Raulin DCF-mallissa Anoran osakkeen arvoa 3,5 eur rasittaa myytyjen saamisten määrä, 164 mio eur per q4/25. Ajatuksena lienee siis se, että “oikeasti” Anoran tulisi rahoittaa tämä summa ottamalla lisää velkaa. Raulin velaton arvo DCF 532 mio eur pohjalta ja ilman tätä korjausta, viimeisen neljän neljänneksen vaihtelu huomioiden, osakkeen arvo on noin 5,2 eur. Myytyihin saamisiin liittyvä korjaus mallissa laskee siis arvoa noin 1,6 euroa per osake. Jos hyväksytty PE on 10, tämä vastaa 0,16 eur tulosvaikutusta ja kun osakkeiden lkm on noin 67,6 mio, noin 10,816 mio eur rahoituskulua, johtuen siis oletetusta lisävelasta. 10,816 mio euron kulu vs. oletettu lisävelka 164 mio euroa vastaa taas noin 6,6 % rahoituskulua, toisaalta yhtiön lainakannan keskikorko on nyt noin 3,9 %. Jos myytyjen saamisten määrä kuitenkin rahoitettaisiin nykyisellä korolla, tulosvaikutus per osake olisi noin 0,066 eur matalampi ja PE-luvulla 10 osakkeen DCF-arvo mallissa noin 0,66 euroa korkeampi, eli siis 3,5+0,66=4,16 eur. Vaikuttaisi näin ollen siltä, että DCF-arvon korjaaminen vähentämällä myytyjen saamisten arvo sellaisenaan on aika tyly toimenpide, vaikka pitäisi jonkinlaista korjausta tarpeellisena. Tarkistuksena vielä Raulin ROE 2025: 5,1 % ja 2026 6,4 % vs. OPO:n tuottovaatimus 8,4 % kertaa OPO, 2025: 5,97 ja 2026: 6,14, tulos 2025: 3,62 ja 2026:4,55, keskiarvo 4,1 eur. Missä ajatus ylläolevassa menee harhaan, jos/kun menee?

Tänään tuli Alkon huhtikuun luvut ja Norjan vinmonopolet myös kertonut omansa. Pääsiäisen myötähän huhtikuun kehitys oli hyvää, joten kannattaa katsoa lähinnä koko alkuvuoden lukuja. Norjassa lasku alkvuonna on 4-5 % ja Suomessa sekä viinien että väkevien suhteen 10-15 %. Kuten todettua, tässä näkyy 8-% viinien siirtyminen ruokakauppoihin. Kuitenkin ainakin Norjan ja Suomen osalta näyttäisi että markkina on laskussa, eikä Anoran odottamalla viime vuoden tasolla (tämä siis oletus koko vuodelle yleisesti Anoran markkinoilla). Vertailukohdat toki helpottaa loppuvuotta kohti, joten nykyiselläkin kysyntätasolla nuo miinukset loivenee koko vuoden lukuja katsottaessa.

Anora yritti myös Q1-tuloksen yhteydessä tuoda esiin, että onhan heillä paljon muutakin myyntiä kuin monopolimarkkinat ja etenkin pelkästään Suomen ja Norjan tuijottelu voikin antaa turhan negatiivisen kuvan, kun suurin monopolimarkkina eli Ruotsi pärjää paremmin (mutta ei raportoi kuukausilukuja julkisesti).

Luulen, että tässä Anoran ketjussa voisi kiinnostaa tämä @Antti_Leinonen:n kirjoitus alkoholiyhtiöistä. ![]()

Morningstarin analyytikot uskovat, että suuri osa nykyisen heikkouden taustalla olevista syistä hälvenee ajan kanssa. Morningstarin mukaan yhtiöt, joilla on laaja tuoteportfolio ja maantieteellisesti hajautettu liiketoiminta, tulevat selviytymään ulkoisten vastatuulten ylitse.

@Rauli_Juva ennakoi pientä parannusta perjantain Q2-katsauksessa, syytä olisikin, sen verran paljon on kiinni tässä tislekasassa ![]() : Anora Q2’25 -ennakko: Pääsiäisen ajoitus tukee pientä parannusta - Inderes

: Anora Q2’25 -ennakko: Pääsiäisen ajoitus tukee pientä parannusta - Inderes

| Ennustetaulukko | Q2’24 | Q2’25 | Q2’25e | Q2’25e | 2025e | |

|---|---|---|---|---|---|---|

| MEUR / EUR | Vertailu | Toteutunut | Inderes | Konsensus | Inderes | |

| Liikevaihto | 177 | 178 | 178 | 689 | ||

| Käyttökate (oik.) | 15,2 | 17,0 | 16,1 | 70,0 | ||

| Käyttökate | 14,9 | 17,0 | 16,1 | 70,9 | ||

| Liikevoitto (oik.) | 8,7 | 10,4 | 9,4 | 43,4 | ||

| Liikevoitto | 8,4 | 10,4 | 9,4 | 44,3 | ||

| EPS (raportoitu) | 0,03 | 0,07 | 0,05 | 0,30 | ||

| Liikevaihdon kasvu-% | -3,1 % | 0,2 % | 0,6 % | -0,4 % | ||

| Liikevoitto-% (oik.) | 4,9 % | 5,9 % | 5,3 % | 6,3 % |

Alkon heinäkuun myyntiluvut julkaistiin tänään, joka on mielenkiintoista ehkä etenkin sen vuoksi, että tämä on ensimmäinen vertailukelpoinen kuukausi viime vuoden kesäkuussa tapahtuneen 8 % viinien lakimuutoksen jälkeen. Kokonaismyynti heinäkuussa laski 2,5 %, mutta Anoralle relevantit viinit ja väkevät laskivat 5% ja 8%. Markkinan laskutrendi siis jatkuu, samahan on ollut toki myös Norjassa ja Ruotsissa nähtävissä alkuvuoden luvuissa.

Perjantaina tosiaan nähdään miten Anora Q2:lla on pärjännyt, jossa pääsiäisen ajoitus tuki volyymeja. Jos muuten firmalle on kysymyksiä mielessä perjantain haastikseen, niin saa laittaa tänne.

Kysymykseen pohjaksi:

Koskenkorvapohjaiset juomasekoitukset (bitter lemon, ginger ale jne.) tulleet kohtuullisen näkyvästi markkinoille tänä vuonna.

Miten näiden myynti on kehittynyt? / Ollaanko tavoitteissa?

Onko suunnitelmissa lisätä tällaisia ruokakauppajuomia?

Semivahvoja brändejä olisi ja halua kasvaa.

Kuitenkin tuo ydinmarkkinoiden ulkopuolinen myynti on aivan nappikauppaa.

Ollaanko vientiä jotenkin aktiivisesti edistämässä ja millaisin toimenpitein ja aikatauluin?

Hyviä kysymyksiä, kiitos!

Kv. liiketoiminnan perään olen kysellyt säännöllisesti ja keväällä laajan raportin päivityksen yhteydessä tulkintani firman puheista oli että se on jäämässä vähän vähemmälle huomiolle. Mutta kysytään toki Kirsin näkemystä asiaan. Alla pieni pätkä kevään laajasta aiheesta.

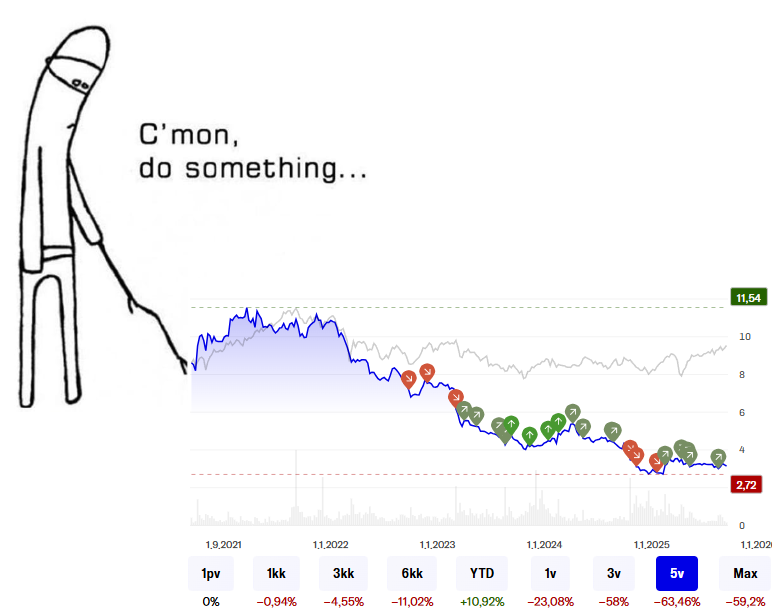

Voi voi, rahavirta sentään oli ihan ok, paitsi ollaan edelleen jäljessä viime vuotta: Anora Group Oyj:n puolivuosikatsaus 1.1.-30.6.2025: Matalampi liikevaihto vaikutti vertailukelpoiseen käyttökatteeseen Q2:lla. Toimenpiteitä taloudellisen suorituskyvyn parantamiseksi nopeutetaan | Kauppalehti

Q2 2025 lyhyesti

- Liikevaihto oli 165,5 (177,1) milj. euroa, laskua 6,6 prosenttia.

- Vertailukelpoinen käyttökate oli 14,0 (15,2) milj. euroa eli 8,4 (8,6) prosenttia liikevaihdosta, laskua 8,3 prosenttia.

- Käyttökate oli 13,5 (14,9) milj. euroa eli 8,1 (8,4) prosenttia liikevaihdosta, laskua 9,9 prosenttia.

- Liiketoiminnan nettorahavirta oli 22,3 (-4,4) milj. euroa.

- Osakekohtainen tulos oli 0,03 (0,03) euroa.

Tammi-kesäkuu 2025 lyhyesti

- Liikevaihto oli 306,8 (324,0) milj. euroa, laskua 5,3 prosenttia.

- Vertailukelpoinen käyttökate oli 22,0 (24,1) milj. euroa eli 7,2 (7,4) prosenttia liikevaihdosta, laskua 8,8 prosenttia.

- Käyttökate oli 22,4 (22,7) milj. euroa eli 7,3 (7,0) prosenttia liikevaihdosta, laskua 1,4 prosenttia.

- Liiketoiminnan nettorahavirta oli -53,4 (-49,0) milj. euroa.

- Osakekohtainen tulos oli -0,00 (-0,01) euroa.

- Nettovelka / vertailukelpoinen käyttökate (liukuva 12 kk) oli 3,0 (2,8).

Vähän huonolta näyttää Q2:n luvut…

@Rauli_Juva `:n pikakommentit tuloksesta: Anora Q2’25 -pikakommentti: Tulos jäi hieman odotuksista ja vertailukaudesta - Inderes

KV toiminnot vaatisivat hieman erilaisia otetta, sojua ja baijiu… Ei oikein Koskenkorva mene premium tuotteena ns. matkustaja myyntinä. Onko Norjan perintönä päällekkäisiä yhtiö rakenteita olemassa, tulos vaatisi rankkaa saneerausta. Voisi ehkä kysäistä onko ollut tarkastelussa tehokkuuden nostoa?

Ei Anoran ongelmat ole puhtaasti yhtiön omaan tekemiseen liittyviä. Hieman vilkaisee miten isoilla toimijoilla menee niin aika tarpomista niilläkin bisneksen teko

Hankala saada sijoituskeissiä tästä, kun näkymät tuloskasvulle vähän niin ja näin

Tuosta haastattelua, tuli nuo @Addick ja @Ummon kysymyksetkin mukaan. Kasvutavoitteiden suhteen vastaukset jäi kuitenkin tänään ilmoitettuun marraskuun CMD:hen.

Rauli on tehnyt yhtiöraportin, kun Anora julkaisee Q2-raporttinsa. ![]()

Anoran Q2-tulos jäi odotuksistamme ja vertailukaudesta. Vaikka yhtiö toisti koko vuoden ohjeistuksensa, ennusteemme laskivat sen alapuolelle, minkä vuoksi laskimme tavoitehinnan 3,3 euroon (aik. 3,5e). Maltillisen arvostuksen myötä toistamme lisää-suosituksen.

Rapsasta lainattua:

Tehostamistoimia nopeutetaan, strategiaa uusitaan – CMD marraskuussa

Raportin yhteydessä maaliskuussa toimitusjohtajana aloittanut Kirsi Puntila kertoi myös, että yhtiö nopeuttaa toimia taloudellisen suorituskyvyn parantamiseksi, joskaan se ei tarkemmin yksilöinyt, mitä tämä tarkoittaa. Yhtiö kertoi myös laativansa strategiapäivitystä, jossa se keskittyy lyhyen ja keskipitkän aikavälin suorituskyvyn parantamiseen 2025-26 ja kasvun tukemiseen 2026 eteenpäin.

Anora kertoi pitävänsä pääomamarkkinapäivän 5.11., jossa se kertoo lisää strategiapäivityksestään. Uskomme yhtiön päivittävän myös taloudelliset tavoitteet tässä yhteydessä. Strategia tulee tähtäämään vuoteen 2028 eli se on selvästi lyhyemmälle aikavälille kuin yhtiön nykyinen vuonna 2022 julkaistu strategia, jossa tavoitevuosi oli vasta 2030. Kommenttimme nykyiseen strategiaan ja tavoitteisiin ja niiden mahdollisiin muutoksiin voi lukea sivuilta 10-12.

Muutkin analyytikot saivat työnsä valmiiksi Q2-raportin johtopäätöksistä, Kauppalehden pikauutisista poiminnat:

OP laskee Anoran tavoitehinnan 3,40 euroon (aik. 3,50 eur.), toistaa lisää-suosituksen.

Nordea laskee Anoran tavoitehinnan 4,60 euroon (aik. 4,70 euroa), toistaa osta-suosituksen

SEB Bank laskee Anoran suosituksen 3,10 euroon (aik. 3,30 euroa), toistaa pidä-suosituksen

Kirsi Puntilan haastattelu Mandatumissa:

Tässä on Raulin kommentit Anoran kilpailijan Viva Winen Q2:sta. ![]()

Anoran Wine-segmentin pääkilpailija Viva Wine raportoi eilen Q2-tuloksensa. Vivan liikevaihto laski hieman Pohjoismaissa ja se poikkeuksellisesti menetti hienoisesti markkinaosuuttaan. Yritysoston ja raportointimuutoksen myötä Pohjoismaiden kannattavuutta ei enää näe suoraan Vivan raportoimista luvuista. Anoran Wine-segmenttiin nähden Vivan suoriutuminen on ollut jo pidempään parempaa ja myös Q2:lla Vivan liikevaihto kehittyi hieman paremmin ja kannattavuus oli selvästi Anoran Wine-segmenttiä parempaa.

Mietiskelin Anoran menoa. On skaalaa, on osaamista, on brändiä.

Pelkästään osinkoa tulee saman verran kuin pörssin historiallinen tuotto on ![]()

Ja sitten kuitenkin:

Toisaalta meillä on laskeva alkoholin kysyntä, mikä ei helpota Anoran liiketoimintaa.

Myynti ylös, kulut alas. Tarvittavia toimenpiteitä ja radikaalejakin liikkeitä, jos liiketoiminta ei suju? Ollaanhan tässä kaikki samassa veneessä ja toivotaan omistaja-arvon maksimointia?

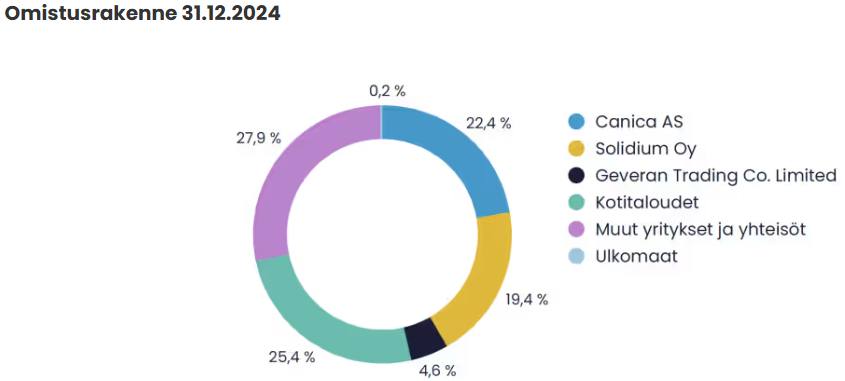

Tietenkin omistaja-arvoa maksimoidaan kaikin mahdollisin tavoin, kun omistusrakenne sisältää mm nuorekkaan dynaamisen Suomen valtion viidenneksen osuudella ![]()

No eihän se omistaja sitä yritystä pyöritä, vaan toimiva johto! Nehän siellä miettii miten liiketoiminta hiotaan huippuunsa!

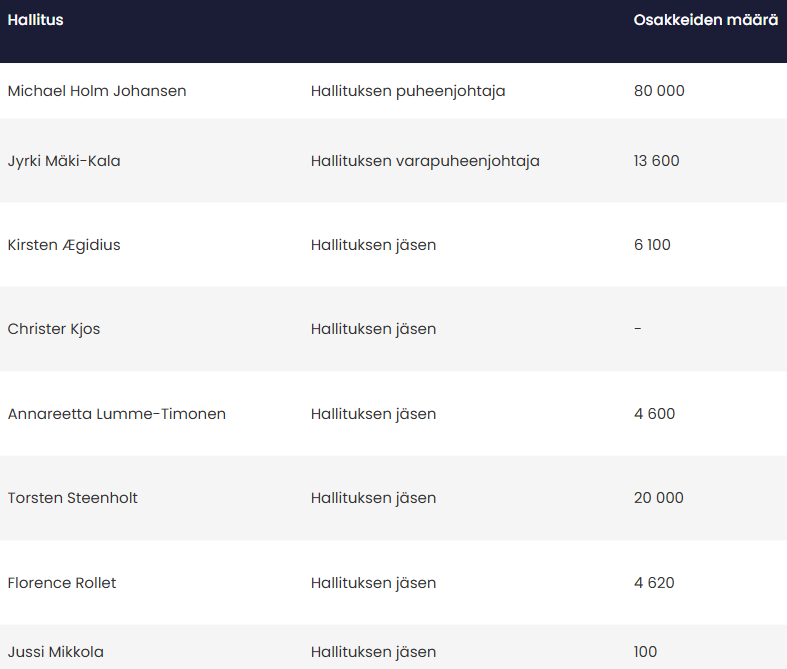

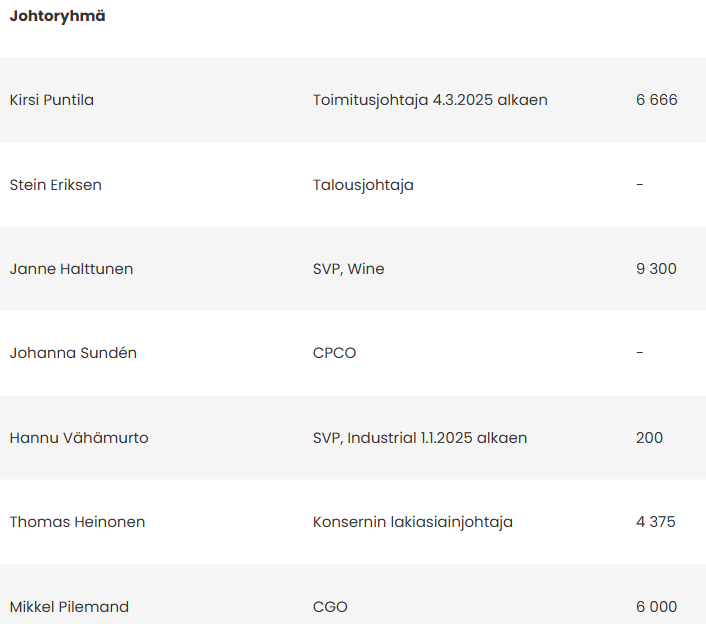

Ainakin Anoran omien nettisivujen mukaan viimeinen johdon liiketoimi on vuodelta 2023!

2024 vuosikertomuksen mukaan toimitusjohtajan kiinteä vuosipalkka on yli 710 tuhatta euroa. Esim TJ näyttää ‘sitoutuneen’ noin 1,5 viikon palkan verran Anoran osakkeisiin.

Vanha viisaus kertoo, että osta kun sisäpiiri ostaa. Olisi yksityissijoittajien kannattanut kuunnella tätä ja olla ostamatta Anoran osaketta.

En ole omia osakkeitani myymässä, mutta kyllä tässä pitäisi kuulla jotain positiivista liiketoiminnasta tai jos sisäpiiri oikeasti uskoo Anoraan, niin voisivat laittaa edes hieman omaa rahaa kiinni yhtiöön.

Voisin tästä ottaa seuraavaan haastatteluun kysymyksen, muistaakseni en ole Anoralta ainakaan toviin tätä kysellut. Nykyinen tj. toki ollut vasta pari kuukautta roolissaan ja strategian ja tavoitteiden päivitys on menossa, jolloin ei ei välttämättä saa ostaa, mutta marraskuun CMD:n jälkeen tuskin on pätevää syytä.