@JNivala Enterprise value is indeed a smarter way for a corporate buyer, i.e., an equity investor, to look at a company. I personally prefer to look at market capitalization, as market capitalization is what I use to calculate dividend yield, P/B ratio, and P/E ratio, although EV-based metrics could certainly be used as well.

As a Master of Science in Engineering, I don’t understand TietoEvry’s business at all, but by looking at the numbers, I think it’s clear that such businesses must exist.

You are also right that better returns on equity were made in the 1990s than today, but by improving efficiency, we can still reach 20%+ figures according to my own estimates.

It may be that TietoEvry is correctly priced at the moment if one examines some key figures. I have studied academic research and investigated what kind of key figures could be used to identify companies that generate excess returns (e.g., P/E, P/B, and dividend yield OR EV/EBITDA and dividend yield OR just dividend yield) enough to dare to claim that TietoEvry will generate excess returns in the future, just as it has historically generated them over the long term (not measured from the peak of the IT bubble to today) but truly over a long period. I have also followed, for example, Kim Lindström, who has been investing for 56 years, has closely followed TietoEvry’s performance over decades, and has bought more Tieto generously over the last couple of years. In addition, I have read Jarkko Aho’s and Karo Hämäläinen’s articles and analyses of the company, and according to their comments, the company is very likely undervalued at the moment.

One could also add, for example, the Phoebus fund to the list; someone could ask in Oldenburg’s blog if he has noticed looking at free cash flow and perhaps even get an answer? Or about a currently quite large owner, Rantalainen Accounting Firm, or well, maybe it’s not worth asking them But you never know about these things, I myself will drop off the list this month if I try to be debt-free for at least some time… the dividend will also decrease next year.. Small companies are more clearly on sale..

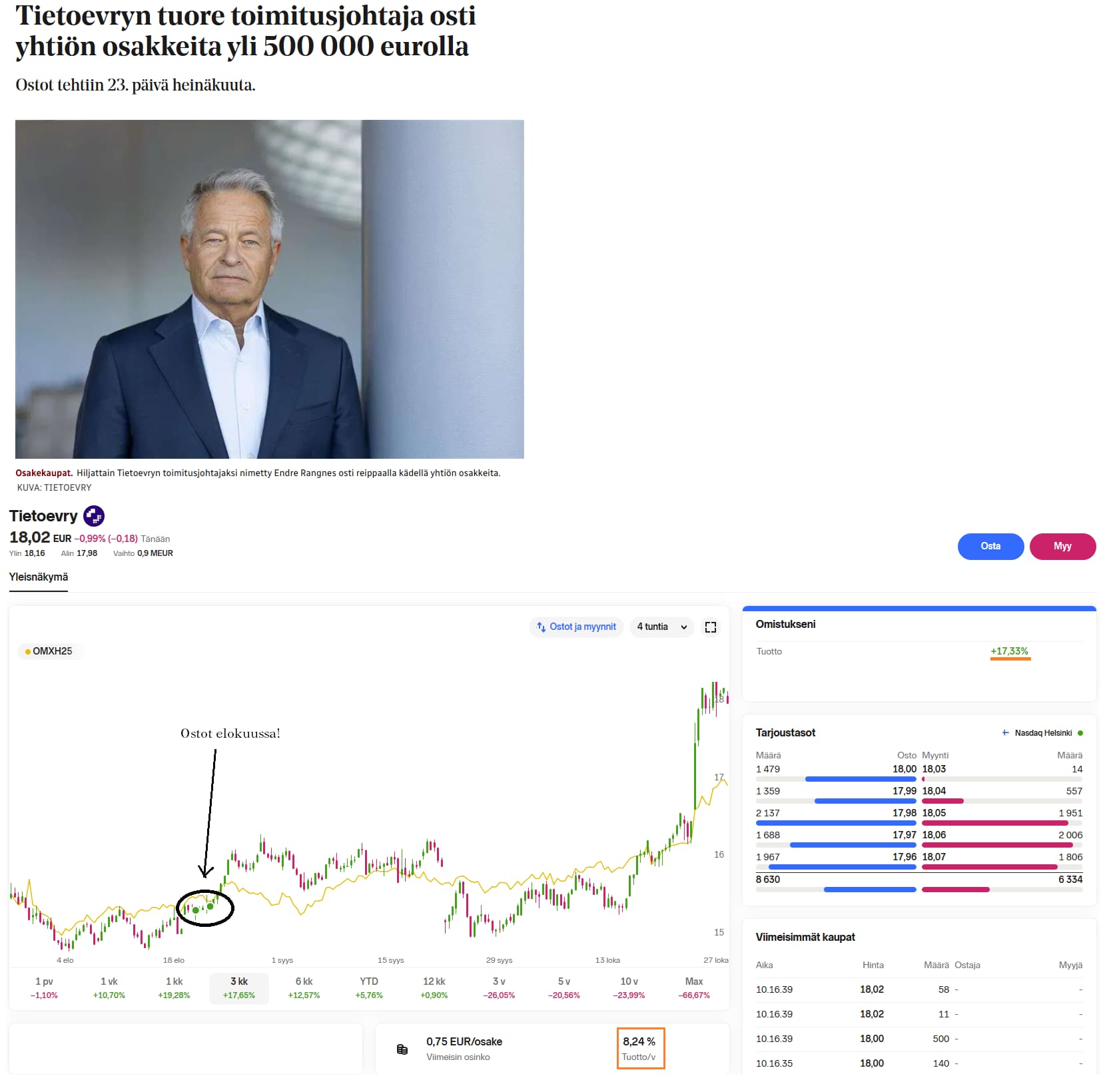

I myself thought of following TietoEvry’s new CEO Endre Rangnes, and so I did. The new CEO put over half a million of his own money into TietoEvry shares in July. It has gone well. Outperformance compared to the HEX25 index and one autumn dividend has already dropped into the account with ~9% dividend yield Note. Not a buy recommendation - make your own decisions!

Tietoevry Care has signed a cooperation agreement with Finland’s leading private healthcare providers Aava and Pikkujätti, Mehiläinen, Pihlajalinna, and Terveystalo. The aim of the agreement is to jointly develop the entire DynamicHealth patient information system to be even more customer-centric. The agreement duration is three years, with an additional three-year option period.

DynamicHealth is used by approximately 60 Tietoevry Care customers, offering comprehensive tools for the needs of private healthcare. It is used by over 50,000 professionals in about a thousand units of Aava and Pikkujätti, as well as Pihlajalinna, Mehiläinen, and Terveystalo. The system covers the most essential functions of private healthcare, from electronic appointment booking and patient data recording to reporting and accounting. Through this cooperation, DynamicHealth will be developed to be even more efficient, user-centric, and digitally advanced for all customers. Thus, it supports high-quality care and enables a smooth customer experience.

Tietoevry’s situation is clearly starting to improve. Good news is slowly emerging. This makes me think, hopefully there won’t be a takeover bid for the company at this price.

So each company chooses its own guidance method, but I’m a bit puzzled by the method Tietoevry has chosen.

In two months, guidance has been updated twice, with the upper end of revenue growth collectively trimmed downwards by 2 percentage points, and the EBITA margins upwards by about 1 percentage point from 12-13% to 13.3-13.8%. The reasons for the changes were mainly the settlement of one legal dispute and, more recently, the faster-than-expected progress of the cost-saving program. Neither, in my opinion, generates much interest, and the changes are quite small.

Wouldn’t it be better to provide guidance a bit more broadly, so that such changes would come to light through “normal familiarization” in some quarterly report, like “okay, good job, let’s continue”? Now I get the impression that they are just focused on calculating every cent precisely, even though the company is involved in the most exciting and investor-interesting topic of recent times (AI) and would at least have opportunities to develop new technology that could accelerate the company’s growth. I don’t know, is there perhaps still room for improvement in the accounting department even after the cost-saving program?

Tietoevry update under CMD, below on financial targets and capital allocation.

A name change is also proposed, dropping ‘evry’ from the name, becoming ‘Tieto’.

The Board of Directors of Tieto (formerly Tietoevry) has approved the company’s new financial targets and capital allocation principles for 2026–2028. Tieto aims for annual revenue growth1) of over 5 percent (compound annual growth rate) in 2027–2028 and an adjusted2) operating profit margin (EBITA) of over 16 percent by 2028. Additionally, the company aims to maintain a net debt/EBITDA ratio below 2.

The new capital allocation principles enable the company to focus on growth while offering attractive returns to shareholders. The company aims to distribute dividends corresponding to 60–80% of net profit. With the remaining capital, the company will repurchase its own shares or pay extraordinary dividends. According to Tieto’s current estimate, the 2025 dividend proposal would be 80% of net profit, adjusted for non-cash impairment charges and cost burdens related to IFRS 5.

I was reading the updated Inderes analysis report after Tieto’s CMD. While reading it, among other things, I was left wondering how or with what figures @Joni_Gronqvist has calculated his 2025e 0.70 dividend/share forecast, when I compared it to what was stated in Tieto’s stock exchange release on 24.11.2025: “According to Tieto’s current estimate, the 2025 dividend proposal would be 80% of net profit, adjusted for non-cash flow-impacting impairments and cost burden related to IFRS 5 standard.”

It does not seem that Inderes’ dividend forecast has been calculated based on the 2025e adjusted EPS of 1.62, but in some other way. Perhaps @Joni_Gronqvist would be keen to explain how or with what net profit-adjusting information he has calculated his 2025e 0.70 dividend/share forecast?

A nitpick. Inderes’ analysis report states that Tieto’s share count is approximately 118.6 million shares. I would,

Tieto (Tietoevry1)) has agreed to sell the Norwegian company Bekk Consulting AS (Bekk) to the private equity firm Axcel. The cash-free, debt-free purchase price (enterprise value) for the divested business is NOK 1,700 million (approximately EUR 140 million). Customary adjustments will be made to the purchase price at the time of closing, and the transaction is estimated to be completed during the first quarter of 2026. In line with Tieto’s new capital allocation principles, the company will use the proceeds from the transaction to reduce debt and distribute funds to shareholders.

Bekk, which employs approximately 600 people and was acquired by ErgoGroup in 2007, is currently part of Tieto Tech Consulting (formerly Tietoevry Create). However, the company has operated independently under the Bekk brand for several years and has a recognized market position in technology and management consulting in Norway. At the end of the third quarter of 2025, Bekk’s revenue for the preceding 12 months was NOK 1,056 million and its operating profit (EBIT) was NOK 150 million.

With its strategic focus, Tieto Tech Consulting has transitioned to a simplified and more integrated operating model. This has been a natural point to assess Bekk’s future, leading to the conclusion that a sale was the best solution.

Reducing debt means that financing costs will decrease, so O’Sinkko will rise even with that measure + a portion of the sales proceeds purely for shareholders

If Tieto announces in a press release (not a stock exchange release) that it has sold a company with a turnover of NOK 1,056 (less than 90 euros) in the previous 12 months, then why would an analyst need to care? And even if we assume that Tieto has failed in this matter too and means 1,056 million kroner, it is still only less than 90 million euros. As Tieto generates 1.86 billion in turnover annually, this barely affects it. The impact is so small that even Inderes doesn’t bother to show that press release on its pages.

This time, Tieto seems to have received a reasonable price for the acquisition. My confidence improved enough that I still believe in a dividend of about one euro.

The Finnish Transport and Communications Agency Traficom has selected Tieto’s Tech Consulting unit (formerly Tietoevry Create) as a provider of quality assurance and testing services based on an extensive tender process during the autumn. The procurement is for a comprehensive service, where Tieto Tech Consulting is responsible for providing the services throughout the entire software development and maintenance lifecycle. The procurement consists of two phases: an implementation project and a continuous service.

The contract period is five years, and it can be extended by two one-year option periods. The estimated value of the procurement for the entire contract period is approximately 24 million euros, and its scope is estimated at 28,000 person-days. Tieto received the highest quality scores in the tender.

The service covers, among other things, testing services, quality assurance development, and performance testing. The quality assurance and testing services primarily target systems implemented by Traficom itself. Test automation will be widely utilized, and the goal is at least 30% cost savings during the contract period. The service scales flexibly according to Traficom’s needs.

Tieto Tech Consulting offers its clients agile and scalable digital development services that support business renewal and growth. Traficom’s procurement strengthens Tieto’s position as a reliable technology partner in the public sector.

Napkin math shows that this will be billed at a commendable hourly rate of €114.3 with the estimated budget and duration. That’s not how it’s actually distributed, but we’re talking about an average of 25 full-time employees. Sounds really good for Tieto. It’s also interesting to consider how the deal came about in such a highly competitive market situation, where prices for public sector projects have been severely driven down elsewhere. Do listed companies have more pricing power, or is Tieto’s combined Finnishness and size still a significant advantage?