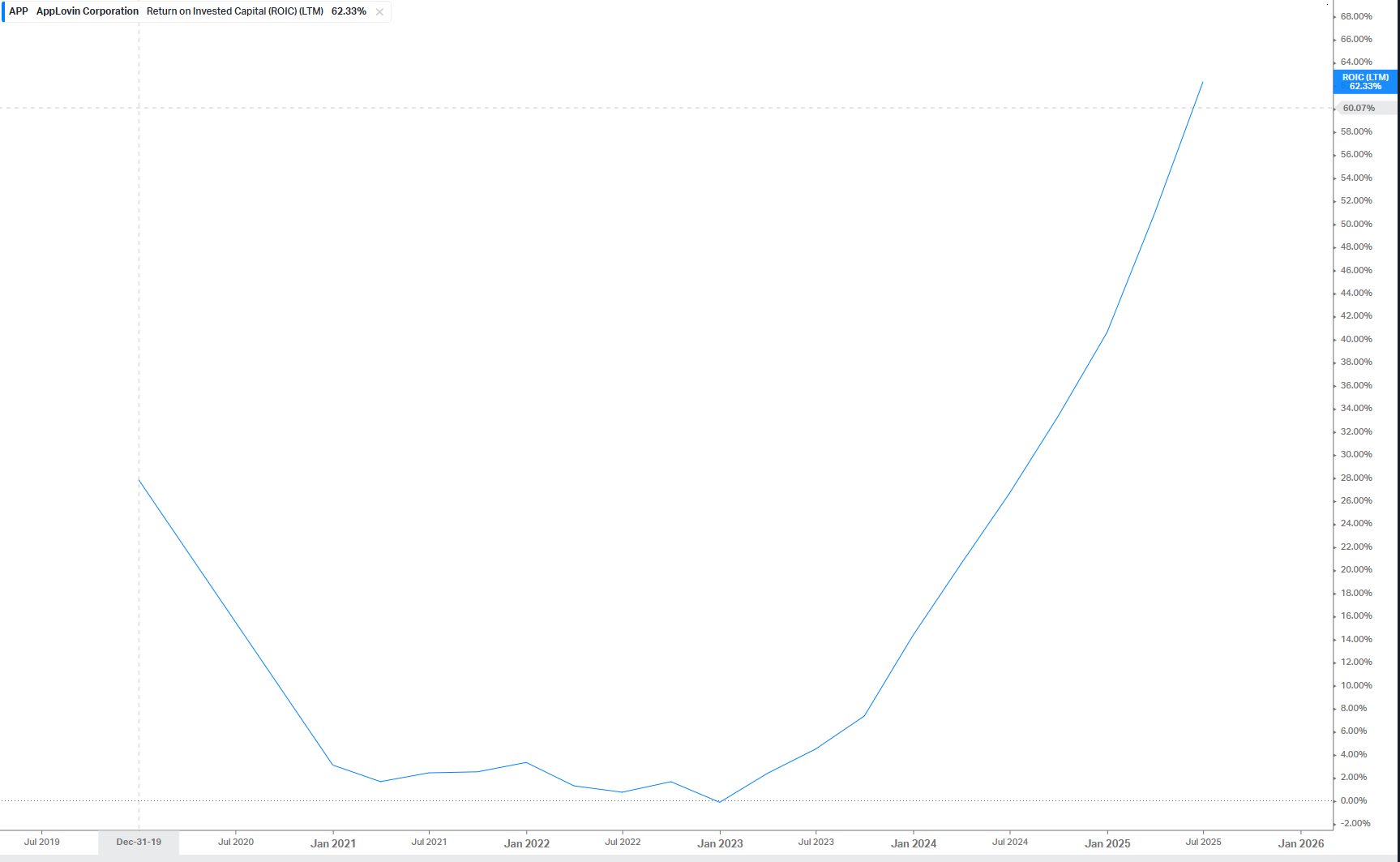

Applovin tuntee, kuinka vauhti kiihtyy…

niin ja liikevaihdon lisäksi ROIC on myös menossa mukana, siis kasvussa.

https://x.com/QualityInvest5/status/1970705399767539994*

ROIC:

Laitan tämän saman viestin tännekin (Kauhistelussa about sama)

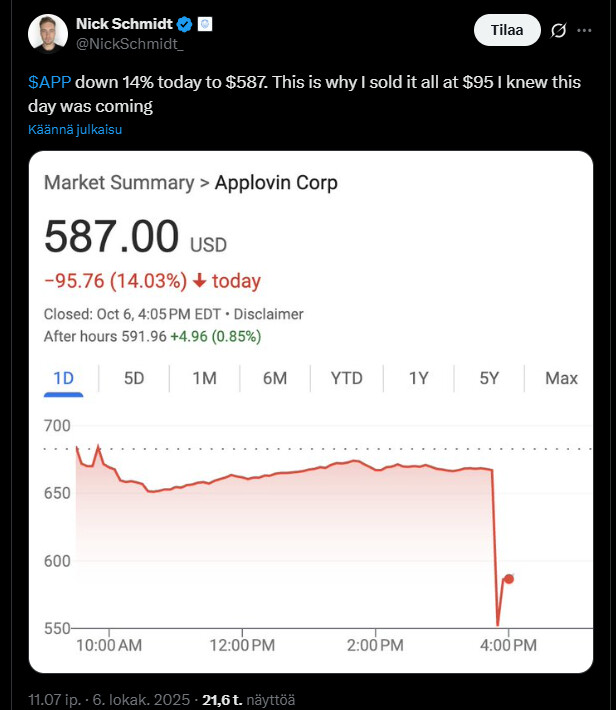

Applovin syöksyi ja tviittaja harrasti itseironiaa, toki jonkun tosikin piti tulla kommentoimaan.

https://x.com/NickSchmidt_/status/1975291885888676053

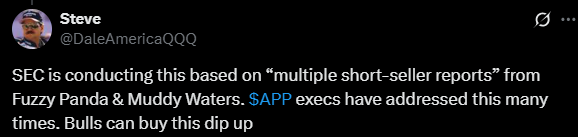

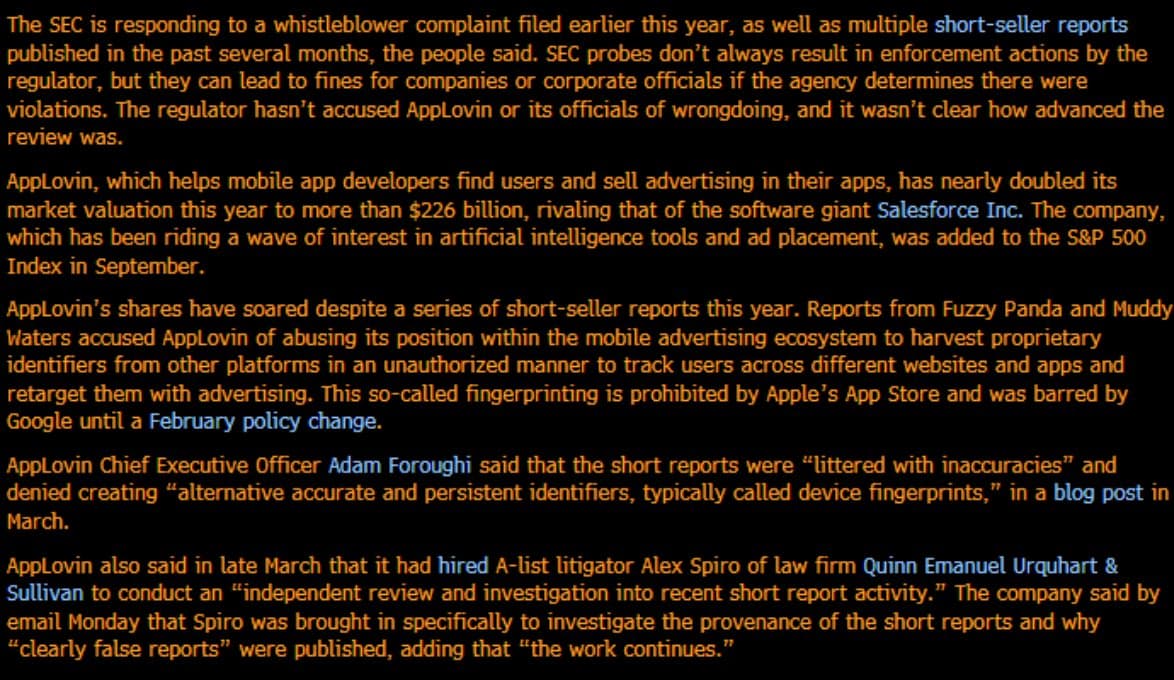

Applovinin kurssi putosi ymmärtäneekseni siksi, koska viranomaiset alkoivat selvittää väitteitä siitä, että Applovin olisi käyttänyt mainonnassaan jotain luvattomia seurantakeinoja useiden joidenkin raporttien perusteella.

https://x.com/DaleAmericaQQQ/status/1975292030617329820

1 tykkäys

Nämä uutisethan olivat esillä jo helmi-maaliskuussa, ei mitään uutta. Nyt shorttifirmojen aikaansaama uutisen uudelleentaimaus ajoittui kätevästi 20 minuuttia ennen pörssin sulkeutumista, jolloin kaikki stopparit paukahtivat, eikä mitään vastineita ennätetty lähettää.

Nothing new. Sijoittajat tietysti inhoavat epävarmuutta, jota tällaiset uutiset hetkeksi synnyttävät. Osa myy sen takia paniikissa osakkeensa, ja siihenhän shorttaajat pyrkivät, sillä he tekevät leipänsä. Googleen ja Metaan on kohdistunut lukuisia samanlaisia tutkimuksia (aiheena “cookie collection practices”) vuosien varrella, ja kannattaa kenties katsoa niiden osakkeiden pidemmän aikavälin kehitystä. Jos sijoitushorisontti on päivä, tai viikko, niin silloin on varmaan iloinen, tai levoton, jos Applovinia eilen omisti/ei omistanut. Tällaisten uutisten takia en käytä stoppareita, sinne katoaisi sekunnissa hyvät osakkeet. Itselle on yhä suunnitelmissa myydä Applovin pois kun sen hinta on noin 750 dollaria, ja tähtäimeni on ensi vuoden alkupuoliskossa.

Mutta jokaisella on oma sijoitusstrategiansa ja aikahorisonttinsa - hyvä niin. Tärkeintä pitkän päälle varmaan olisi se, etteivät sijoittajan ostot olisi enimmäkseen peesausostoja yrityksiin perehtymättä ja myynnit paniikkimyyntejä. Tällä yhdistelmällä sijoitusomaisuus vähenee, eikä lisäänny.

3 tykkäystä

Tässä vielä kiinnostuneille Applovinin toimitusjohtajan Adam Foroughin postaukset helmi- ja maaliskuulta, kun tästä ihan samasta asiasta puhuttiin:

2 tykkäystä

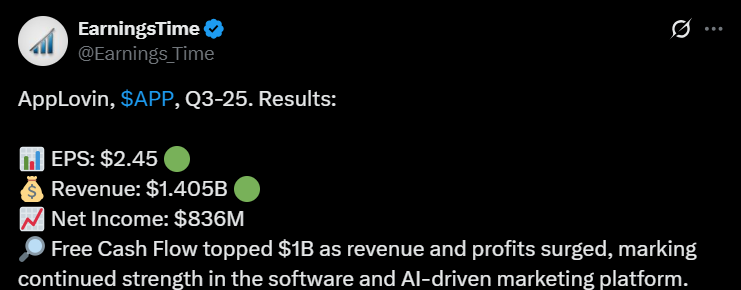

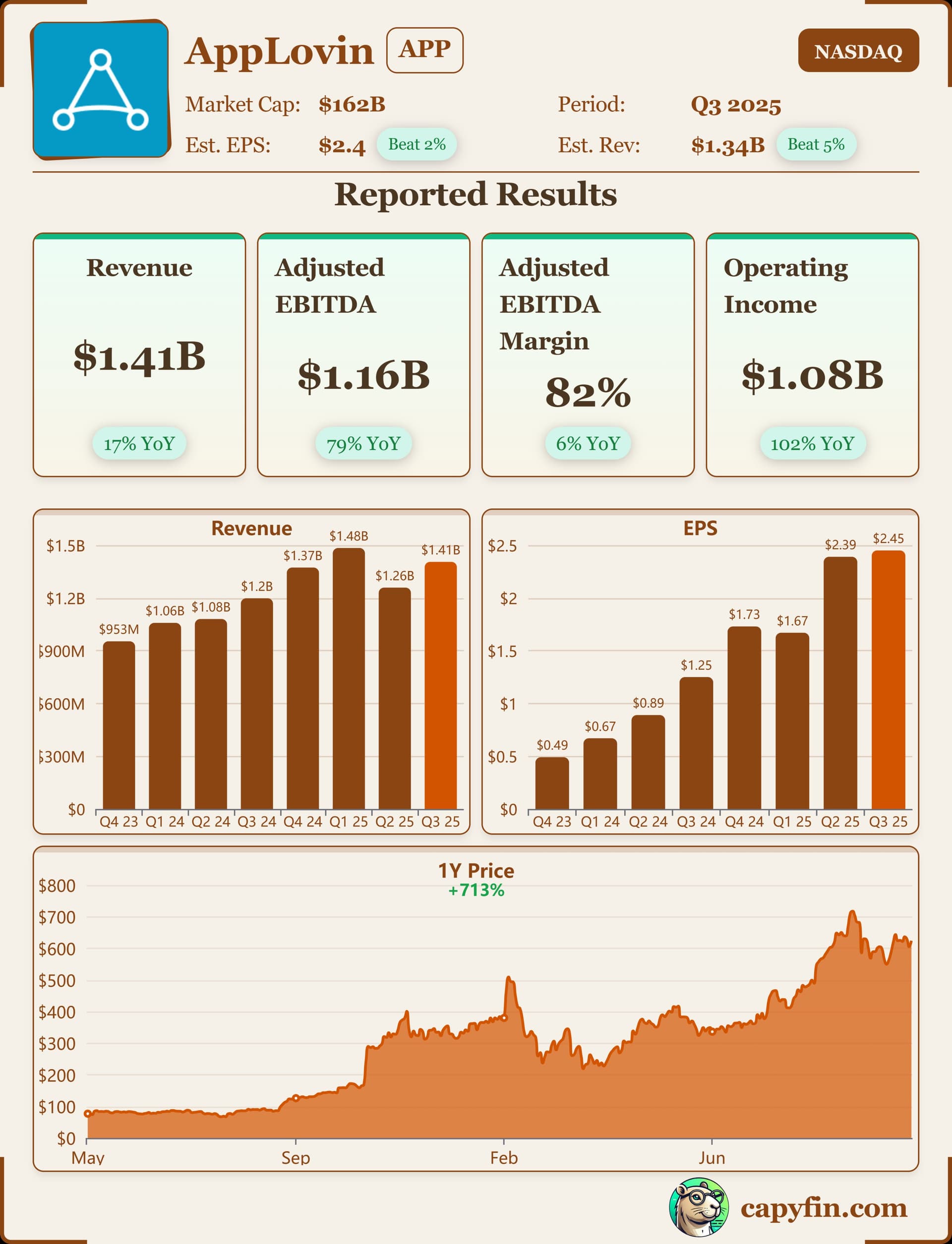

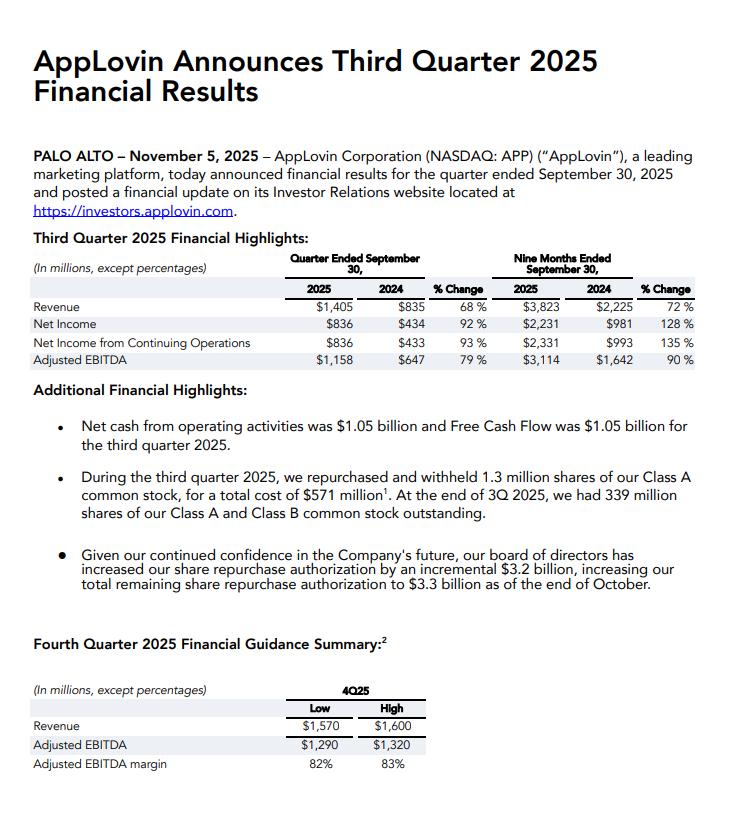

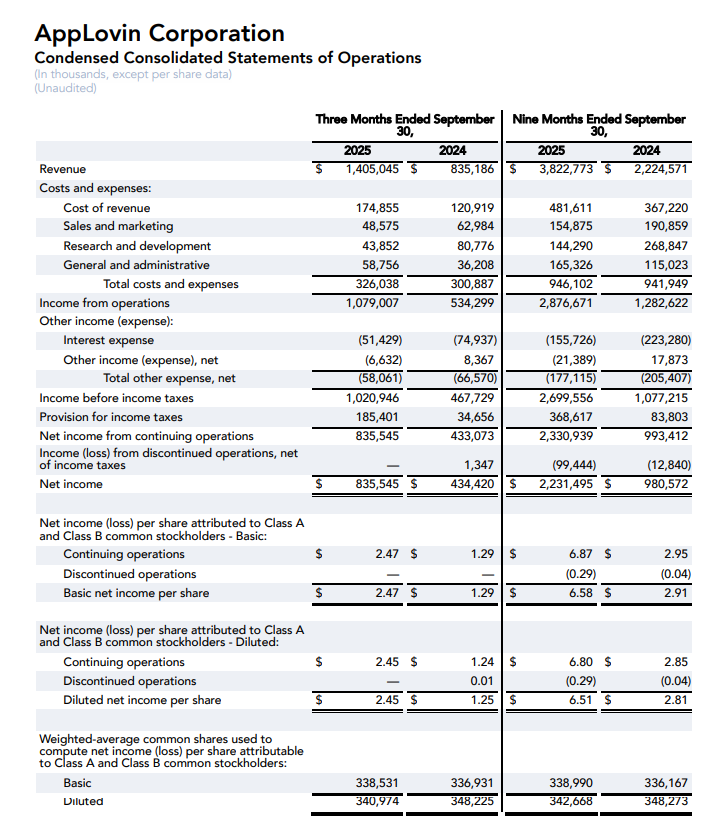

AppLovin vet vahvasti. Liikevaihto ja tulos kasvoivat reippaasti odotuksia paremmin, lisäksi etenkin mainosalusta toi vauhtia lukuihin. Kannattavuus pysyi korkealla ja tekeminen oli ilmeisesti hallitua eikä ollut mitään suurempia yllätyksiä.

Yhtiö odottaa loppuvuodelta lisää kasvua ja luottaa omaan tekemiseensä. Katteiden pitäisi pysyä vahvoina, eikä johdon viestinnästä heijastunut erityistä varovaisuutta – enemmänkin johto katsoi tulevaisuuteen.

Rahaa virtaa oli a sitä käytetään mm. omien osakkeiden ostoon. Samalla kehitetään palveluja eteenpäin ja tähdätään uusiin kasvusuuntiin tai jotain sellaista.

https://x.com/Earnings_Time/status/1986183215179063782

2 tykkäystä

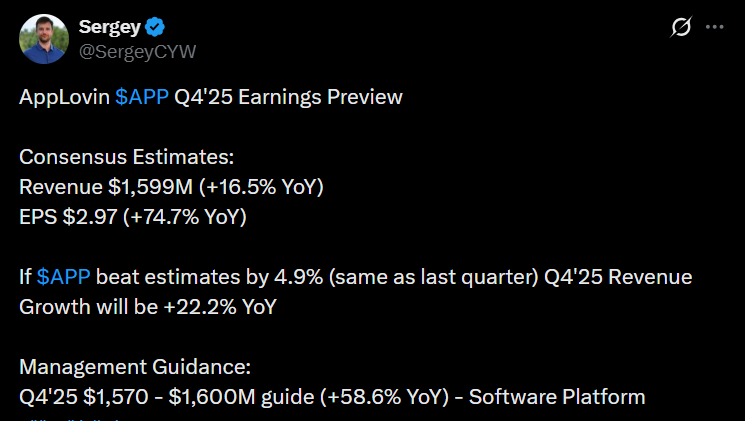

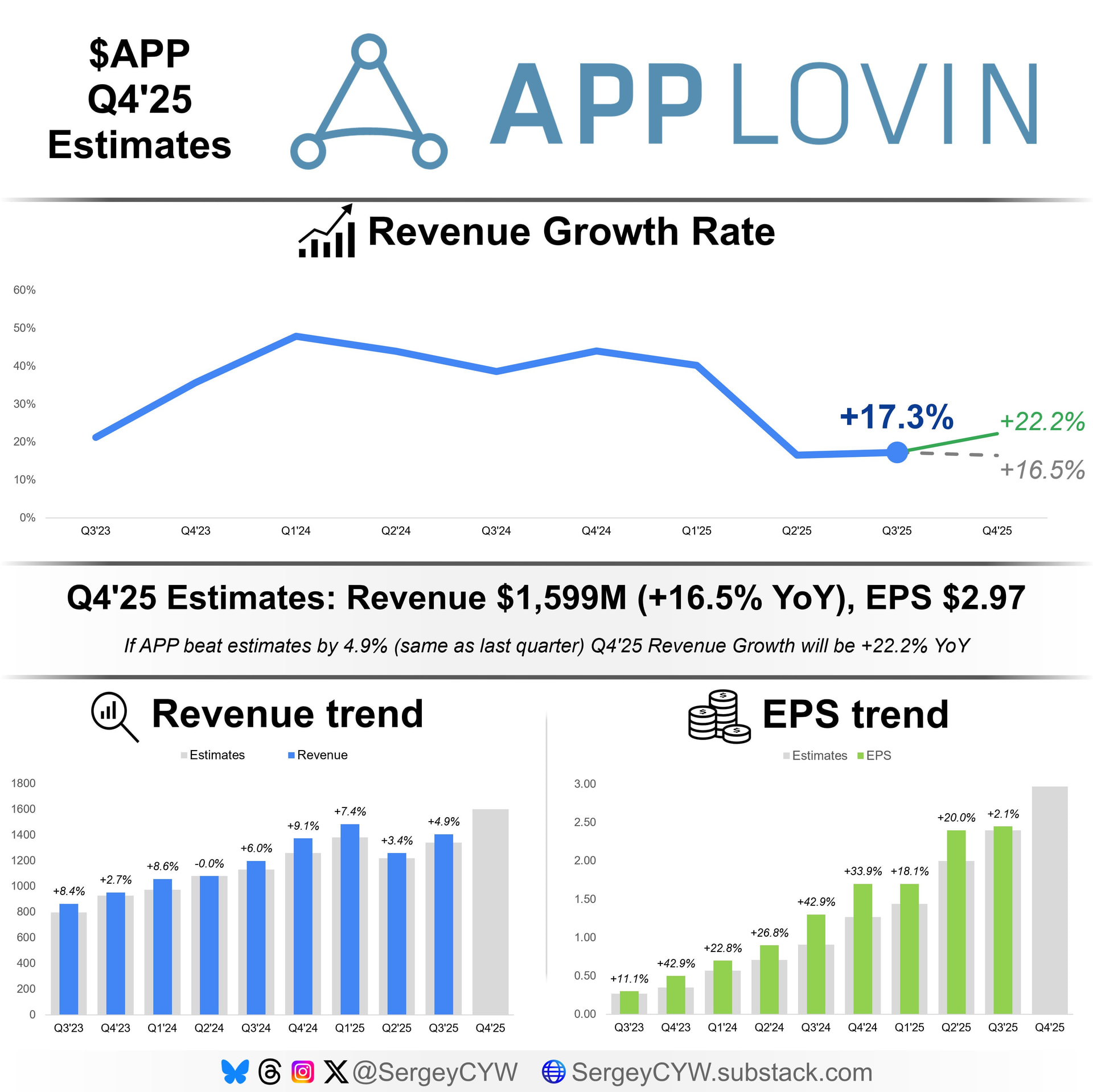

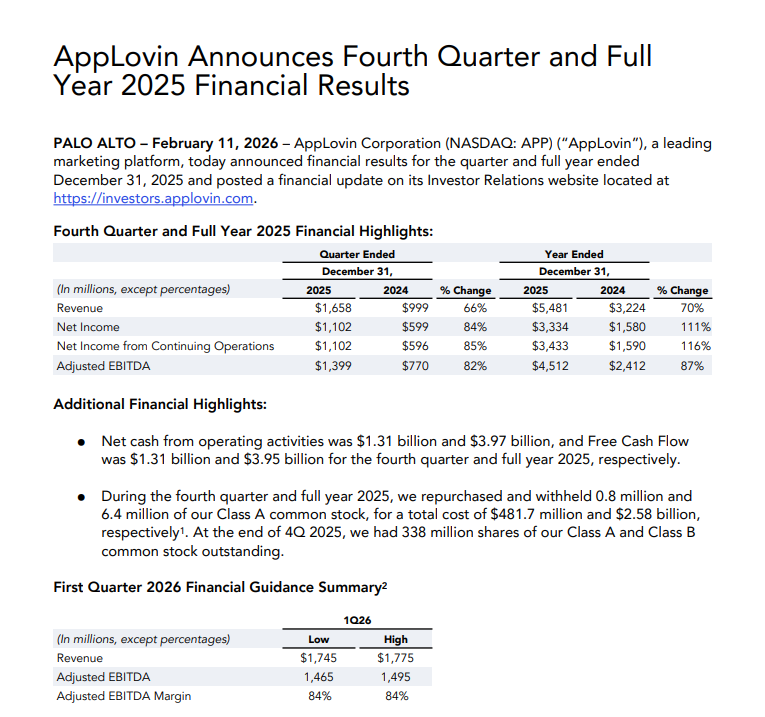

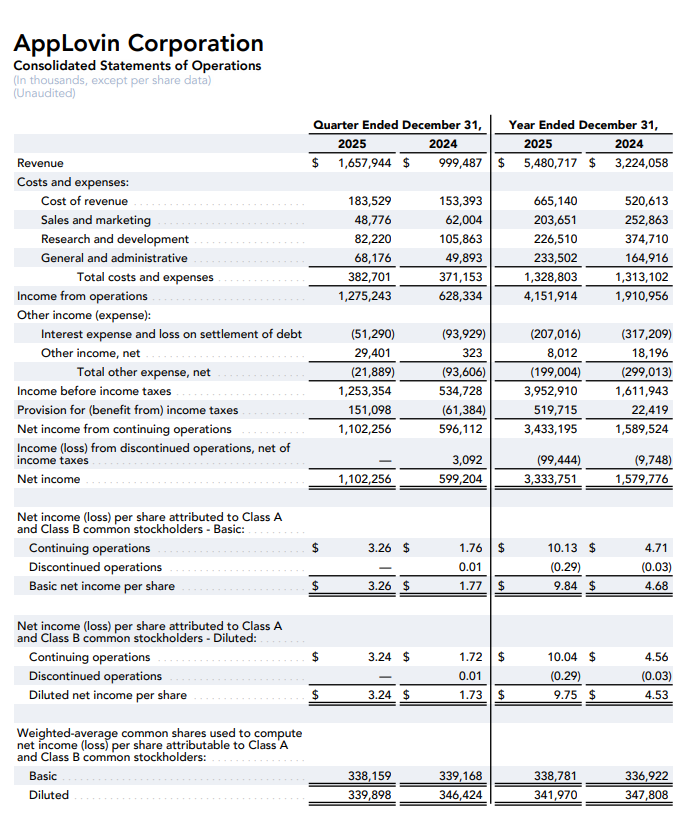

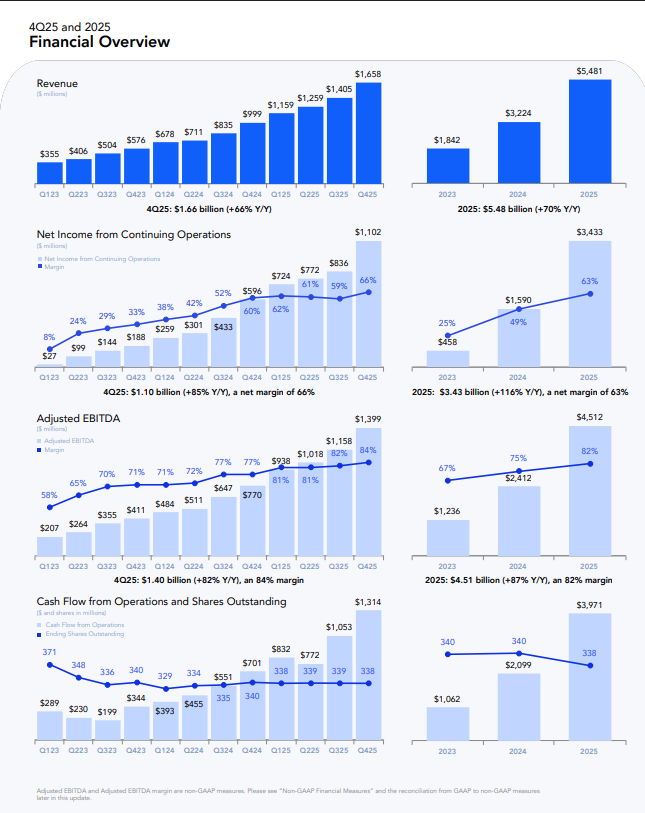

Applovin raportoi poikkeuksellisen vahvasta loppuvuodesta sekä liikevaihto että tulos ylittivät markkinoiden odotukset reilusti.

Menestyksen ajurina oli tietysti AI-pohjainen mainosteknologia, jonka kiihtyvä kasvu siivitti yhtiön historiallisen kovaan suoritukseen. Toisaalta sijoittajat olivat vähän epäröiviä yhtiön tulevaisuuden näkymiin, mutta yhtiö ennustaa kasvun pysyvän vauhdikkaana myös tänä vuonna, mikä vahvistaa sen asemaa alan huipulla.

https://x.com/SergeyCYW/status/2021562629718958515

3 tykkäystä