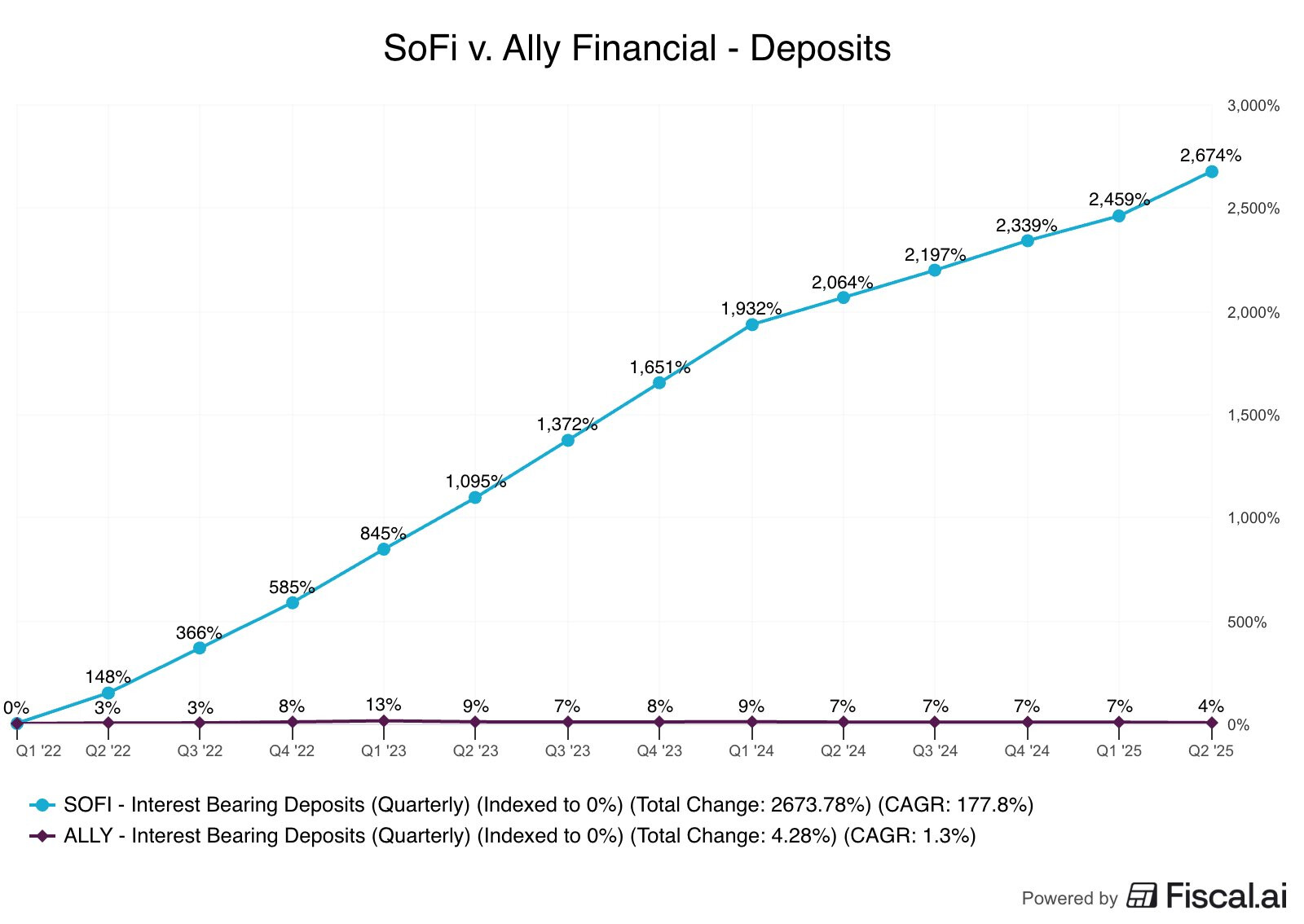

Alla olevasta tviitistä näkee, miten kivasti SoFi on ottanut markkinaosuuksia verkkopankkimarkkinoilta. ![]()

https://x.com/fiscal_ai/status/1965777340400820431

Alla olevasta tviitistä näkee, miten kivasti SoFi on ottanut markkinaosuuksia verkkopankkimarkkinoilta. ![]()

https://x.com/fiscal_ai/status/1965777340400820431

https://x.com/datadinvesting/status/1965640887985471869?s=46ä

Robinhood on esitellyt shorttaus mahdollisuuden alustallaan ja käyttivät Sofi osaketta esimerkkinä ![]()

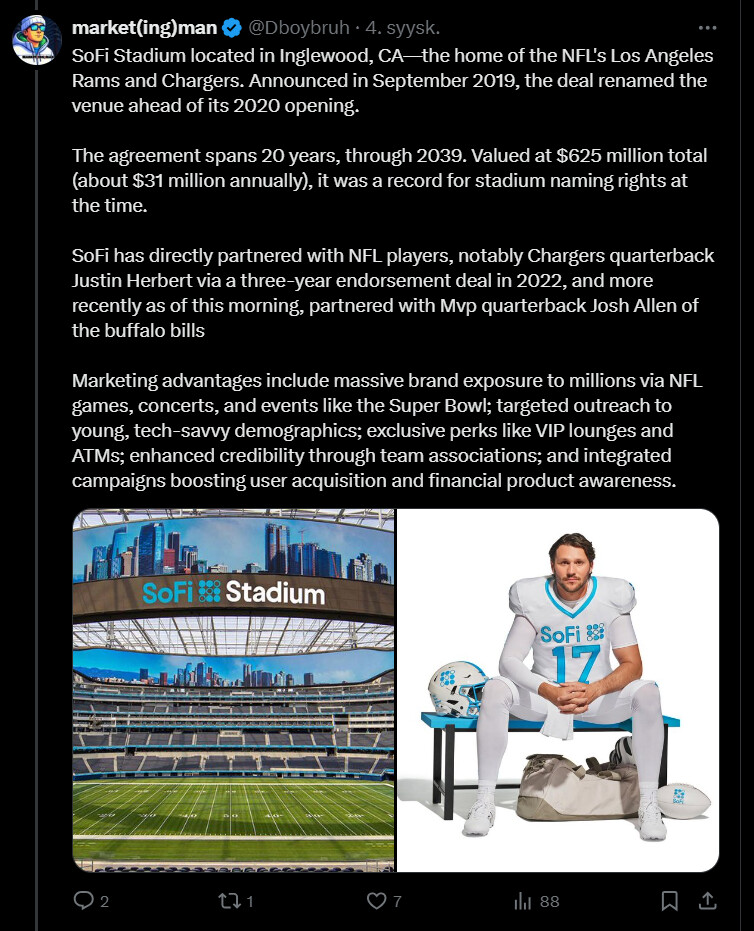

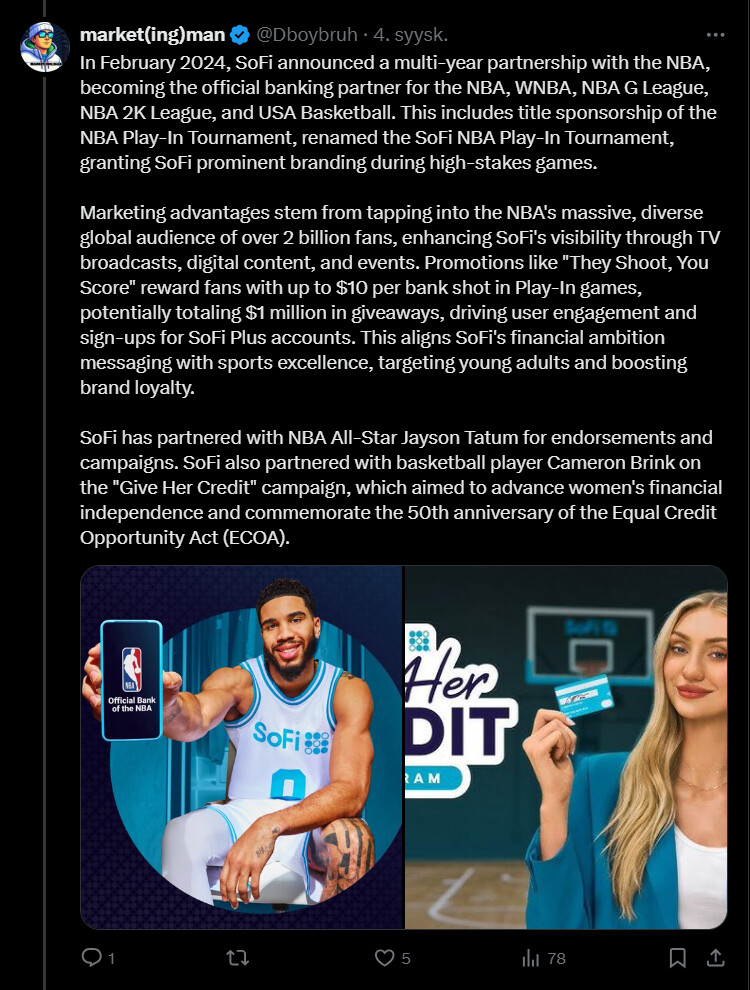

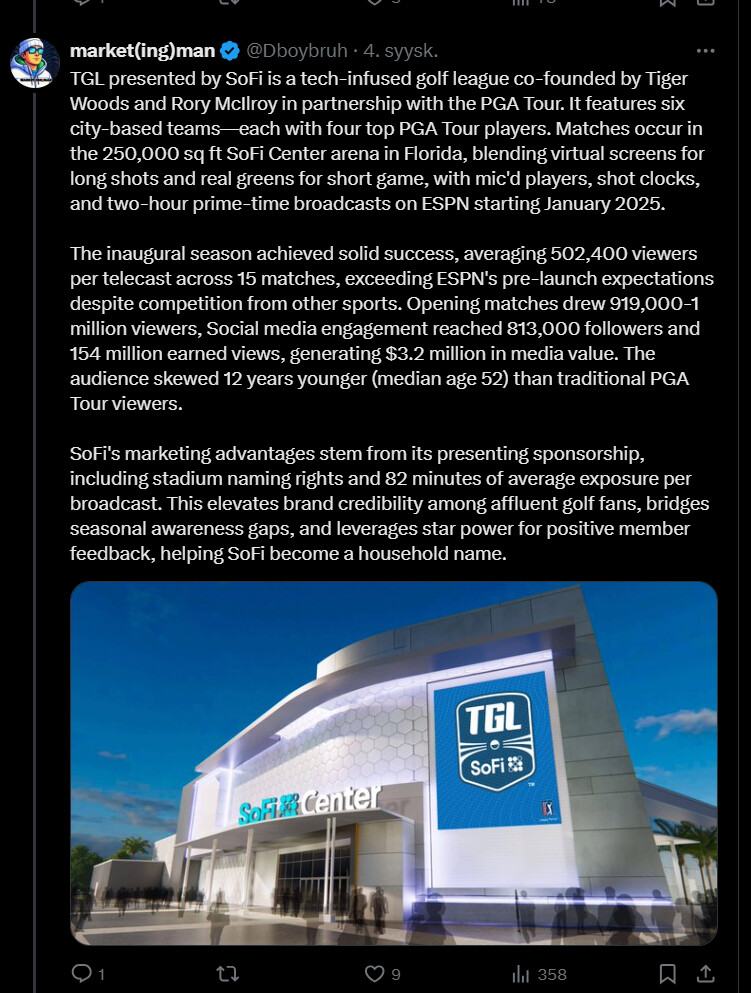

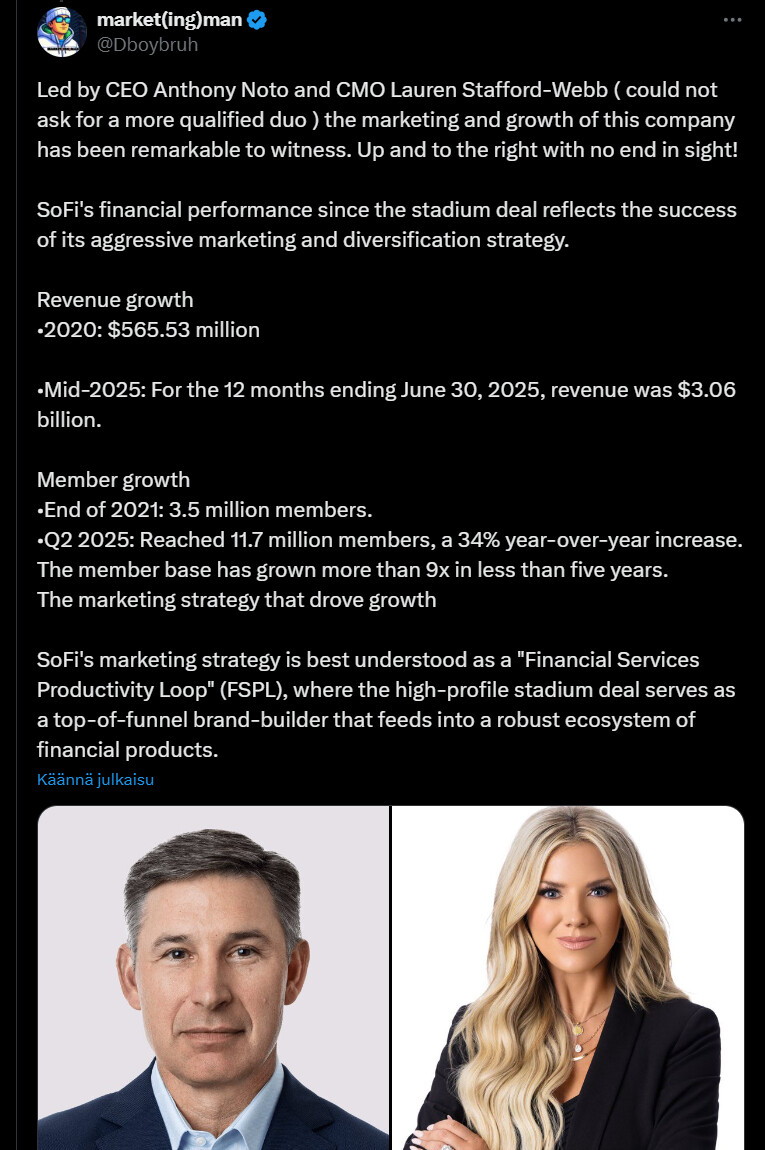

Alla olevassa tviittiketjussa kerrotaan, että SoFi on rakentanut vaikuttavan urheilumarkkinointistrategian, joka kattaa NFL:n, NBA:n ja jopa uuden TGL-golfliigan.

Miljardiluokan stadiondiilit, pelaajayhteistyöt ja kumppanuudet ovat kasvattaneet brändiä sekä myös jäsenmääriä valtavasti vahvistaen yhtiön asemaa finanssipalveluiden markkinoilla. ![]()

https://x.com/Dboybruh/status/1963635813503439063

Eihän vaan ole liian hyvää ollakseen totta? Eihän kasvua negatiivisella kannattavuudella?Numerot kyllä pian kertoo.

Nyt P/E yli 50 eli tulostuotto vain vajaa 2%. Vuotta aiemmin vielä huonommin, joka voidaan myös tulkita kehitykseksi. Kasvufirmalle ok? Juurikin sijoitusstrategia vaatii 10%.

Millä tavoin tämä firma osaa nettipankin paremmin kuin vaikkapa Ålandsbankenin Crosskey? Jos arvostusta ei selitä tekninen ylivertaisuus, niin ehkä jo vakiintunut ja kasvava asema toimialueellaan?

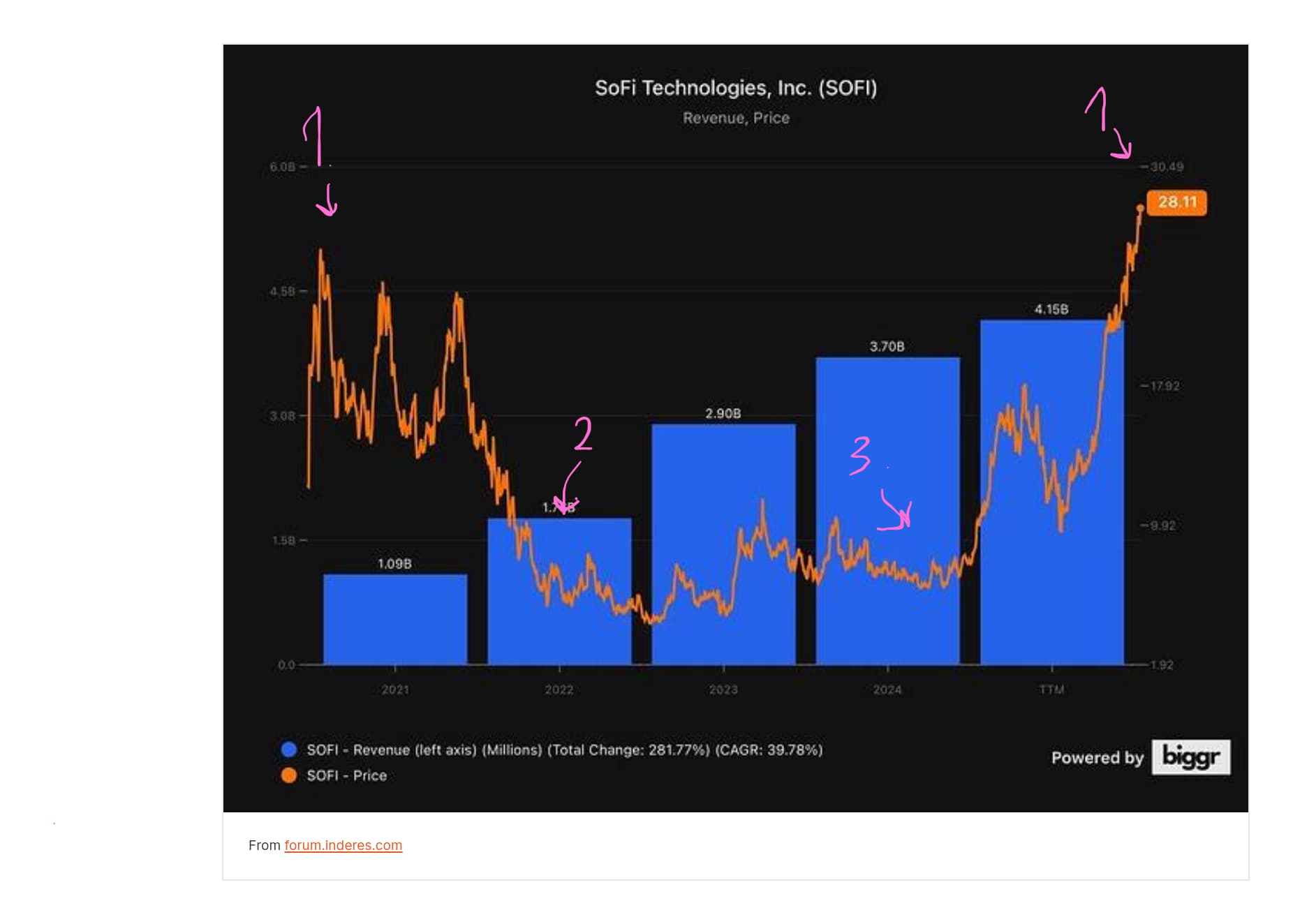

Käppyrä kertoo, mitä Juurikki varoo:

Ehkä this time is different. Juurikki ei omista ko. firmaa, eikä enää osta hintaan 25, kun olisi vasta ollut 5. Juurikki ei maksa tulevaisuususkosta, mutta toivoo omistajille hyvää tulevaisuutta, silti muistuttaen isosta riskistä (lue: miljardiluokan stadion-diilit).

Ps. Yllä oleva ei ole analyysi, vaan joukko irrallisia fundaankin pohjautuvia heittoja. Valistakaa Juurikkia, kiitos. Moittikaa edes.

Voi olla juuri noin, että liian hyvää ollakseen totta. ![]()

SoFi on kyllä musta kiinnostava, kuten Hyzon sekä Voxtur aikanaan… SoFi jopa kasvaa hurjaa vauhtia, mutta arvostus mietityttää ja on mietityttänyt monia. Eihän P/E-luku ja “tulostuotot” oikein vielä houkuttele, vaikka kyllähän noissa luvuissa on tapahtunut kehitystä, mutta kalliiltahan näyttää. ![]()

Vahvuuksia on monipuolisuus ja teknologiapuoli, mutta riskit regulaatiossa ja myös kilpailussa voivat olla suhteellisen suuria. Stadion-diilitkin ja vastaavat voivat kääntyä miinukseksi eikä ne kai nyt positiivisimmissakaan skenaariossa olisi niin valtavassa roolissa. Potentiaalia riittää kuten aina tulevissa turskissa ![]() , mutta varovaisuus on tosiaan tarpeen.

, mutta varovaisuus on tosiaan tarpeen.

Jos arvostuskertoimia katsoo, niin ei nyt halpana voi pitää, jos ei pärjääkään kilpailussa ja jos ala tulee yleisestikin haasteellisemmiksi esimerkiksi lakimuutosten takia jne. ![]()

Tulevaisuudenusko ja toivo ovat sijoitussuunnitelmieni ytimessä. ![]()

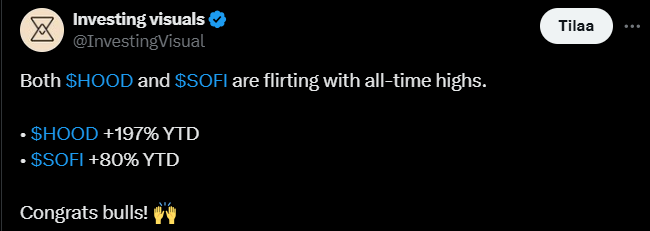

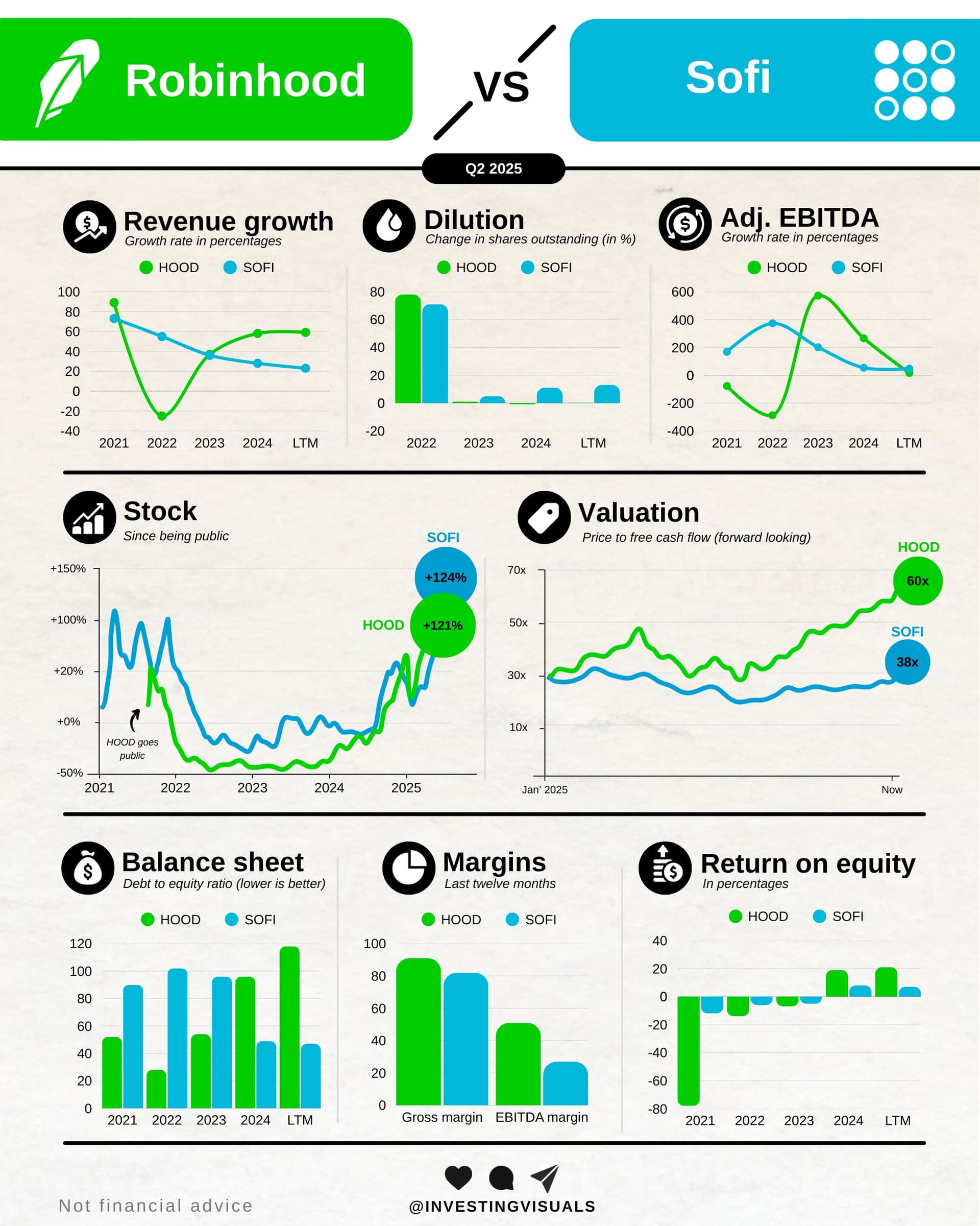

Tässä on vertailussa Sohvi ja Hoodi ![]()

https://x.com/InvestingVisual/status/1966139673446867291

EDIT:

Mä lisään tämän tähän. ![]()

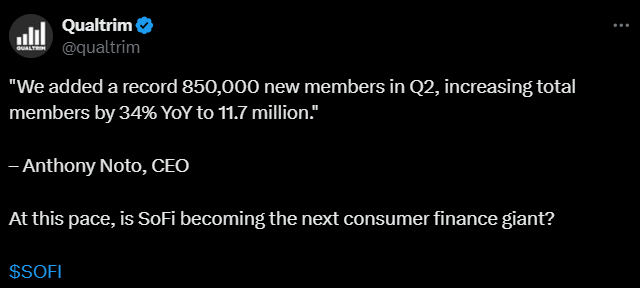

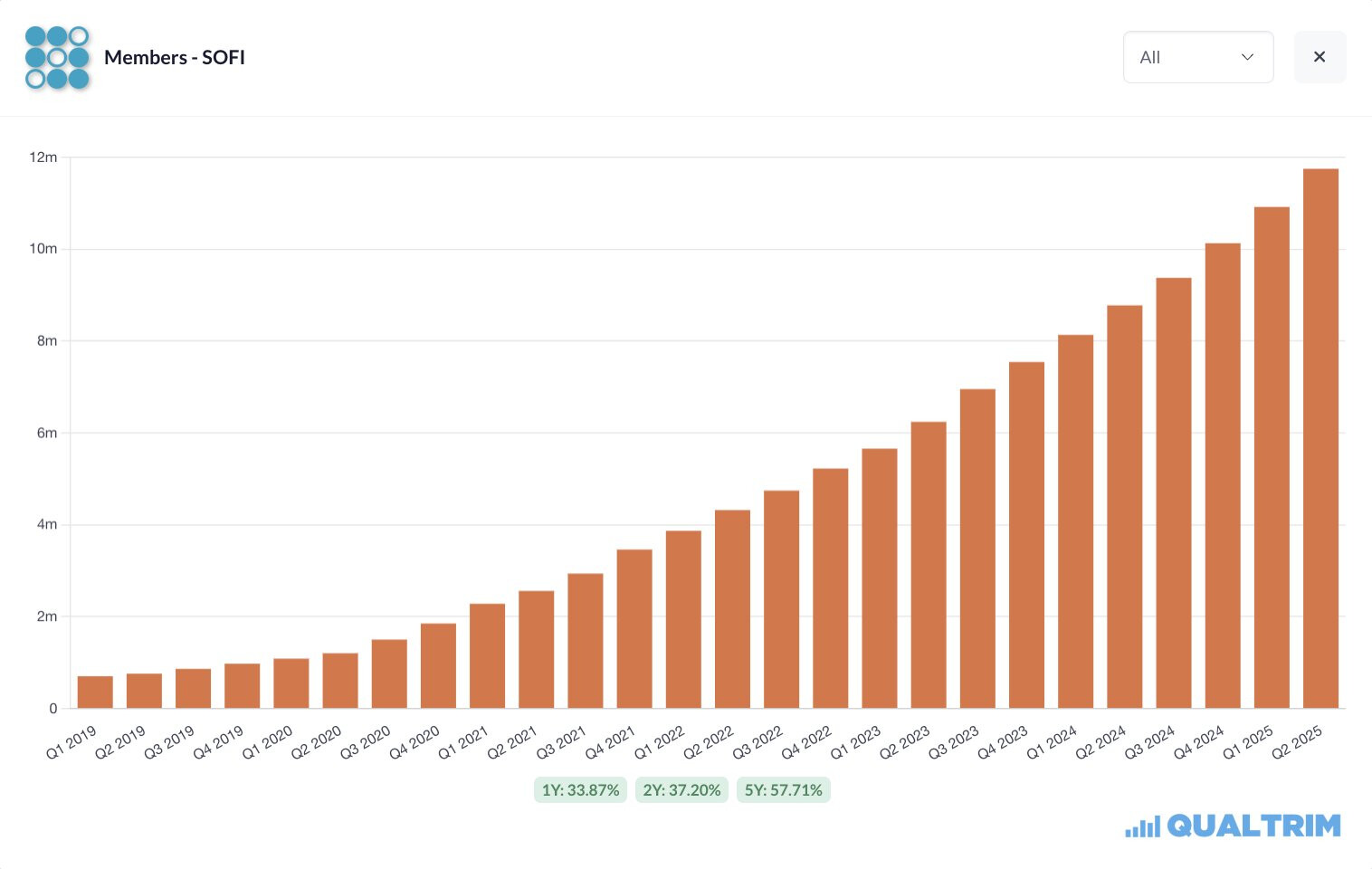

https://x.com/qualtrim/status/1967298261989150773

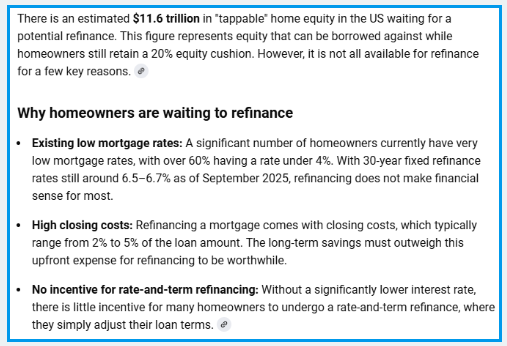

Alla olevassa tviitissä kerrotaan, että Yhdysvalloissa on 11,6 biljoonaa dollaria kotien vakuusarvoa “odottamassa” uudelleenrahoitusta, mutta matalat korot, korkeat kulut ja vähäinen hyöty jarruttavat.

Tviitissä haetaan kai sitä, että Sohvi hyötyisi korkojen laskusta, koska se lisäisi kysyntää yhtiön rahoituspalveluille.

https://x.com/dewmboom/status/1967988134852837533

Tähän väliin tällainen hieman kevyempi juttu. ![]()

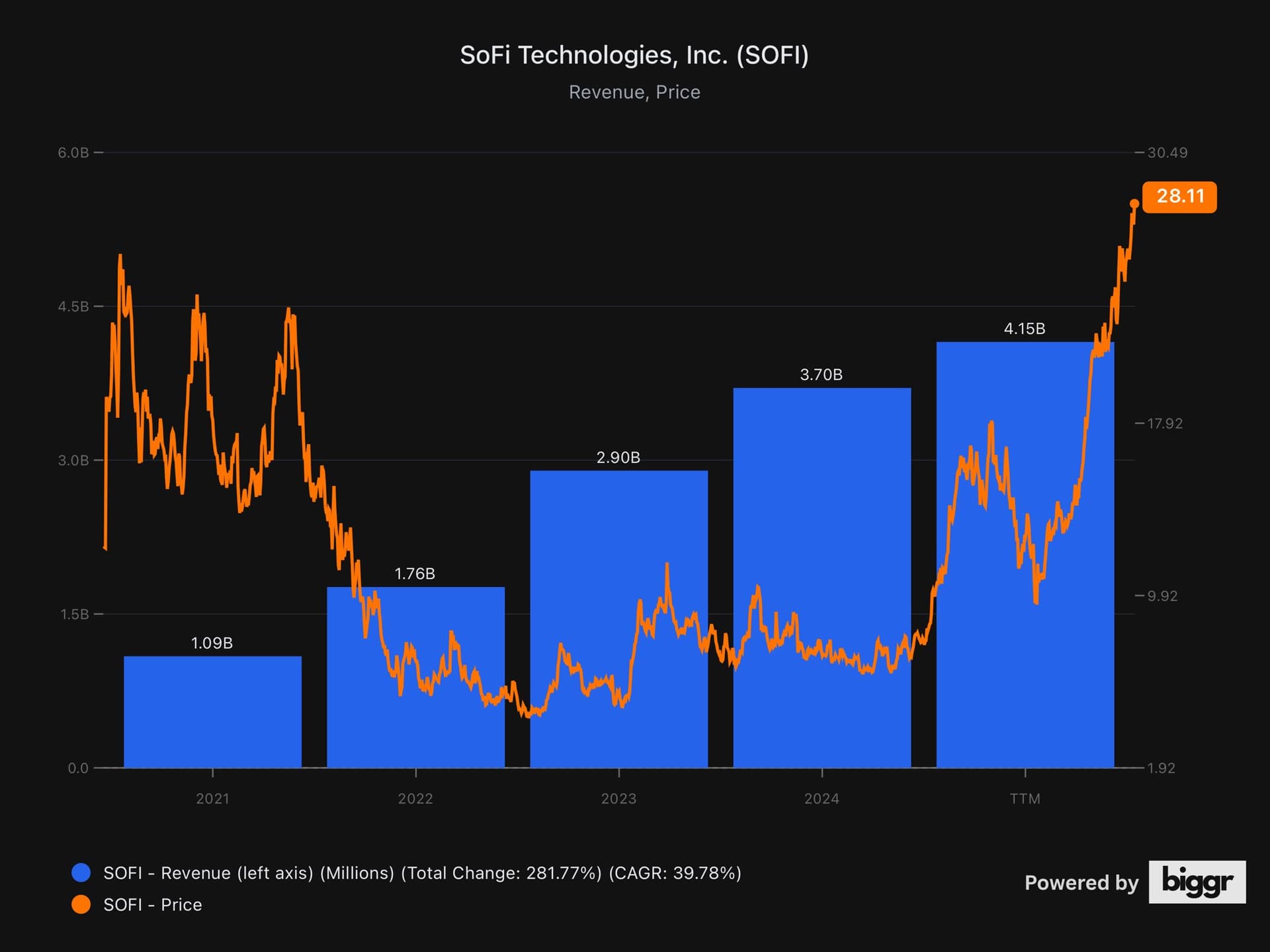

SoFi on raketoinut jälleen, kuten tviitistä käy ilmi. Siinä käydään läpi myös muutama asia, jotka voivat auttaa Sohvia raketoimaan jatkossakin. ![]()

https://x.com/thexcapitalist/status/1969013697805779289

Hassu juttu, mutta tämä kuva kertoo hyvin miten pelkästään Yhtiön luokittelu muuttaa sen arvoa.

1 (Yhtiö tulee pörssiin ja on kannattamaton):

“Yhtiö tulee muuttamaan koko fintek alan ja edustaa sen tulevaisuutta, ilman fyysisiä konttoreita, pelkästään digitaalisesti, palvelimilla, se on pääoma kevyt, ketterä, ja loputtomasti skaalautuva”.

Yhtiön kannattamattomuus tai korkea P/E on sivuseikka, sillä potenttiaali on kova ja bruttokate muuttuu nettokatteeksi ajan kuluessa. (Yhtiölle annetaan korkea arvostustaso).

(Yhtiö tulee kannattavaksi EBIDA-tasolla) osake alimmillaan käy 3.XX dollaria tasolla ja on saanut/saamassa pankin toimiluvan.

Yhtiötä verrataan nyt muihin (P/E-luvulla), kannattaviin pankkeihin ja todetaan tämän olevan kallis.

"Mutku pankeilla on tämä ja tämä P/E luku " ja ne maksaa osinkoa. "Miksi ottaa jotain ylihintaista pankkia, voivat ne jättipankitkin muuttua digitaaliseksi/ostaa digitaalisen kilpailijan.

Yhtiön kannattavuus saavuttaa pankit: ( osake alimmillaa pitkän aikaa 5-6.XX dollaria ) mutku jättipankeilla on isommat kassat, niin ei tää kestä seuraavaa taantumaa, jättipankit on parempi vaihtoehto"

1 Sama kuin alunperinkin, kaikki alunperin yhtiötä korkealle arvostaneet youtubettajat/some olivat oikeassa, mutta korpivaellus kesti 3 vuotta ja suurin osa heistä luovuttu loputtoman negatiivisen palautteen alla.

SOFI, siis itse yritys tickerin takana on koko ajan toiminut niikuin se on sanonut ja kehittynyt, Pääjohtaja sanoi alunperin että heistä tulee yksi 20 suurimmasta pankista Yhdysvalloissa ja on toistanut tätä monesti. Mikään asia yrityksessä ei ole muuttunut perustavalla tasolla, ainoastaan miten sijoittajat arvostavat eri tilanteissa sen.

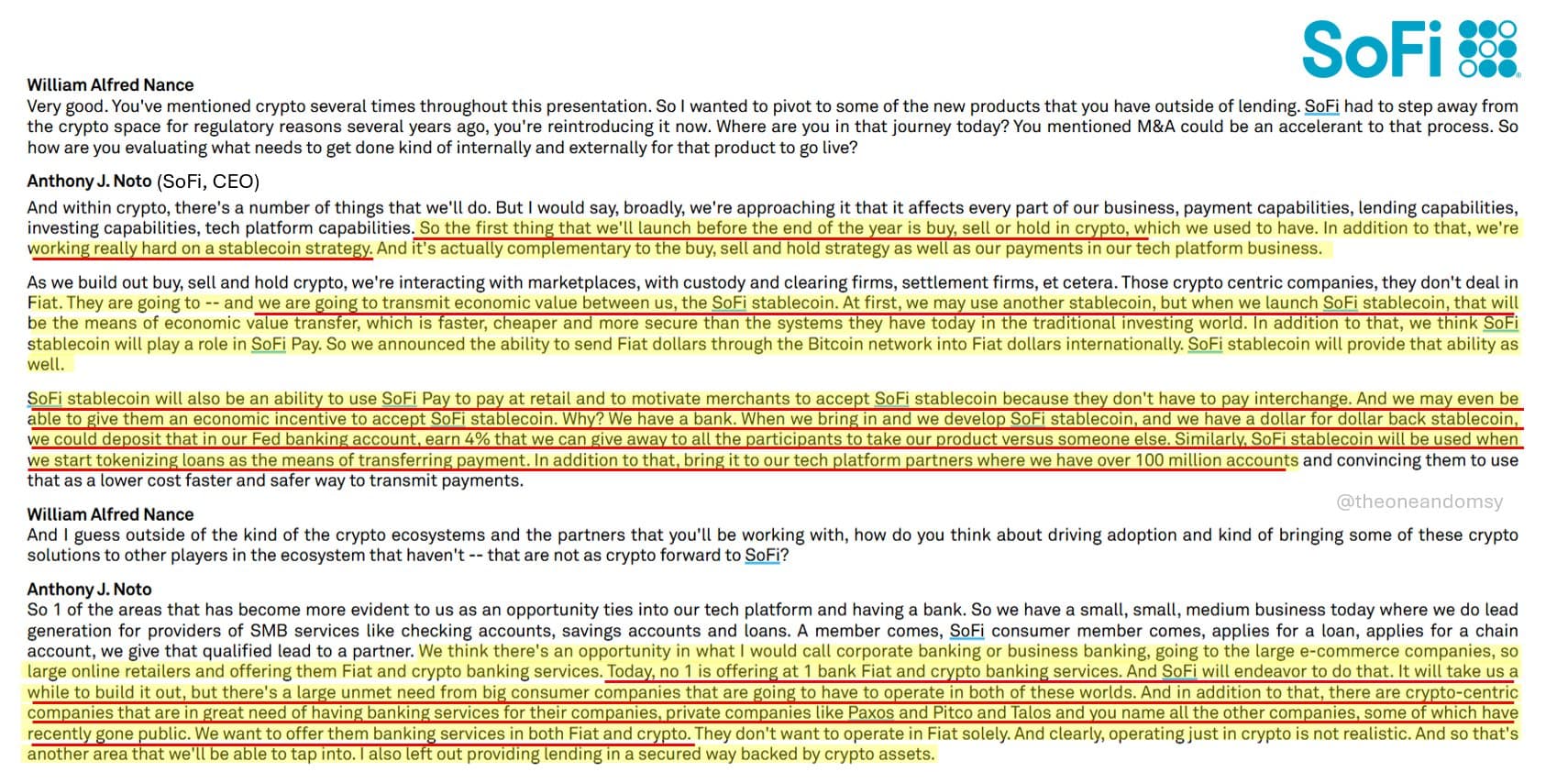

Sofilta voitanee odottaa kryptoihin liittyvää julkistusta lähiaikoina, sillä Sofi osallistui krypto-startup Zerohashin rahoituskierrokselle.

Myös Morgan Stanley osallistui kierrokselle ja he kommentoivat, että heillä pääsee käymään kauppaa kryptoilla (BTC, ETH ja SOL) H1 2026 aikana - Zerohash partnerin kautta.

Toivon, että Sofin käyttäjät pääsevät kryptojen pariin vielä tämän vuoden puolella, ja että valikoima olisi vähän laajempi mitä Morgan Stanley kommentoi heillä olevan. Ehkä kaikkia meemikolikoita ei pankin kannata alkaa tarjoamaan. Fartcoinit yms eivät kenties sovi yhteen Sofin “get your money right” sloganin kanssa

Alla on tviitti Sohvista ja kryptoista.

Yhtiö vie kryptosuunnitelmansa seuraavalle tasolle. Stablecoin on tulossa jäsenille vielä tänä vuonna ja sitä ajetaan SofiPayn kautta 4 prosentin tuotolla ja ilman interchange-kuluja, koska se on houkutteleva yhdistelmä sekä asiakkaille että kauppiaille.

Lisäksi rajat ylittävät maksut ja Galileon >100M tiliä luovat potentiaalia nopeaan skaalaamiseen. Retail-brokerage (yhtiön tauolla ollut osake- ja sijoituskaupankäyntipalvelu) palaa loppuvuodesta ja lainat kryptovakuuksia vastaan tuovat uusia tulovirtoja.

https://x.com/TheOneandOmsy/status/1972318132191760631

SoFi laajentaa alla olevan jutun mukaan sijoituspalveluitaan tuomalla käyttöön Options Level 1 -kaupankäynnin, joka mahdollistaa covered call- ja cash-secured put -strategiat (optiostrategioita).

Palvelu on ilman välityspalkkioita, lisäksi sisältää opetusta ja tarjoaa jäsenille keinoja hajauttaa, suojata ja kasvattaa tuottoja. Tämä laajennus vastaa sijoittajien kasvavaan kysyntään.

Looking ahead, SoFi plans to broaden its capabilities with additional options levels and strategies, options trading in IRAs, zero-day to expiration contracts, and enhanced tools for screening and profitability analysis.

Alla on linkki suhteellisen kattavaan Type-F Capitalin tuoreeseen analyysiin/rapsaan, joka nostaa esiin SoFin nykytilanteen: jäsen- ja tuotemäärät kasvavat edelleen yli 30 prosentin vuosivauhtia, mutta ristiinmyynti laahaa paikallaan 1,3 tuotteen tasolla per asiakas (muistin itse, että korkeampi) Tämä on hänen mukaansa selvä jarru – mutta toisaalta tietysti samalla myös suurin käyttämätön vipu.

Uutena kasvumoottorina raportissa korostuu lainausalustaliiketoiminta, joka on skaalautuva ja tuo pääomakevyttä tulovirtaa. Rapsas korostetaan myös, että luottotappiot pysyvät selvästi verrokkeja alempana, mikä vahvistaa riskiprofiilia.

Analyysi antaa edelleen selkeän nousuvaran käypään arvoon nähden, joten tilanne on ilmeisesti hänen mukaans mielenkiintoinen erityisesti niille, jotka pohtivat lisäyksiä tai holdaamista tässä vaiheessa. ![]()

"Report summary

SoFi is consistently performing better than peers while assuming less risk.

The one-stop-shop concept where members cross-sell into different financial

products has not materialized yet.

The lending business is a robust fortress.

Lending Platform Business (LPB) solves many of SoFi’s inherent problems and

will be a core revenue driver.

SoFi trades undervalued while demonstrating the characteristics of a high-

quality bank with impressive scaling levers."

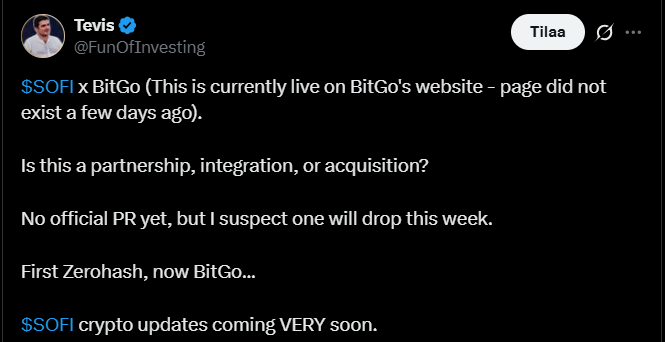

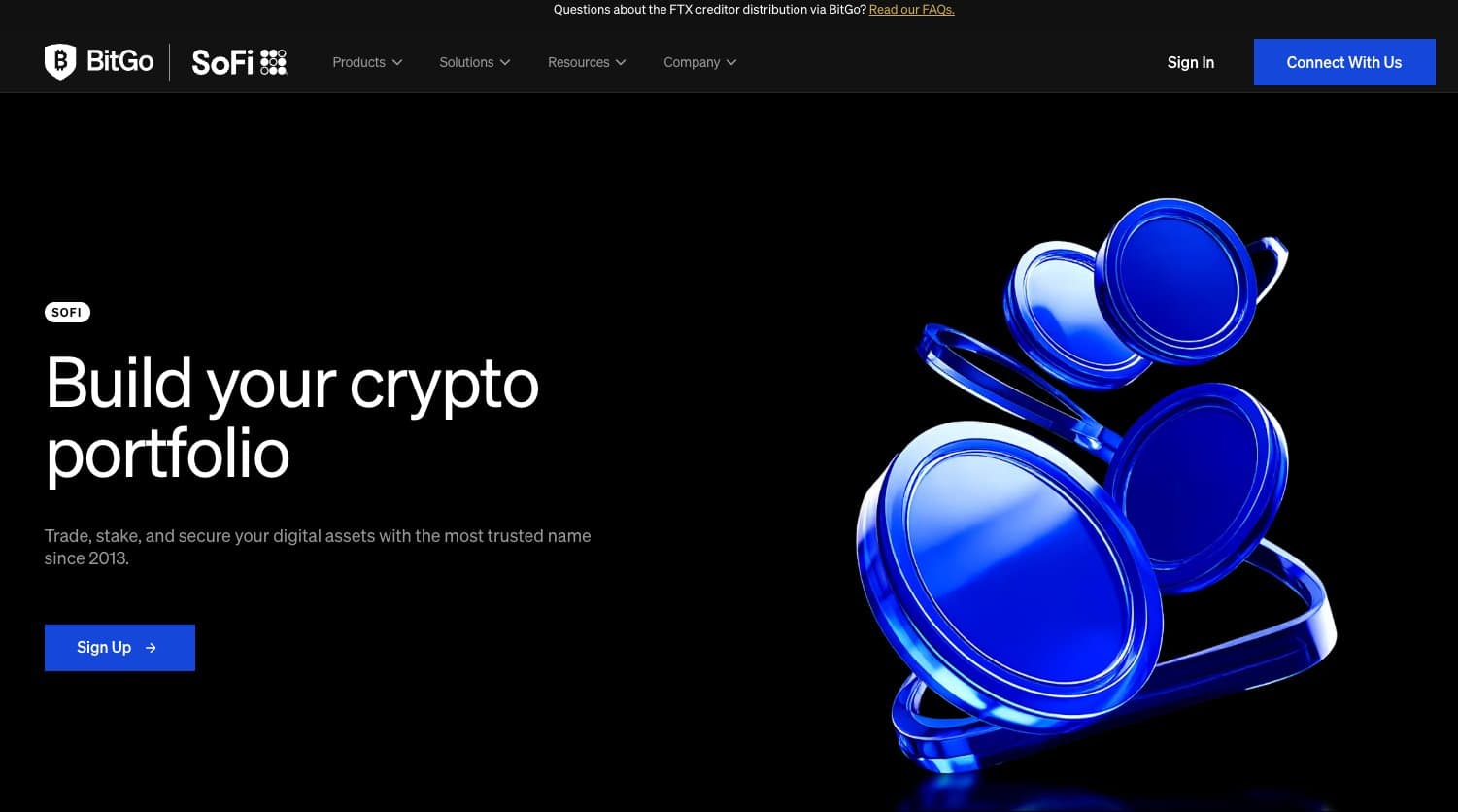

En ihan heti tajunnut, mutta tviitissä ehkä vihjataan, että SoFi ja BitGo ovat aloittaneet jonkinlaisen yhteistyön, joka näkyy jo BitGo:n sivuilla (BitGo on yhdysvaltalainen kryptopalveluyritys), vaikka mitään virallista tiedotetta ei ole edesjulkaistu.

Ei vielä tiedetä, onko kyse kumppanuudesta vai integraatiosta vai yritysostosta, mutta jotain uutista kai sijoittajat odottavat.

https://x.com/FunOfInvesting/status/1974909334657352145

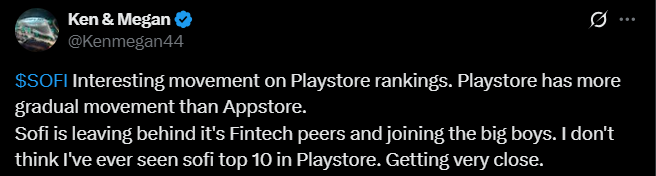

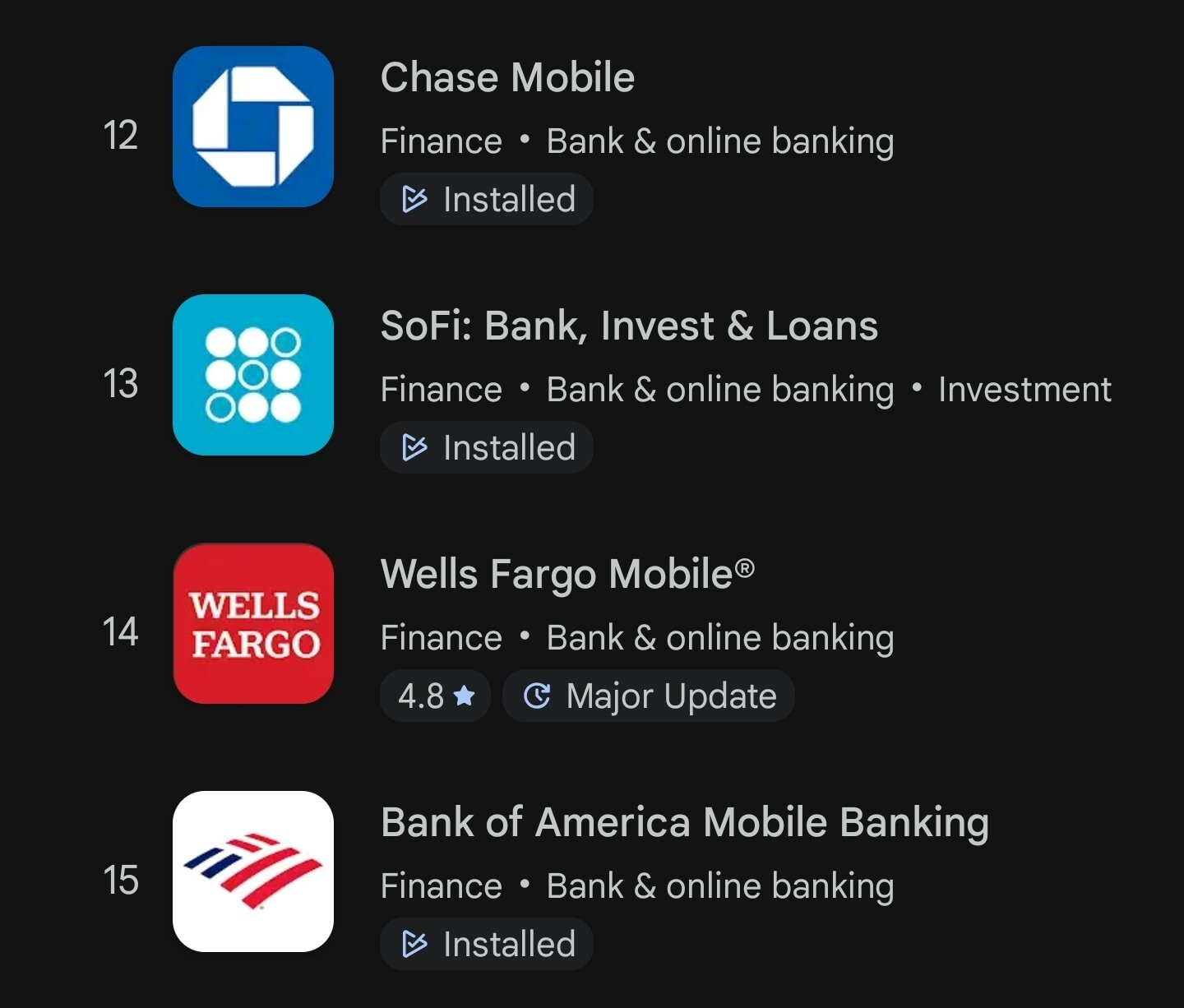

Sofi on noussut Google Playn pankkisovellusten kärkeen ja on lähestymässä isoja pankkeja, kuten Chasea ja Wells Fargoa.

Toisaalta tuossa pohditaan myös, että vaikuttavatko sovelluspäivitykset sijoituksiin ja sitä, että sijoitusten algoritmit ovat hämäriä ja vaikeasti ennustettavia.

https://x.com/Kenmegan44/status/1974864550651662707

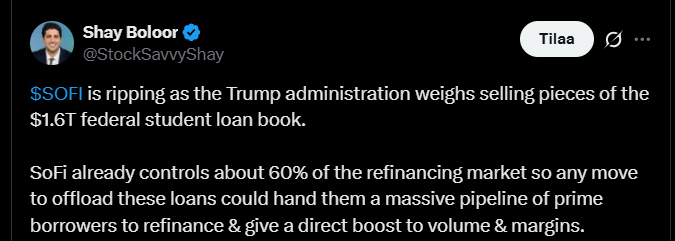

Laitetaan tännekin vielä, kun jo Kauhisteluketjuunkin laitoin. SoFi nousi tänään reippaasti ja tviitissä lienee syy sille:

https://x.com/StockSavvyShay/status/1975562157011149250

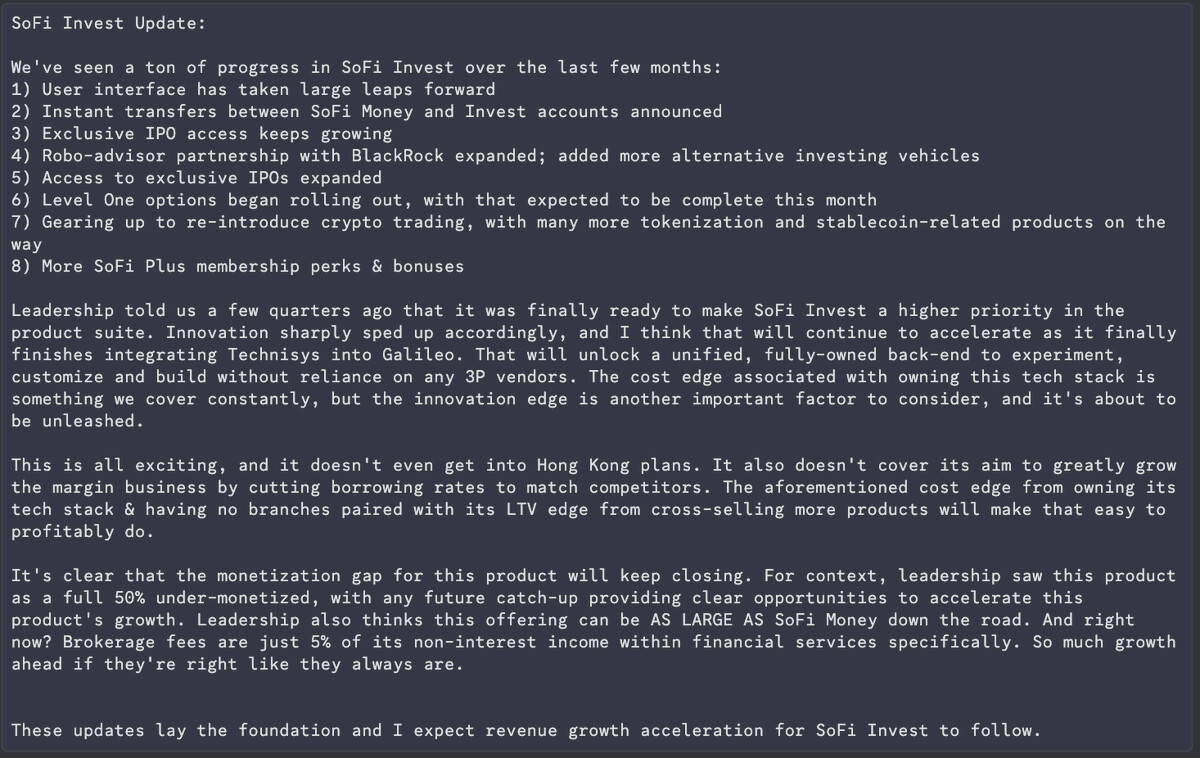

Tviitissä kerrotaan, miten SoFi Invest on ottanut isoja harppauksia viime kuukausina esim. käyttöliittymä on parantunut, siirrot SoFi Money -tileiltä onnistuvat nopeasti ja lisäksi yhteistyö BlackRockin kanssa tuo uusia sijoitusmahdollisuuksia. Myös osakeoptiot ja kryptovaluuttatuotteet ovat laajentumassa, mikä tekee alustasta entistä monipuolisemman.

Tviitissä kerrotaan, että johto panostaa nyt tosissaan Invest-palvelun kasvuun, koska sen odotetaan tuovan lisää tuloja sekä käyttäjiä. SoFin tavoitteena on tehdä sijoittamisesta helpompaa ja kilpailukykyisempää, koska se voi pitkällä aikavälillä kasvattaa sen asemaa finanssialalla merkittävästi.

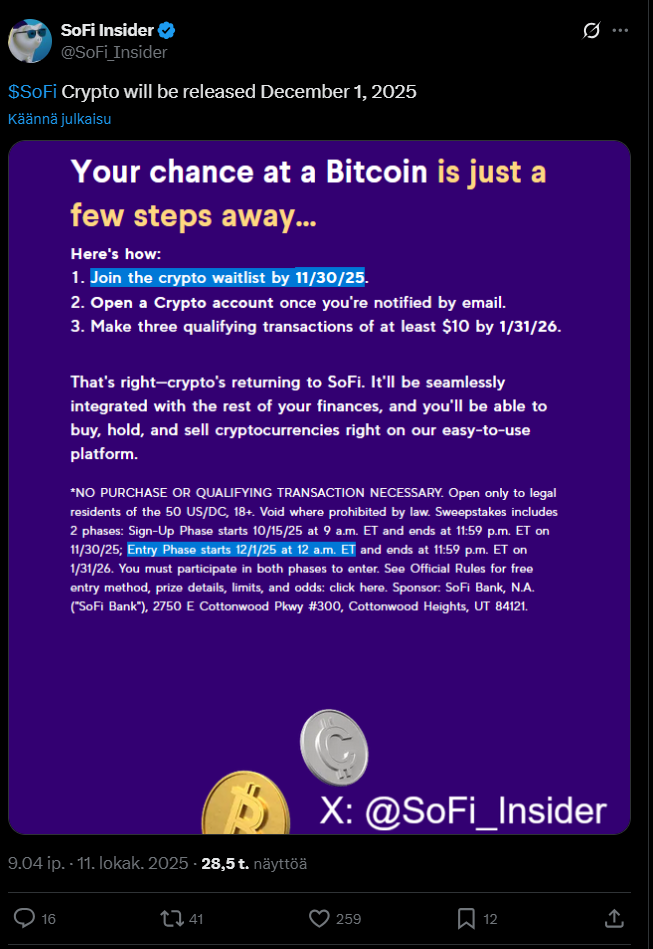

Vissiin SoFi tuo kryptovaluuttapalvelunsa takaisin 1.12.

Käyttäjät voivat liittyä kryptojen jonotuslistalle 30.11. mennessä ja tehdä kolme vähintään 10 dollarin toimeksiantoa tammikuun 2026 loppuun asti.

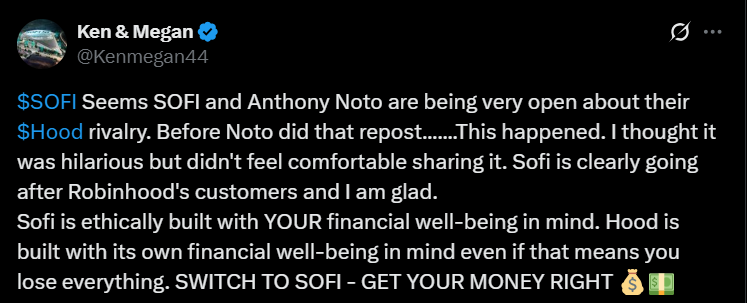

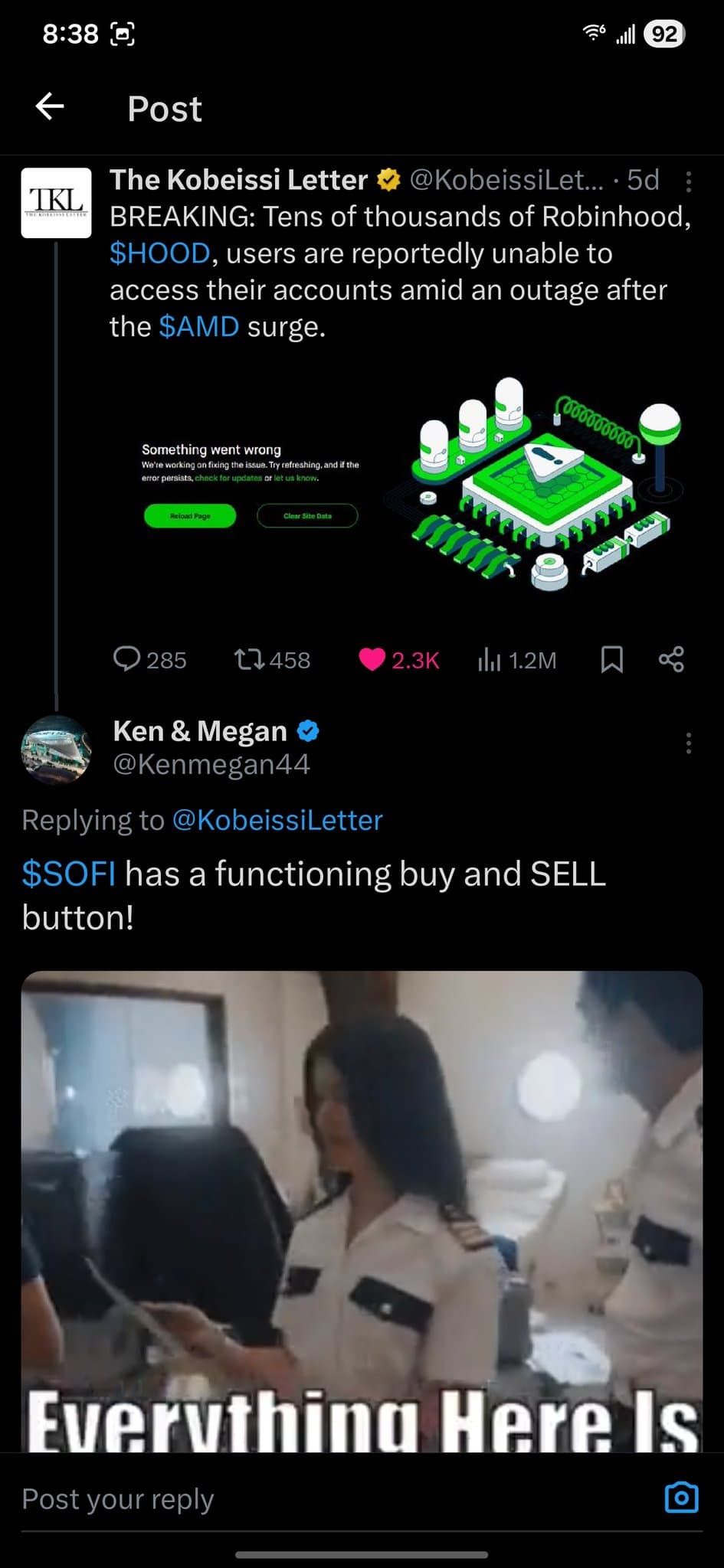

Alla olevassa tviitissä tuodaan esille, että SoFi näyttää hyödyntävän tilannetta, jossa “tutun kilpailijan” alustalla on ongelmia.

He korostavat omaa luotettavuuttaan ja asiakkaiden etua, kun taas toisen yhtiön koetaan ajavan lähinnä omaa etuaan. Yhtiön viesti on selvä; vaihda meille, me pidämme huolta rahoistasi. ![]()

https://x.com/Kenmegan44/status/1977393932976693363

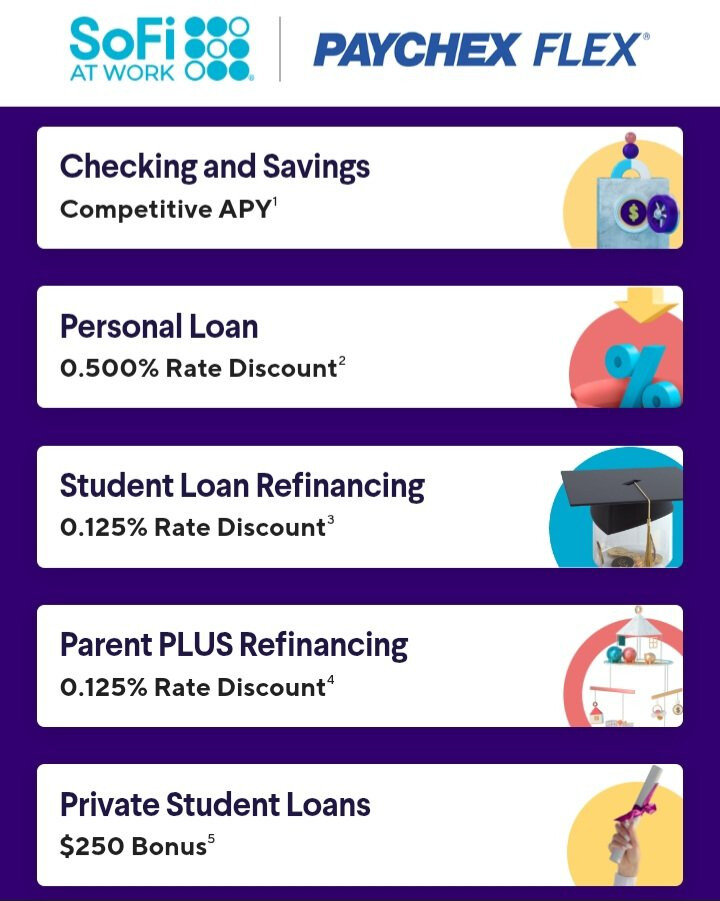

Tviitin pointti on kai se, että SoFi on laajentanut yhteistyötään Paychexin kanssa, eli nyt Paychex Flex -käyttäjät voivat hyödyntää SoFin pankki- ja lainatuotteita jonkun etuohjelman kautta.

Pitäisi olla kai hyvä uutinen SoFin asiakas- ja käyttäjämäärän kasvulle.

Tviittitilin nimeä katsoessa tulee mieleen, että pitää ottaa varovaisesti tämä tviitti. ![]()