I’ve been thinking specifically about these balance sheet investments: the company is constantly involved in funding rounds for Finland’s most prominent startups, which means that if you want to indirectly own a slice of such companies, Springvest would be a gateway for this (although I don’t own Springvest myself).

It is of course great that the size of the funding rounds has grown, which also brings actual euros into the coffers, but still, what makes Springvest interesting in my opinion is the possibility to get a diversified sample of a large and high-quality portfolio with a single investment. I would argue that it’s specifically this quality of startups that has received too little attention. During the previous hype, exits were achieved early, but I would see that companies like Paptic, Kuva Space, and now Solar Foods are even more Grade-A startups. If some of these don’t succeed in the future, then it’s unlikely others will either.

Of course, you need heaps of these companies to get those 1-2 real winning cases, but if the current trend continues, Springvest would have about 10-15 of these in its pocket over the next couple of years.

Could one even see Springvest as having a two-phase cycle: now, at the bottom of the wave (of startup funding), a bunch of tough startups are added to the portfolio because money still seems to be available through Springvest. Then, when a new hype is generated in a few years(?), they can exit this cheaply acquired pot with top multiples at the crest of the wave.

Yup - this is a very relevant perspective; in terms of its value creation logic, Springvest is practically a kind of equity-based VC fund. However, the company doesn’t invest capital in the companies itself but receives them as fees for organizing the funding rounds, so in that sense, this “fund” gets to “make investments” without capital requirements from Springvest’s shareholders

That’s how I’ve been thinking about the big picture as well; of course, in addition to exits, it’s also easier to raise money during a strong cycle. I don’t take a strong view on the cycle’s turning point, though, mainly assuming the weak cycle will continue for the time being. For now, we continue adding substance to the portfolio (=organizing funding rounds) as long as investor clients have enough capital. In time, in a more buoyant market situation, with successful company selections and a dash of honest luck, one should be able to expect a certain number of exits.

Here is an article in Kauppalehti regarding the value of Springvest’s balance sheet investments^

In my opinion, Rajala is cutting some corners here in his valuation based on the remaining equity (OPO), considering it is a technology-weighted portfolio. If you are interested in exploring this topic further, there is a good amount of research available on the transparency of private asset valuations

It’s good to remember that being at the bottom of the cycle also means that existing investments take a hit; this shouldn’t perhaps be viewed exclusively in a positive light, as lower valuations (rising return requirements and a difficult economic situation) are reflected in current holdings as well, and not just in the opportunistic outlook for new investments…

If someone wanted to do some honest “legwork” on the balance sheet, they could go through the financial statements from the rounds and look up valuation benchmarks (EV/Sales, EV/EBITDA…) and start pondering how the multiples reflect forecasts and actual figures from previous rounds, etc.. the problem would likely be this biotech weighting and the impossibility of DCF without forecasts…

By the way, it occurred to me while I was reflecting on the balance sheet valuation after reading previous comments in the thread, could @Antti_Luiro explain how these balance sheet items are valued?

The question mainly concerns the fact that between 2012 and 2017, financing was raised for approximately 30 companies for which, as I understand it, there has been no exit event. How long can these be “kept” at face value on the balance sheet if no signs of growth have occurred and, for example, the forecasts in the investment memorandums have been dramatically missed?

Similarly, if we look at a company like ArcDia International, which according to its website has raised about 5.5 million in capital, and if I recall correctly, in 2022 the company tried to raise a round through Invesdor with poor success (the round did not materialize). Wouldn’t these types of companies distort the balance sheet structure if 5.5m has been raised but they can’t even secure 0.5m EUR on a competitor’s platform today, especially since I understand Springvest Oyj doesn’t really adjust these with value changes?

Short comments on this can be found on pages 21 and 29 of the comprehensive report:

So, the balance sheet value moves either based on:

Market terms based on the valuation of a new funding round or

An assessment made by Springvest.

The first of these is a “hard” market-tested valuation, while the latter is the company’s subjective assessment of changes. If the company’s own adjustments are made conservatively in accordance with the company’s communication, then the balance sheet value is a relevant metric. In practice, if nothing is heard from a company, I believe Springvest cuts the balance sheet value downwards based on the principle of prudence. Conversely, for good business momentum, the balance sheet value can also be increased compared to the previous market-tested value.

However, here we are mostly relying on trust, as the balance sheet values of individual companies are not published. In the long run, conservatism should be reflected in the fact that in exit situations, companies would bring in clearly more cash than their balance sheet value, after taxes. My understanding is that this was the case with the 2020–2021 exits, but during Springvest’s time as a listed company, no (at least positive) exit events have occurred, so clear reporting on these exit values vs. balance sheet values probably doesn’t exist yet.

It is still clear that for these riskier early-stage growth companies, valuation is almost always extremely difficult. Although Springvest does its best with balance sheet values, surprises will occur. Of course, it’s better to prepare for this by leaning towards the cautious side.

To prevent the discussion from becoming a monologue on my part, I have to state in conclusion that these rounds seem to get filled at an incredibly high rate.

In Tamturbo Oyj’s share issue (5.6 MEUR 2022), they didn’t even publish targets for the coming years because the company “plans to apply for the Nasdaq First North Growth Market,” yet investors (and Springvest on its own balance sheet) fully subscribed to a company with approx. 3 MEUR negative EBITDA at an EV/Sales 15x (2022) multiple The company had canceled its listing plans in June 2020 due to a strategic investment received, but apparently in the red-hot 2022 IPO market, listing was a reality once again…

I have a deeper view on this topic, but let’s leave it unsaid for the sake of Friday night and move to the sidelines in this thread… The new CEO is a great hire, and it’s actually a pretty intriguing situation when both Invesdor Nordics and Springvest have historically strong leaders at the helm in terms of CVs. I still wouldn’t hold my breath regarding a “new Mobidiag,” considering the 2021 valuation multiples (Mobidiag) and the pure probability that companies for which multiple rounds have been raised would even be close in potential to this single case bravely sustaining the IRR %

Someone contemplating the company’s investment philosophy could, of course, ask how much equity upside was left in this Tamturbo (as well) offering if you buy a company at a 15x EV/Sales multiple that, according to the presentation, plans an IPO within 12 months, considering unlisted risk premiums and general market uncertainty…

It looks like one more round will make it for this year

This is a real test of increasing the round size. Is there enough interest and dry powder among investor clients? With a maximum amount of 12 MEUR, this would be the largest funding round organized in Springvest’s history

In my opinion, this brings us to a key topic regarding Springvest Oyj: Acting simultaneously as a venture capitalist and a fundraiser

Case Verge:

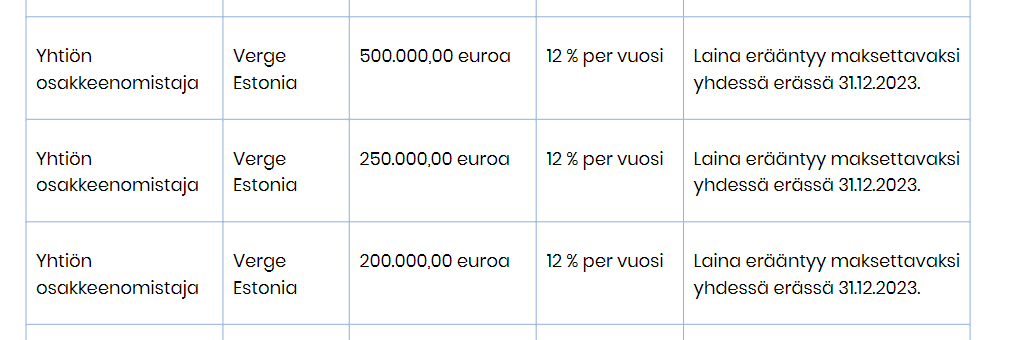

Convertible loan, where the reward for mandatory conversion is a discount of approx. 20% on the next round. The most likely exit scenario according to management is an IPO, so here the unlisted risk premium + equity upside = only 20% for a company with a turnover of 13k EUR and a valuation of several tens of millions? In the stock market, Nordea’s strategists’ expected return for next year is +10%, so as an investor, am I taking a bigger risk on an approximately pre-revenue (13k turnover 2022) unlisted company than what Nordea’s strategist estimates as the stock market return?

Funding round spread 1-12m EUR. OK, I understand wanting to benefit from high interest by setting a large upper limit, but if money is being sought for “scaling international operations,” how much and for how long are international operations scaled with 1.1m EUR in funding?

Is the cash reserve empty? In the interim, it’s in the red and the assets side consists of receivables from intra-group companies. Why is there no consolidated financial statement here if the operational side is in Estonia?

Is the company paying its current shareholder a higher interest rate than what is being offered here? Will the shareholders’ debts be paid off with the funding round if only 1-2m EUR comes in, or how does it work?

The company’s home country could be clarified a bit for the media, as it now seems to be headlined as Estonian in several news sources?

I believe this was previously called RMK Vehicle Corporation (from the Ostrobothnia region, if I recall correctly), which was already raising money from investors back in 2019. The first bikes were supposed to go on sale at the beginning of 2020, and the revenue target for 2025 was 100 million euros (4,000 bikes). That didn’t quite materialize…

Without bashing them any further in this thread (we can move over to the “Unlisted shares” section), they are currently trying to raise money under quite incomprehensible terms. I have to wonder if anyone will actually put their money into it.

Springvest, which raises funding for growth companies, is an exceptional company with clearly distinct income statement and balance sheet components. One can invest in the company based either on its balance sheet or its income statement.

Organizing funding rounds, i.e., the operational business, generates earnings that can be predicted reasonably well based on the number of funding rounds: revenue amounts to about ten percent of the capital Springvest raises for its client companies.

The balance sheet, on the other hand, consists of Springvest’s holdings in the growth companies for which it has raised funding. Springvest is quite sparing in disclosing details about its balance sheet. In Karon Grilli, Springvest CEO Aki Soudunsaari talks about Springvest’s holdings and highlights the companies whose development he follows most closely.

Isn’t there a risk in this business that when companies are gathered into a “portfolio,” there are both good and bad companies at the start? Then over time, you exit the good ones, etc., and get cash, but at the same time, the amount of substandard assets on the balance sheet grows. Slowly but surely, because you can’t get rid of poor holdings (except for those that go bust).

A kind of style drift occurs, where an originally high-quality portfolio inevitably becomes worse and worse, as unlisted poor companies cannot simply be sold off.

The weakest companies are also removed from the portfolio through bankruptcies

Springvest’s holdings are diluted to a small size if a company in a weak trend raises several rounds of funding. In these contexts, balance sheet values are also updated to reflect the new ownership stake and the valuation of the funding round

The current (31.12.22) portfolio’s share of our sum-of-the-parts is in the range of 25-30%. With the current pace, new holdings are added through new rounds so frequently that the company’s portfolio is also constantly being renewed

In our analysis, we categorize the portfolio companies and through this, form an understanding of the quality of the current portfolio. Of course, there are so many companies and visibility into their developments as unlisted entities is so limited that it is difficult to achieve a very high level of quality in these assessments.

This valuation discussion was a bit confusing. It was stated that the value of Springvest’s share is largely equal to the value of its portfolio on the balance sheet, and the CEO commented that the portfolio’s valuation is clearly on the low side. Shouldn’t such information, which materially affects the share price, be provided to investors equally and simultaneously—i.e., via a release? Yet, nothing has been announced.

Greetings again to the forum - with a slight delay after the Christmas holidays a few comments on that discussion between Karo and Aki

In my opinion, this referred to the fact that the company’s market value is currently close to its book value (2024e P/B 1.0x).

In our estimates, however, the current holdings in the portfolio (owned as of Dec 31, 2022) have been in the magnitude of ~20-25% of the sum of the parts. So I would see the connection between the current market value and the value of the current portfolio as more of a coincidence.

The company has communicated its valuation principle externally before, so in that sense, there is no new information here. The valuation of early-stage growth companies (some of which do not even have a clear business yet) is more of an art than a science, and from this perspective, a conservative approach to balance sheet values is a good starting assumption. The value of Springvest’s portfolio is only realized in potential exit situations, so in my opinion, relying directly on balance sheet values is also a bit dangerous.

Springvest’s largest funding round to date has been launched for drug development company Desentum.

@Antti_Luiro Do you expect more of these +€10m rounds in the future? Offerings of this magnitude, when fully subscribed, are certainly in strong contradiction to the idea that the “IPO window” is closed for small-cap companies.

I do expect so. Springvest is capable of conducting around 8–12 funding rounds per year, and the only way to grow operations is through the round size. The company’s strategy is also to increase the round size, so in that sense, it’s quite an expected development Admittedly, the availability of funding in Springvest’s rounds has been surprisingly good compared to the general development of the Helsinki Stock Exchange and the quiet IPO season.

Could it be inferred from this that there is a rush of certain-sized companies seeking growth financing for Springvest’s rounds, now that the IPO window is closed?

If I recall correctly, I asked management about this in a previous interview, or at least the topic has been touched upon in other discussions with the company in any case, there has been a good supply of seemingly high-quality growth companies for Springvest’s funding rounds, and the sluggishness of the IPO route certainly hasn’t hurt the company