Disclaimer. I’ve already managed to bring at least two Swedish stock exchange companies to the forum whose share prices have since tanked by over 50%, so third time’s the charm ![]()

The industry is not familiar to me, so I’ll focus on the business numbers.

AlphaHelix’s description on Nordnet:

“AlphaHelix Molecular Diagnostics AB develops, manufactures, and markets products for DNA-identification and quantitation in molecular diagnostics and life science research. Its product inlcude Rob, BugScreener MRSA, and aAmp. The company applications inlcude Diagnostics, PCR and Liquid handling.”

So the business is related to DNA identification in the health technology sector. (The Swedish Nightingale?)

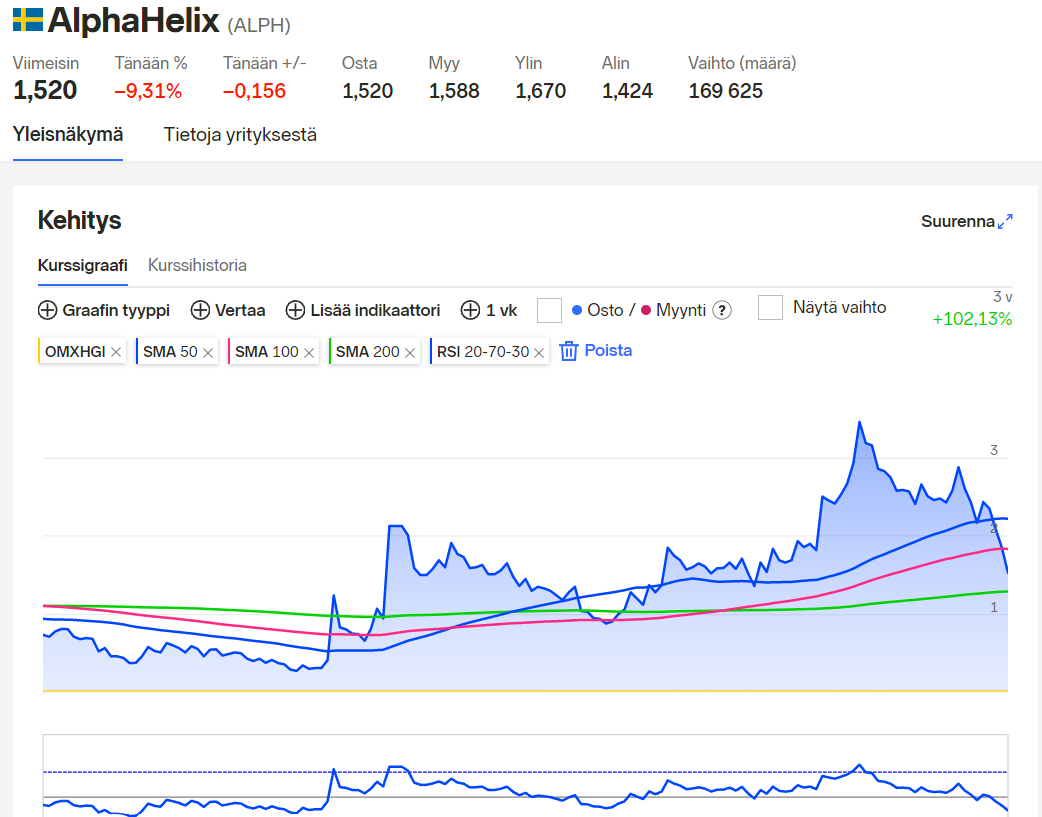

The stock price has fallen significantly, as have other growth companies.

However, the company is already profitable, and growth has continued well, at least in some parts, also at the beginning of 2022. Apparently, the cash position is also quite good:

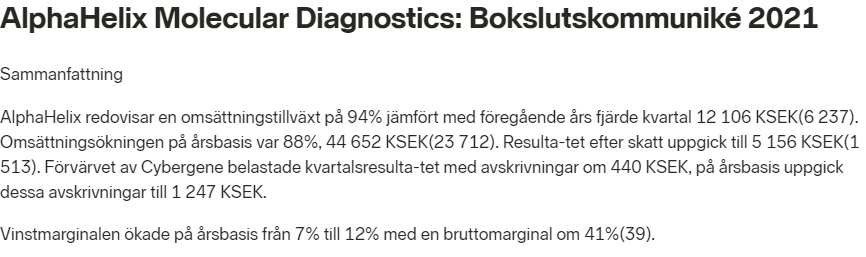

Key highlights from the Q4/2021 report:

Q4 profitability was seemingly quite weak, but still profitable. I don’t know what kind of seasonality there is, or if there were one-time items/investments etc.

And the report

Bokslutskommuniké 2021 - AlphaHelix Molecular Diagnostics (cision.com)

Notice from January about a subsidiary (with Google Translate)

"Alphahelix’s subsidiary Techtum set a sales record in January

The life science company Alphahelix’s subsidiary Techtum set a new sales record in January.

The company had sales of close to SEK 6.8 million during the first month of the year. January is normally a seasonally weak month and last year sales were around SEK 2.4 million. Techtum also set a sales record in December.

In January, the company entered into a distribution agreement with Italian Sentinel regarding the Nordic market.

"It is mainly increased diagnostic sales that accounted for the increased sales in January, but it is gratifying that the majority of agencies have made a positive contribution. The collaboration with Sentinel strengthens Techtum’s product portfolio, primarily for increased automation for clinical operations. Sentinel’s products are characterized by user benefits combined with an attractive price picture "Techtum continues to connect with new interesting diagnostic companies for the Nordic market. The fact that we were contacted by Sentinel also indicates that our competitiveness has attracted international attention," says CEO Mikael Havsjö in a comment."

A member of the management team apparently bought some shares

“Board member increases his shareholding in Alphahelix

On February 23, Artur Aira bought 27,152 shares in the life science company Alphahelix, where he is a board member. The shares were purchased at a price of SEK 1.96 per share, a deal of SEK 53,000. The deal was made outside the trading post. It appears from Finansinspektionen’s transparency register.”

In the autumn, however, some sold larger amounts.

P/E with 2021 results approx. 20

Has anyone else come across the company? It seems quite cheap, so I assume there’s some bomb hidden that I haven’t yet noticed due to the Swedish-language releases ![]() . Of course, I could be wrong and actually found a hidden gem this time.

. Of course, I could be wrong and actually found a hidden gem this time.