Talousjohtaja on ostanut osaketta reilulla 44 000 eurolla.

4 tykkäystä

Tänään lienee Alman osingonmaksupäivä, joten mikä homma että käteisen sijasta tilille on ilmestynyt muutama uusi osake 0,00e hankintahintaan?

2 tykkäystä

Ei mulle ole ilmestynyt mitään ja osingon maksukin on vasta noin kuukauden kuluttua:

Alma Median hallitus tulee ehdottamaan varsinaiselle yhtiökokoukselle, että tilikaudelta 2025 maksetaan osinkoa 0,48 euroa osaketta kohden (2024: 0,46 euroa osakkeelta). Osinko maksetaan sille, joka on merkitty osingonmaksun täsmäytyspäivänä 13.4.2026 osakkeenomistajaksi Euroclear Finland Oy:n pitämään Alma Media Oyj:n osakasluetteloon. Hallituksen alustava ehdotus on, että osinko maksetaan 20.4.2026.

6 tykkäystä

Jahaa, katsoin sekä vuotta että kuukautta väärin. Mysteeri siis paranee vain ![]()

5 tykkäystä

Mitä olen tänään missannut kun Alman osake +7,82% muun pörssin olessa laskussa?

Päivän lopun nousu näyttää tapahtuneen hyvin pienellä vaihdolla. Reilu sata osaketta päätöskurssilla ja muutama sata enemmän hiukan halvemmalla vähän aiemmin.

6 tykkäystä

Tässä on Petrin ennakoinnit, kun Alma kertoo tuloksestaan keskiviikkona ![]()

Ennustamme yhtiön liikevaihdon ja operatiivisen tuloksen kasvaneen vertailukaudesta, vaikkakin markkinatilanne on jatkunut suhteellisen tahmeana. Vuoden 2026 ennusteemme odottavat liikevaihdon kohtuullista ja tuloksen tuntuvaa kasvua (+ 8 %), joten odotamme yhtiön toistavan ohjeistuksensa.

3 tykkäystä

ALMA MEDIAN OSAVUOSIKATSAUS TAMMI-MAALISKUU 2026: Kannattavuus jatkoi vahvistumistaan, kaikki segmentit paransivat tulostaan

Taloudellinen kehitys tammi-maaliskuussa 2026:

- Liikevaihto 83,1 (79,2) milj. euroa, kasvua 4,9 %.

- Digiliiketoiminnan osuus liikevaihdosta 85,9 % (83,9 %).

- Oikaistu liikevoitto 20,4 (17,2) milj. euroa, 24,6 % (21,7 %) liikevaihdosta.

- Liikevoitto 20,3 (16,6) milj. euroa, kasvua 22,5 %.

- Oikaistu käyttökate 24,5 (21,6) milj. euroa, kasvua 13,2 %.

- Osakekohtainen tulos 0,19 (0,14) euroa, kasvoi 41,2 %.

- Alma Career: Liikevaihto kasvoi Tšekin markkinan vetämänä, oikaistu liikevoitto vahvistui 14,4 %.

- Alma Marketplaces: Liikevaihto kasvoi 11,8 %, oikaistu liikevoitto parani 29,0 %.

- Alma News Media: Kannattavuuden kehitys jatkui vahvana. Oikaistu liikevoitto kasvoi 21,9 %.

8 tykkäystä

Mukava ennusteylitys Alma Medialta. Tässä vielä Petrin kommentit:

9 tykkäystä

”Kunhan ajat paranee, niin Alma lähtee kuin hauki kaislikosta”. Tämän olen foorumille kirjoittanut aiemmin, mutta lähtee jo nyt![]() Etenkin tulos kova. Lisäksi ilmassa leijuu vieno tuoksu yritysjärjestelyoptiosta - joko kotimaassa tai ulkomailla.

Etenkin tulos kova. Lisäksi ilmassa leijuu vieno tuoksu yritysjärjestelyoptiosta - joko kotimaassa tai ulkomailla.

Toimarin haastattelu:

10 tykkäystä

Petrilta tuore raportti Alma Mediasta:

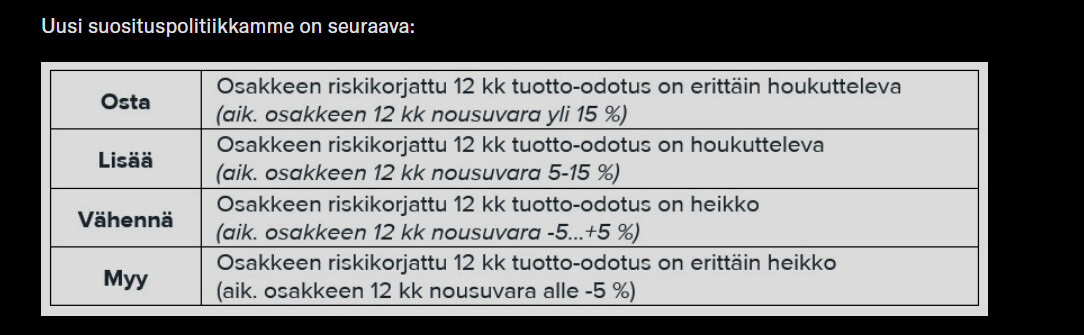

Enemmän yleisluonteinen kysymys @Petri_Gostowski , mutta miksi tässä tapauksessa ei annettu Osta-suositusta vaikka nousuvaraa tavoitehintaan on 21% ja sen lisäksi vielä 4% osinkotuotto? Ennen osta-suositukseen riitti yli 15% kokonaistuotto-odotus ja tästä määritelmästä on sittemmin luovuttu, mutta onhan tuo tuotto-odotus nyt sentään jo 25% eikä Alman riskitkään taida olla poikkeuksellisen isot.

Tämä ilmeisesti tuorein suosituspolitiikka.

11 tykkäystä

Hyvä kysymys, ja kyllä mä mietin sitä Osta-suositustakin. Se miksi himmailin sen kanssa on se, että on vaikea nähdä tässä toimintaympäristössä ajureita sen realisoitumiselle.

Toisekseen mietin, että tuon Lähi-idän yhä kiinni olevan salmen takia makroriskit on ennemmin kallellaan alas kun ylöspäin nyt. Siten mielellään säästelen sitä Osta suositusta, jos mr. market antaisikin vielä paremman paikan.

All in all, tää oli rajatapaus ja nyt päädyin säästelemään voimakkaampaa näkemystä.

13 tykkäystä

Oma näkemykseni on että suosituksen lisäksi ennusteet on turhan varovaisia. Uskon että 0,85 eps on lähempänä, mutta silti vielä antaa varaa markkinan ja toimintaympäristön riskeille. Arvostus voisi olla se pe 20, kun se ennen raporttia oli Inderesillä 19,5. Nyt on pe 18,5 kun se ennen Q1- rapsaa oli 15e tavoitehinnalla. Pe 20 päästään tp 17e mikä mielestäni pitäisi olla ilman että on turhan varovainen.

Yhtiö hyötyy tekoälystä, oma tekeminen on todella tehokasta, 4% osinkotuotto, varaa yritysostoihin, hyvä pääomantuotto ja firma omaa resilienssiä vaikeassakin markkinassa.

Tänään muuten oli myös n. 700 000kpl blokkikauppa Alman osakkeella. Mielenkiintoinen mauste omistajajärjestelyineen. Uskon tosin että aiemmin tapahtuu liki satavarmasti Almalla isompi yritysosto. Mielenkiinnolla odotan mitä on löydetty!

4 tykkäystä

Tuo 700.000 kpl kauppa lienee ao uutisessa mainittu, eli Otava on saanut luvan Kilpailu- ja Kuluttajavirastolta luvan toteuttaa sen / 40% omistusosuuden ylitys.

Kaupan (?) kunniaksi myös hallituksen PJ vaihdettiin. Lindholm on Otava-konsernin TJ.

Mitä tahansa yritysjärjestelyjä tapahtuisikin niin Otavalla on se ‘the’ rooli. Otava itse on vuosien varrella lisännyt omistusosuuttaan, ja 30% rajapyykissä teki maltillisen / pakollisen lunastustarjouksen, ja ilman mitään preemiota saikin reilun prossan lisää omistusta 9,1euron hintaan kesällä 2023

Alma Media Oyj:n hallituksen puheenjohtaja vaihtuu - Alma Media Alma Media Oyj:n hallituksen puheenjohtaja vaihtuu - Alma Media

Otava on saanut KKV:n hyväksynnän kasvattaa omistustaan Alma Mediassa - Otavakonserni Otava on saanut KKV:n hyväksynnän kasvattaa omistustaan Alma Mediassa - Otavakonserni

Otava Oy kasvattaa omistustaan Alma Media Oyj:ssä - Otavakonserni Otava Oy kasvattaa omistustaan Alma Media Oyj:ssä - Otavakonserni

6 tykkäystä

Mielenkiintoista olisi olla kärpäsenä katossa Otavan hallituksen kokouksissa. Mikä on heidän end game tässä Alma Media -pelissä?

“Strateginen omistus ja Alma tulee säilymään itsenäisenä pörssiyhtiönä” ja mitä näitä jargoneita onkaan aina saatu Otavalta.

Jotenkin ei käy järkeen Otavan toiminta puhtaasti taloudellisin perustein. Onko käynnissä mediakentän konsolidaatio, jossa rationaalisuuden voittaa kunnianhimo ja suuruudentavoittelu? Onko Otava valmis maksamaan kontrollipreemiota (niin kuin nyt tekee) ja jättämään Alman pörssiin “ummehtumaan”? No ainakin ok osinkoa maksellee tulevaisuudessakin. KKV:n mukanaolo ja hpj:n vaihtaminen indikoivat itsessään jotain.

Mariatorp Oy, Ilkka Oyj ja Keskisuomalainen Oyj (osittain välillisesti Ilkan kautta) vaikuttavat tähän tapahtumakulkuun omilla äänillään ja suunnitelmillaan. Alkavatko palaset liikkumaan, kun Ilkassa saatiin nyt osakesarjat yhdistettyä? Joko pohjalaiset jäärät rahastavat ja Almat päätyvät Otavalle hyvään hintaan? Onko paikka hypätä Alman (tai Ilkan tai Keskisuomalaisen) vaunuun ja kerätä konsolidoinnin hedelmiä?

IMO Otavan kannattaisi poistaa Alma listoilta vai onko sittenkin liian iso pala haukattavaksi?

1 tykkäys

Voi olla liian iso pala Otavalle yksinään, mutta miksi ei kumppanin kanssa. Esimerkiksi Herlin