Mieheni on tässä jo hetken höpötellyt salkkunsa kummallisesta yrityksestä, joka vain tuntuu sinkoavan raketti nousua. Hiukan rennolla otteella hän on sitä sinne ostanut ja nyt kysynkin, mitä mieltä parviäly on tästä.

Vaikuttaa ihanan kalliilta.

Kummallekaan meistä terveydenhuollon ala ei ole erityisen tuttu, mikäli ei lasketa omaa nuoruuden kokeilua sairaanhoidon opiskeluiden parissa. Olisi siis hienoa kuulla, onko näistä tytäryhtiöistä mikään tuttu alan ammattilaisille ja millainen asema niillä on kilpailukentässä.

Tässä kaiveluni tuloksia:

Addvise Group AB on 1989 perustettu ja se on listautunut 1998 Tukholman Nasdaq First North pörssiin. 2010 yhtiö vaihtoi strategiaansa ja päätti alkaa laajenemaan ja kasvattamaan omistaja-arvoa päämäärätietoisesti yrityskauppojen avulla orgaanisen kasvun lisäksi. Tarkoituksena on laajentaa tuoteportfoliota ja laajentua myös maantieteellisesti.

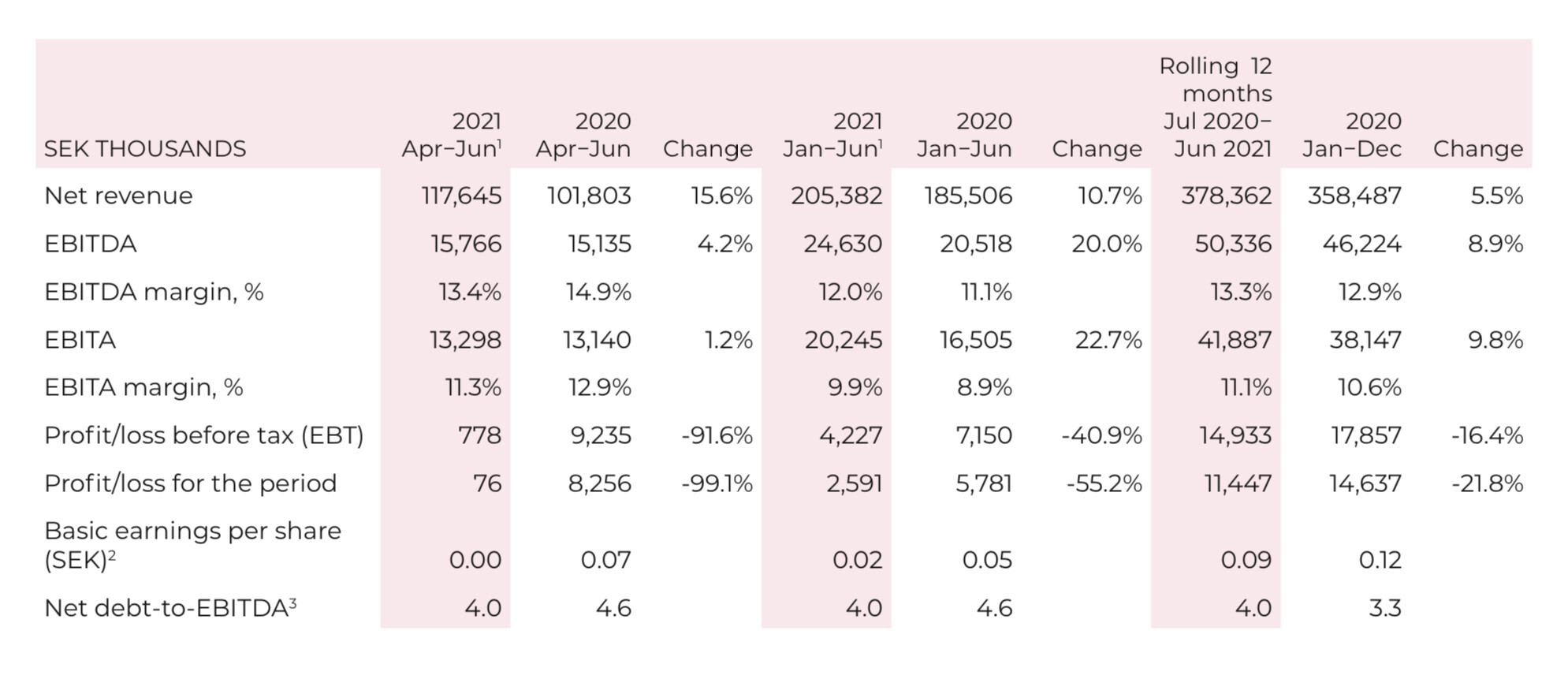

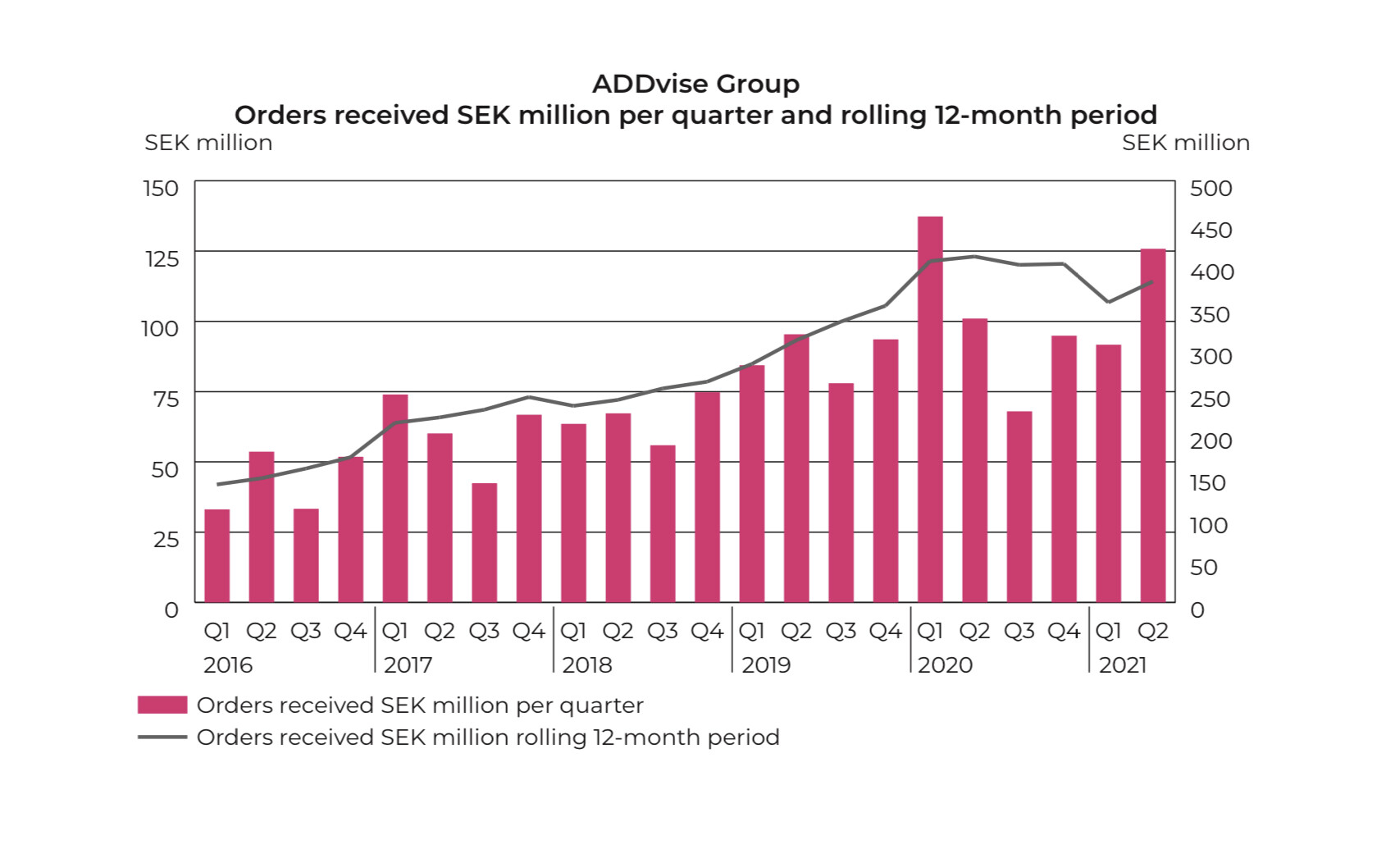

Otteita Q2 23.7.2021 julkaistusta raportista:

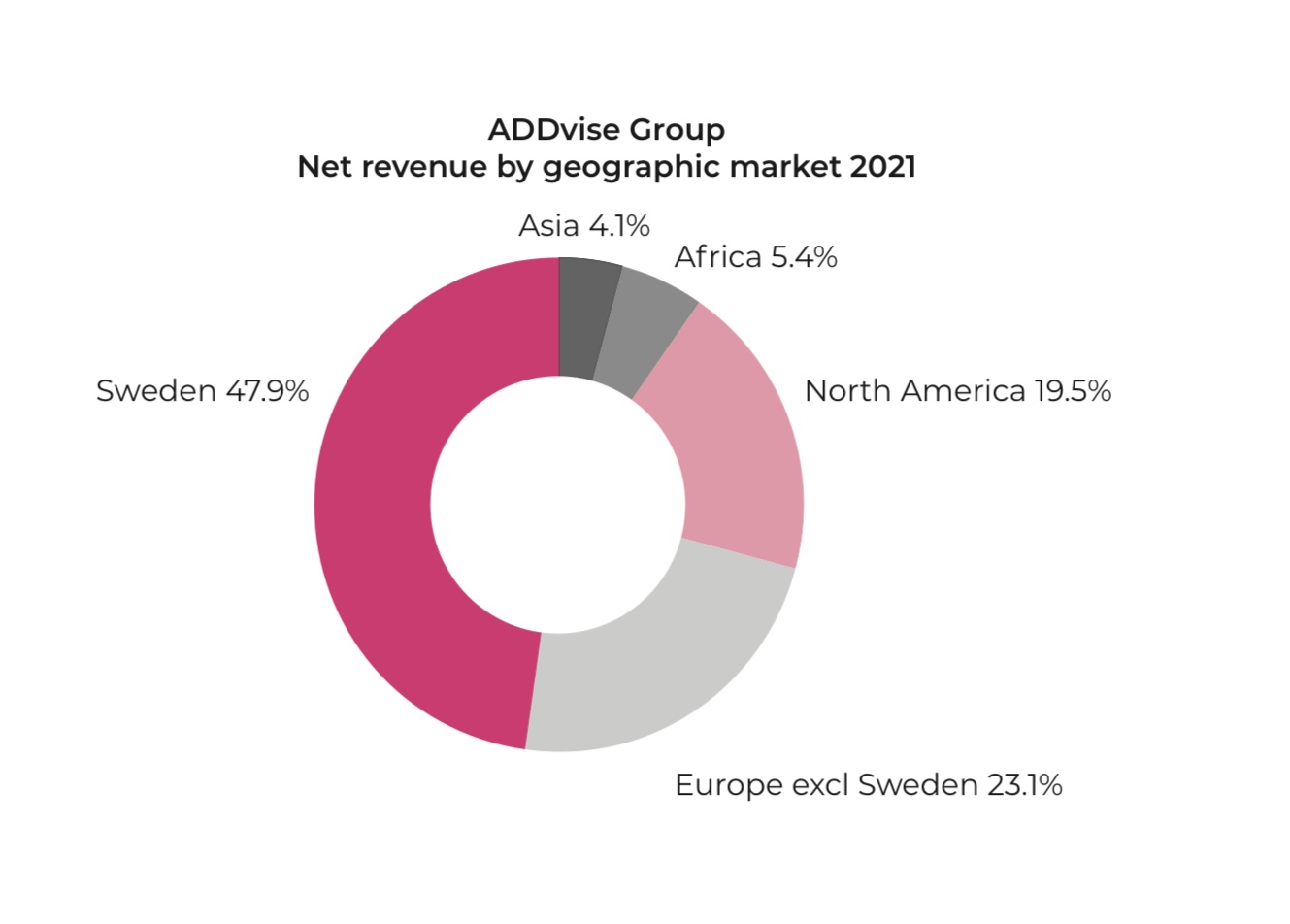

Maantieteellisesti liikevaihdosta liki puolet syntyy vielä Ruotsissa:

Q2 raportissa yritys kertoi parantuneista katteista. Inflaatio ei ilmeisesti aiheuttanut turhia paineita

Itseä kiinnostaa aina eniten tulevaisuus. COVID pandemia on saanut kiireettömiä hoitoja tarjoavien yritysten liikevaihdon heikentymisestä. Q2 raportissa

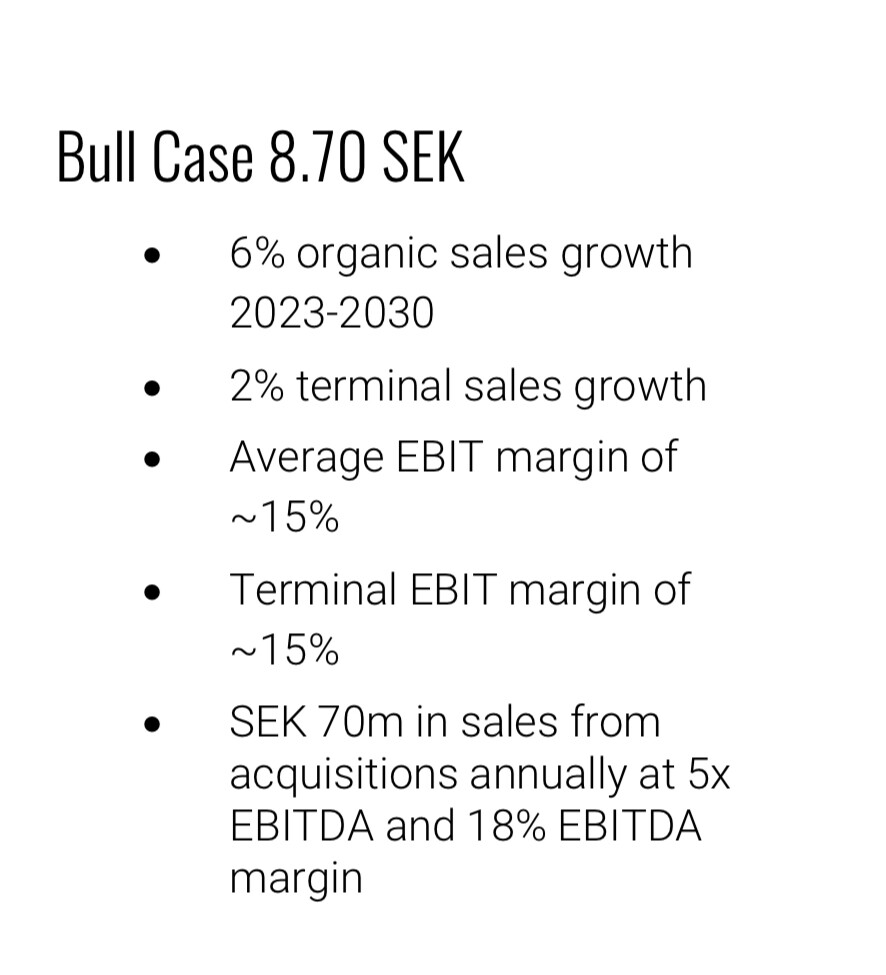

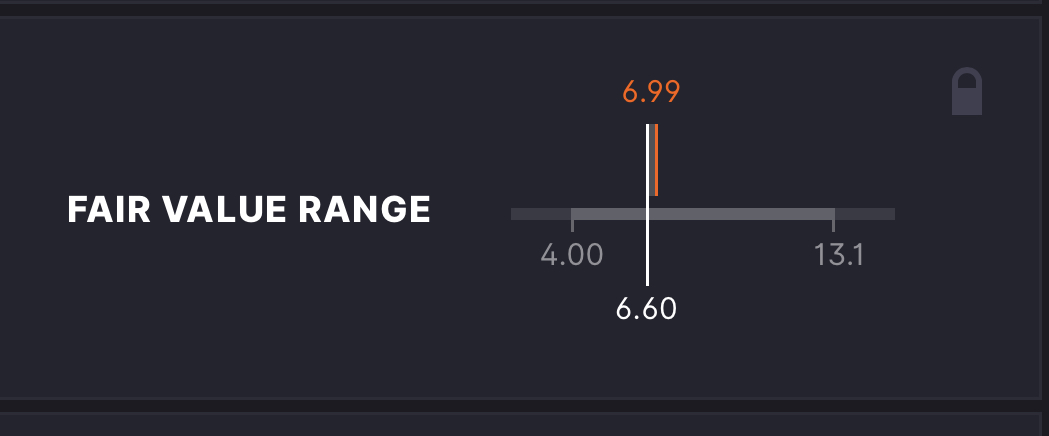

23.9.2021 yritys nosti pitkäntähtäimen EBITDAn 15% —> 20%

Kasvutavoiteet nousivat 20% —> 25%

Tämä on varmasti saanut sijoittajat pukemaan ostohousut jalkaan.

Labra

Tytäryhtiöiden kotisivuja:

Asiakkaita sekä julkisella että yksityisellä sektorilla.

Hettich Lavinstrument

- Toimittaa erilaisia laboratorio välineitä, joiden ainutlaatuisuutta en osaa arvioida pitkäaikaisille asiakkailleen

MRC Modular Room Construction Puhtaantilanhuoneet:

- Yritys suunnittelee, rakentaa ja toimittaa erilaisia rakenteita tiloihin, jotka vaativat korkeaa hygieniaa

- kaupat heinäkuussa 2021

Tillquist

- 125 vuotta vanha mittalaitteiden valmistaja

- Energy, Power Automation, Machine Builders, Process Automation, Photonics and the Electronics Industry.

Kebolabrum

- 40 vuoden kokemus

- suunnittelevat ja toimittavat laboratorioita laitteineen ”avaimet käteen”-meiningillä ja luoaavat olla kaverina jatkossakin.

Healthcare

Tytäryhtiöiden kotisivuja:

AB Germa

- erilaisia tyhjiöpatjoja ja tyynyjä

IM-Medico

- lääketieteellisiä laitteita pääasiassa Ruotsissa, mutta myös kansainvälisesti

- Lääketieteellisten laukkujen suunnittelu yhdessä englantilaisen yrityksen kanssa

- Yrityksellä ei ollut englannin kielisiä sivuja.

Sonesta

- urologin ja gynekologin tuoleja

STI-kirurgisia pöytiä

- c-arm table

- Streamline, Economax ja Max

Sonar Oy

- Sijaitsee Espoossa

- Kuvantamislaitteita terveydenhuoltoon: ultraääni-, röntgen- ja dopplerlaitteet

- Teollisuuden mittalaitteita mm. Endoskopia, digitalinen radiografia, kovuusmittarit, paksuusmittarit, pyörrevirta- ja magnetointilaitteet

- Teollisuuden ja terveydenhuollon isotoopimittarit

- Huolto

- Ilmeisesti laitteet eivät ole Sonarin. Esimerkiksi kuvantamislaitteet ovat Samsungin.

Merit Cables

- kaapeli kauppaa vuodesta 1983

- Yritys sijaitsee Kaliforniassa

MediSuite

- Amerikkalainen verkkokauppa miesten terveyteen erikoistuneita lääkkeitä mm. potenssioireisiin

- ostoaikeista ilmoitettu 05/21 ja kaupoista sovittu 08/21

GraMedica

- Erikoistunut jalkojen ja nilkan leikkauksiin tarkoitettujen ortopedisten implanttien ja stenttien kehittämiseen.

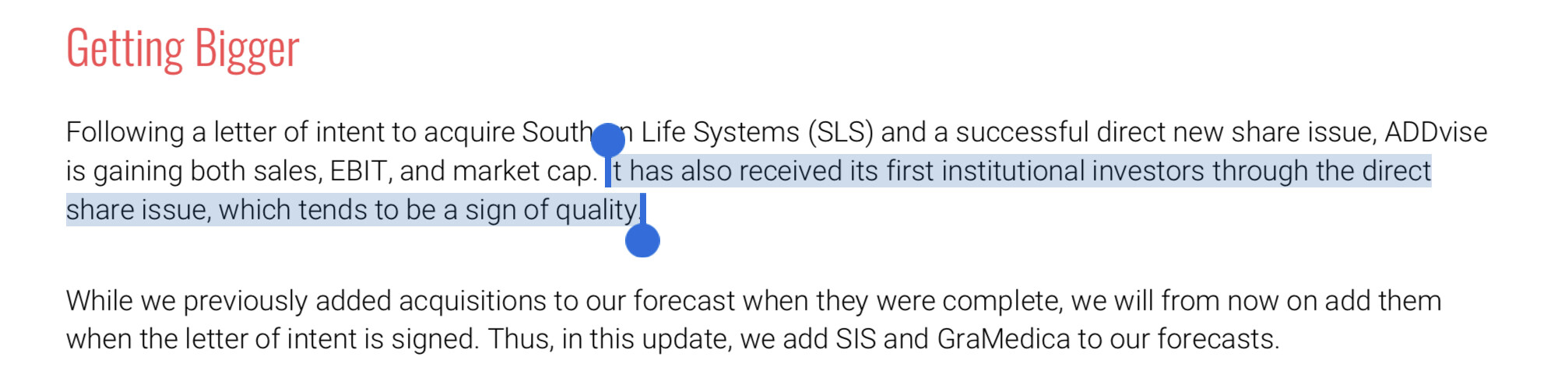

- Viimeisin yritysostos, jonka aikeista ilmoitettiin maaliskuussa ja päästiin sopuun 15.9.

Aika kattava pakettihan tästä löytyy erilaisia terveydenalan yrityksiä yrityksen sisältä. Väkisinkin tulee Boreo mieleen näistä innokkaista yritysostoista ja kurssinoususta. Positiivista on maantieteellinen laajentuminen.