I’ve had a quick look, but haven’t had time to dive in deeply. I’ll continue later in the evening, but here are a few thoughts that came to mind during a quick scroll.

The core of the case is clearly the Radon measurement; otherwise, the product doesn’t seem to have much that would differentiate it in a highly competitive market, with basic CO2 measurement, temperatures, IoT, etc. As a moat, Radon measurement doesn’t seem to be among the worst, as its reliable measurement requires approval from the Radiation and Nuclear Safety Authority (STUK) in Finland and America. Even if competitors were interested in the market, mandatory regulatory approvals in different countries are, in my opinion, a relatively reasonable moat. However, there are still competitors in this field, and Airthings’ product, at a quick glance, seems to be among the most expensive on the market, at least in Finland.

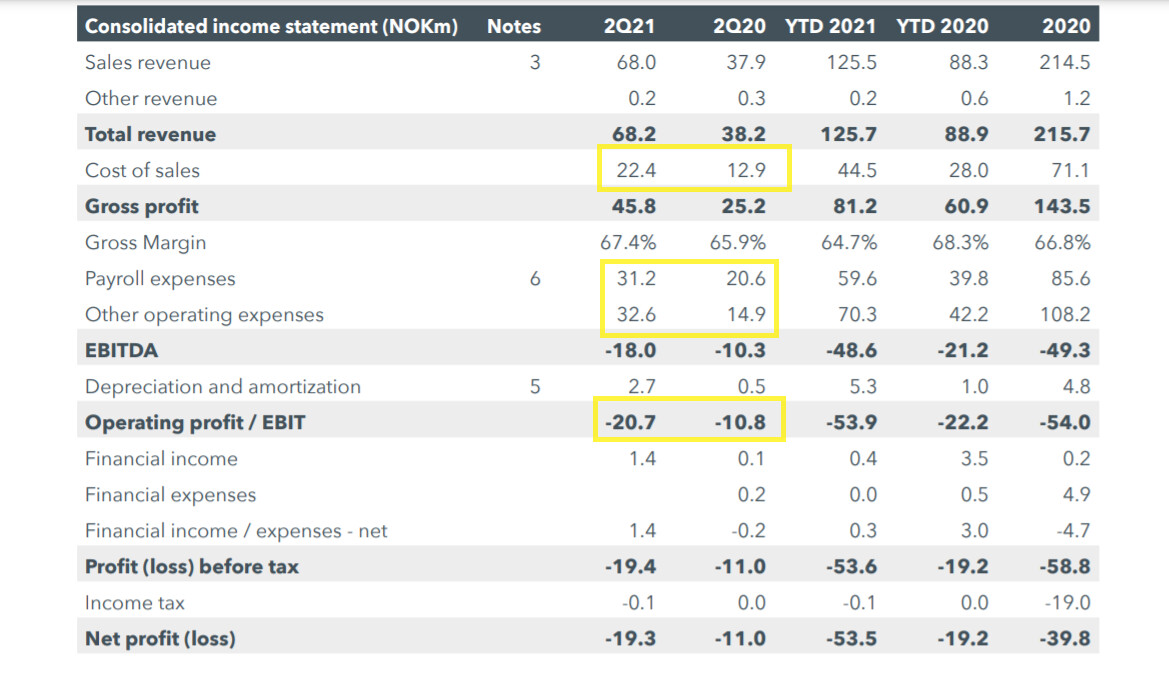

Income statement 21Q2

Although the company has communicated its focus on growth, the income statement lines still catch my eye. Revenue growth is okay, and most of it was organic. Unfortunately, expenses almost always grow proportionally with sales, and the same pattern was observed in the 21Q1 and 2020 reports. Sales don’t seem to scale very well; to sell more products, more marketing, components, and salespeople are currently needed. One solution to this could be to focus more on B2B and professional sales, but for now, clearly most sales come from consumers (Q2 Consumers 49.8M NOK, Businesses 9.7M NOK, and Professionals 8.5M NOK). I’d be interested in the vision for how this operation will eventually turn profitable ![]() .

.

I also wonder a bit about the current valuation multiples, as this is pretty much a full-fledged product company whose operations don’t seem to scale very well. Not that it’s absolutely expensive in the current market, but there’s still a bit to prove. This is a very superficial scratch from my end too; I’ll try to go deeper in the evening.