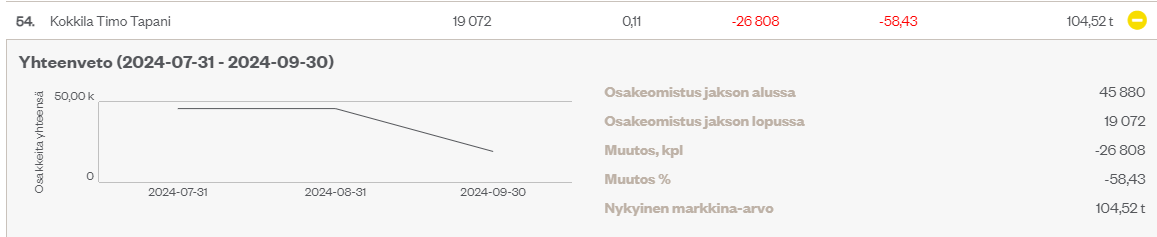

A good block for sale on the SRV side for anyone interested, perhaps genuine Kokkila?

Well, over 950,000 shares still remain with Havu Capital for the same gentleman if that’s what it’s about.

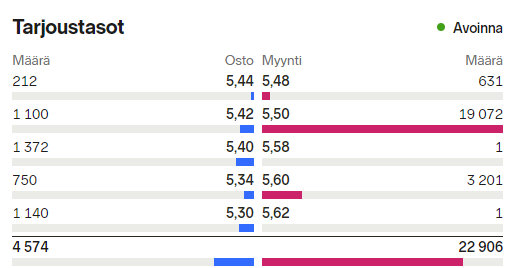

Anyway, a small trim indeed to the total stake, although it’s always hard to find a buyer through the exchange for a low-volume stock.

Quite a sizable hall; check the decision for more information about the project and the selection process in general.

Decision

The preliminary scope of the project is approximately 13,000 gross m2. According to the decision made by the Hyvinkää City Board on October 9, 2023, the city will allocate 45.6 million euros for the implementation of the Hangonsilta multi-purpose hall.

Procurement notice

The preliminary scope of the procurement is approximately 13,000 gross m2, of which the sports hall accounts for about 9,800 gross m2 and the university facilities for about 3,200 gross m2. The city has allocated a budget of 45.6 million euros for the project. The design and construction of the project are scheduled for 2024–2027.

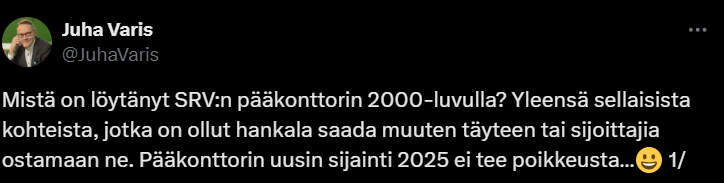

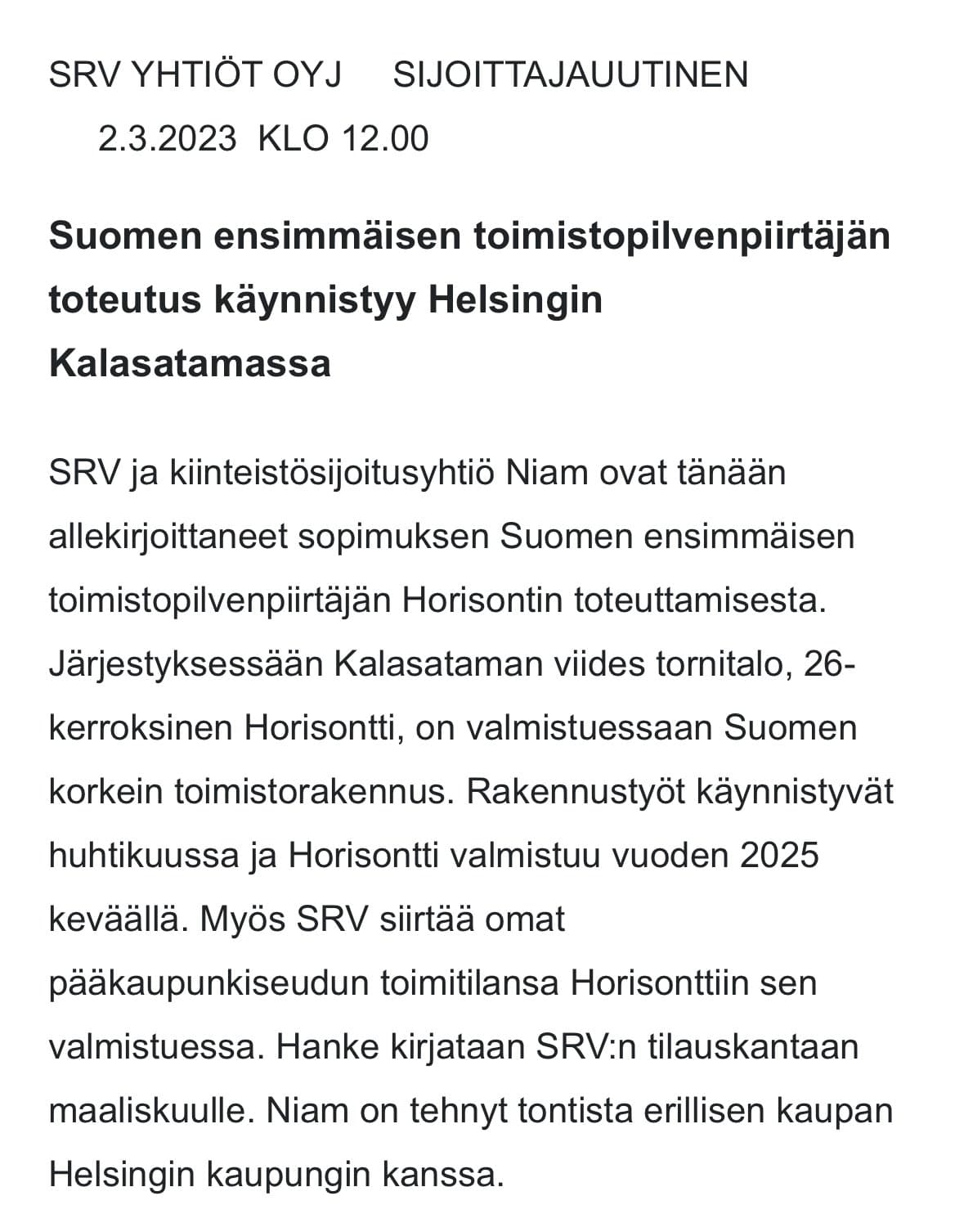

Well, the entire project wouldn’t have gotten off the ground if SRV hadn’t signed a lease there. Or, of course, it would have if another anchor tenant of the same size had been found. But I suspect SRV turned over every stone themselves, and moving their own headquarters to Kalasatama was the solution when no other tenants were found. And apparently, the same ”trick” was used with their current headquarters, Derby, in 2012–13. There’s nothing wrong with that per se, though one can certainly wonder how good a price it was from SRV’s perspective when NIAM bought Horisont.

Olli is previewing the situation as SRV releases its Q3 results on Thursday, 24 October 2024.

We expect revenue to have risen strongly from the level of the comparison period, driven by an increase in business premises construction volumes. We expect the overall result to still be at a low level. In our estimation, the result is low, as the majority of the current revenue comes from low-margin business premises contracting and the housing market remains quiet. The construction market has remained quiet throughout the year, but the company’s order flow has picked up and the first own-development residential projects have already entered the marketing phase. We are monitoring comments for a possible pick-up in the market turnaround.

Greater variance in revenue, but the bottom-line figures are very close to each other.

A pickup in residential construction is a prerequisite for a clear improvement in results. Cash flow will be boosted more quickly by the realization of the Oulu hotel project, which involves a significant amount of receivables by any comparison, and hopefully also by the sale of the final holding in Russia.

An official press release was also issued regarding the Hyvinkää project

SRV and the City of Hyvinkää have signed an agreement for the implementation of the Hangonsilta multipurpose arena. The total cost estimate for the project, which will be carried out as a collaborative project management contract, is EUR 45.6 million, of which SRV’s share of the contract is EUR 32–40 million. The project will be implemented as a joint procurement between the City of Hyvinkää and Laurea University of Applied Sciences.

The project will begin with a development phase and will be added to SRV’s order backlog when construction begins, estimated in the spring of 2025. The project further strengthens SRV’s leading position in collaborative contracting.

SRV managed to get its interim report together and is specifying its guidance.

The guidance range is still wide, even though the range has at least been narrowed down.

As for the operative operating profit guidance, since the figures are small, the guidance is also a bit all over the place.

Based on the guidance specification for Q4 2024:

revenue is 0-15% vs Q3 2024, or 0-15% vs Q4 2023 (Q4 2023 was 182 MEUR)

operative operating profit is -100%…0% vs Q3 2024, or -100%…+100% vs Q4 2023 (Q4 2023 was 2.4 MEUR)

4Q 2024:

Revenue 720-750 MEUR => 4Q: (720-537)…(750-537) => 183…213 MEUR

Operative operating profit 7-12 MEUR => 4Q: (7-7.3)…(12-7.3) => -0.3…4.7 MEUR

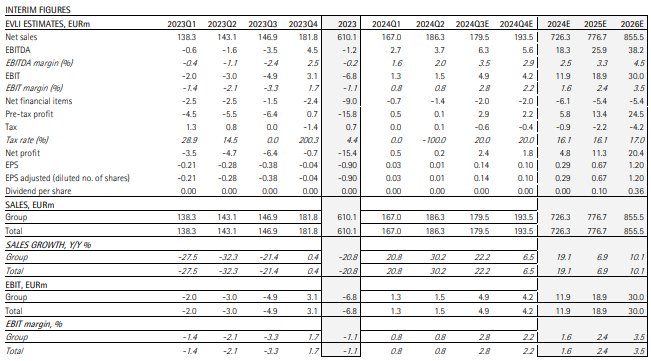

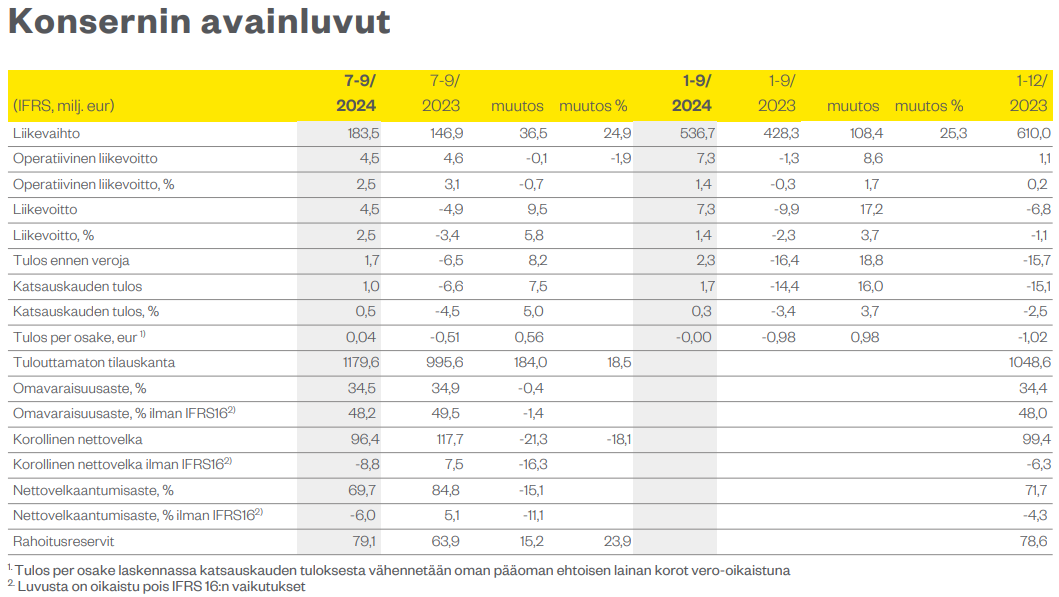

July-September 2024 in brief:

Revenue was EUR 183.5 (146.9) million (+24.9%). Revenue grew in alliance and project management contracts in business premises and infrastructure construction.

Operative operating profit was EUR 4.5 (4.6) million and operating profit was EUR 4.5 (-4.9) million. Increased volume in business premises and infrastructure construction compared to the comparison period had a positive impact on operative operating profit. On the other hand, the continued low volume of housing construction, which was also focused on lower-margin competitive and negotiated contracting, had a negative impact on operative operating profit. Operating profit for the comparison period was weakened by the loss on the sale of SRV Russia Oy and its subsidiaries.

Result before taxes was EUR 1.7 (-6.5) million.

The equity ratio was 34.5 (34.9% 9/2023)% and the gearing ratio was 69.7 (84.8% 9/2023)%. Calculated without the impact of IFRS 16, the equity ratio was 48.2 (49.5)% and the gearing ratio was -6.0 (5.1)%.

The order backlog at the end of the period was EUR 1,179.6 (995.6) million. The sold share of the order backlog was 93.5 (92.1)%.

In July-September, new agreements were signed for EUR 273.9 (132.5) million.

Emission intensity (scope 1 and 2, rolling 12 months) decreased and was 3.0 (3.1) tCO2 / EUR million revenue at the end of September. The level of emission intensity has stabilized, but varies moderately as revenue and project phases change.

Guidance specification:

The Group’s revenue for 2024 is expected to grow compared to 2023 and be EUR 720–750 million (revenue in 2023: EUR 610.0 million). (previously: The Group’s revenue for 2024 is expected to grow compared to 2023)

Operative operating profit is expected to improve compared to 2023 operative operating profit and be EUR 7–12 million (operative operating profit in 2023: EUR 1.1 million). (previously: Operative operating profit is expected to improve compared to 2023 operative operating profit)

Here are Olli Koponen’s quick comments on SRV’s Q3 results

SRV announced a Q3 report on Thursday with figures slightly better than our expectations, but the specification of the earnings guidance and the outlook left a weaker impression of the report. Revenue from business premises construction was again stronger than expected, and the entire group’s revenue rose by more than 20%. Thanks to the strong revenue, the result was on par with the comparison period and exceeded our expectations. The guidance ranges were specified; the revenue range exceeded our expectations, but the earnings guidance range fell clearly short of our expectations. Most significantly, the outlook remains challenging, and the delay in the market turnaround is slowing down what SRV describes as the significant expected earnings improvement.

00:00 Introduction

00:14 Q3’24

01:14 Flexibility of the business model

02:45 Margin structure of the order book

04:10 Profitability outlook

04:48 Financial targets and market outlook

07:40 Exit from Russia

It is obviously clear that a significant improvement in the company’s operating profit and the target of EUR 50 million requires, above all, residential construction.

According to the company’s announcement, the market recovery is being delayed.

The company previously assumed the recovery would happen faster, which partly shows how difficult it is even for SRV to predict the market recovery. This inevitably raises the question of how well SRV can predict the prolongation of the recovery, given that their previous forecast didn’t quite hit the mark.

Market recovery is based partly on facts, by which I refer to the need for housing and the emergence of buyers in the market. The former is obviously a numerical calculation, but the latter is also very much about psychology, regarding which it is very difficult to estimate in advance when the “darkness” will disappear and the sun will rise. I have already lived through several market swings from darkness to light. It has always happened quite suddenly and unpredictably. At the moment, it is hard to estimate what piece of information or what 12-month Euribor interest rate level will trigger interest in people to buy or change homes. It could happen as early as December or in mid-February, when the sun starts shining after 5:00 PM again and people’s spirits lift.

Buying a home for one’s own use is surprisingly much about psychology.

Here is a fresh company report on SRV from Koponen.

We reiterate our Reduce recommendation and target price of EUR 5.00 for SRV following the company’s Q3 report. SRV’s revenue and earnings were better than our expectations in Q3, but the delay in the market turnaround was reflected negatively in the outlook. A clearer turn in the business cycle will take years, which will keep SRV’s earnings at a low level for the coming years. SRV is financially in a good position for an improving market, but it will be a long wait and, in our view, the short-term expected return is not worth the wait.

Quote from the report:

On the positive side for SRV, there is still enough work in business premises construction, although private demand remains weak there as well. Interest rates are still high, and demand from investors, consumers, and institutions alike is waiting for a clear recovery.

Sometime in March 2023, I read a then-fresh extensive report where Olli was expecting residential construction and the market to pick up in late 2023 / during H1 2024. I challenged that a bit here in the thread even then, and soon we’ll be a year behind that schedule. This is not meant as criticism of Olli; forecasting is just very difficult, especially about the future.

It feels like no one, not even the professional economists at the Confederation of Finnish Construction Industries, can credibly predict that market recovery, though there are plenty of views to be found.

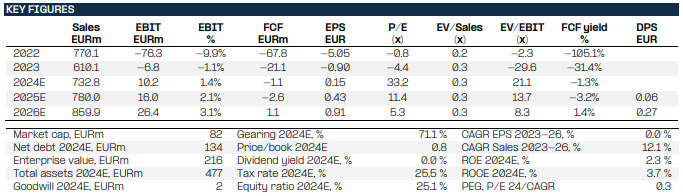

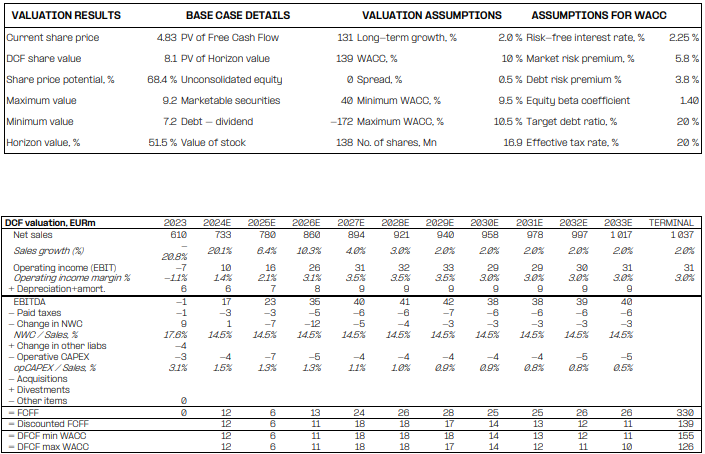

Evli has published a new SRV report (43 pages)

Target price remains unchanged at EUR 5.0, based on 6% growth and 2.1% EBIT in 2025.

The potential of future years is not relied upon.

The 2026 estimate shows that with 10% growth (partly due to the return of self-developed residential construction) and 3.1% EBIT, the P/E would drop to 5.3.

With this estimate, the valuation was -30%…-50% vs “peers”.

DCF estimate EUR 8.1, if EBIT margin were to rise and stabilize at 3.0% or slightly above.

A success story almost ready, just needs some work…

HOLD with a TP of EUR 5.0

Our estimates for 2024E do not support the current pricing. For 2025E the valuation is neutral, yet the potential beyond 2025 remains high. Further evidence of the company’s turnaround and pick-up in the residential construction market are needed for us to put greater emphasis on the long-term potential. With only small adjustments to our estimates, we keep our TP and recommendation intact.