Rauli has prepared a new company report on Suominen right after Q2.

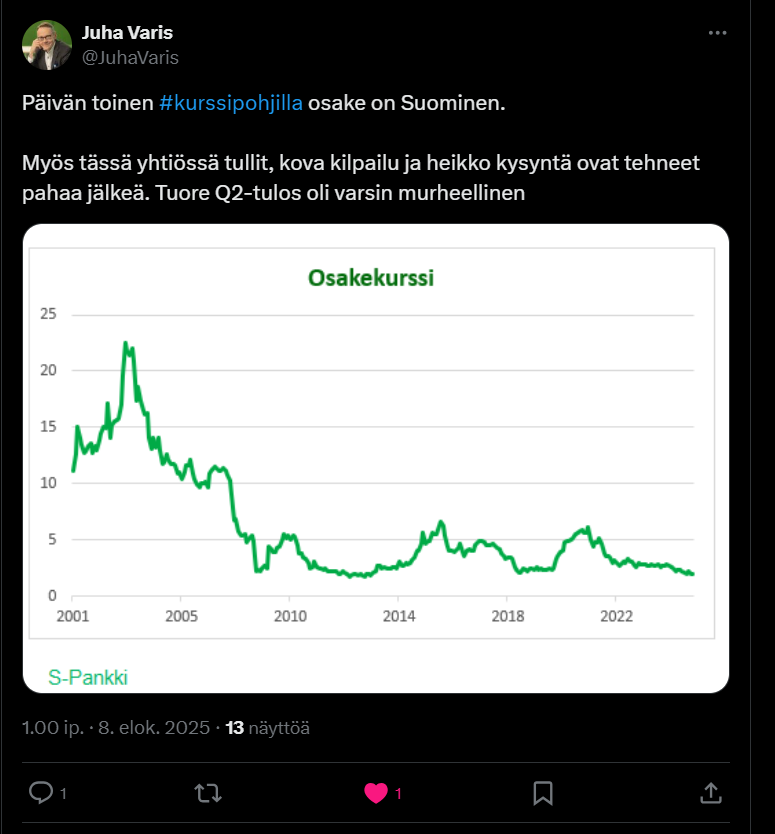

Suominen’s Q2 figures were weak, as the indirect impact of tariffs hit its demand in the USA. The company reiterated its guidance for improving full-year results, but we lowered our forecast below the guidance. We believe the company’s situation remains challenging, and the stock’s valuation is high.

A sad (stock market) story both from the company’s and owners’ perspective. Probably the only sensible option is to sell either to private equity investors or an industrial buyer.

Hopefully, this task given to the new CEO (he gave it to himself when coming from the chairman position).

Rauli and Tomi discussed Suominen and its performance and attractiveness.

Topics:

00:00 Start

00:18 Years after COVID have been difficult

03:07 Early year even more challenging than the previous year

03:54 Pricing power put to the test

06:47 Change of CEO

08:51 Mergers and acquisitions and industry consolidation

10:04 Indebtedness elevated

11:55 Efficiency measures should be visible by year-end

14:00 Valuation not attractive

Suominen Corporation, Inside Information, October 15, 2025, 2:30 p.m. EEST

In its 2024 financial statements release, published on March 5, 2025, and its half-year report, published on August 7, 2025, Suominen estimated that the company’s comparable operating profit (EBITDA) in 2025 would improve from 2024. Suominen now expects that its comparable operating profit (EBITDA) in 2025 will be lower than in 2024.

“Although demand for nonwovens has historically been stronger in the second half of the year and our cost-saving measures have started to yield results, the recovery of volumes, mainly due to the fluctuating customs situation in the United States and related supply chain disruptions, progressed slower in the third quarter than we had previously estimated. In addition, two significant events affected our U.S. plants in the third quarter: due to an equipment breakdown at one plant, one production line was out of operation for an extended period and caused additional costs, while a major water damage incident in the storage area of another plant led to the spoilage of products in stock. An investigation is underway regarding the damages to seek potential compensation, but the timeline for receiving it is uncertain. Third-quarter net sales were EUR 99.8 million and comparable operating profit is estimated to be approximately EUR 3.4 million. As a result, we estimate that the full-year comparable operating profit will be lower than the 2024 level," states Suominen’s President and CEO Charles Héaulmé.

New Outlook: Suominen expects that its comparable operating profit (EBITDA) in 2025 will be lower than in 2024. In 2024, Suominen’s comparable operating profit was EUR 17.0 million.

Previous Outlook: Suominen expected that its comparable operating profit (EBITDA) in 2025 would improve from 2024. In 2024, Suominen’s comparable operating profit was EUR 17.0 million.

Suominen will publish its third-quarter interim report on Wednesday, October 29, 2025, at approximately 9:30 a.m. EEST.

Rauli has published a new company report after the negative outlook.

Suominen issued an expected profit warning regarding its results and stated that the full-year adjusted operating profit would fall short of the comparison period. The warning and the preliminary information provided on Q3 results were largely in line with our expectations. We slightly lowered our forecasts. We upgrade the recommendation to ‘reduce’ (previously ‘sell’) and lower the target price to 1.6 euros (previously 1.7e) due to slightly lower forecasts.

Rauli interviewed Suominen’s new CEO Charles Héaulmé regarding Q3

Topics:

00:00 Introduction

00:14 Charles Héaulmé starts as the new CEO

09:08 Scaling Suominen to the next level

11:21 Main highlights of Q3’25

13:37 Outlook and drivers for the fourth quarter

16:35 Past efficiency measures and their results

20:13 Building a culture of winners

An impressive performance by Charles Héaulmé. It instilled confidence in the future. I bought Suominen shares. Seems like a good value - strong presence in the USA. I see that as a strength.

Rauli has prepared a new company report following Suominen’s Q3. Suominen’s Q3 report contained limited new information after the preliminary data and guidance cut provided by the company two weeks ago. The new CEO will launch some kind of profitability program. In our opinion, this is necessary, considering the company’s loss-making earnings level. However, we believe the company’s valuation already prices in a higher earnings level than our forecasts, and thus the return expectation remains weak. We reiterate our Reduce recommendation and a target price of 1.6 euros.

We value Suominen using earnings and balance sheet-based multiples and a DCF model. The earnings improvement we forecast will go into digesting the multiples in the coming years, and even with a significantly better earnings level (2027), we consider the valuation high. With the dividend being zero in the coming years, it also does not offer support for the return expectation. Thus, we see the return expectation as weak.

I agree, and it’s definitely worth listening to if Suominen interests you at all. I don’t know if even Charles can turn this around, but at least he seems to have a good grip, and new, perhaps big, actions are coming. We’ll see in the coming years how far they go.

Here are the preview comments from Rauli ahead of Suominen’s Q4 result on Jan 29.

Suominen will report its Q4 results on Thursday, January 29, 2026. We expect the company’s year-end result to have remained weak, as the production issues that emerged in Q3 were still partly reflected in the final quarter. The main focus of the report will, however, be on 2026 and the measures potentially presented by CEO Charles Héaulme to turn profitability back towards growth. We expect the company to guide for an improved result for 2026.

Let’s mention here that since the current Chairman of the Board, Heaulme, has stepped up as CEO, the leadership of the board will naturally change at the spring Annual General Meeting. Joining the board as a new member to take on the role is Ville Vuori, who is currently the Chairman of Aspocomp and Incap. A figure unknown to me, at least.

CEO Heaulme already promised in the Q3 interview that some new efficiency measures would be coming on a relatively fast schedule (this could well be in connection with Thursday’s results), with a strategy update following in the summer. Thus, the new Chairman will be joining these processes mid-way, and the initiative in them seems to rest with Heaulme and his team.

By the way, there will be the usual CEO interview in connection with Thursday’s Q4 results – if you have any questions, feel free to send them our way. In the Q3 interview, we already covered quite a lot of Charles’s general views on Suominen.

A miserable Q4 from Suominen today: revenue fell sharply and adj. EBITDA was less than half of expectations. As expected, the company announced a much-needed new and broader efficiency program. Below are comments from CEO Heaulme; more of our thoughts will follow in tomorrow’s report.

Rauli has published a new company report on Suominen following Q4

Suominen’s Q4 figures were clearly weaker than our forecasts. In line with our expectations, the company announced a new multi-year and extensive efficiency program that supports our forecasted earnings growth for the coming years. However, in our view, the stock’s valuation is already pricing in a level of earnings better than our forecasts for the next few years. We estimate that, in addition to this, the company may need equity financing to implement the efficiency program and support the balance sheet. We are lowering the target price to EUR 1.3 (prev. EUR 1.6) due to the weakened forecasts and updating our recommendation to Sell (prev. Reduce).

Rauli has written a new company report on Suominen

We believe that the increase in the price of oil-based raw materials will hit Suominen’s results in the coming quarters and keep the earnings level weak. Due to an already weak balance sheet and deteriorating forecasts, we believe the company will acquire equity financing this year. In this report, we added a hybrid bond to our forecasts. Due to lower forecasts, we lower our target price to 1.1 euros (previously 1.3e), but due to the sharp decline in the share price, we raise our recommendation to reduce (previously sell).