This is financial jargon that is almost impossible for an outsider to understand.

I’m a bit puzzled by the timing. No new self-initiated projects are likely to start for the next month, and current cash reserves + infrastructure sale price + Tower Hotel sale price - VVL redemption should mean cash reserves + €50 million.

Why is €20-30 million in borrowed money needed right now? Or is it customary to draw down these loans so much upfront to accumulate interest expenses?

SRV’s equity ratio will decrease significantly upon the repayment of VVL, unless replacement loan capital that can be classified as equity is acquired. One of the loan covenants is an equity ratio of over 30%, which SRV will not meet after the loan repayment without compensatory measures.

57 million euros of that hybrid bond (vvk-hybridi) is outstanding, according to SRV’s pages.

If that were halved with this new hybrid, then it is certainly a step in a more secure direction regarding dilution, and @ValkoinenPeura probably correctly estimated the reason above.

The interest rate of the current hybrid is 4.875%, it might be challenging to get a hybrid at that price.

Grok identified two realized hybrids in Helsinki, YIT (8.5%) and Relais (7.875%).

Now, of course, a hybrid for half of the current amount is being sought, and perhaps it has been concluded that the rest will be handled from other funds / financing.

EDIT: in addition to the above, Rapala just issued a 25 million euro hybrid loan, interest rate 9.00%

Now, thinking with common sense, this is utterly foolish if the company has to take out new loans (which is what it really is, regardless of its accounting classification) to satisfy the covenant clauses of other loans.

Wouldn’t it be better for the old financiers the less debt (regardless of its accounting status) the company actually has?

And doesn’t VVL also mean that the company’s loans relate almost solely or even exclusively to housing company loans and plot loans, i.e., real estate investments?

The financiers of the plots surely have mortgages on the plots as collateral, and those who have lent to housing companies surely have mortgages on the plots.

Regardless of the accounting classification of the loan, these other loans don’t even compete with secured loans, which presumably mention a minimum equity level.

Am I completely mistaken, and please guide me towards the light of knowledge from this darkness.

It’s not crazy at all if SRV can buy back those loans with a nominal value of €57 million at a clear discount and at the same time issue new loans, e.g., €30 million. In SRV’s balance sheet, those €57 million loans are recorded as being worth €33.5 million:

We’re getting to the point of questions again where I, at least, can’t be bothered to explain these things in simple terms. Learn things yourselves sometimes, acquire knowledge, and don’t expect everything to be served to you on a silver platter.

In my understanding, the company cannot buy back loans at a discount, but at their nominal value of €57 million.

The company’s balance sheet shows that the liabilities are mainly VVL and lease liabilities, which are mainly related to plots of land and completed housing company loans.

If covenants are disregarded, what benefit does the company gain from issuing a new loan if the company does not need funds for its business operations?

Or do you see the company needing more than +€50 million in cash?

If this were my company, I would try to renegotiate the covenants in this situation and would not take out a new loan, unless the initiation of self-funded projects or the acquisition of land reserves required it.

A loan is always a loan and it has its price, which, based on OPA’s message, is at least at a reasonably high level, i.e., from €20 million, interest expenses are around €1.6 million per year, and these always involve quite substantial drawdown fees.

How did you come to this understanding? According to the announcement, private and investor-specific negotiations are being held regarding the buyback and its terms.

If the company were to buy those loans at nominal value, it would have to record the difference between their acquisition price and book value in the income statement. This, in turn, would further reduce the equity ratio.

Hi, the hybrid has caused a good deal of discussion here. As a recap, the repayment and conversion of the current hybrid bonds indeed proceed according to the nominal value of the loans (EUR 57 million). This planned new green hybrid would strengthen the company’s balance sheet, and as its name suggests, the capital obtained from it would be used to finance green projects (practically all of the company’s self-developed and self-initiated projects). It’s worth considering the company’s financing arrangements as a whole. For example, the sale of SRV Infra plays an important role in the redemption of current hybrids, but on the other hand, despite the redemption, this arrangement would secure the prerequisites for initiating projects based on own project development.

How has the esteemed analyst arrived at this conclusion? The company’s release states:

\u003e The price and other terms of each Acquisition will be determined on market terms in private and investor-specific negotiations. The Acquisitions are conditional on the issuance of the New Hybrid Bond.

Have you received information from the company that the conversion would occur at nominal value, as it is not stated in the release?

I was just referring to the June 2026 review date for the current hybrids, when redemption at the nominal value of the loans is possible. The terms of the current hybrids are available on the company’s website: Velka- ja hybridisijoittajat. As I understand it, I cannot comment on the negotiations currently underway with a very limited group of investors regarding the new hybrid, nor can the company, of course, communicate about these.

Well, we discussed the price at which those old hybrids are now being acquired. This is still unknown.

In my opinion, this concerns negotiations on the terms of the buyback of old hybrids. According to the loan terms, the first reset date is indeed June 30, 2026, but the company has the option to buy back the loan at any time, provided it reaches an agreement on the terms with the bondholder.

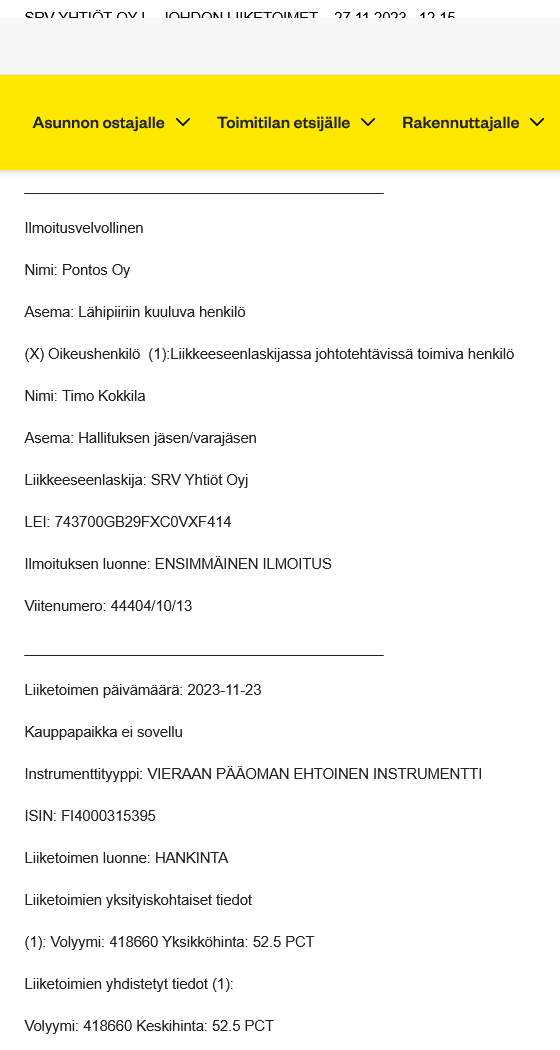

I don’t have precise information on how large a share of these hybrids is held by the Kokkila family, but at least Pontos Oy bought the loan in November 2023 at 52.5% of its nominal value:

Conversion of loans into shares is also possible after June 30, 2026, at a price of 4.0 euros. In that case, the number of shares could almost double if the loans are not bought back and the entire loan amount were converted into shares.

A separate issue is the impact of the buyback on SRV’s profit and loss statement and balance sheet, as these hybrids are currently on the balance sheet valued at €33.5m.

This is still a LOAN, even though from an accounting perspective it has been converted into the company’s own equity.

Regarding the repayment of the loan, the company’s management has made the repayment completely clear, meaning it will not dilute shares.

According to my own calculations, the company will have over 100 M€ by 30.6.26, so the company management’s statements and the company’s repayment capability are aligned.

From an accounting perspective, that potential repayment only affects the balance sheet and does not go through the income statement. So, if we consider a theoretical situation where the loan is fully repaid on the review date, the difference between the repaid price (nominal value EUR 57 million) and the balance sheet value of the hybrid (approx. 60% of the nominal value or EUR 33.5 million) is recorded directly in the retained earnings in equity.

I recall that the difference has already been recognized as income, so the effect is exactly the opposite and must be recorded through the income statement. I’ll have to check this.

E: I remembered correctly:

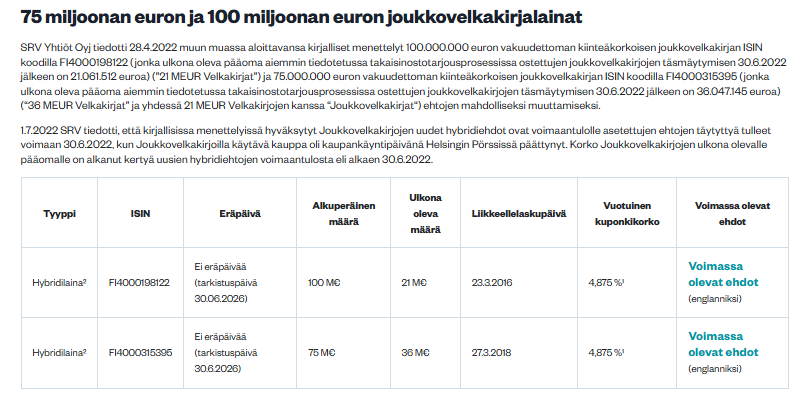

During the reporting period, the Company’s EUR 100 million unsecured fixed-rate bond (the outstanding principal of which, after the settlement of bonds purchased in the tender offer process on 30 June 2022, is EUR 21.1 million) and EUR 75 million unsecured fixed-rate bond (the outstanding principal of which, after the settlement of bonds purchased in the tender offer process on 30 June 2022, is EUR 36.0 million) were converted into hybrid and convertible bond terms through written procedures. The convertible bond terms were implemented by amending the bond terms to include a special right, in accordance with the Companies Act, to convert the bonds into shares, if the company does not redeem them by 30 June 2026. The hybrid terms were implemented such that, with the change in terms, the loan has no repayment date, nor does it obligate the issuer to pay interest. The loans were valued at fair value, which at the time of the change in loan terms was 60 percent of the nominal value of the loans. Of the hybrid and convertible bonds with a nominal value of EUR 57.1 million, EUR 34.3 million was recognized in the balance sheet as equity-accounted loans, and the difference between the nominal value and fair value of the loans, EUR 22.8 million, was recognized as other financial income. During the written procedure concerning the change in loan terms, the Company made a voluntary tender offer to the bondholders at 60 percent of the nominal value. In the tender offer, bonds with a total nominal value of EUR 42.7 million were purchased, and EUR 25.6 million was paid for them. Due to the conversion of the bonds into hybrid terms, they are no longer presented as interest-bearing liabilities at the end of the reporting period but as an equity item.

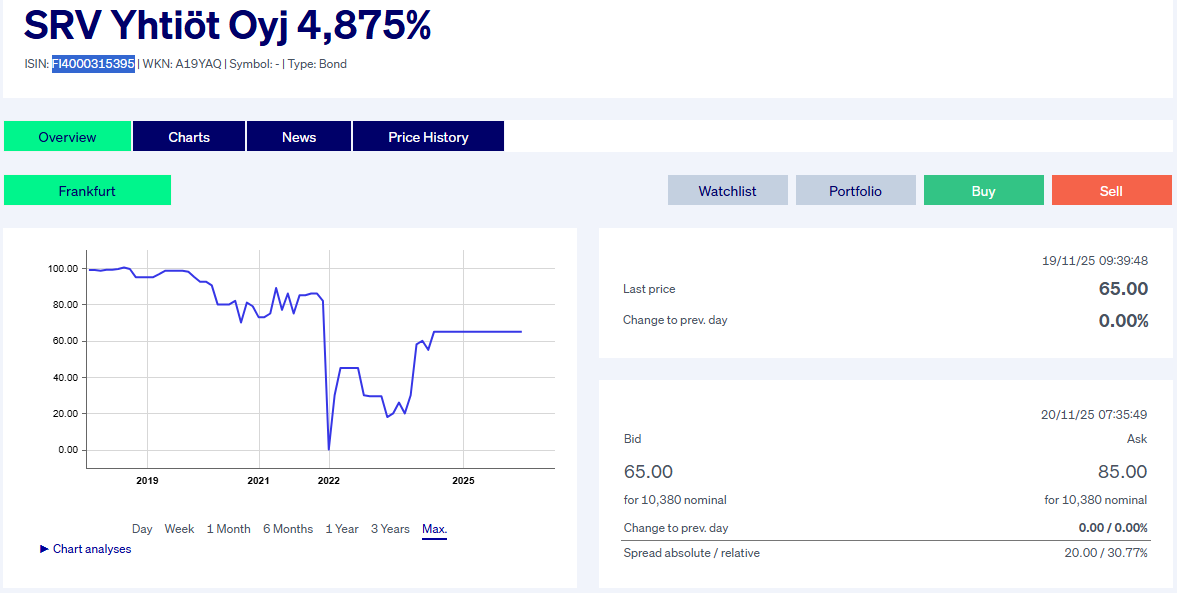

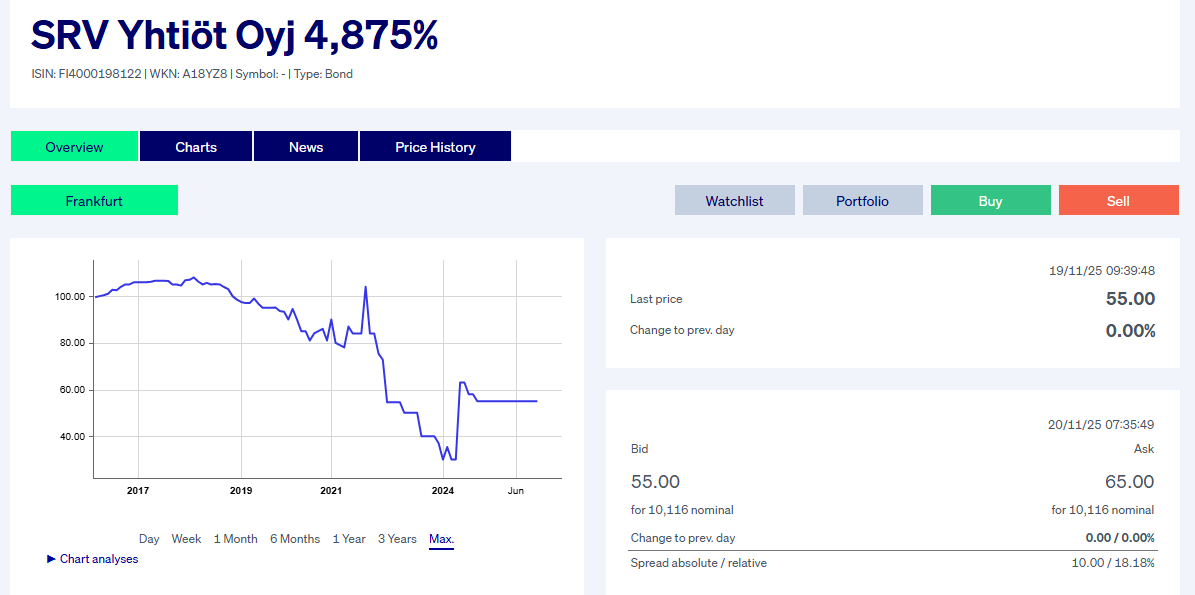

Those hybrid bonds are “listed,” but the bid levels are probably historical, and the actual trading is bilateral / brokered.

SRV as a buyer - if one considers that

SRV has “certain” funds for repayment

SRV is entitled and “certainly” intends to redeem before a dilution possibility arises

=> then, from SRV’s perspective, the maximum price could be 100% of the nominal value

(Potential) Seller:

if the seller thinks as above that SRV has certain funds and that SRV intends to redeem before a dilution possibility, then the minimum price would also be 100% of the nominal price

Interest:

if there is unpaid interest, it could increase the bond’s value

on the other hand, early redemption gives the seller an interest benefit, i.e., saves their capital interest for well over half a year

Special situations:

the seller may have a need for their money for entirely other reasons, which encourages (such as alternative investments, etc.) or even forces them to sell, “underpriced,” when a buyer is available (margin calls, fund closures / redemptions, etc.), and the VVK share option also seems to have expired.

SRV may also have a special interest, as speculated in previous messages (balance sheet position / solvency target as part of financing prospects or loan covenants) and a linked commitment to participate in a new hybrid, in which case it might be interesting for continuity to pay a separate redemption premium, or consider it in the price. However, the interest rate of the new hybrid is likely higher than the current one’s less than 5%, so it’s a bit awkward to pay something separate in such a scenario.

=> perhaps these create the personal market price, which is likely already conditionally agreed upon, as can be inferred from the announcement. That is, at its most favorable for SRV when the seller simply wants to get rid of these, and at its most expensive, the nominal price minus the seller’s interest benefit, plus any accumulated interest.

I find it a bit inconsistent to record the difference directly as a reduction in retained earnings when it was previously recognized as income through the income statement. But that’s that.

The redemption of hybrids at par value would thus create a total €57 million hole in equity, which is partly intended to be covered by a new hybrid. What would SRV’s equity ratio be after this, and would it meet the loan covenant conditions regarding the equity ratio, e.g., with the help of a new €30 million hybrid, and are lease liabilities taken into account in the equity ratio?

It would just be better if there was an option to record it through the income statement, because for me the loan cost is 57 m€, but through the income statement, the company would incur an accounting

Well, no. 57 M€ leaves the cash register, and equity decreases by 22.8 M€ (previously recorded difference) + 34.3 M€ (balance sheet value of hybrids), meaning total equity decreases by 57.1 M€.

The company already has plenty of accounting and unused tax losses.