Hei Inderes-yhteisö! Liityin mukaan, kun sen verran kiinnostavia keskusteluja teillä ja opin aina jotain uutta.

Olen aloitteleva piensijoittaja keskisuurella aloitussummalla. OST ja AOT avaushakemukset paraikaa pankissa prosessissa. Nyt opiskelen sijoittamisen aakkosia ja väsäilen ensimmäistä sijoitussuunnitelmaa, strategiaa ja salkkua. Perusasiat jo jotakuinkin tunnen: hajauttaminen, buy and hold, verotusperiaatteet, osingot vs kasvuyritykset, jne.

Ajattelin perustaa sekä OST että AOT, hieman eri tarkoituksiin. Kiinnostaisi kuulla, onko ideassa teidän kokeneempien mielestä mitään järkeä? :

Haluaisin yhdistelmän i) järkevää ja pitkälinjaista vaurastumista keskisuurella riskillä (70% alkupääomasta), sekä ii) viihdyttävää riskihakuisempaa “pelaamista” tavoitteena nopeampi varallisuuden kasvu (30%). (Lisäksi pidän loput säästöistäni perustileillä, jotta elämiseen aina riittävästi varaa; ja siirrän kuukausittain jotain sijoitustileilleni). Tavoiteaikaa ei sinänsä ole, mutta pääsääntöisesti pitkällä tähtäimellä ollaan liikkeellä, ellei jossain vaiheessa tarvitse nostaa asuntoa tai autoa varten, tms.

Kumpaa tiliä suosittelisitte kumpaan tarkoitukseen? Ajattelin että ensimmäiselle vaihtoehdolle pääsääntöisesti AOT, ja OST jälkimmäiselle.

Lisäksi pohdin salkun tarkempia sisältöjä näiden eri tilien välillä: OST: Kotimaisiin osinkolehmiin ja kasvuyrityksiin, melko aktiivisesti tasapainottamalla. Riski voi olla suurikin. Vertailuindeksiksi OMXH25. Esimerkkinä esim Inderesin mallisalkku. Osingot sijoittaisin samantien eteenpäin korkoa korolle kasvamaan. AOT: Kotimaisiin ja ulkomaisiin kasvurityksiin ja myös ulkomaisiin vakaisiin osinkolehmiin, vähemmän aktiivisesti vaihtamalla ja tasapainoisemmalla riskillä. Vertailuindeksiksi esim. Tukholma tai Köpis.

Ja tähän vielä lisäkysymyksenä: nyt kun OST-tilien avausbuumi on käynnissä ja mahd. uusia piensijoittajia tulee siksi pian markkinoille, ja treidaaminen OST-tilien kautta lähtee käyntiin virallisesti 1.1.2020., onko tässä vaiheessa strategisen ja kärsivällisen sijoittajan parempi odottaa ja katsoa miten kotimaiset osakemarkkinat reagoivat vuoden alussa osakekysynnän kasvuun? Vai kannattaako kärkkyä ja olla nopea ostamaan heti vuoden alusta?

Melkein mututuntumalla tuntuisi maltillisemmalta jäädä OST-kilpailusta vuoden alussa pois, ja kääntää oma huomio AOT-tilin kautta sijoittamiseen yllämainitun alustavan strategian mukaisesti. Thoughts?

Minusta suunnitelmasi kuullostaa ihan järkevältä. Mukava myös huomata, että sinulla on strategia.

Itseäni hieman häiritsee yleisellä tasolla keskustelu OST ympärillä, että se olisi ilmainen lounas ja varsinkin treidaamisen suhteen. Pitää kuitenkin muistaa, että OST:llä pitää olla voitollinen treidaaja. Jos taas tekee tappiota vuositasolla OST on mielestäni enemmän haittaa kun hyötä. Noh, kukapa se tappiota tekisi

Itse siis treidaan ja meinaan jatkaa toistaiseksi AOT, koska siinä on useampia hyötyjä treidaajan näkökulmasta, vaikkakin samanlaista verohyötyä ei ole. Jossain kohti meinaan kyllä ottaa OST myös käyttöön.

Ps. Foorumilla on myös oma topic osakesäästötilille, josta löytyy paljon myös ajatuksia.

Vähän riippuu alkupääomasta, mutta pitäisin osakesäästötilin puhtaasti osinkoyhtiöille. Kasvuyhtiöille saat aot:n kautta hyldynnettyä hankintameno-olettaman. Lisäks aktiivinen kaupankäynti ost:n puolelle. Aot:lle sitten ne kasvuyhtiöt.

Osakesäästötilille voi muuten vero-optimoinin näkökulmasta ostaa myös englantilaisia ja kaiketi virolaisia yhtiöitä.

Minä varmaan sinun kengissäsi tuuttaisin vaan kaiken 50keur asti OST:lle, kunnes se on tapissa. Sitten rupeaisin ostamaan AOT:hen niitä pidempiaikaisia papereita ja keventilisin vastaavasti OST:n puolella jos haluat lisätä siellä puolella riskisempiä ja/tai treidaus positioita.

Logiikka siis se, että ei sun edes tässä alussa ole järkeä maksaa niistä osingoista veroja jos et tarvitse sitä cash flow:ta johonkin nyt heti, eli tavoite on kasvattaa pääomaa 10+ vuoden horisontilla.

Minäkin mietiskelin samoja juttuja reilu kuukausi takaperin. Päädyin siihen, etten toistaiseksi avaa osakesäästötiliä lainkaan. Minusta OST näyttää säästöpossulta, jonka kanssa tulee itku jos rahoja sattuu tarvitsemaan yllättäen.

Ennemmin ottaa sitten vaikka lainaa. Melko harvoin tulee sellasia tilanteita vastaan, että tarvis osakesäästötiliä laittaa lihoiks, jos menot ei liity asuntoon. Jos asuntoon tarvii rahaa, niin laina on kyllä niin halpaa, että verohyödyllä maksaa useempaan kertaan nykyset korot. Eri asia on sitten, jos rahoille on tarve tiedossa, niin sitten ei varmaan osakesäästötilille kannata omistuksiaan siirtää (ja joo, tietty käteisen kautta x)). Siinä tapauksessa ei kannattaisi niitä varoja suuressa määrin edes osakkeissa pitää aot:lla.

Miten se on ongelma? Käsittääkseni sieltä voi nostaa haluamansa summan josta sitten maksetaan voitto-osuudesta veroa, eli vero jonka olisit joutunut joka tapauksessa maksaan AOT:llä.

Itse näen sen niin että OST:llä saat “option” korkoa korolle myös vero-osuuksista… Varsinkin jos aiot tehdä kauppaa vähääkään tai panostat korkeaan osinkotuottoon, niin tämä on merkittävä 10 vuoden aikana.

Mutta tosiaan OST on parhaimmillaan aloittelevalle sijoittajalle, joka ottaa riskiä ja tulee myös hyötymään korkoa korolle efektistä pidemmän ajan kuluessa, sekä jolla on käteistä laittaa ilman että pitää realisoida nykyisiä omistuksia.

No siis, tuohan on vain yksi syy. En sano ettei kenenkään kannata laittaa rahaa osakesäästötilille, mutta kannattaa kyllä huolella pohtia tuleeko pysymään kaikkien reunaehtojen sisällä riittävän pitkään. Tuolla OST-ketjussa niitä on käyty läpi. Esim. lainan vakuudeksihan OST ei kelpaa.

OST:n ottaisin kasvuyrityksien aktiiviseen kaupankäyntiin suomalaisilla ja ulkomaisilla osakkeilla. En suosisi osinko-osakkeita, koska niiden osalta AOT tarjoaa verohyödyn (25,5% vs 30%) ja ulkomaisten osakkeiden osinkoverotus OST:llä on vielä epäselvä.

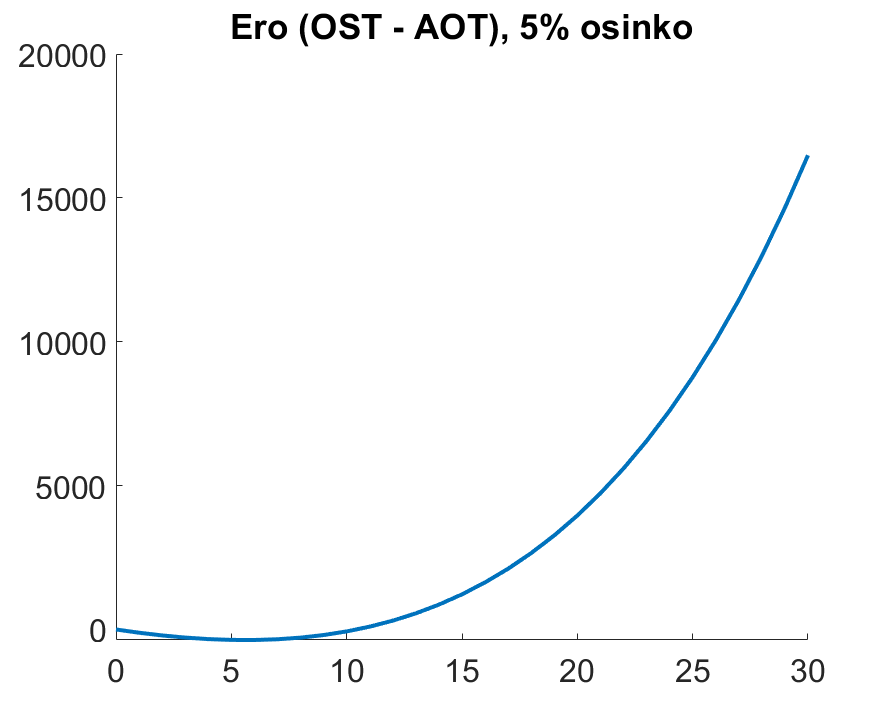

Kannattaa muistaa, että tuo verohyöty on kuitenkin kohtuullisen pieni. Tässä on nopea laskelma 5% osingolla ja 50k€ aloitussummalla. Tuossa on siis OST verojen jälkeen kun on kasvanut tuohon vuoteen asti tilin sisällä. 6 vuoden jälkeen AOT on 365€ voitolla ja se on tuon käppyrän pohja. 11 vuoden jälkeen OST siirtyy voitolle n. 100€ ja loppu on historiaa.

Olen pyöritellyt tätä OST asiaa omalta kantilta ja päädyin kuitenkin ratkaisuun, että siirrän osan treidaamisesta OST:lle.

Verohyöty on kieltämättä kiistaton, vaikkakin sulkee osaltaan mahdollisuuksia pois.

Sen takia jätän myös AOT, jossa on limitit, lyhyeksi myynnit yms. mahdollisuudet.

OST toimii kuitenkin niin kauan hyvin, kun pystyy tekemään longina treidejä

Mun mielestä osa aloittelevan salkunrakentajan palettia on joku automatisoitu sijoittaminen johonkin rahastoon tai etf:ään.

Vaikka esim niin että jos on sijoittaa 500€/kk niin 250€ suoraan osakkeisiin, 125€ superrahastoihin ja 125€ SP500 etf:ään.

Tolla tavalla jokainen pääsee kyllä tekemään sijoituspäätöksiä mutta hilaa tuotto-odotuksen lähemmäksi indeksiä. 50/50 suhdetta voi sitten ajan kanssa muuttaa kun ymmärtää miten menestyvä sijoittaja on.

Itsellänikin hieman samankaltaiset jutut mielessä. Nyt kun Hoivatiloista vapautuu rahaa, niin olen miettinyt pitäisikö koko potti lykätä OST vai AOT. Mielessä olisi Hoivatilojen tilalle sellaisia yhtiöitä kuin Qt, Revenio (vihdoin) ja mahdollisesti Harvia. Tavoitteena ostaa ja pitää todella pitkällä tähtäimellä.

Näistä yksikään ei juuri osinkoa maksa, joten meneekö siinä OST-hyödyt sitten ikään kuin hukkaan? Toisaalta se vähäkin mikä niistä osinkoina tulee, ei kuitenkaan verotettavaksi mene, joten plussa se on pienikin plussa. Ja kuten yllä oltiin kirjoitettu, nuo voi sitten myöhemmin (kun OST siirretty yli 50k) tilin sisällä myydä ja ostaa tilalle osinkoyhtiöitä ja ostaa nuo sitten tilalle AOT puolelle. Sillä oletuksella, että OST on voimassa samat ehdot kuin nyt.

Miinuksena sitten se, etteivät nuo käy lainan vakuudeksi, toisin kuin arvo-osuustilillä. Tosin sijoituslainaa en olisi luultavasti lähivuosina ottamassakaan, ainakaan tässä markkinatilanteessa.

Ehkä siis siirrän Hoivatiloista saamani rahat vain OST ja ostan noita yllä luettelemiani yhtiöitä huolimatta siitä, etteivät osinkoa juuri maksakaan. Tilannetta ehtii muuttaa sitten myöhemmin, kun se 50k on yhteensä saatu OST siirrettyä…

Itse päädyin nyt siihen että

OST :n rinnalle avaan AOT:n . AOT tulee olemaan osakkeille jotka yritän ostaa ja unohtaa. OST tulee nyt hetken olemaan hiekkalaatikkona . En tiedä onko markkinoilla aina tälläistä että hype siirtyy sektorista toiseen ? OST:lla tulen tekemään enemmän kauppaa esim nyt vety / EV osastolla . Todennäköisesti poltan näppini , mutta saanhan kuitenkin tuntumaa sijoittamiseen .

AOT toivottavasti sitten opettaa käsien päällä istumisen.

Kuten sanottu sijoitus suunnitelma hakee vielä sitä itselleni sopivaa raidetta .

Lainaan tästä ketjua aloittelevan sijoittajan tyhmään kysymykseen, liittyy kuitenkin mielestäni osittain valintaan OST ja AOT välillä:

Hankintameno-olettama. Tyhmä kysymys, mutta jos ostan yhtiön X osaketta yhden kappaleen per kuukausi kymmenen vuoden ajan, jonka jälkeen myyn kaikki. Miten hmo lasketaan tässä tapauksessa? Vain ensimmäisestä osakkeesta voidaan laskea hmo piiriin ja kaikki muut verotetaan täydellä arvolla?