You don’t necessarily have to ask these, maybe they’re a bit silly questions, but I posted them anyway.

Suominen has been striving to improve its profitability for several years, but the earnings development has been even slower than expected. What were the most important lessons learned and concrete actions taken in Q4 or in 2024 in general that could support a sustainable improvement in profitability in 2025? Does management see light at the end of the tunnel, or are there still significant challenges + difficult times ahead?

The company’s industry seems challenging in terms of making money. Does the company intend to develop or innovate something new for the industry… or otherwise renew itself? I’m just wondering if Suominen will remain an eternal plodder.

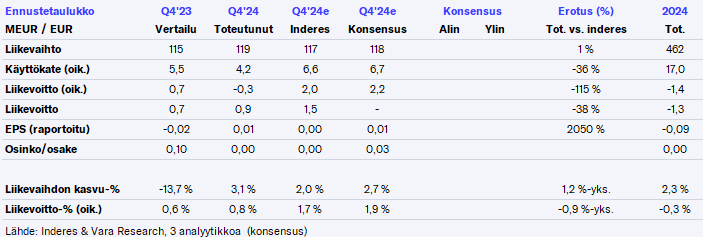

Suominen’s result, similar to Q3, fell short of the previous year, even though expectations were (again) higher. However, the explanation had changed; instead of Q3’s operational problems, tighter competition and rising raw material prices were now lamented. At the full-year level, they again just barely reached the guided improving adjusted EBITDA, but at the operating profit level, losses were made for the third consecutive year. The dividend was cut to zero as expected, given the losses and a tightening balance sheet. The guidance is again for an improving adjusted EBITDA in 2025, but forecasts will likely have to be cut once again.

Here’s a fresh interview, where I also tackled, slightly rephrased, questions from @Sijoittaja-alokas, including one that was left unasked in the previous quarter.

Suominen’s Q4 result, as well as for the full year 2024, was weak. Although the company guides for an improving result this year, we believe the result will remain loss-making.

Quoted from the report:

Suominen’s net sales grew by 3% in Q4, largely driven by improved sales prices and product mix. Volumes decreased slightly, as volumes from lower-cost production countries were, according to the company, directed more towards the European market. Geographically, however, Suominen grew in Europe, and in the Americas, net sales were at the comparison period’s level. Net sales were roughly in line with forecasts.

Here are Rauli’s preliminary comments for Wednesday’s Q1 release.

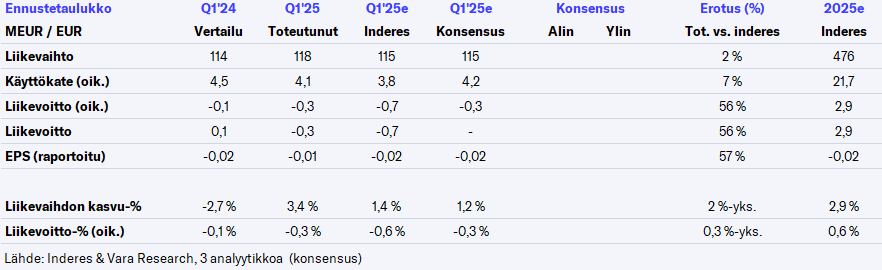

Suominen will report its Q1 results on Wednesday around 9:30 AM. We expect Suominen’s adjusted EBITDA to weaken slightly from the comparison period and to be roughly at the level of the two preceding quarters. The guidance for an improving 2025 adjusted EBITDA is likely to remain unchanged. At the net income level, we expect a loss for both Q1’25 and the full year, similar to the previous three years.

The figures are slightly better than our forecasts, but still at a dismal level, of course. That EUR 10 million savings program is already significant in magnitude, but it naturally raises questions as to why it wasn’t done earlier and whether the outlook is now weaker if such a big move is being made…

The full-year guidance for improving adjusted operating profit was unchanged, but at the net income level, this will still be loss-making this year, at least in our forecasts.

Suominen’s CEO Tommi Björnman was interviewed by Tomppa.

Topics:

00:00 Introduction

00:11 Key highlights of the beginning of the year

01:20 Decline in result from the comparison period

02:14 Impact of tariffs on raw materials

04:19 Erratic trade policy creates uncertainty

06:00 Suominen launches a significant cost-saving program

08:14 Indebtedness is high

09:58 Guidance leaves room for improvement for the rest of the year

Suominen’s Q1 result weakened from the comparison period as the market situation remained challenging. Despite the new savings program, we believe the company’s situation remains difficult and the stock’s valuation is high.

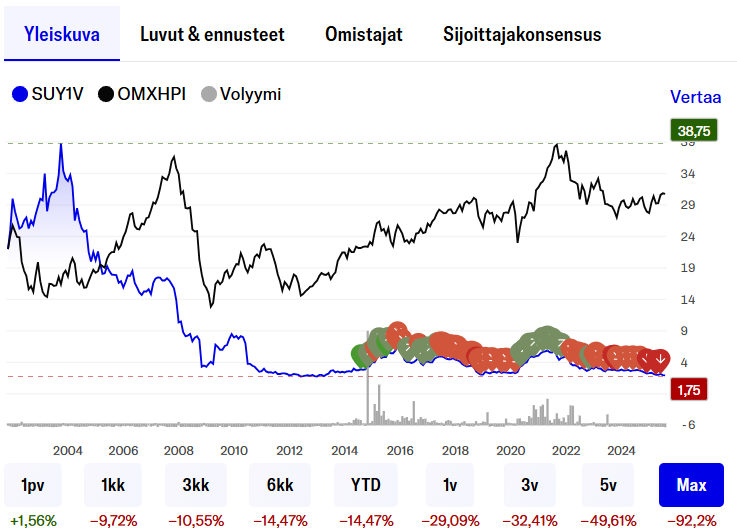

Throughout its stock market history, Suominen has managed to cause its shareholders headaches and a decline in value.

The position of a bulk subcontractor in the value chain has hardly been profitable at any point. Occasional profitable years have been followed by difficulties and crises.

I have often wondered why Suominen doesn’t boldly “reset” its business model and start selling directly under its own brand in consumer and B2B markets? What could go worse by taking control of the value chain instead of meagerly scraping by on thin margins in the mass production of nonwovens?

Huhtamäki has succeeded in its own category, but Suominen simply cannot sustainably turn the ship around.

From Suominen, in connection with Thursday’s results, we will this time get an interview with CFO Janne Silonsaari, who has served as acting CEO for the summer. If you have any questions in mind for them, please send them in.

Here are Rauli’s preliminary comments as Suominen publishes its Q2 results this Thursday.

We expect Suominen’s adjusted EBITDA to weaken slightly from the comparison period and to be approximately at the level of the two preceding quarters (EUR 4 million). The guidance for improving 2025 adjusted EBITDA is likely to remain unchanged, although there is a downside risk. At the net result level, we expect a loss for both Q2’25 and the full year, similar to the previous three years.

Have you already figured out how the company could address permanent structural costs and efficiencies, or is the emphasis more on shorter-term efficiency measures rather than structural matters? Whichever it is, of course, significant results cannot be expected instantly.

Rauli interviewed Suominen’s CFO Janne Silonsaari well.

Topics:

00:00 Start

00:13 CFO Janne Silonsaari introduces himself

00:58 Reasons for revenue decline

03:03 Impact of tariffs on sales and raw material procurement

05:51 Margin development

07:00 Savings program and improving profitability

08:55 Balance sheet situation

12:34 Reaching guidance

I phrased this a bit differently, but the answer was roughly that we’ll do these planned actions first, but surely the CEO starting next week will come up with new ways to improve profitability. Of course, that’s why the CEO was changed in the first place, because the results have been dismal for four years, let’s see if Mr. Heaulme can find some philosopher’s stone for this struggle.