When this was asked in the Coffee Room, then in this thread we can chat about investment taxation, and possibly, for example, the taxation of a limited company (Oy) ![]()

10 Likes

I wrote an answer in the “Coffee Room” section to @Taloudellinen_Ajatte’s question about value-added taxes (VAT). Here it is again:

If a limited company (Oy) sells VAT-liable services, it must be registered for VAT. The tax authority considers investing and service sales as different business activities. You can deduct VAT from purchases from the VAT of service sales if the purchase directly relates to the service sales. General overhead purchases (e.g., a computer used in both business activities) can be deducted according to the relative proportions of the business activities. The relative proportions can be determined, for example, by the ratio of working hours used. So, if you spend 90% of your working time on service sales and 10% on investing, then 90% of the VAT from the computer purchase can be deducted from the VAT on sales.

4 Likes

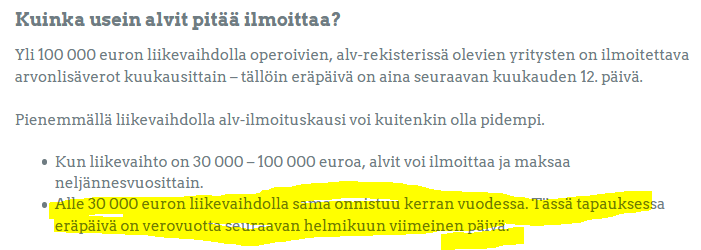

Thanks for the answer. So, in practice, belonging to the VAT register is mandatory if one wants to sell services. In small-scale businesses, how do VAT remittances to the state work; is it annually or more often? What about VAT refunds if purchases have exceeded the VAT accumulated from the sale of services? Does the tax authority automatically refund VAT, or does one have to apply for a refund separately?

There is an exception. A company with an annual turnover of less than 10,000 euros is not obliged to pay value-added tax.

1 Like

But it can still be invoiced? I also found an answer there regarding VAT payments, which is once a year if the turnover was less than 30k euros. All in all, a good link, thank you!

Does anyone know how the Finnish tax authorities treat US Master Limited Partnerships (MLPs)? They pay Limited Partnership distributions instead of dividends. Does the taxation go like with US dividends, or how? ![]()

EDIT:

The Osinkokone blog actually had an article about this topic.

http://www.osinkokone.com/2016/10/05/lmlp-etn-lahes-15-osinkotuottoa-kuukausittain/

EDIT2:

If I understood correctly, the “income distribution yield” distributed by LP companies is counted as earned income.

1 Like

Are there other people here investing through a company besides Medifilm mogul @Johannes_Sippola?

I was pondering setting up a company for real estate investing and it occurred to me that it’s probably worth thinking about this as a whole, where all investment assets would be accumulated for the company. I did some googling on the topic and it seems there’s very little sensible popularized writing on the subject, whether it’s about setting up a company for real estate investing, stock investing, or both asset classes.

Can you advise on where to start and what are the easy pros and cons to focus on?

I’ve been investing sporadically through my company for about twenty years and half-time for a few years. For risk management, I’ve divided capital about 1/3 to the company, 1/3 to myself, and 1/3 to family. Taxation in Finland is also erratic, and with current tax laws, one cannot plan decades ahead. That’s another reason why I don’t put everything into the company.

Already at the company formation stage, it’s good to decide whether you’ll leave the company as an inheritance to future generations, take future generations as co-owners, siphon off all profits for yourself, or distribute them to charity.

If your capital is substantial, enlist a tax consultant to help with the setup. Or perhaps even otherwise. Calling a consultant is still free.

Pros of a company:

- For now, slightly lighter taxation

- Share appreciation is not taxable income unless sold

- E.g., futures can be traded tax-efficiently outside the EEA

Cons of a company:

- Funds in the company are not fully liquid for tax reasons.

- Bookkeeping costs 1000-2000 EUR/year when outsourced. Do bookkeeping only once a year, as you don’t need monthly reporting. Talenom TiliJaska is worth checking out. I’m very interested in what they would offer an investment company.

- Investment activities are not subject to VAT. You cannot deduct VAT on purchases from anything. Conversely, in personal taxation, investment expenses are mostly fully deductible as income acquisition costs if you are primarily an investor by profession.

- Auditing costs 500-1000 EUR/year. In a limited company, auditing is mandatory if two or three of these conditions are met: 1) the balance sheet total exceeds 100,000 euros, 2) turnover exceeds 200,000 euros, 3) more than 3 employees.

- Banks charge higher service fees from companies than from individuals. Look carefully at which bank you want to be a customer of. Be prepared that banks are not very interested in you.

- Stockbrokers require annual reports from companies to prevent money laundering. This takes at least a couple of hours a year.

- A company needs an LEI code. This costs 37.20 EUR/year.

- Opening an account with a bank and a broker is slow. Be prepared for a two-month delay.

- All sorts of salespeople harass you by phone more than usual. Hide your company online.

36 Likes

First, thank you for the good information package! Could you tell me how transferring a stock portfolio to a company’s name works in practice? What kind of fees, for example, does NN charge for the operation?

The goal is to establish a company after my studies to generate side income, so I’ve been considering whether to transfer investments there or just invest new capital through the company. Thanks in advance!

I have only invested money into my own company. You can subscribe for shares in your own company with shares from other companies (apport).

I work through my own company and invest the extra money in apartments and stocks. It’s more pleasant to pay 20% income tax and then invest than to pay income tax first.

It’s important to consider all costs. Every year, you have to pay a Lei fee of about 37€. Banks really don’t want investment companies as clients. As far as I understand, Nordea is the cheapest bank where you can open a mandatory current account for a company, costing a little over 12€ per month. Of course, it depends on the amount of capital the company invests, but it’s not worth investing very small sums through a company. Then, if you have a slightly larger limited company, an audit is mandatory. I handle the bookkeeping myself, which is really easy to do if you trade a reasonable amount. Every investor must calculate for themselves with what amount of capital all costs are less than the tax benefit.

The plus, of course, is lighter taxation, especially if you don’t withdraw funds from the limited company but reinvest them. I personally feel that an investment company is somewhere between a traditional securities account and an equity savings account in terms of its features. A slightly wealthier long-term investor should set up an investment company when the deposit limit for their equity savings account has been reached.

3 Likes

I came across this ad on Facebook:

On Wednesday, December 9, 2020, from 1:00 PM to 2:00 PM, Rantalainen is organizing a webinar on the topic of Investment Companies in Taxation. The webinar is part 2 of the “Opportunities in Tax Planning” series.

Are you considering setting up an investment company? What benefits can be gained by investing through an investment company? Or would it be more sensible to invest directly as a personal holding? How does taxation work in these alternatives? We will discuss investment options through an investment company and through personal ownership, and provide more detailed information on the tax aspects related to these alternatives.

In the webinar, you will learn:

- the concept of an investment company

- conducting investment activities through a limited company

- establishing an investment company

- investing as a private individual

- tax aspects and differences of the alternatives

Expert introduction:

Senior Tax Manager, Hannu Heinonsalmi, works as an expert in corporate restructuring, mergers and acquisitions, and generational changes in Rantalainen’s expert services. Hannu has extensive experience in tax planning. Hannu’s special expertise includes corporate restructuring and mergers and acquisitions.

Tax Specialist, BBA, KLT Juho Heikkinen, works as an expert in taxation and corporate restructuring in Rantalainen’s expert services. Juho has over 10 years of work experience in the taxation of various company forms and specific issues in accounting.

7 Likes

Even though the discussion has turned to companies, I dare to ask a question concerning the taxation of a natural person’s capital income, or rather, deductions from taxable capital income. More specifically, the timing of deductible expenses in relation to the timing of the deduction.

A seemingly complex question with a simple example:

Person H puts a small sum of money into indexes every month. Has been doing so for years. The question is about monthly savings into accumulating ETFs, so the activity practically requires no resources (time, place, equipment) and does not generate capital income.

In late 2018, H acquires a new desktop computer and a huge new monitor, with the idea of utilizing them in a planned construction project.

In late 2019, H acquires a new laptop and a new smartphone with a large screen. No specific focused use case had been considered for either at the time of purchase.

The coronavirus dip causes H some kind of stroke. First, all ETFs are sold, then some trading is done with similar products for a while, until the portfolio is emptied of all funds and investing directly in stocks begins.

In late 2020, we look back a bit…

There are easily three-digit stock trades behind H. Dividends have been received from some tens of companies, and capital gains, after losses, have materialized into a five-digit figure, meaning H will, at the latest in January 2021, get to pay taxes on the capital side as well. Both sales and purchases have been made with a sum significantly larger than earned income.

But then to the deductions… H considers himself an irreproachable “sensible citizen.” You shouldn’t cheat, but who would want to pay extra taxes? So, the relationship between the events of the quarantine year and taxation makes one wonder…

The desktop computer assembled in 2018 has been dedicated to investment activities since winter 2020. And that’s not all, the entire room where it is located is Out of Bounds, for example, for the children. It is a space intended for Dad’s “second job.” Approximately 80% of the use of the phone purchased in 2019, in terms of time, is related to investing (surfing on Inderes naturally takes up most of the time, but a significant portion of trading is also done via the phone), and the 2019 laptop also gets its share, meaning roughly half of its use is related to investing activities.

If the newer games, gadgets, and bells and whistles had been purchased in the last six months, the answer would be clear. The whole lot for tax deductions.

But what about when the acquisitions were made slightly before the start of active investment activities… during the tax years 2018 and 2019. Is it possible to propose deductions for these?

Of course, the taxation of the aforementioned tax years could be requested to be fully reopened, but at that time, investment activities were not active churning, so claiming deductions on that basis would be at least questionable.

But if we are completely honest. Is equipment purchased in December 2019, which is put into investment use in March 2020, deductible in the 2020 taxation, and if so, how?

4 Likes

Here it is clearly stated that you can deduct the purchase price of a computer under 1000 euros all at once in the year of purchase.

https://www.vero.fi/henkiloasiakkaat/verokortti-ja-veroilmoitus/tulot-ja-vahennykset/tulonhankkimismenot/tietokoneet/

Additionally, it is written there:

Start the deduction in the year of acquisition of the item. In the year when the item is no longer used for income generation, the depreciation is not deductible in taxation.

The acquisition cost of a computer is deducted with 25% annual declining balance depreciations.

Strictly interpreted, hardware purchased in December 2019 for at least 1000 euros, which is taken into investment use in March 2020, would only be subject to a declining balance depreciation of 75% in the 2020 taxation. I recommend calling the tax office to verify the matter.

![]()

1 Like

When investing in rental properties, if an invoice is not actually sent on the due date, should unpaid rental receivables still be recorded as receivables in the financial statements? Or as income when they are paid?

Thanks @MoneyWalker for a very informative post!

My own idea is somewhat similar when it comes to diversification. The goal would be to invest as both an individual and an entrepreneur to protect against the negative effects of tax policy.

Over the weekend, I was thinking about a package like this:

Mauri as an individual:

- Gets cheaper loans as a private customer

- Monthly invests salary income in stocks with a buy-and-hold approach

- Invests as an individual in older housing shares with a buy, renovate, rent, refinance strategy

Mauri’s investment company:

- Gets expensive loans as a corporate customer

- Occasionally invests in stocks with a buy-and-hold approach

- Invests in new construction with large housing company loans (reduces the need for expensive corporate loans) or in older housing shares with a buy, renovate, sell strategy

Initially, there probably isn’t much benefit to setting up a company. More likely, it’s a disadvantage as time is spent on running it, fees accumulate, and loans are expensive. However, when considering the matter over decades, investing through a company can be quite sensible and cost-effective in a long-term and ambitious investment plan.

A couple of questions:

- What are the most sensible ways to transfer capital to a company? Capital loans have been discussed in a positive light, at least.

- How much does the bank consider the overall tax burden of the company and the private customer in a lending situation (e.g., a situation where the company has a couple of apartments with housing company loans with high leverage, and the private customer applies for a loan for a new investment apartment, or vice versa)?

- Where can I find more information on the subject?

That Rantalainen webinar tip seems interesting, thanks @T3r00!

1 Like

Fundamentally, all such items should be recorded as receivables based on the invoice date, or in this case, I would say the due date.

If there is a credit loss, that loss can be deducted in the following year’s taxation.

Unpaid rental invoices are recorded as deferred receivables in the financial statements. If, in your discretion, it is probable that you will not receive payment for the rent, a mandatory provision is made, which can be deducted as an expense for tax purposes only when it is clear that the money will not be received. However, this can also be recorded as a bad debt, but one must be a bit more careful with its recording, as it can be immediately deducted as an expense for tax purposes. This means that the income is recorded in the financial statements on an accrual basis, meaning the rental income is recognized in the results of the ended financial period. The timing of the invoice payment has no significance for the income statement.

1 Like

If your intention is also to withdraw dividends from your investment company, SVOP (Shareholder’s Equity Fund) funding is a better tax-wise option than a shareholder loan. SVOP funding increases net assets, while a loan decreases them. You can also withdraw funds from SVOP funding, as long as you do so within 10 years and can prove that you originally invested the funds in the SVOP.

3 Likes